With higher temperatures come greater hazards for the poorly paid working outdoors. One parametric insurance pilot aimed to help protect vulnerable women in India.

News reports are increasingly dominated by headlines such as ‘Record-breaking temperatures’ and ‘Hottest summer ever recorded’.

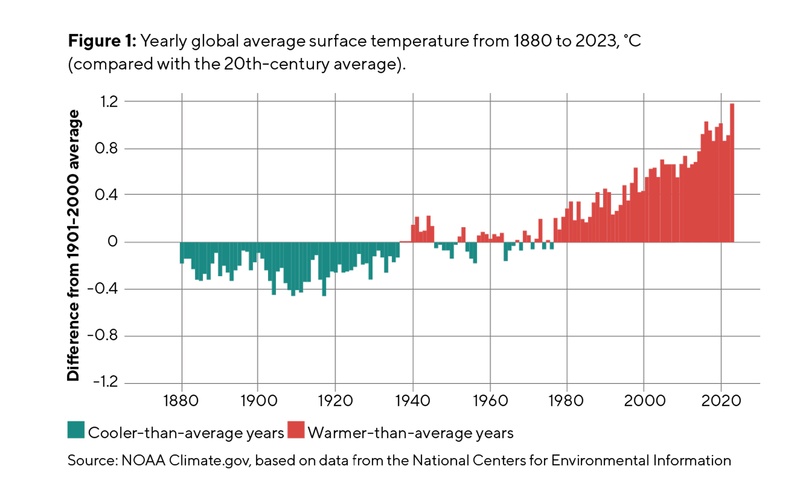

For those with access to air conditioning and cooling centres, extreme heat is uncomfortable but not dangerous. However, for millions of people, it is a serious threat to health, livelihoods and wellbeing. And as the climate changes, the issue is becoming more relevant each year. The year 2023 was the hottest on record, and 2024 temperatures are already surpassing previous records in some cities.

In 2023, climate insurtech Blue Marble partnered with the Adrienne Arsht-Rockefeller Resilience Center (Arsht-Rock) and the Self-Employed Women’s Association (SEWA) – an Indian trade union with more than 2.9 million members – to design an insurance solution that would protect vulnerable women from the health and income effects of extreme heat. They piloted a new kind of parametric insurance product: extreme heat income replacement protection for women.

Gathering intelligence

Hundreds of people die each year during heatwaves in India as rising temperatures hit densely populated urban areas. The pilot product targeted 21,000 women living in urban areas and rural slums in the western state of Gujarat, working in trades where they were highly exposed to extreme heat – waste picking, recycling, shipbuilding, head loading, selling fruit and vegetables, and so on. These women worked outdoors for extended hours with little or no access to shade, water or toilets, in temperatures of 49.3°C or more. As a result, they endured multiple health issues, such as rashes, infections, burns, headaches, miscarriages, urinary tract infections and dehydration.

If the sum of three consecutive daily high temperatures crossed a predetermined trigger threshold, the women in that district received a payout

Wanting to launch the product ahead of the 2023 heatwave season, the team worked quickly to understand the women’s needs. SEWA mobilised its network of grassroots community leaders to organise focus group discussions, which provided valuable information on the women’s sensitivity to heat, health effects, lost wages and the other effects of extreme heat on their lives and livelihoods.

Using this information, along with information from heat-health experts at Arsht-Rock, the team designed a parametric insurance product to help the women quickly recover lost income during heatwaves. Typically, such a product would take up to a year to develop from inception to launch – perhaps even longer, taking regulatory delays into account. However, the team managed to design, test and launch the product within 90 days.

