Every woman I know Googles a man before a first date. Not a quick Instagram lookup. A minor background investigation. Full name into Google. LinkedIn. Instagram. Screenshot his profile and send it to a group chat. (This is how we got the “Are we dating the same guy?” groups.)

It’s a sort of reflexive action, the way you check the weather before leaving the house. It feels like common sense, the bare minimum of due diligence before sitting across from a stranger at a bar.

I check reviews before I buy anything over $50. I read the one-star reviews first, because I assume the five-star ones might be fake. I check multiple browsers before buying plane tickets because I’ve heard the prices change based on your search history. (Do they? It’s not 100% confirmed, but I’ve written about surveillance pricing too many times to not be suspicious.)

I don’t think any of this makes me paranoid. I think it makes me normal. Everyone I know does some version of this.

This is tax you pay for living in a society that doesn’t trust itself.

There’s a particular kind of exhaustion that comes from living in a society where you can’t take anything at face value. Not the price on the label, not the job listing, not the product review, not the terms of the contract. You develop a permanent squint — a low-grade suspicion that hums beneath every transaction, every interaction, every click.

We tend to talk about trust as a social or political problem. Declining trust in institutions, in government, in each other — these are the subjects of concerned op-eds and Pew Research surveys. And they should be.

But the erosion of trust is also an economic problem. And the economic system we’ve built — one that rewards extraction, obfuscation, and short-term profit above all else — is the engine driving that erosion.

