It’s been a while since I updated my thoughts on this area and with some of the recent news I thought it’d be helpful to post an update — it is clear that the trends I was pointing towards in previous posts {Aug 24, May 24] are becoming reality. Take a look at the latest Household Debt and Credit report as a continued example of how delinquencies are on the rise across all forms of credit in the US.

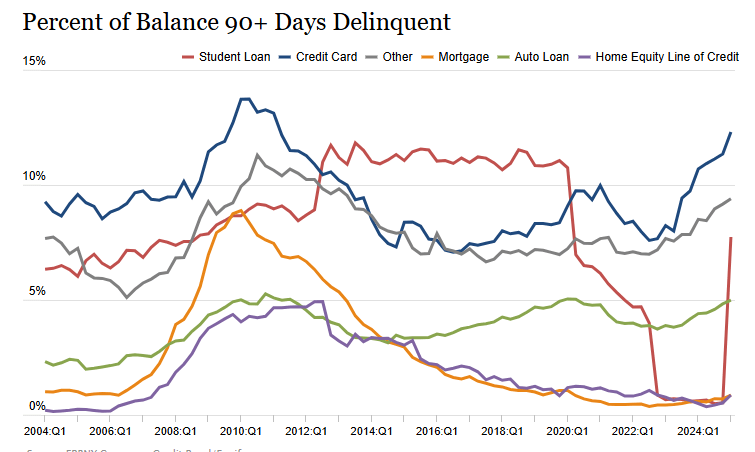

Student loan delinquencies are spiking as predicted (going from 0.5% to 7.7%), which is putting pressure on credit cards and auto loan delinquencies (Credit cards increasing to 12.3% from 11.4% and Auto Loans from 9.2% to 9.4%). I suspect the Student Loan number will continue to climb to return to historical norms closer to 10-12%. Putting additional pressure on the American consumer.

Fortunately, mortgages have yet to see the impact that these other areas have. Albeit, a small increase in the last quarter on both mortgage and Home Equity Line of Credit delinquencies. Usually, these are the last to fail as people will do everything they can to keep their home; that usually means defaulting on credit cards, auto loans, and other debt before calling it quits on the mortgage.

Given the trends we’re seeing, I doubt that mortgages will continue to perform as well as they have in regards to low delinquency rates. As other forms of debt come due, there is also the additional pressure due to continued elevated levels on US Bond prices, with the 10 year note hitting 4.5% and the 30 year eclipsing 5%. These higher rates will prevent homeowners from refinancing or getting Home Equity Lines of credit to pay off other rising debt loads as mortgage rates are directly tied to these rates.

The growing concern that isn’t talked about enough is still making progress in the background: “phantom debt”. This problem I called out previously, which is centered around companies that offer “Buy Now Pay Later” services. This ecosystem is beginning to crumble as well; so much so that it is now impacting the bottom lines of popular companies like Klarna. In the last quarter they saw delinquencies double and their IPO was put on pause. Another sign that the US credit crunch is rapidly approaching.

I suspect, the American consumer will begin to cut back heavily on spending leading to many companies cutting their workforce. This will elevate unemployment, leading to further delinquencies and lower consumer spending. There’s a bumpy road ahead.