Tesla is Now the World’s Most Valuable Automaker

Even in the midst of a pandemic, Tesla continues to reach new heights.

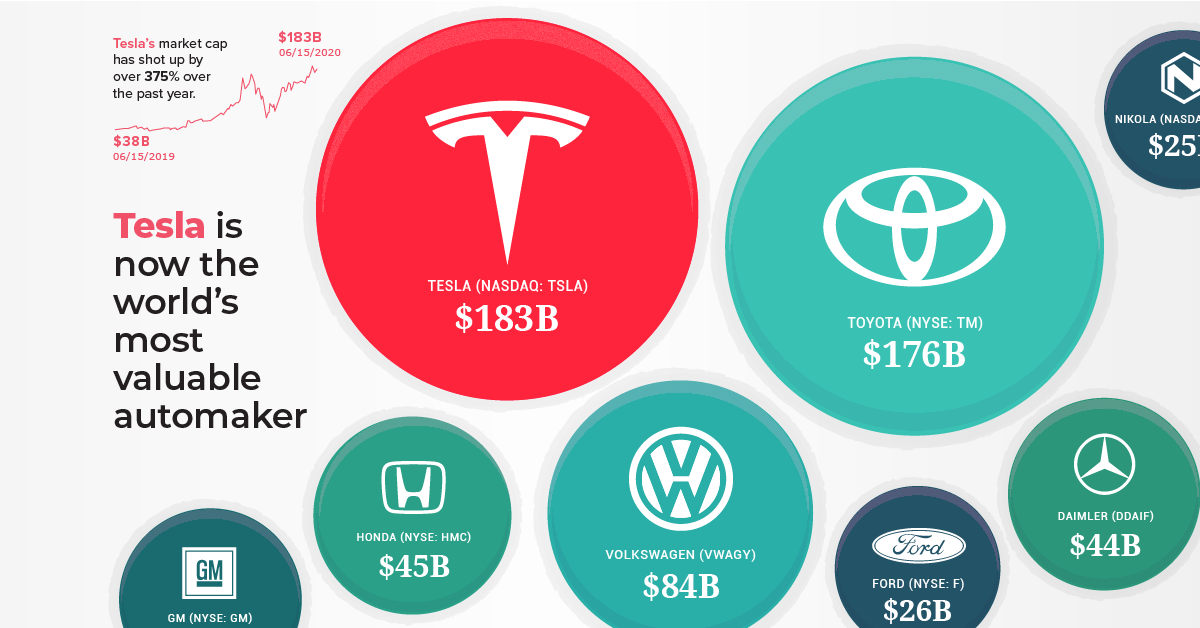

The company, which began as a problem-plagued upstart a little over 15 years ago, has now become the world’s most valuable automaker – surpassing industry giants such as Toyota and Volkswagen.

This milestone comes after a year of steady growth, which only hit a speed bump earlier this year due to COVID-19’s negative impact on new car sales. Despite these headwinds, Tesla’s valuation has jumped by an impressive 375% since this time last year.

How does Tesla’s value continue to balloon, despite repeated cries that the company is overvalued? Will shortsellers declare a long-awaited victory, or is there still open road ahead?

Tesla’s Race to the Top

Earlier this year, Tesla hit an impressive milestone, surpassing the value of GM and Ford combined. Since then, the automaker’s stock has continued it’s upward trajectory.

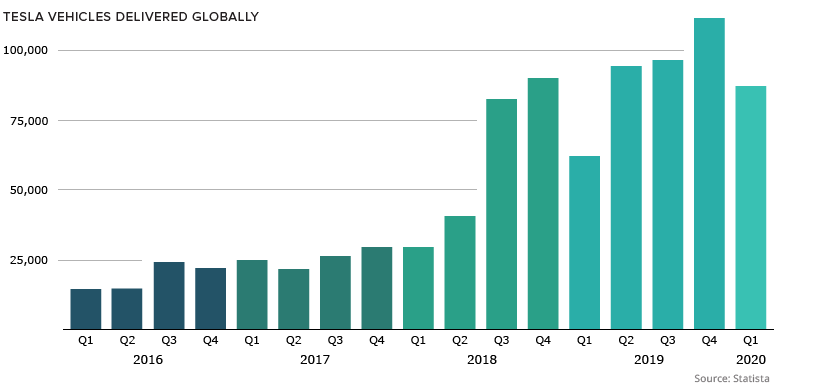

Thanks to the popularity of the Model 3, Tesla sold more cars in 2019 than it did in the previous two years combined:

As well, the company is taking big steps to up its production capacity.

