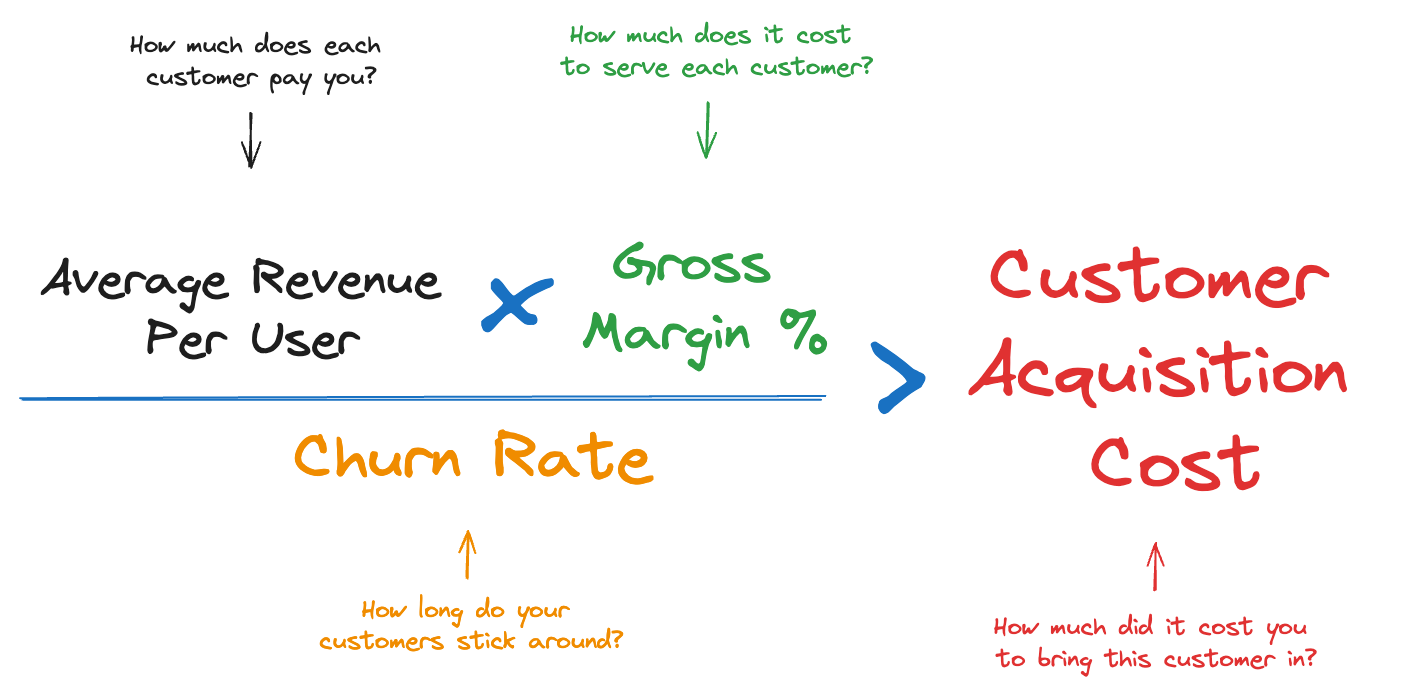

This isn’t some theoretical construct. It’s the law of gravity for software businesses. Violate it for long enough and you die. The only exception is if you’re being subsidized by venture capital, which is really just dying on a delayed schedule if you never fix the math.

For the past fifteen years, this equation has been remarkably favorable to software companies. Gross margins of 80%+ were normal. Once you built the software, the cost of serving each additional customer was negligible. That’s what made SaaS such an attractive business model.

AI is about to break this equation from multiple directions at once.

The most obvious pressure is on gross margin. To stay competitive, you need to add AI features. But AI features have real marginal costs. Every query hits an API that charges by the token. Unlike traditional software, where the millionth user costs almost nothing to serve, AI-powered software has costs that scale with usage.

You can try to absorb this and watch your margins compress. Or you can pass the cost to customers and watch them leave for competitors who are willing to subsidize it. Neither option is good.

But the margin pressure is actually the least interesting part of what’s happening.

The more existential threat is to LTV itself. And it’s coming from an unexpected direction: your customers might just build their own version of your product.

Not all of them. But enough of them.

We’re entering an era where a reasonably technical person can describe what they want and get working software back. Not perfect software. Not enterprise-grade software. But software that solves 70% of the problem they were paying you to solve.

This is a new kind of competition. It’s not a startup trying to take your market. It’s your own customers realizing they might not need you.

The traditional response to competition is to add more features, to move upmarket, to build a moat through complexity. But that playbook assumes your competitor is another company that also has to deal with the costs and coordination problems of building software. When your competitor is your customer with a weekend and a chat interface, the dynamics are completely different.

The third piece of the equation is CAC, and here the picture is genuinely uncertain.

There’s a case that CAC goes down. AI makes content cheaper to produce. Outbound can be more automated. You can build sophisticated product-led growth funnels faster.

But there’s also a case that CAC goes up, and I think this case is underrated.

When everyone can produce content at near-zero cost, channels get saturated. Google is already drowning in AI-generated content of dubious quality. Standing out in a sea of noise requires more effort, not less.

There’s also a trust problem. When anyone can spin up a plausible-looking SaaS product in a weekend, being a real company with a real track record actually matters more. But building that trust takes time and money. The cost of acquiring a customer who actually believes you’ll be around next year might be higher than it used to be.

And here’s the really uncomfortable part: if a potential customer can vibe code 70% of your product themselves, your marketing now has to justify why the remaining 30% is worth paying for. That’s a harder sale. Harder sales mean more touches, more demos, more effort per conversion.

So we have:

Gross margins compressing due to AI costs

LTV under pressure from both pricing competition and customers building their own alternatives

CAC potentially rising due to channel saturation and higher trust requirements

When all three variables move against you simultaneously, a lot of businesses that looked healthy are suddenly underwater. Not because they did anything wrong, but because the environment changed.

I don’t have a neat answer. The honest answer is that a lot of companies won’t.

People will say moats still matter—data network effects, deep integrations, regulatory expertise. And those things do help. But they help at the margins. If all three variables in your fundamental equation are moving against you simultaneously, a slightly better moat just means you die slower.

The math is unforgiving. When gross margins compress, LTV drops, and CAC rises all at once, you don’t get a graceful decline. You get a cliff. Companies that looked healthy twelve months ago will be underwater twelve months from now. Not because they made mistakes, but because the environment changed and their business model stopped working.

This isn’t a situation where the smart founders adapt and the dumb ones fail. Some businesses were just built on assumptions—about margins, about what customers would pay for, about the cost of alternatives—that are no longer true. You can be smart and still be standing in the wrong place when the ground shifts..

The SaaS unit economics of the past were a product of a particular moment: building software was expensive, distributing it was cheap, and marginal costs were near zero. That moment is ending.

Thanks to the conversations that sparked this essay, particularly Enterprise AI Trends