Last year, on August 19 2025, the day before Powell was to give his annual Jackson Hole speech, the White House pressured Chairman Powell to lower rates. “Could somebody please inform Jerome ‘Too Late’ Powell that he is hurting the housing industry, very badly?” the President wrote on Truth Social. “People can’t get a mortgage because of him.”

A common view among policy makers is that housing is more affordable for Americans in a low-rate environment. Here is one salient example. Congresswoman Ayanna Pressley pressured Chairman Powell to lower rates when he appeared before the House Financial Services Committee on March 6, 2024:

“Chairman Powell, I welcomed the decision of the Fed to pause rates at the end of last year, but for families in my district and across the country, that is not enough. We need the Fed to start cutting. Because like the rent, interest rates are too damn high. Just yesterday, actually, I met with a number of representatives from state housing finance agencies from throughout the country. And they were talking about the barriers to affordable housing projects, given the current interest rate environment. Obviously, higher interest rates have raised costs for affordable housing developers, and many of them have chosen to slow down or halt construction entirely. So fewer homes are being built, which means fewer people are being housed.”

Around the same time, Senator Warren and three other Democratic lawmakers wrote to Powell urging him to lower interest rates "to make housing more affordable," calling the rates "astronomical" and arguing "the direct effect of these astronomical rates has been a significant increase in the overall home purchasing cost."

The bipartisan consensus on rates and housing affordability is probably wrong. This is a good example of the pitfalls of partial equilibrium thinking. These policy makers implicitly assume everything else is constant, but, to put it plainly, ceteris is not paribus in the housing market when the Fed lowers mortgage rates.

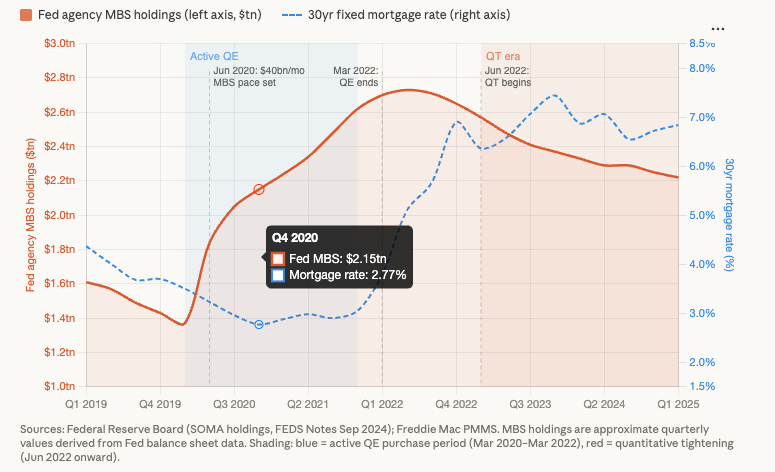

The Fed ran this experiment for us during the pandemic. On March 15, 2020, the FOMC announced an increase in agency MBS holdings by at least $200 billion over several months to improve market functioning. On March 23, the FOMC instructed its FRBNY trading desk to purchase Treasury securities and agency MBS “in the amounts needed to support smooth market functioning,” removing all caps. The purchases became open-ended.

The desk announced plans to conduct approximately $50 billion of agency MBS purchases each business day that week. From March 2020 through June 2021, the Federal Reserve increased its agency MBS holdings from $1.4 trillion to $2.3 trillion — purchasing a total of $580 billion in agency MBS in March and April 2020 alone, and averaging about $114 billion per month thereafter including reinvestments. As the Fed’s MBS holdings rise from $1.37tn to $2.73tn — nearly doubling — mortgage rates fell to historic lows below 3%, its lowest level in recorded history. As QT begins in March 2022 and holdings slowly contract, rates snapped back and then climbed to more than 400 bps to 7%. Mortgage rates during 2020–2022 were set by a huge inelastic buyer controlling an enormous share of the market.

The Fed’s MBS purchases between 2020 and 2021 led to a 90 bps compression in the mortgage spread — the difference between mortgage rates and Treasury yields from 180 bps to 90 bps, leading to a cumulative increase in mortgage originations of about $3 trillion and net MBS issuance of about $1 trillion

Many observers think that they make housing more affordable by lowering mortgage rates. Of course, holding house prices fixed, mortgages payments do go down. But that’s partial equilibrium reasoning, holding house prices fixed. Houses are assets. To value these assets, it helps to think of these as a claim to a growing stream of rental income streams, just like a stock is a claim to a growing stream of dividends. As the Fed lowers long term real rates, it inevitably will push prices up because you’re discounting future cash flows at a lower discount rate. That’s what happened during the pandemic. Naturally, there were other factors contributing to the run-up in house prices. Everyone was stuck at home. But the point is that the marginal buyer’s willingness to pay for this asset should be much higher than it was, simply because of the mortgage rate declines.