Designing the product

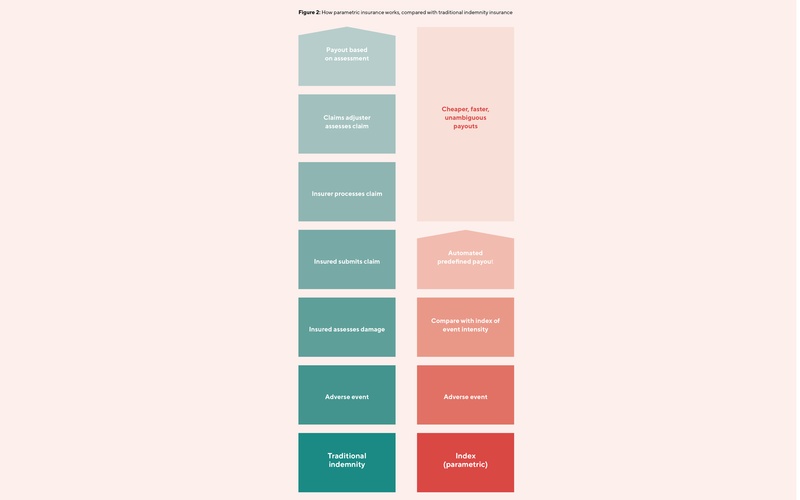

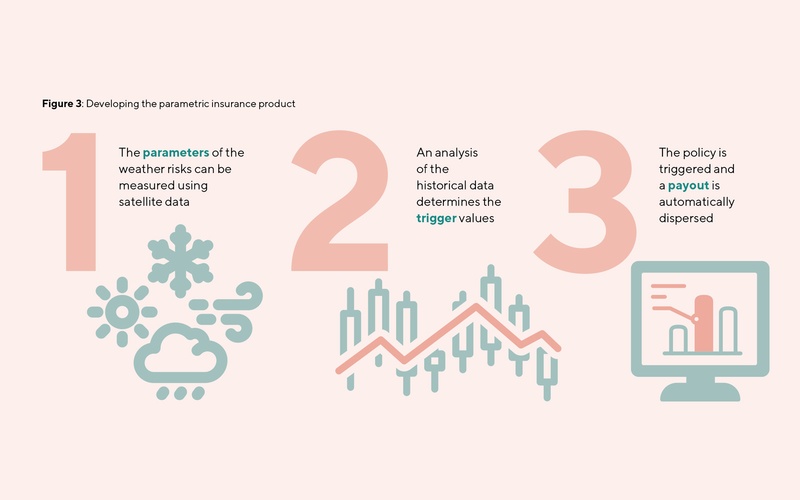

Unlike traditional insurance, where policyholders must prove their losses before they receive a payout, parametric insurance is designed so that a beneficiary can receive money directly to their bank account within days if satellite data shows that a predetermined threshold – or ‘trigger’ – has been crossed. This creates a quicker and more seamless claims process, removing lengthy wait times and the need for in-person claims adjustments.

The pilot product used a remotely sensed historical daily temperature dataset spanning 30 years, collected by a weather satellite, to determine the trigger temperature at which payouts would be made.

The heatwave season was broken into 10-day phases, with a different trigger for each phase to reflect fluctuating temperatures. This was based on the women’s feedback. During each phase, if the sum of three consecutive daily high temperatures crossed a predetermined trigger threshold, the women in that district received a payout. The calculation determining the trigger varied across the five districts covered, to reflect geographical differences.

The team also used feedback from focus group discussions to offer tangible benefits (‘value-added services’) that would help the women cope with extreme heat; these included shade tarpaulins, water coolers and solar lamps. With each policy purchased, the women could select one of these items to receive on top of the insurance. This built trust between the women and the insurance firm, given that many of the women were unfamiliar with insurance. Solar lamps were particularly popular, enabling the women to complete chores and their children to study during the cooler evening hours.

Pilot results

The 2023 pilot took place during an earlier-than-usual monsoon season, with heavy rains, flooding and cooler-than-usual temperatures.

The trigger temperature thresholds were therefore not met – but the women’s feedback remained positive. Although no payouts were made, the women expressed gratitude for the insurance because of the tangible benefits they had received, showing that the value-added services were crucial in increasing their satisfaction with the insurance. The women also shared valuable feedback for future seasons, for example suggesting that the coverage could be extended to include flood insurance during the rainy season. Looking forward, Blue Marble will be incorporating this feedback as coverage is extended to other states in India.

One woman commented: “We signed up for the insurance for our benefit. When we are given a solar light, we save on electricity, when there is no electricity we use the solar light, if we go to fields we take it with us, and we can educate our kids when there is no electricity.

For all these types of work, the solar light is useful. If we get any sickness in this type of heat, then the money can be used for medicines or we can choose to stay inside. In these situations, the insurance is helpful.”

How else can actuaries help?

As well as supporting innovation by advocating for the development and implementation of parametric insurance products that are tailored to vulnerable communities, actuaries can also:

- Promote climate resilience – champion climate adaptation strategies within their organisations.

- Collaborate – partner with innovators and local associations to create effective insurance solutions.

- Educate – inform policymakers and stakeholders about the benefits of parametric insurance.

- Implement pilots – support and refine pilot programmes to gather data and improve product designs.

Rising temperatures and extreme heat are here to stay – and while efforts to reduce carbon emissions are ongoing, adaptation measures will also be needed. This insurance pilot showed that a solution can be designed, priced and rolled out relatively quickly, and has led to the crowding-in of capital and the emergence of several new schemes for the 2024-2025 heatwave season. Looking forward, this model could be replicated across India and in other countries affected by extreme heat.

Sarah Ebrahimi is head of institutional partnerships and personal lines at Blue Marble