TL;DR: There are nine ways to get electricity to a data center. Leopold Aschenbrenner’s $5.5B hedge fund is concentrated in the two that deliver power fastest, and last week Oracle validated the bet. This piece walks through all nine.

Leopold Aschenbrenner made $1.3 billion last week. He is 24.

He had $875 million riding on the stock of a company called Bloom Energy. Last week, Oracle signed a deal to buy 2.8 gigawatts of fuel cells from Bloom Energy1. Bloom’s stock jumped 24% the next day, hit an all-time high, and closed the week up 60%. By Friday Aschenbrenner’s Bloom position was worth roughly $2.2 billion2.

Two years ago, OpenAI fired him. His version is that he raised security concerns internally and got pushed out. He responded by publishing “Situational Awareness,” a 165 page essay predicting AGI by 20273, and starting a hedge fund with the same name.

Here is the part that should bother you if you allocate capital. In Q4 2025, Aschenbrenner exited Nvidia entirely. He had been holding puts against the stock, actively shorting the consensus AI trade. He closed out Broadcom and TSMC the same quarter. Then he put the money into a fuel cell manufacturer, seven Bitcoin mining companies, and CoreWeave call options. A fund built on an AGI thesis had become, to a large extent, a power infrastructure fund.

And last Monday, Oracle validated the bet.

His read is simple: the market has priced in the demand for compute. It has not priced in what powers the compute