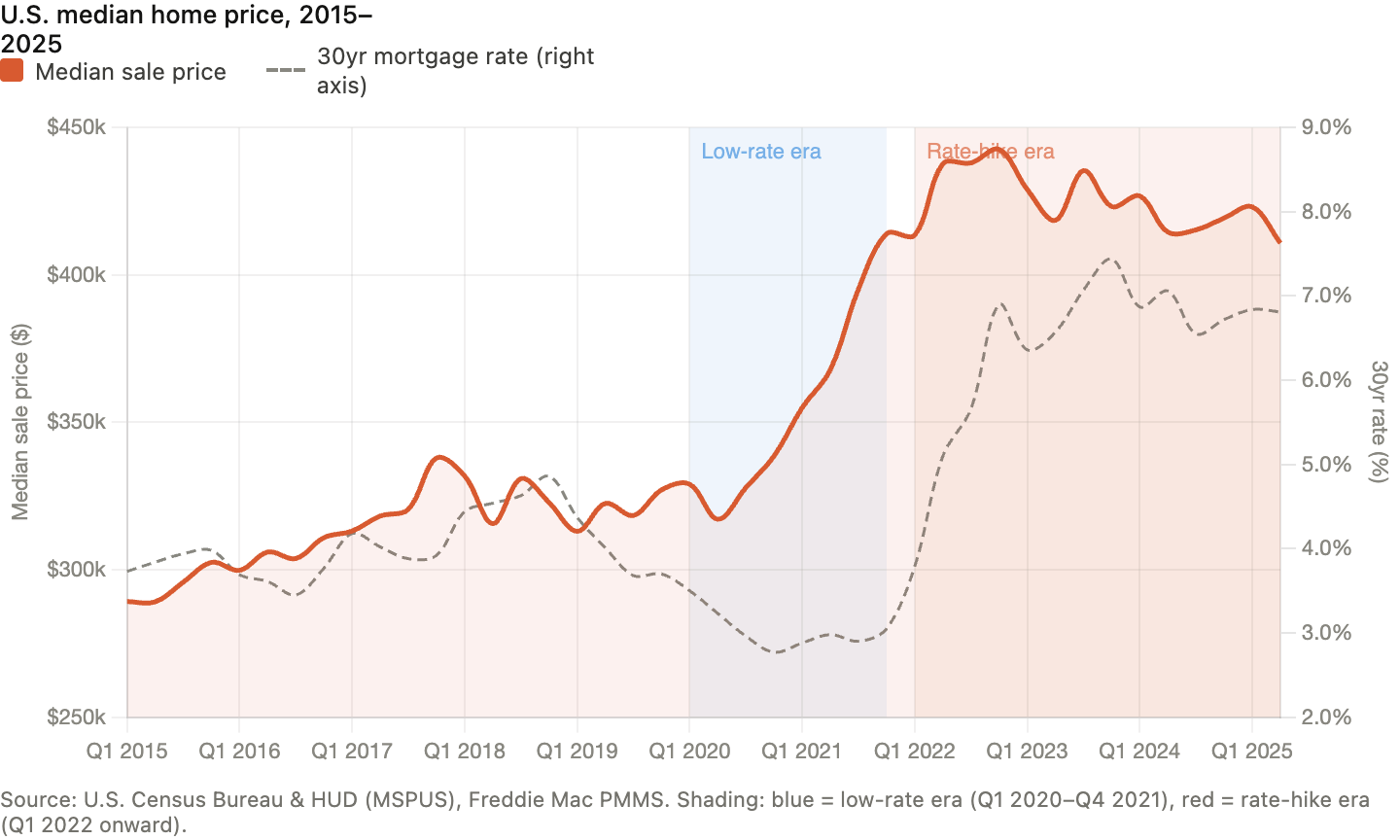

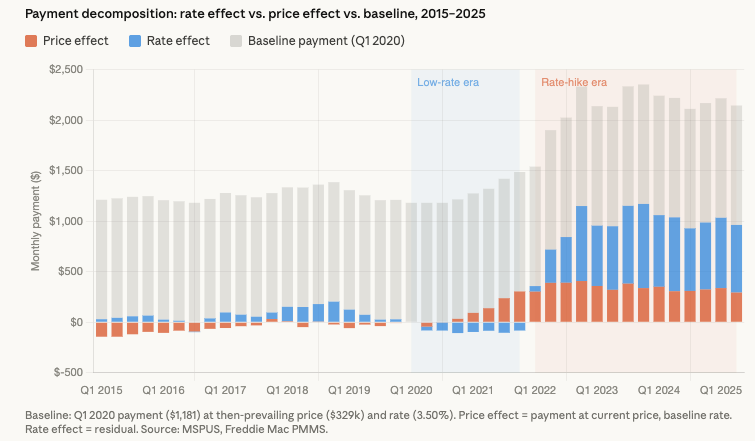

As rates declined in 2020, house prices started to surge, with the median sale prices surging nearly 40% while the dashed rate line falls. In the rate hike era (red shading). median sale prices were barely moving. Prices didn’t come back down to offset the higher rates.

A large number of US households were locked in to the extraordinarily low mortgage rates they obtained during the pandemic. Millions of households who would have transacted in the housing market, e.g., to pursue better job opportunities elsewhere, decided not to, because they did not want to give up the low-rate mortgage, as was shown by Julia Fonseca and Lu Liu in “Mortgage Lock-In, Mobility, and Labor Reallocation” in their recent paper. Mortgages are not portable in the US. If you move, you lose your low rate. This lock-in effect reduces the net supply of homes for sale, and may even push the price/rent ratio up in the housing market, even though mortgage rates are increasing (see recent work by Justin Katz “Mortgage Rate Lock and House Prices”).

