Model inputs

Required inputs are in red.

Your ownership form

Number of shares or options you own

Option exercise price (aka strike price)

dollars

Company

or

Data for company loading error.

Click here to be contacted when we gather updated data on your company.

We do not have preloaded data for your company. Enter company details manually or click here to be contacted when we have data on your company.

Post-money valuation at last financing round

million dollars

Share price paid by investors in last financing round

dollars

Additional model inputs

Company growth since last financing round

%

Amount invested in last financing round

million dollars

Liquidation multiple of last financing round

x

Participation for last financing round

Cumulative dividend rate

%

The most recent investor can block a down-IPO

The most recent investor gets extra shares in a down-IPO

The return the most recent investor is entitled to in a down-IPO Enter 1 if the most recent investor has a 1X IPO ratchet and so gets extra shares in down-IPOs to prevent them losing money

X

Total investment in rounds prior to the last financing round

million dollars

Average time until exit

years

Random exit distribution

Annualized volatility

%

Beta

Risk free rate

%

Market risk premium

%

%

Model outputs

The numbers here are estimates of the fair value of your shares or options. When we say fair value, we mean the value that something would have if they were sold in an orderly transaction. We determine fair value by looking at the prices paid for other securities issued by the same company.

Estimated fair value of company

Post-money valuation at previous round:

ERROR!

million

Fair value of company at previous round:

ERROR!

million

Fair value of company after

ERROR!

growth:

ERROR!

million

Estimated fair value of each type of share

The most recent preferred shares:

ERROR!

A common share:

ERROR!

Exercise price paid today for one common share:

ERROR!

ERROR!

ERROR!

The option exercise price was set so that the option would be at the money at the time of the previous financing round.

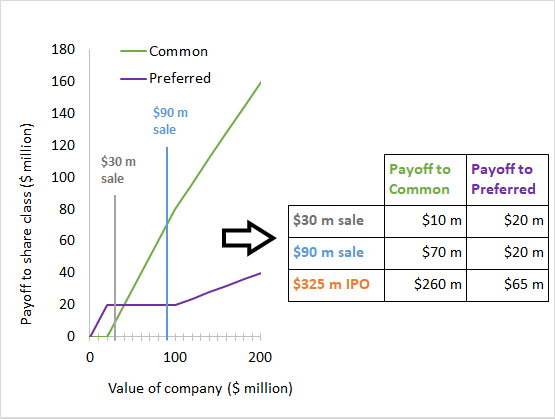

What different shares are worth in different liquidity events

Estimated distribution of payoffs at liquidity event

ERROR!

|

ERROR! |

|

|

|

ERROR! |

||

|

ERROR! |

||

|

ERROR! |

||

|

ERROR! |

||

|

ERROR! (or possibly much more!) |

||

| With all of these payofs occuring when the company eventually exits. These values are the 8th, 25th, 42nd, 58th, 75th, and 92nd percentiles of the return distribution. | ||

Other considerations

This calculator values shares from the perspective of a diversified investor. The value of these shares to YOU may be substantially lower.

Can you tolerate risk?

Startup options are very risky, as illustrated by the dice roll example above. The more money you have and the more secure your job is, the better you are able to deal with that risk. Beyond that, some people are more worried about risk than others.

The less you are able to deal with risk, the less your shares are worth to you.

Are you impatient?

If you have high interest debt or need to buy a house, you may prioritize money today. That reduces the value of payoffs that will come years from now.

The more you need money today or in a few years, the less your shares are worth.

Will you quit?

If you leave a startup, you lose your unvested ownership. Vested ownership may also lose value as you may have to exercise options (creating tax and cash-flow issues) or be forced to sell them to the company.

The more likely you are to leave the company early, the less your shares are worth.

Will you need to sell?

Selling shares in startups can be hard. First, startups have a variety of contractual rights that make it hard for employees to sell their shares to outsiders. Second, buyers may know less about the startup than employees will be worried the company is a lemon - if the company was great, why would you sell? Third, the platforms that facilitate share sales, such as EquityZen and SharesPost charge a sizeable commission.

If you need to sell ownership in startup, you may get less than the fair value.

What is your tax situation?

Receiving, exercising, or selling stock options or shares can create complicated tax situations. You should consult with a tax advisor in order to avoid an unwanted tax surprise. Your tax bill may end up being between 15% to 50% of the proceeds.

Plan for taxes and talk to a tax advisor.

Are the model assumptions correct?

This model uses parameter assumptions that are appropriate for the average VC-backed company. These assumptions were designed to be appropriate for the typical such company. If your company has definite plans to go public in the next year, it is likely no longer typical (you may want to reduce the "Avg. time until exit" to 2 years in such a case). Similarly, if your company has just had a recap or significant down round, it is not typical. In either case, these special considerations prevent our off-the-shelf model from reflecting your company's reality unless you customize the parameter assumptions.