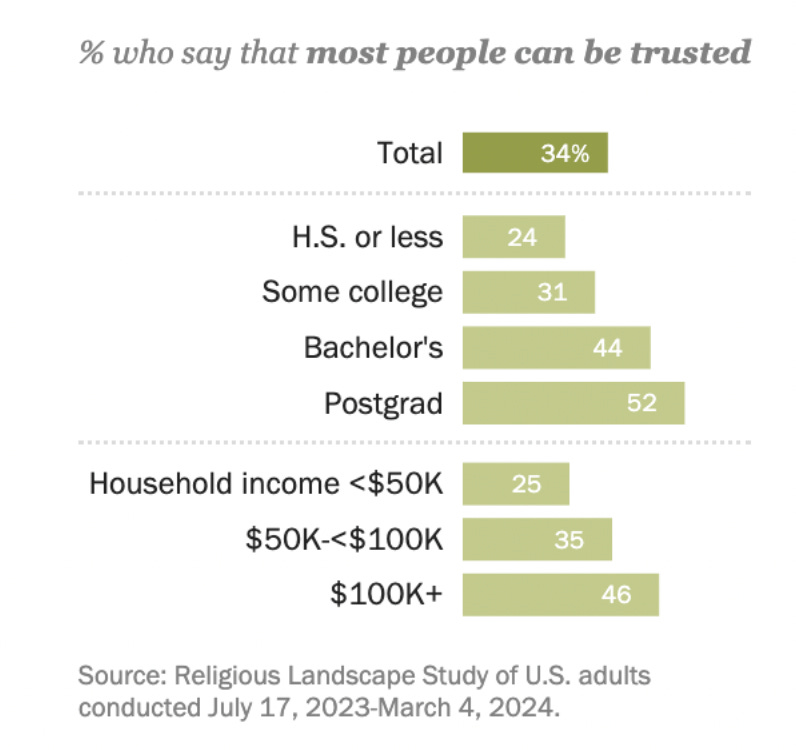

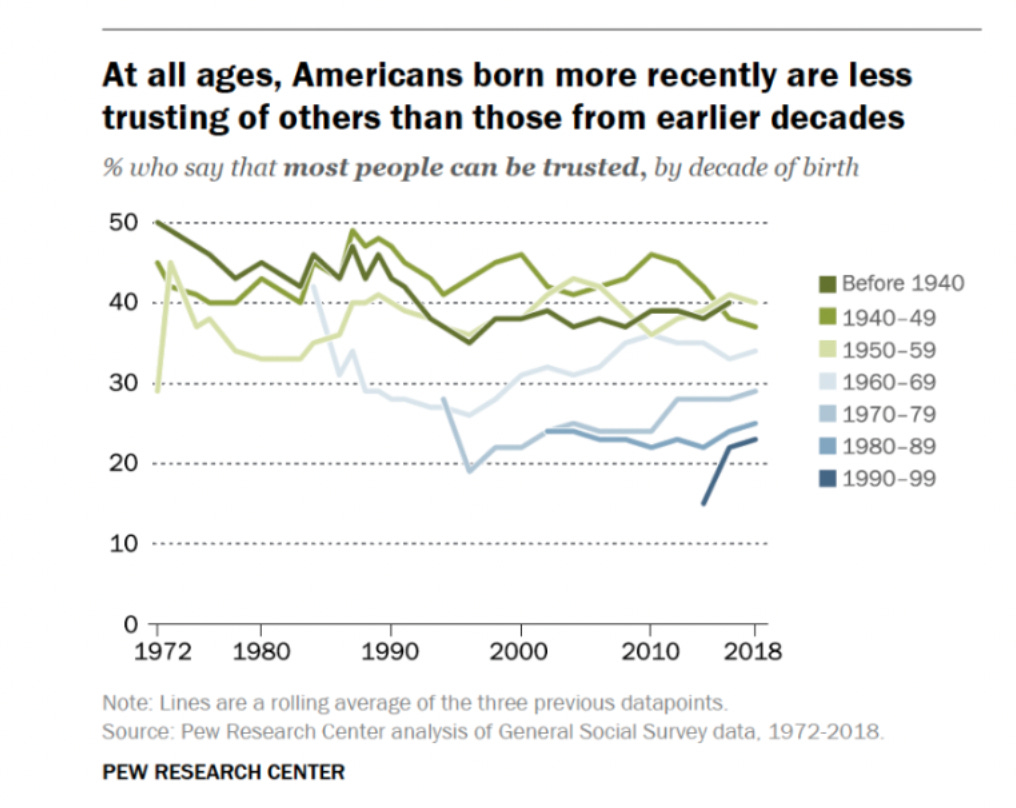

The Pew Research Center has been tracking interpersonal trust since 1972. Back then, 46% of Americans said “most people can be trusted.” Today, it’s 34%. Just 28% trust the media — down from 72% in the 1970s.

The 2026 Edelman Trust Barometer found that seven in ten people globally now report “unwillingness or hesitance to trust someone with different values.”

Economists have a term for this: social capital. It’s the idea that trust is a precondition for markets to actually work. When people trust that contracts will be honored, that products are what they claim to be, that the person on the other side of the transaction isn’t trying to destroy them — commerce flows. Innovation happens. People take risks, start businesses, lend money, collaborate.

When trust collapses, all of that seizes up.

Think about what a low-trust economy actually looks like in practice. Everything gets expensive. Contracts get thicker. Lawyers get richer. Every transaction requires documentation, verification, third-party guarantees.

The friction is very much structural. It’s a tax on everything, paid in time, money, and cognitive bandwidth.

Last week, I wrote about 2025 as the year the grift economy went mainstream — surveillance pricing, prediction markets, AI slop, fraud at industrial scale. All of that is real. But it’s downstream of something deeper: we live in an economy that has systematically destroyed the conditions for trust, and then charges us for the workarounds.

Consider the subscription economy. What was once a convenience — auto-renew so you don’t have to think about it — has become a tool of exploitation.

Surveillance pricing that charges you the maximum the algorithm thinks you’ll tolerate. Cancellation processes so labyrinthine that Amazon named theirs “Iliad” internally — as in, the epic Greek poem — because escaping was supposed to be an odyssey. (They settled an FTC lawsuit over it.) Junk fees buried in checkout flows. Shrinkflation. Service shrinkflation — hotels offering fewer cleanings, loyalty programs requiring more points, AI chatbots replacing human service.

A lot of today’s regulatory apparatus now exists because companies abused the assumption of good faith.