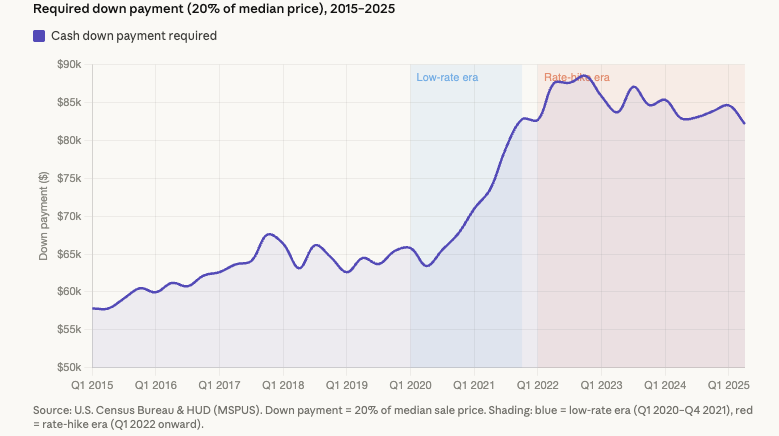

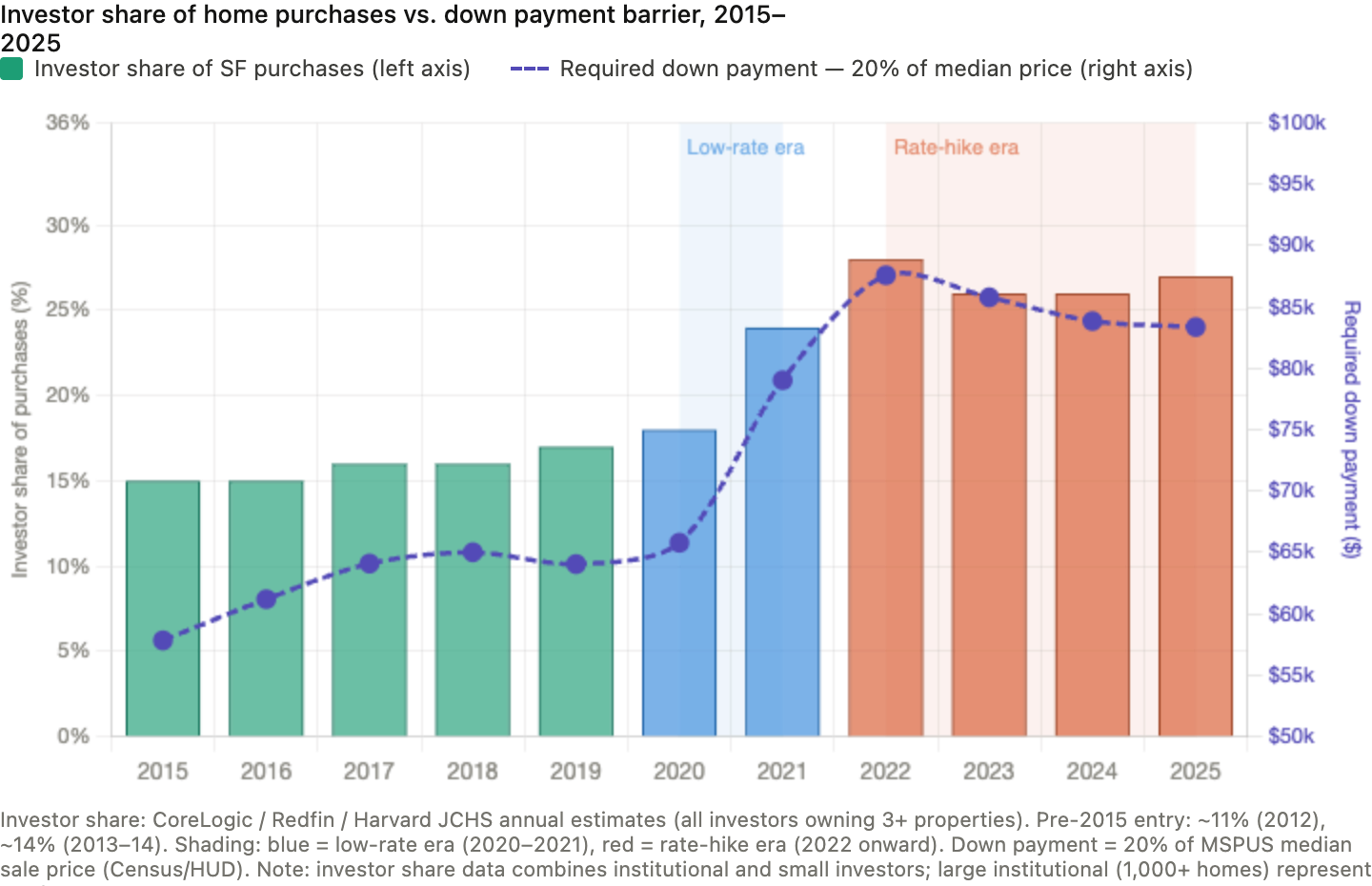

Let’s take the example of a newly married couple taking out a new mortgage to purchase a home. A 20% down payment on the median house went from roughly $66,000 in Q1 2020 to nearly $89,000 by late 2022. These first-time buyers without existing home equity now need a lot more cash before they can even access the mortgage market.

