I fucking hate filing my taxes.

This year I have fifteen 1099s. I also have a W-2 from my former day job, investment accounts, a home office deduction, quarterly estimated payments I may or may not have calculated correctly (spoiler: I did not), and the distinct sense that I am one misplaced decimal away from an audit.

I’m also a certified financial planner. I literally do this for a living — or at least a version of this. I help people understand their money. I write about financial systems. And every April, I sit down at my laptop with a shoebox of tax documents and the emotional composure of someone defusing a bomb.

This year, I decided to do two things differently. First, I was going to file my own taxes instead of paying an accountant. Which meant I would need to find a tax filing software, and embarked on a mission to find a company that wasn’t extremely corrupt.1

How hard could that be?

Very hard, it turns out. Borderline impossible.

I started where most people start: TurboTax. Intuit, TurboTax’s parent company, has spent more than $55 million on federal lobbying since 1998 — much of it aimed explicitly at preventing the IRS from creating a free filing system. They donated a million dollars to Trump’s inaugural committee. The FTC sued them for deceptive advertising. Multiple state attorneys general investigated them. They paid $141 million in settlements to customers who were tricked into paying for services that should have been free. So. No TurboTax.

H&R Block? Also lobbied against free filing. Also got sued by the FTC for deceptive marketing. Also got caught sharing sensitive taxpayer data with Meta and Google. Meta used that data to target ads. So. No H&R Block.

Jackson Hewitt? Owned by Corsair Capital, a private equity firm, since 2018. (If you read my piece on how everything is private equity, you’ll understand why I’m not interested!) Also a member of the trade group that lobbied to kill free filing. No.

TaxSlayer? Member of the same lobbying coalition. Also caught sharing taxpayer data with Meta and Google. No.

TaxAct? Owned by Cinven, a London-based private equity firm. Congressional investigators found they collected more taxpayer data than anyone previously reported and sent it to Meta, which confirmed using it to train AI algorithms. Absolutely not.

Cash App Taxes? Not a member of the lobbying coalition, no history of fighting Direct File, no data-sharing scandals, free for federal and state with no upsells. But … it’s owned by Block, Inc. (formerly Square), which also owns Afterpay — a buy now, pay later company — soooo … no.

At this point I’m running out of options and starting to feel like I’m in one of those nightmares where every door opens to the same room.

I ended up going with FreeTaxUSA — the internet’s darling. Reddit loves it. Personal finance TikTok loves it. It’s cheap (free federal filing, roughly $15 for state), and the interface doesn’t try to trick you into upgrading every thirty seconds. It felt like the one ethical option.

But, while reporting this piece, I found out it wasn’t.

FreeTaxUSA’s parent company, TaxHawk, is a confirmed member of the American Coalition for Taxpayer Rights — the same coalition that includes Intuit, H&R Block, Jackson Hewitt, and TaxSlayer. The coalition whose stated position is that the government should not offer free tax filing because the private sector does it better.

I had already filed by the time I learned this, and wanted to scream into the nearest pillow. Taxes are one of the biggest financial constants in our lives — death and taxes, the whole bit — and I couldn’t even get through the filing part without accidentally funding the machinery that keeps filing miserable.

Before we get into who made it this way (we will, I promise), it’s worth understanding what makes the American tax system such an outlier. Because the US isn’t the single hardest system on earth. But among other wealthy democracies, it puts more burden on individual taxpayers than almost anyone else.

Start with the structure itself. Most developed countries rely on a national consumption tax — a VAT — as the backbone of their revenue system. The US doesn’t have one. Instead, we layer federal income tax on top of state income tax (which varies wildly — some states have none, others take over 13%), on top of local income taxes in some cities, on top of payroll taxes, capital gains taxes, estate taxes, sales taxes that differ by municipality, and property taxes set at the county level.

Other countries also deliver social benefits through direct spending — the government writes you a check, provides a service, funds a program. The US does this too, but it also does something unusual: it buries an enormous amount of social policy inside the tax code.