If your company is atypical, the values produced may be incorrect.

How does it work?

Step 1 The program guesses the value of the company. Based on that value, it projects out many potential exits.

Step 2 For each possible exit, the program finds the payoff to each class of share.

Step 3 Based on these exits, the program values each security.

Step 4 The program sets the value of the company so that the most recent VC round is fairly priced. That company value is then divided between options, common shares, and preferred shares.

Refer to our paper Squaring Venture Capital Valuations with Reality for full details of the valuation process.

About the authors

WILL GORNALL

Assistant Professor of Finance, University of British Columbia

will.gornall@sauder.ubc.ca

willgornall.com

Will Gornall is an Assistant Professor of Finance at the University of British Columbia. He is an expert on venture

capital and innovation financing.

ILYA A. STREBULAEV

The David S. Lobel Professor of Private Equity, Graduate School of Business, Stanford University

istrebulaev@stanford.edu

https://ilyas1.people.stanford.edu/

Ilya A. Strebulaev is the David S. Lobel Professor of Private Equity and Professor of Finance at the Stanford Graduate

School of Business, and a Research Associate at the National Bureau of Economic Research. He is an expert in corporate finance,

venture capital, innovation financing, and financial decision-making. He is the faculty director of the Stanford GSB Venture

Capital Initiative.

Venture Capital Writing

The Venture Mindset Strebulaev, Ilya A and Dang, Alex National Bestseller, Financial Times Business Book Of The Month The Venture Mindset is a new mental model where failure is a must, ideas are rejected in their myriads in search of a single winner, due diligence is put on its head, dissent is encouraged, plugs are pulled, and time horizons are extended. It is fundamentally different from the mindset found throughout the rest of the business world. This mindset helps leaders to develop a strong pipeline of ideas, make smarter, quicker decisions, and deliver more value at scale.

Customer Data Access and Fintech Entry: Early Evidence from Open Banking Babina, Tania and Bahaj, Saleem A. and Buchak, Greg and De Marco, Filippo and Foulis, Angus K. and Gornall, Will and Mazzola, Francesco and Yu, Tong Forthcoming in Journal of Financial Economics We provide a global overview of the causes and effects of open banking, policies that empower customers to share their banking data with fintechs A previous version of this manuscript was distributed as "Customer Data Access and Fintech Entry: Early Evidence from Open Banking" (2022) by Tania Babina, Greg Buchak, and Will Gornall.

Venture Capitalists and COVID-19 Gompers, Paul and Gornall, Will and Kaplan, Steven N and Strebulaev, Ilya A Journal of Financial and Quantitative Analysis 2021, 56(7), 2474-2499 We survey 1,000 venture capitalists on how they were affected by COVID-19 Mentioned in Inst. Investor, HLS Corp. Gov. Forum

Squaring Venture Capital Valuations with Reality Gornall, Will and Strebulaev, Ilya A Journal of Financial Economics 2020, 135(1), 120–143; Doriot Award We model venture capital-backed company exits and show post--money valuations exceed fair values by 48% Teaching slides about post-money valuation and value Code Tool to value employee stock options Mentioned in Barrons 1, 2, BC Business, BIV, BJ, Bloomberg, Bloomberg, TV, Business Insider 1, 2, CNBC, Economist 1, 2, El Economista, Entreprenuer 1, 2, Financial Post, Forbes, Fortune 1, 2, G&M, Inc., Institutional Investor, JDSupra, 36kr 1, 2, Les Echos, MSN, NBER, NY Mag, NYT, Pitchbook 1, 2, 3, Reuters, Stanford, Tech Crunch, TechVibes, The Real Deal, Wired, WSJ 1, 2, 3

How Do Venture Capitalists Make Decisions? Gompers, Paul A and Gornall, Will and Kaplan, Steven N and Strebulaev, Ilya A Journal of Financial Economics 2020, 135(1), 169–190; Jensen Prize We survey 885 venture capitalists to learn how they make decisions Summarized in this Harvard Business Review article Teaching slides on the venture capital investment selection process Mentioned in Bizztor, Chicago, Havard Law School Forum, Stanford, VentureBeat

The Contracting and Valuation of Venture Capital-Backed Companies Gornall, Will and Strebulaev, Ilya A In: Eckbo, B.E., Phillips, G.M. , Sorensen, M. (eds) Handbook of the Economics of Corporate Finance. Amsterdam: North-Holland, an imprint of Elsevier, 2023. 1, 3-76 We outline key considerations for startup financing in a handbook chapter that may be a useful reference for faculty, students, and practitioners

Venture Capital Valuation Gornall, Will and Strebulaev, Ilya A In: Cumming, D., Hammer, B. (eds) The Palgrave Encyclopedia of Private Equity. Cham: Springer International Publishing, 2023. 1-5. We provide a brief outline of startup valuation considerations