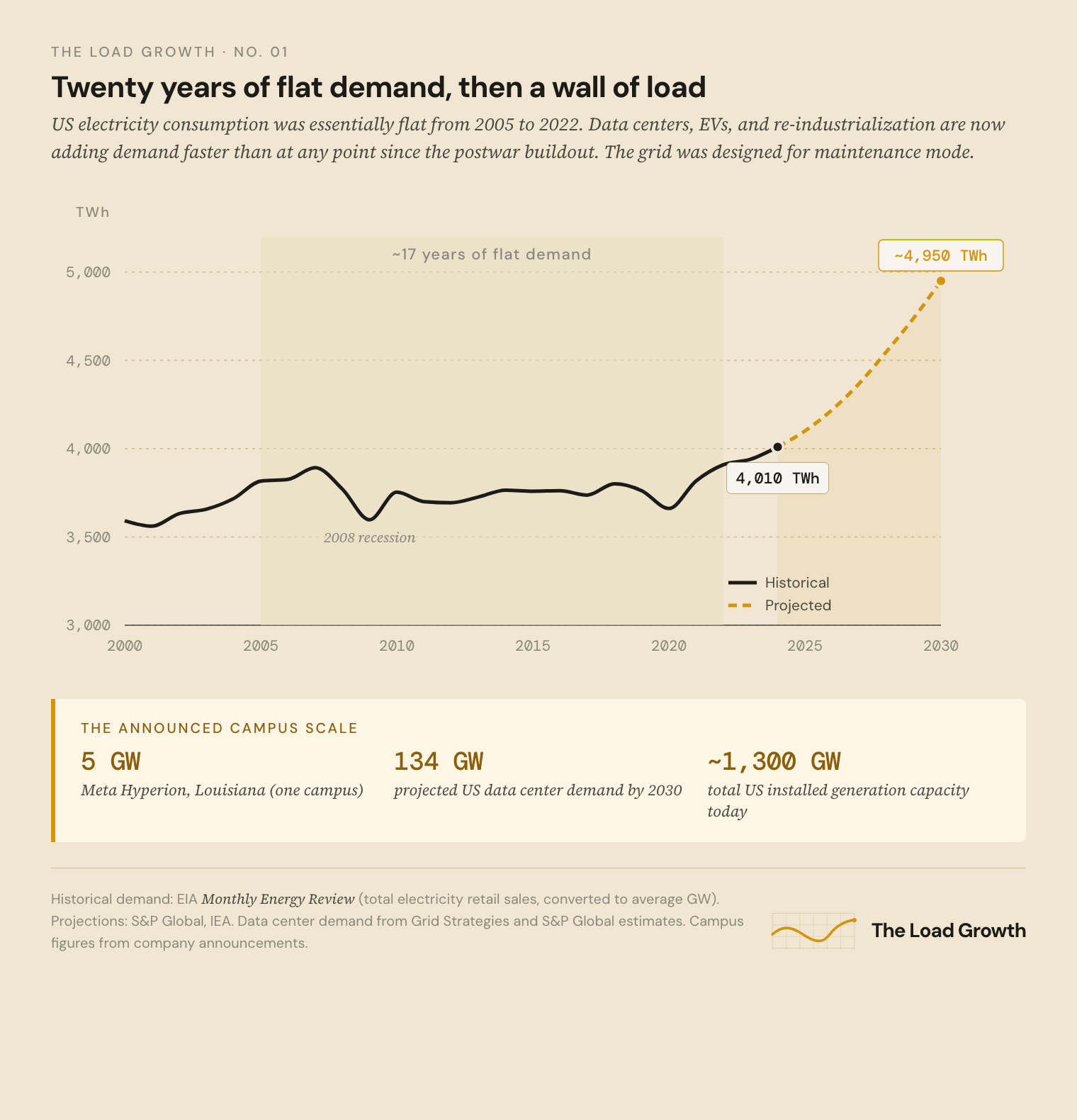

The numbers explain why he might be right. Meta’s planned Hyperion campus in Richland Parish, Louisiana will draw 5GW at full build, the output of five nuclear reactors, for one building complex. AWS’s Project Rainier in Indiana is the first campus to reach 1GW. Across the industry, roughly 550 planned data centers carry a combined power requirement of about 125 GW. S&P Global projects US data center power demand will roughly triple, from about 50GW in 2024 to 134 GW by 2020.

Those numbers land in a context that makes them much scarier. For twenty years, from roughly 2005 to 2023, US electricity demand was flat. LED lighting, deindustrialization, efficiency mandates and the 2008 recession had decoupled economic growth from electricity consumption. The entire power sector, from utility capital plans to workforce pipelines, had calibrated to zero load growth. Utilies stopped hiring linemen at replacement rates.

Then came the age of LLMs. Starting in 2023, the flatline broke. AI training clusters consuming hundreds of megawatts each began appearing in grid queues that were never designed for them. The US plugged a new industrial revolution in to a system built for maintenance mode.

Leopold’s portfolio is a bet on who solves that problem. Last week’s Oracle deal was the first proof point.