This is because it’s politically easier to pass what looks like a tax cut rather than a new government program. And it shifts the burden to the individual — you have to know the benefit exists, figure out if you qualify, and actively claim it (often with professional help).

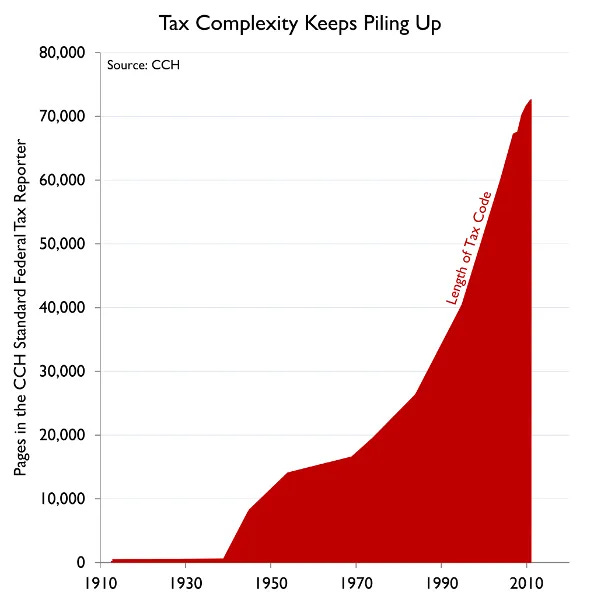

Any U.S. tax provision likely has a constituency that lobbied for it and will fight to keep it. That’s why simplification efforts in Congress almost always die. The tax code is 4 million words long. With regulations, it’s over 10 million. And it keeps growing because cutting anything out is often politically harder than adding something new.

So that’s the code. But then … there’s the filing process itself.

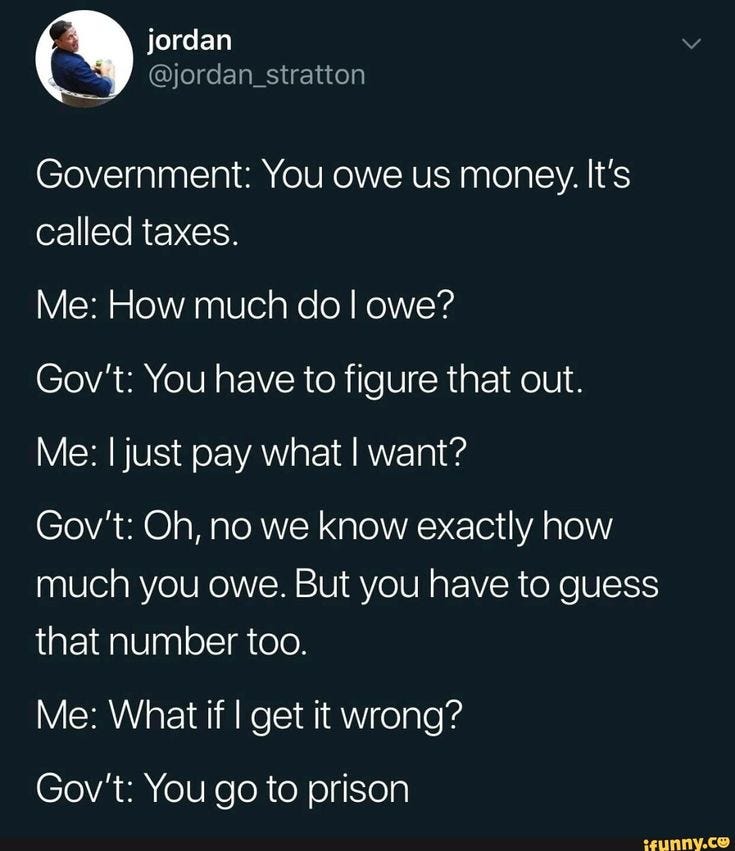

So this is only … partly true. The IRS knows a lot of things about you, but it doesn’t know everything.

Your employer sends the IRS your W-2, your bank sends them your 1099-INT, and so on. When you get a number wrong on your return, the IRS sends you a letter with the correct amount.