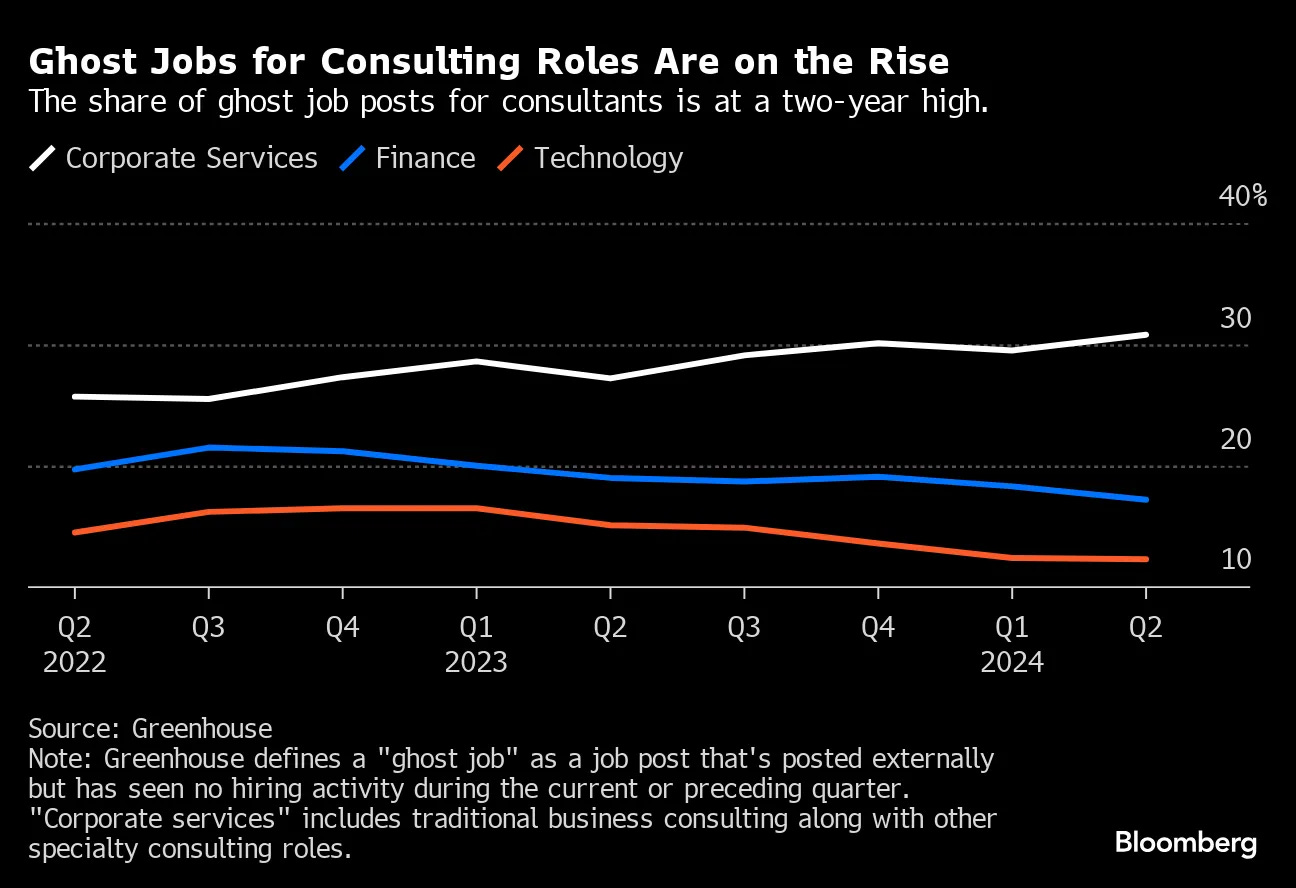

Or consider the job market. Fake job listings — “ghost jobs“ that companies post with no intention of filling — have become so pervasive that they distort labor market data and waste millions of hours of applicant time.

Why do they exist? Because companies discovered that the appearance of hiring is useful for investor relations, for internal politics, for building a candidate pipeline. The cost is externalized onto the people who spend hours tailoring resumes and sitting through interviews for positions that were never real.

When the system rewards dishonesty, dishonesty is what you get.

As I wrote last week, the grift economy isn’t just about single bad actors — it’s what a low-trust system produces.

When institutions and corporations behave in predatory ways, individuals start to adopt the same logic. If the system is a grift, then grifting becomes rational. If everyone is trying to extract value from you, why wouldn’t you try to extract value from them?