Austin, Texas and Tulsa, Oklahoma are currently rolling out the incentives to attract Tesla’s new U.S.-based factory. The company is also increasing its global presence with the construction of Giga Berlin, it’s first European production facility, as well as completing the ongoing expansion of its Giga Shanghai facility in China.

Battle of the Namesakes

Tesla’s most recent price bump was fueled in part by a leaked internal memo from Tesla’s CEO, Elon Musk, urging the company’s staff to go “all out” on bringing electric semi trucks to the global market at scale.

It’s time to go all out and bring the Tesla Semi to volume production.

– Elon Musk

Of course, Musk’s enthusiasm for semi trucks isn’t coming from nowhere. Another company, Nikola (also named after famed inventor Nikola Tesla), is focused on electrifying the two million or so semi trucks in operation in the U.S. market.

Although Nikola has yet to produce a vehicle, its market cap has surged to $24 billion – which puts its valuation nearly on par with Ford. Much like Tesla, the company already has preorders from major companies looking to add electric-powered trucks to their delivery fleets.

For major brands looking to hit ESG targets, zero-emission heavy-duty trucks is an easy solution, particularly if the vehicles also live up to claims of being cheaper over the vehicle’s lifecycle. The big question is which automaker will capitalize on this mega market first?

Oil and Gas

Visualizing 75 Years of U.S. Energy Production

In 1950, coal was America’s top energy source, but by 2025 it’s natural gas. See how the U.S. energy mix transformed over 75 years.

Published

1 day ago

on

July 14, 2026

Visualizing 75 Years of U.S. Energy Production

See visuals like this from many other data creators on our Voronoi app. Download it for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Key Takeaways

- Coal and natural gas have swapped places since 1950. Coal fell from 41% of U.S. energy production to 10%, while natural gas rose from 20% to 47%.

- Crude oil ranked second in both 1950 and 2025, despite falling from nearly 40% of production in the early 1970s to just 15% in 2008.

- Total U.S. primary energy production more than tripled over the period, rising from 34.5 to 107.1 quadrillion BTU.

Over the last 75 years, the sources powering U.S. energy production have changed significantly, shaped by new technologies, shifting economics, and major global events.

This visualization tracks the production share and total output of major U.S. energy sources from 1950 to 2025.

Energy production is measured in quadrillion British thermal units (quads). The figures come from the U.S. Energy Information Administration.

75 Years of U.S. Energy Production (1950–2025)

U.S. primary energy production climbed from 34.5 quadrillion BTU in 1950 to 107.1 quadrillion BTU in 2025.

Natural gas accounted for much of that growth, rising from 7.0 to 50.5 quads, an increase of more than sevenfold. Most of the gain came after 2008, when shale drilling ended a four-decade stretch of largely stagnant output.

The data table below shows U.S. energy production by source from 1950 to 2025, measured in quads:

| Energy Source | 1950 (Quads) | 2025 (Quads) | % Change (1950–2025) |

|---|---|---|---|

| Coal | 14.1 | 11.0 | -22.0% |

| Natural Gas | 7.0 | 50.5 | 621.4% |

| Crude Oil | 11.4 | 28.2 | 147.4% |

| Nuclear | 0.0 | 8.2 | n/a |

| Hydroelectric and Geothermal | 0.3 | 1.0 | 233.3% |

| Solar and Wind | 0.0 | 3.0 | n/a |

| Wood and Waste | 1.6 | 2.4 | 50.0% |

| Biofuels and Waste | 0.0 | 2.8 | n/a |

| Total U.S. Primary Energy Production | 34.5 | 107.1 | 210.4% |

Coal moved in the opposite direction. Production rose from 14.1 quads in 1950 to a peak of 24.0 quads in 1998, before falling sharply after 2009 as utilities increasingly switched to lower-cost natural gas. By 2025, coal production had declined to 11.0 quads.