But the IRS doesn’t know your childcare expenses, your charitable donations, your business deductions, or whether you’re claiming the home office in your apartment. For self-employed people, itemizers, and anyone with a pretty complicated financial life, the IRS can’t figure out how much you owe without some extra input from you.

Most people have objectively simple taxes. Around 90% of taxpayers take the standard deduction. So for them, the IRS already has almost everything it needs.

And this is where the American system starts to look less like a policy problem and more like a choice.

A 2022 study found that the IRS could auto-fill nearly half of taxpayer returns, which would save people (specifically younger people and lower-income people) time and money on their taxes.

Many other developed countries already do this.

In Sweden, the tax authority pre-fills your return and sends it to your phone. If it looks right, you text a confirmation code to a five-digit number. In the Netherlands, you’d go online, check to make sure the government filled out everything correctly, and then click “OK”. In Japan, most employees never file at all — your employer handles everything through a year-end adjustment. You get a postcard telling you what you earned and what your refund will be.

So why does the US make roughly 150 million households do their own math every year?2

Part of it is the complexity of the tax code, sure. But there’s also the tax prep industry itself — AKA companies that have spent decades lobbying to keep filing complicated, because their entire business model depends on you not being able to do it yourself.

Tiktok failed to load.

Tiktok failed to load.

Enable 3rd party cookies or use another browser

Intuit — the company that owns TurboTax — has spent more than $55 million on federal lobbying since 1998. H&R Block has spent tens of millions more. Together with Jackson Hewitt, TaxSlayer, and the rest of the industry’s trade coalition, they’ve poured over $93 million into federal lobbying since 2003. Intuit alone employed 55 lobbyists at their peak — 41 of them through the revolving door from government jobs.

The target of all that money: any attempt by the government to let you file for free.

It started in 2002, when the Bush administration proposed a free online filing option. Intuit’s lobbyists killed it and replaced it with the Free File Alliance — a public-private partnership where the companies would offer free filing to lower-income taxpayers. In exchange, the IRS agreed not to build its own tax filing system.

The tax software companies then made the free option nearly impossible to find on their platforms. Intuit and H&R Block added code to their websites to hide their Free File pages from Google. A Treasury Inspector General audit found 14 million Americans paid for tax prep that should have been free.