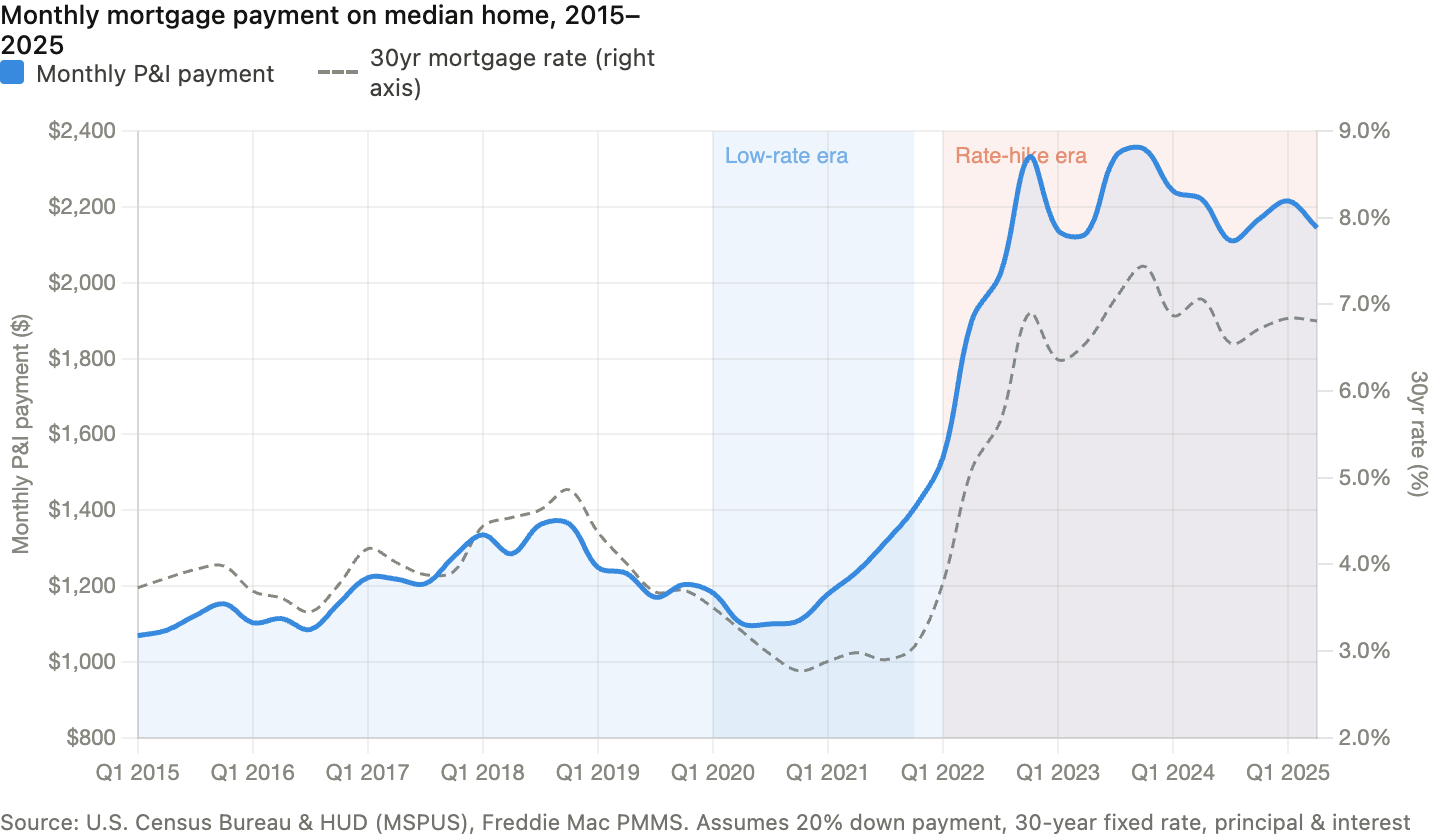

The monthly payment on a new mortgage for median home increased from $1200 prior to the pandemic to $1400 towards the end, in spite of declining rates, and then continued to increase $2200 as the Fed stopped buying mortgages in 2022 and mortgage rates snapped back and then some.

In the low-rate era the blue rate-effect bars are slightly negative — rates did help a little — but the red price-effect bars dominate the effects of lower rates. In the rate-hike era the blue bars explode, while the red bars remain stubbornly elevated because the price floor never came back down.