The explosion of scams, side-hustle culture repackaged as “courses” that teach you to scam others, dropshipping empires built on misleading ads, influencer marketing that can’t be distinguished from real advice.

The rise of “fake it till you make it” as a legitimate business philosophy. Something like Theranos didn’t happen in a vacuum. It happened in a culture where the line between storytelling and fraud had been so thoroughly blurred that a company could fake an entire technology and attract billions in investment.

The scam economy is what a low-trust system produces. When people lose faith that playing by the rules leads to fair outcomes, the rules start to feel optional. And once that happens, trust erodes further, which makes the rules feel even more optional, which erodes trust further still. It’s a death spiral.

And the people who suffer most are the ones who can least afford to. Wealthy people can absorb the cost of a bad deal, a misleading investment, a predatory subscription. They have lawyers. They have financial advisors. For everyone else, a single scam — a fake landlord, a fraudulent contractor, a deceptive loan — can be financially devastating. Low trust is regressive. It functions as a tax on the poor.

Living in a state of perpetual vigilance is cognitively expensive.

Every email could be phishing. Every phone call could be fraud. Every price could be inflated, every review could be fake, every “limited time offer” could be manufactured urgency. There’s a clear mental labor involved with trying to figure out if you’re getting dupped or not.

Behavioral economists call this “decision fatigue.” But it’s more than that. It’s trust fatigue — the weariness of living in a world where you have to assume bad faith as your default.

People in low-trust environments experience higher rates of anxiety, depression, and chronic stress. They’re more likely to feel isolated, because distrust doesn’t stay contained to commercial transactions — it bleeds into personal relationships. If you spend all day navigating systems designed to exploit you, it becomes harder to turn that off when you get home.

There’s a concept in psychology called “epistemic learned helplessness“ — the state where you’ve been deceived so many times that you stop trying to figure out what’s true. You don’t become smarter or more discerning. You just give up on discernment entirely. This is where conspiracy thinking flourishes.

And that, conspiracy thinking, is the psychological endgame of a low-trust economy. Not a population of savvy, skeptical consumers making smart choices. A population of exhausted, anxious people who can’t tell what’s real anymore.

The erosion of trust in our country is the predictable outcome of specific economic choices.

Start with deregulation. When you systematically remove the guardrails that prevented companies from deceiving consumers — and then underfund the agencies tasked with enforcing what remains — you help create an environment where dishonesty is profitable.

Add financialization. When companies are optimized for quarterly earnings rather than long-term value creation, customer relationships are viewed as a short-term extraction opportunity.

Layer on the platform economy, which has created new and spectacular ways to scale dishonesty. Fake reviews are an industry. Dark patterns — interface designs specifically engineered to trick you into choices you didn’t mean to make — become the standard.

And then there’s consolidation. When industries are dominated by a handful of players, consumers can’t make better choices (because there are none).

A great example of what a low-trust society looks like.

Trust is not just a nice-to-have. It’s not a soft, sentimental concept that belongs in a TED Talk but not in serious economic analysis.

Trust is a public good — like clean air, like roads, like the electrical grid. It’s the invisible infrastructure that makes everything else work.

And like all public goods, it’s subject to the tragedy of the commons. Every company that uses a dark pattern, every platform that allows fake reviews, every employer that posts a ghost job — they’re each making a singular rational decision that degrades a shared resource. No individual actor bears the full cost of the trust they destroy. But collectively, we all pay for it.

In higher transaction costs. In wasted time. In anxiety. In a political system increasingly unable to function because its citizens don’t believe anything anymore.

The idea that self-interest, left alone, will produce good outcomes? It’s failed. Markets need trust to function. And markets, left to their own devices, will consume the trust they depend on.

Rebuilding trust requires treating it like the infrastructure it is. Real regulation with real enforcement and real penalties. Antitrust action that restores competitive markets where you can actually choose trustworthy businesses. Incentive structures that reward long-term relationships over short-term extraction.

But it also requires something that can’t be legislated: people and communities choosing to operate differently. Choosing trust not as naïveté, but as strategy.

That’s what I want to explore next week — community as an economic strategy, not just a nice-to-have. How investing in relationships might be the smartest financial decision you can make. How trust, when you build it intentionally, compounds the same way money does.