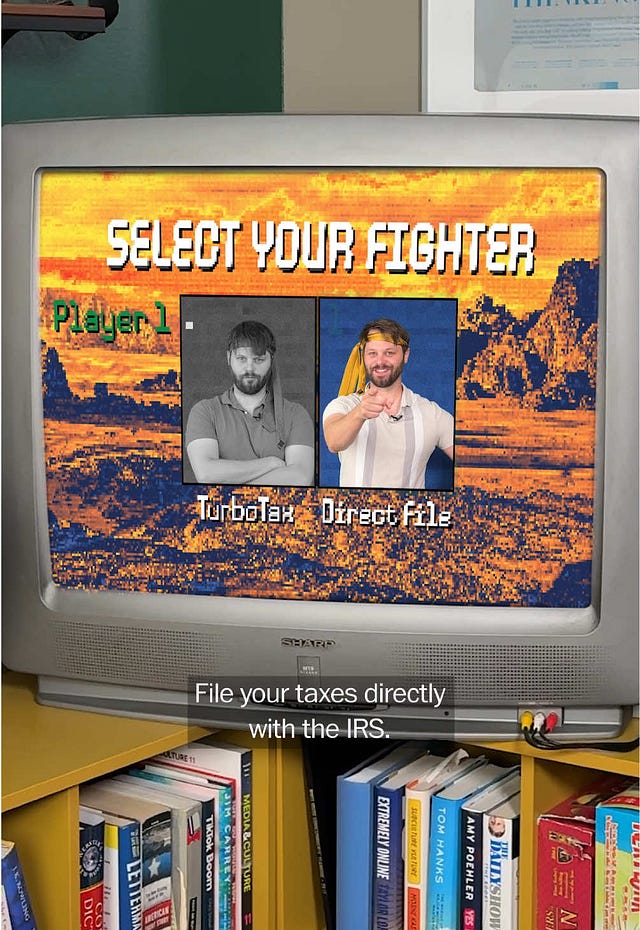

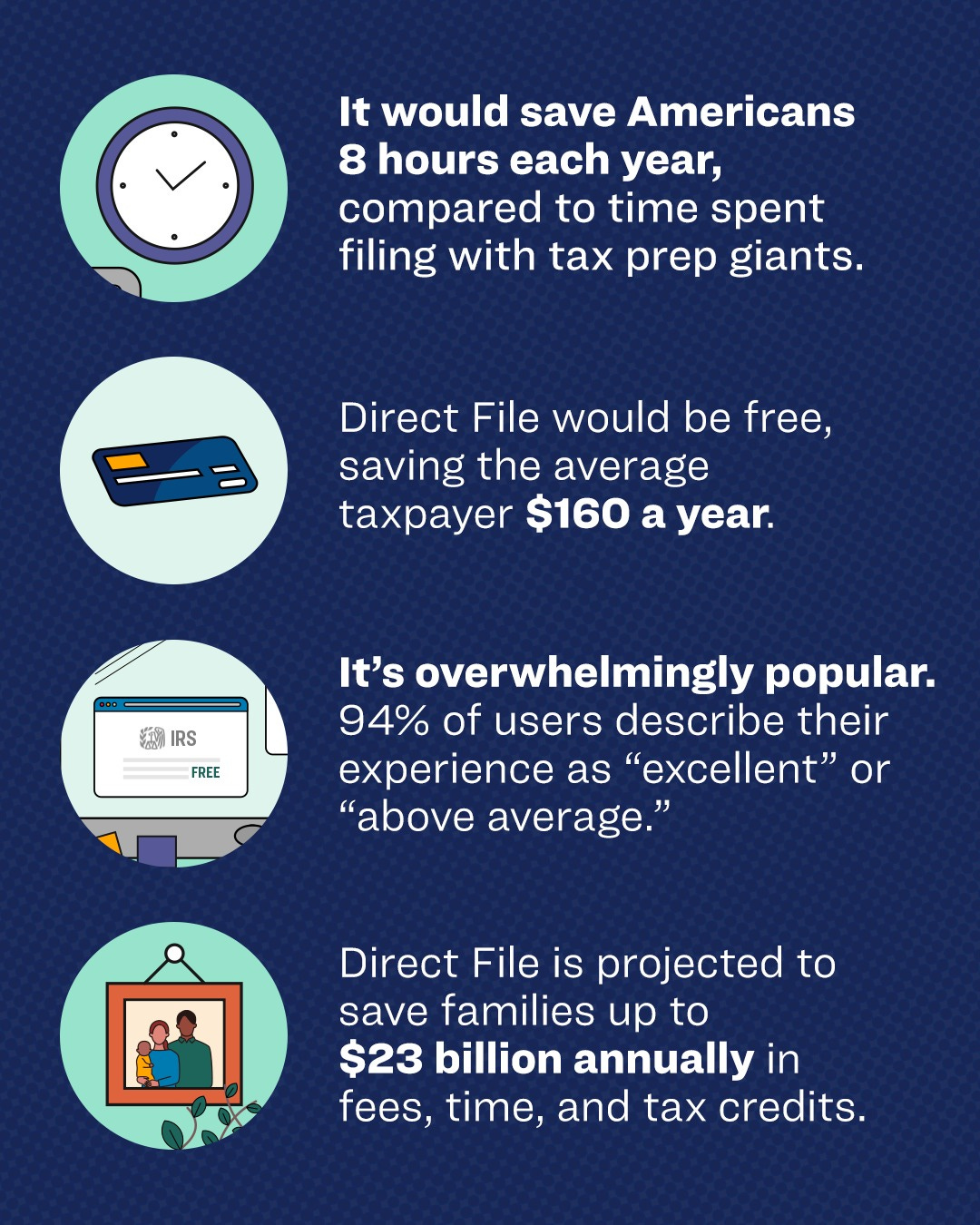

In 2024, the IRS launched Direct File: free, government-run, funded by the Inflation Reduction Act. It started as a pilot project in 12 states. It had an over 90% satisfaction rating. Nearly 300,000 people used it.