Crude oil followed a longer and more volatile path. Production nearly doubled from 11.4 quads in 1950 to 20.4 quads in 1970, then declined for more than three decades to a low of 10.6 quads in 2008.

The same shale techniques that revived natural gas production also pushed crude oil output to a record 28.2 quads in 2025, helping make the U.S. the world’s largest oil producer.

Coal and Natural Gas Have Swapped Places

In 1950, coal was the largest source of U.S. primary energy production, followed by crude oil and natural gas. By 2025, natural gas had moved into first place, crude oil remained second, and coal had fallen to third.

The data table below shows each major energy source’s share of U.S. production in 1950 and 2025:

| Energy Source | 1950 (Share of Energy Mix) | 2025 (Share of Energy Mix) | Percentage Point Change (1950–2025) |

|---|---|---|---|

| Coal | 40.9% | 10.3% | -30.6 |

| Natural Gas | 20.3% | 47.2% | +26.9 |

| Crude Oil | 33.0% | 26.3% | -6.7 |

| Nuclear | 0.0% | 7.7% | +7.7 |

| Hydroelectric and Geothermal | 0.9% | 0.9% | +0.1 |

| Solar and Wind | 0.0% | 2.8% | +2.8 |

| Wood and Waste | 4.6% | 2.2% | -2.4 |

| Biofuels and Waste | 0.0% | 2.6% | +2.6 |

Crude oil is the one major fuel that ended close to where it began. It supplied 33% of U.S. production in 1950 and 26% in 2025, ranking second in both years. In between, its share rose to nearly 40% in the early 1970s before falling to just 15% by 2008 amid a multidecade production decline.

The shale-driven rebound in oil and natural gas has helped keep the U.S. among a small group of major economies that produce more energy than they consume, alongside countries such as Russia, Saudi Arabia, and Canada.

Renewable sources have also expanded from a relatively small base. Solar, wind, hydroelectric, and biofuels collectively increased their share of U.S. production from 3.4% in 2006 to 6.7% in 2025. Even so, the country’s production mix remains dominated by the same three fossil fuels as in 1950, only in a different order.

Learn More on the Voronoi App

If you enjoyed today’s post, check out Mapped: The World’s Biggest Energy Sources by Country on Voronoi.

Energy

Charted: How China Reshaped Global Oil Trade

See how global crude oil trade has shifted since 1990, with China and India driving import growth and North America becoming a net exporter.

Published

2 weeks ago

on

July 3, 2026

Charted: How China Reshaped Global Oil Trade

See visuals like this from many other data creators on our Voronoi app. Download it for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Key Takeaways

- China is now the world’s largest crude oil importer, with net imports reaching 11.5 million barrels per day in 2025.

- North America has transformed from a major importer into a net exporter following the U.S. shale boom.

- Despite shifting demand toward Asia, the Middle East remains the world’s largest crude oil exporting region.

Over the past three decades, the geography of global crude oil trade has been fundamentally reshaped.

Rapid economic growth across Asia fueled a surge in oil demand, while advances in North American production altered long-established trade flows.

This visualization tracks net crude oil imports and exports by region from 1990 to 2025, using data from OPEC, the U.S. Energy Information Administration (EIA), and the UN Comtrade Database.

Asia Has Become the Center of Global Oil Demand

China experienced the largest change of any region in the dataset.