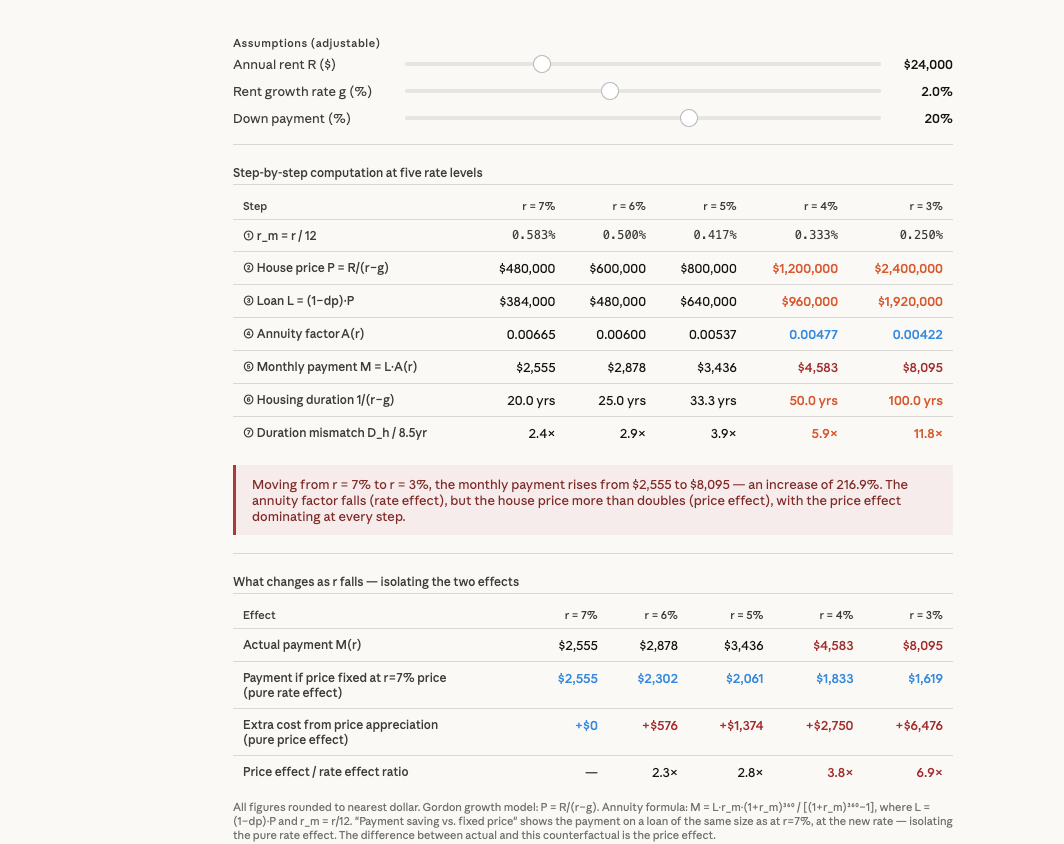

You might conclude that this period was just an anomaly, but actually, it’s not. It’s easy to show that lowering long-term rates will always tend to make housing more expensive, as measured by the monthly mortgage payment, if you price the house as a claim to a growing stream of rents. The logic is straightforward. Housing is a long-lived asset, especially the land value component. Its duration, a measure of how far in the future the typical cash flow accrues to its owner, is quite high. Duration governs how sensitive the price of the asset is to a change in the rate. Importantly, the duration of the house will exceed the duration of the mortgage that finances the purchase. As a result, the house price increase will dominate the direct rate effect on mortgage payments when rates are lowered. And the monthly payment increases. The table below develops a simple, very stylized example. As we (permanently) lower the mortgage rate from 7% to 3%, the house price increases from $480,000 to $2,400,000, and the monthly payment rises from $2,555 to $8,095.1

As a result, when the Fed lowers mortgage rates dramatically, there is a sizeable intergenerational wealth transfer from young, prospective first-time homebuyers to older, existing homeowners, contributing to the boomer wealth boom. The latter are undeniably better off because they will realize large capital gains as long as they’re willing to downsize at some point in the future and move to a smaller house. The former are worse off. Low-rate policies have made the housing affordability crisis worse (see John Burn-Murdoch’s excellent column in the FT).

The housing market during the pandemic is yet another example of how low-rate policies benefit the older and wealthier households who have invested a large share of their portfolio in long-lived assets, bonds, stocks and private companies, and hurt younger and poorer households who have not, as we explain in “Winners and Losers when Interest Rates Change.” (joint work with Dan Greenwald, Matteo Leombroni and Stijn Van Nieuwerburgh). Those who are long duration tend to be better off when rates are pushed down. Homeowners are long duration. Prospective homeowners are not.