In December 2024, 29 House Republicans wrote to Trump asking him to end it. Twenty-seven of those 29 had received a combined $1.8 million from Intuit, H&R Block, and the industry coalition. In March 2025, DOGE gutted the team that built it. By November, the program was dead. Its webpage now returns a 404.

Why, you ask? In the words of our current Treasury Secretary Bessent: “The private sector can do a better job.”

Direct File cost roughly $41 million a year. Intuit received $94 million in federal research tax credits in a single year. So, essentially, company that helped kill free filing got more than double its cost in government subsidies.

This particular type of dysfunction feels very American to me.

I grew up in D.C. “No taxation without representation” was on every license plate. And while D.C.’s complaint is specific — we pay federal taxes with no voting representation in Congress — the phrase taps into something that runs through everything about how this country handles money.

America’s origin story is an anti-tax story. The Revolution wasn’t really about the amount being taxed. It was about consent — about who gets to impose those taxes. That made anti-tax sentiment patriotic in a way that doesn’t really have an equivalent in Scandinavia or Japan, where taxation is understood more straightforwardly as the price of a functioning country.

That instinct shaped everything that came after. The US was one of the last industrialized nations to adopt a federal income tax. And the political fragility of taxation is a big reason why the code is so full of carve-outs: it’s always been easier to add a deduction than to simplify rates, because simplification means someone loses a break, and the anti-tax reflex means that loss becomes “the government is taking more from you.”

So the code grows but never shrinks. Every social policy goal — homeownership, kids, education, retirement, clean energy — gets routed through the tax system because Congress often won’t pass the direct spending version. And then the complexity becomes its own argument: See? The government can’t make this simple. Better let the private sector handle it.

You earn money. The government takes some through withholding. You pay a private company $50 to $200 (or way more) to figure out whether the government took the right amount. That company uses part of your payment to lobby the government to make sure you keep needing them. The government plays along because the company funds campaigns and hires its former employees.

And next April, it starts again.

This is a form of manufactured helplessness, and. I believe it’s one of the defining features of how money works right now. The financial system is full of problems that have been engineered to require paid intermediaries, and then the intermediaries spend money to make sure the problems don’t get solved.

You can see this in health insurance, credit cards, the retirement system, hombuying, student loans. The pattern is often the same: Make the system complex enough that navigating it feels impossible without help, then sell the help, then lobby to keep the system complex.

And the psychological cost of living inside that pattern — the ambient sense that you are always one missed step away from getting screwed — is what I think drives so much of the financial nihilism and anxiety I write about. (Earlier this year I wrote about how living in a low-trust society is bad for our society and economy).

And in many cases, the complexity is very much designed to redistribute upward.