After importing almost no crude oil in the early 1990s, China’s net imports climbed to 11.5 million barrels per day in 2025, making it the world’s largest importer.

| Year | Europe (Oil Imports, Mb/d) | China | India | S. Korea | Japan | Rest of Asia Pacific |

|---|---|---|---|---|---|---|

| 1990 | 8.8 | — | 0.4 | 0.8 | 4.0 | 0.8 |

| 1991 | 8.4 | — | 0.5 | 1.1 | 4.1 | 0.6 |

| 1992 | 8.4 | — | 0.6 | 1.4 | 4.3 | 0.9 |

| 1993 | 8.3 | — | 0.6 | 1.5 | 4.3 | 1.1 |

| 1994 | 7.8 | — | 0.6 | 1.6 | 4.6 | 1.2 |

| 1995 | 7.6 | — | 0.6 | 1.7 | 4.6 | 1.5 |

| 1996 | 7.7 | 0.0 | 0.7 | 2.0 | 4.5 | 1.9 |

| 1997 | 7.8 | 0.3 | 0.7 | 2.4 | 4.6 | 2.0 |

| 1998 | 8.5 | 0.2 | 0.8 | 2.3 | 4.3 | 1.9 |

| 1999 | 7.6 | 0.6 | 1.2 | 2.4 | 4.2 | 1.7 |

| 2000 | 7.6 | 1.2 | 1.5 | 2.5 | 4.3 | 1.8 |

| 2001 | 7.8 | 1.1 | 1.6 | 2.4 | 4.2 | 1.9 |

| 2002 | 7.7 | 1.2 | 1.7 | 2.2 | 4.1 | 2.0 |

| 2003 | 8.4 | 1.7 | 1.8 | 2.2 | 4.2 | 1.9 |

| 2004 | 9.1 | 2.4 | 1.9 | 2.3 | 4.0 | 2.2 |

| 2005 | 9.6 | 2.4 | 1.9 | 2.4 | 4.2 | 2.6 |

| 2006 | 9.7 | 2.8 | 2.2 | 2.5 | 4.1 | 2.6 |

| 2007 | 9.7 | 3.2 | 2.4 | 2.4 | 4.0 | 2.7 |

| 2008 | 10.2 | 3.5 | 2.6 | 2.3 | 4.0 | 2.5 |

| 2009 | 9.0 | 4.0 | 2.6 | 2.3 | 3.4 | 2.3 |

| 2010 | 9.3 | 4.7 | 2.8 | 2.4 | 3.5 | 2.6 |

| 2011 | 9.3 | 5.0 | 3.4 | 2.5 | 3.5 | 2.8 |

| 2012 | 9.6 | 5.4 | 3.7 | 2.6 | 3.5 | 3.2 |

| 2013 | 9.2 | 5.6 | 3.8 | 2.5 | 3.4 | 3.1 |

| 2014 | 9.1 | 6.2 | 3.8 | 2.5 | 3.2 | 3.1 |

| 2015 | 9.8 | 6.7 | 3.9 | 2.8 | 3.2 | 2.9 |

| 2016 | 9.5 | 7.6 | 4.3 | 2.9 | 3.2 | 3.0 |

| 2017 | 10 | 8.3 | 4.3 | 3.0 | 3.2 | 3.2 |

| 2018 | 9.7 | 9.2 | 4.5 | 3.0 | 3.1 | 3.3 |

| 2019 | 9.8 | 10.2 | 4.5 | 2.9 | 3.0 | 3.3 |

| 2020 | 8.1 | 10.8 | 4.0 | 2.7 | 2.5 | 2.8 |

| 2021 | 8.3 | 10.2 | 4.2 | 2.6 | 2.5 | 2.9 |

| 2022 | 9.2 | 10.1 | 4.6 | 2.8 | 2.7 | 3.4 |

| 2023 | 8.9 | 11.3 | 4.7 | 2.7 | 2.5 | 3.5 |

| 2024 | 8.9 | 11.0 | 4.8 | 2.8 | 2.3 | 3.5 |

| 2025 | 8.7 | 11.5 | 5.0 | 2.8 | 2.4 | 3.7 |

India also saw rapid growth, with imports rising from 0.8 to 5.0 million barrels per day over the same period.