Just this month, Senator Warren sponsored a bill, the 1st Century ROAD to Housing Act (S. 2651), to limit institutional ownership in housing markets. Actually, investors —anyone owning 3+ properties— share of home purchases rose from 16% to 28% during the pandemic, just as the downpayment on the median house increased by $20,000. Unlike prospective homebuyers, these investors, especially institutional investors, like Blackstone, don’t have any trouble coming up with the cash for a downpayment, and they have no trouble accessing larger loans when house prices rise. Institutional investors specialize in deploying leverage. In fact, in “Institutional investors in the market for single-family housing:Where did they come from, where did they go?” Sebastian Hanson attributes the entry of institutional investors into local housing markets to the decline in long-term rates. According to Sebastian, these investors are more likely to enter into those local markets where households are more financially constrained.

The pandemic was economically harmful to younger generations, not just because governments largely shifted the burden to the young by borrowing massive amounts, but also because central banks implemented a large wealth transfer from the young who will be buying assets to the old who will be selling assets, including housing, by pushing down long-term real rates into negative territory.

If Sen. Warren thinks it’s undesirable that institutional investors end up owning a larger fraction of the residential housing stock, she should talk to the Fed about its low-rate policies during the pandemic. The problem is not that interest rates are currently “too damn high”. It’s that they were “too damn low” during the pandemic. Low-rate policies give an edge in housing markets to unconstrained, sophisticated investors with access to cheap leverage.