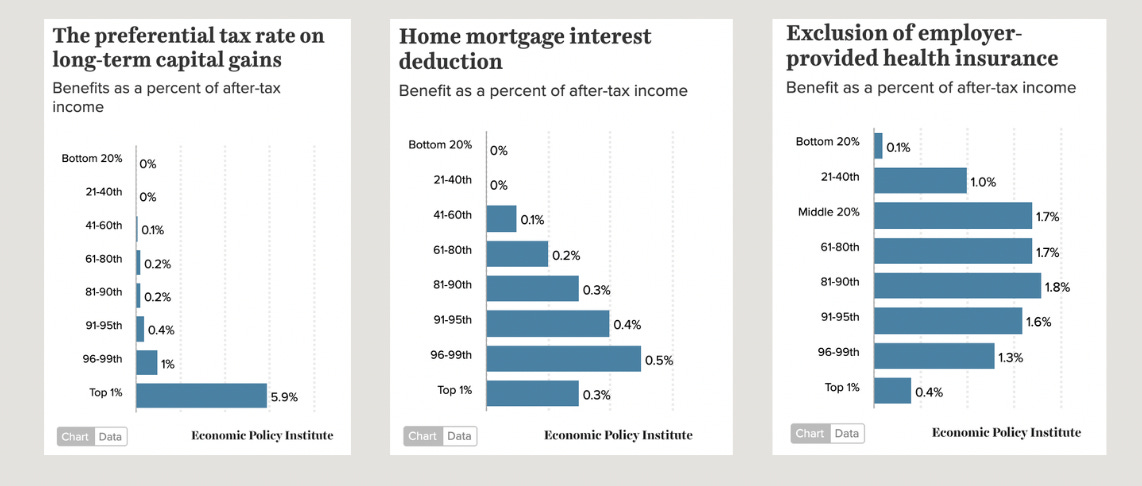

We talk about welfare in this country like its food stamps and Medicaid. But the biggest welfare program in America is the tax code, through the tax deductions, credits, and exemptions that disproportionately benefit rich people:

Many tax benefits scale with income. The mortgage interest deduction saves you nothing if you rent, a little if you own a modest home, and a lot if you own an expensive one. Same with the deduction for employer-sponsored health insurance, retirement account contributions, and capital gains tax rates — the more you earn and own, the more you benefit.

Many of these tax benefits require you to itemize, which most lower-income filers don’t do. So the benefit technically exists for everyone but functionally flows upward.

The tax code is generous with incentives to buy property, invest in the market, and save in tax-advantaged accounts — things that require disposable income in the first place. Meanwhile, the direct spending programs that serve lower-income people (SNAP, housing vouchers) are means-tested, stigmatized, and chronically underfunded.

The people who benefit most from the tax code’s complexity are the ones who can pay someone to navigate it for them. Everyone else just absorbs the cost — the mental, financial, and time cost.

Which might explain why people — on both ends of the political spectrum — are starting to refuse.

In recent months, you’ve seen left-leaning protesters calling for tax resistance to avoid funding ICE deportations. You’ve seen Marjorie Taylor Greene (and other Republicans) endorse a “tax revolt” among Trump supporters over foreign aid spending. While these two groups don’t agree on much, they have arrived at a remarkably similar place.

I want to be clear about something, as a financial planner: I am not telling you to stop paying your taxes. If you are thinking of doing that, you need to be fully aware of the real and serious consequences (penalties, interest, liens, criminal prosecution, etc).

But, these movements signal to me that people are not just frustrated with how much they pay. They’re frustrated with a system that takes their money, makes the process of giving it miserable, offers no transparency about where it goes, and then uses the confusion to extract even more.

I started this piece trying to find an ethical way to file my taxes. I ended up with a map of a system that’s designed to make ethical choices invisible, exhausting, and just inconvenient enough that most people give up and go with the default. Which is, of course, the point.

Here’s what I’m doing about it. Take what’s useful, leave what’s not.

I’m talking about this! Most people I’ve mentioned Direct File to had never heard of it. They didn’t know it existed, they didn’t know it worked, and they definitely didn’t know it was killed by the same companies that charge them to file.

I’m calling my representative about the Direct File Act. In March 2026, over 160 lawmakers introduced the Direct File Act — legislation that would make Direct File permanent and prohibit the IRS from ever again agreeing not to offer free filing. It’s backed by organizations like Public Citizen, Americans for Tax Fairness, and the Economic Security Project. If you want to do one thing after reading this, call your rep and ask where they stand on it.

Support the orgs doing this work. The Economic Security Project has been the leading advocacy group for free filing and Direct File. Americans for Tax Fairness runs campaigns for a fairer tax code. ITEP (Institute on Taxation and Economic Policy) does the research that makes pieces like this one possible.

And I’m trying to let my frustration be useful instead of just exhausting. It can feel very, very easy to just throw up your hands, but change is born from hope and desire for a better world. I personally think simply having the awareness that the system is set up to make the default option the worst one is a great first step.

So if you’re sitting at your kitchen table this week, staring at a TurboTax upsell screen and a sinking feeling in your stomach — just know that you’re not alone.