Together, China and India have become the primary drivers of global crude oil demand growth.

North America’s Energy Revolution

In the early 1990s, North America was a significant net importer of crude oil. By 2019, however, the region had become a net exporter, reaching 2.5 million barrels per day by 2025.

| Year | Middle East (Oil Exports - Mb/d) | CIS | Africa | South & Central America | North America |

|---|---|---|---|---|---|

| 1990 | 11.6 | 2.1 | 3.8 | 0.2 | — |

| 1991 | 12.2 | 1.4 | 4.1 | 0.4 | — |

| 1992 | 13.0 | 1.6 | 4.0 | 0.4 | — |

| 1993 | 13.6 | 1.7 | 3.9 | 0.6 | — |

| 1994 | 13.5 | 2.0 | 4.0 | 0.8 | — |

| 1995 | 13.5 | 2.0 | 4.1 | 1.2 | — |

| 1996 | 13.4 | 2.2 | 4.3 | 1.3 | — |

| 1997 | 14.1 | 2.4 | 4.4 | 1.5 | — |

| 1998 | 15.2 | 2.6 | 4.7 | 1.6 | — |

| 1999 | 14.7 | 2.8 | 4.3 | 1.4 | — |

| 2000 | 15.6 | 3.3 | 4.6 | 1.5 | — |

| 2001 | 14.7 | 3.4 | 4.5 | 1.5 | — |

| 2002 | 13.4 | 4.0 | 4.6 | 1.1 | — |

| 2003 | 14.1 | 4.6 | 5.2 | 1.0 | — |

| 2004 | 15.9 | 5.2 | 5.9 | 1.0 | — |

| 2005 | 16.5 | 5.6 | 5.9 | 1.8 | — |

| 2006 | 16.4 | 5.8 | 5.9 | 1.3 | — |

| 2007 | 16.2 | 6.1 | 6.5 | 1.5 | — |

| 2008 | 17.0 | 6.3 | 5.8 | 1.4 | — |

| 2009 | 14.9 | 6.4 | 6.5 | 1.4 | — |

| 2010 | 15.6 | 6.5 | 6.7 | 1.8 | — |

| 2011 | 17.4 | 6.2 | 5.6 | 2.0 | — |

| 2012 | 17.7 | 6.2 | 6.4 | 2.3 | — |

| 2013 | 17.1 | 6.1 | 5.9 | 2.0 | — |

| 2014 | 16.4 | 6.0 | 5.1 | 2.7 | — |

| 2015 | 16.6 | 6.4 | 5.3 | 3.0 | — |

| 2016 | 18.9 | 6.6 | 4.9 | 3.0 | — |

| 2017 | 18.3 | 6.7 | 5.3 | 3.0 | — |

| 2018 | 18.5 | 6.9 | 5.5 | 2.6 | — |

| 2019 | 17.1 | 6.9 | 5.5 | 2.5 | 0.4 |

| 2020 | 15.8 | 6.2 | 4.4 | 2.4 | 1.6 |

| 2021 | 15.5 | 6.0 | 4.9 | 2.0 | 1.4 |

| 2022 | 17.7 | 6.3 | 4.5 | 2.2 | 1.8 |

| 2023 | 16.6 | 6.2 | 4.7 | 2.7 | 2.4 |

| 2024 | 15.7 | 6.1 | 4.6 | 3.1 | 2.2 |

| 2025 | 16.3 | 6.2 | 4.6 | 3.7 | 2.5 |

The shift was largely driven by the U.S. shale revolution, which increased domestic oil production.

Combined with growing exports from Canada, North America has become an increasingly important supplier to global markets.

The Middle East Remains the World’s Export Hub

Even as oil demand has shifted toward Asia, the Middle East remains the dominant crude oil exporting region.

Net exports stood at 16.3 million barrels per day in 2025, far exceeding those of the CIS and Africa.

Learn More on the Voronoi App

If you enjoyed today’s post, check out Charted: The World’s Biggest Oil Producers on Voronoi.