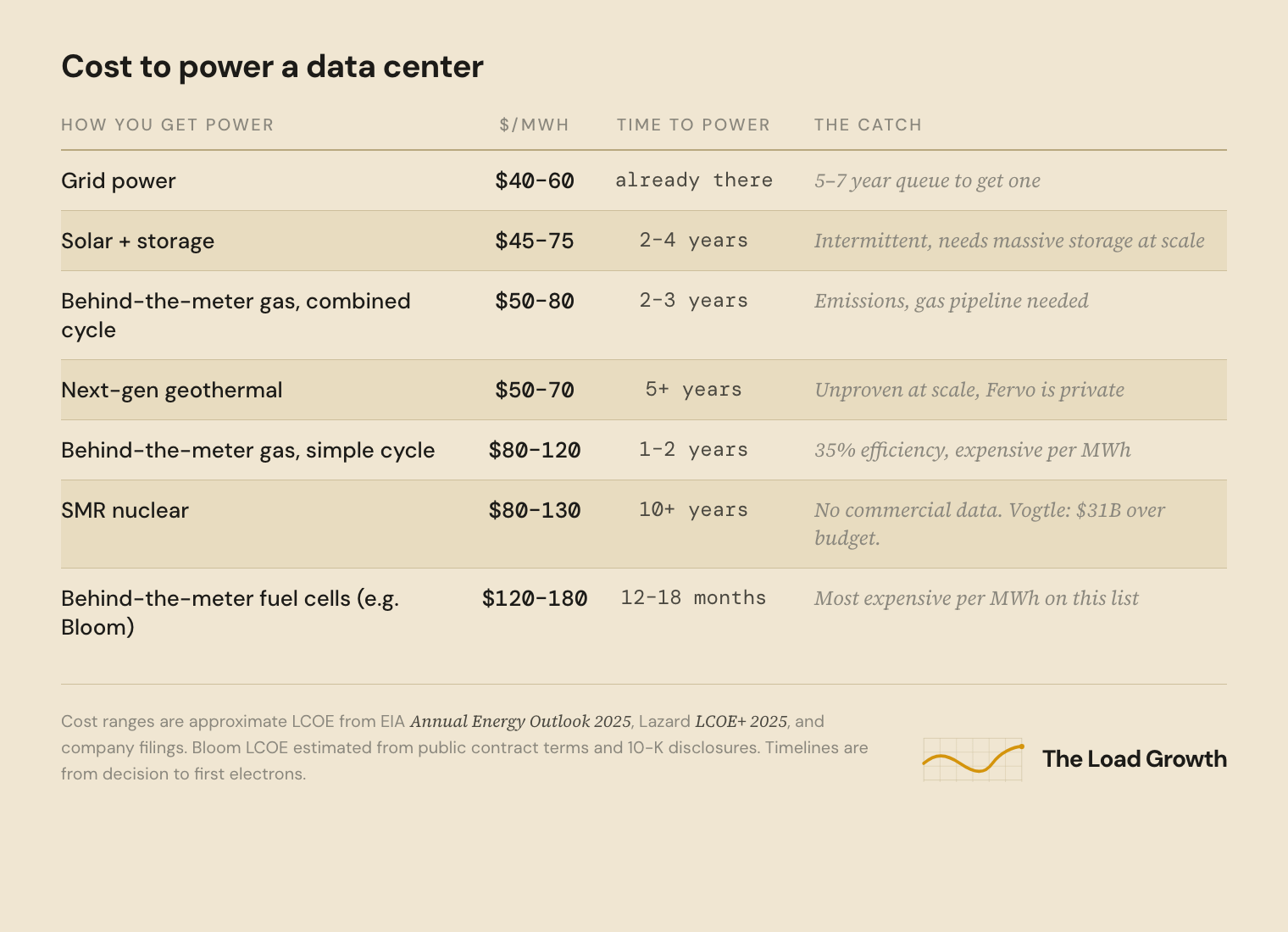

There are exactly nine ways to get power to a data center. Leopold’s holdings concentrate on the ones he thinks work on realistic timescales.

The grid is of course the default option, but it’s also broken. Connecting anything new to it currently takes five to seven years. Behind-the–meter generation, building your own power plant on your own site bypasses the grid completely. That is the escape route. Then there are the emerging paths, geothermal, nuclear, better transmission technology. Each of these have a different timeline and a different probability of succeeding.

Leopold is not spread across all nine. He is concentrated in two, the ones that deliver power on the timescale AI needs it, not the timescale the grid operates on. His largest positions are a fuel cell company and a set of bitcoin miners. To understand why, you need to understand what each of those businesses is.

Bloom Energy was Aschenbrenner's largest position at the time of his Q4 2025 filing: $876 million, 21% of the portfolio. After last week's Oracle deal sent the stock up 60%, that position is worth roughly $2.2 billion.

Bloom makes solid oxide fuel cells (SOFCs). The distinction from a gas turbine matters. A gas turbine burns natural gas: combustion, a spinning shaft, a generator. An SOFC converts natural gas to electricity electrochemically, the same basic principle as a battery but with fuel flowing through continuously, which means there is no spinning parts or combustion. The result is 54% electrical efficiency (versus 35% for a simple-cycle gas turbine), rising above 90% when you capture the waste heat. Emissions are near zero for NOx and SOx because nothing is burning.

That emissions profile is load-bearing for the investment thesis. An SOFC installation can often be permitted locally, without the air quality reviews and state PUC proceedings that a combustion turbine triggers. In a regulatory environment where permitting timelines determine project viability, that advantage converts directly to speed.

The speed is the point. A Bloom deployment takes 12 to 18 months from contract to electrons. That is faster than a gas plant (two to three years), faster than a solar farm with storage (two to four years depending on interconnection), and dramatically faster than a grid interconnection (five to seven years). The fuel cells sit on the customer’s site, behind the utility meter, and do not require a grid interconnection agreement at all.

In the first quarter of 2026, the deals came fast. Oracle signed a master services agreement for up to 2.8 GW of Bloom fuel cells to power data centers. AEP finalized a $2.65 billion, 20-year agreement for up to 1 GW. Brookfield committed a $5 billion financing framework for Bloom deployments. That is $7.65 billion in committed deals in roughly 90 days. Bloom is now racing to double its manufacturing capacity from 1 GW to 2 GW annually4.

The open question is scale. Bloom has proven the technology at 10 to 50 MW deployments. The new contracts call for hundreds of megawatts, eventually gigawatts, at single campuses. Scaling an electrochemical manufacturing process by 10x or more is not the same as scaling a software product. It requires ceramic supply chains, quality control at volume, and field reliability data that does not yet exist at the target scale. Whether Bloom can deliver 500 MW to a single campus with the same reliability it demonstrated at 50 MW is not proven. That is the bet Leopold is making. It is his largest position because he (presumably) believes the answer is yes.

The second concentration in the portfolio is a cluster of Bitcoin mining companies. Core Scientific at roughly $419 million, Riot Platforms at $78 million, Hut 8 at $40 million, plus smaller positions in Cipher Mining, CleanSpark, Bitfarms, and Bitdeer.

These are not crypto bets. They are infrastructure bets. To understand why, you need to understand the interconnection queue.

Every new generator or large electrical load that wants to connect to the US power grid must go through a formal study process managed by the regional grid operator (PJM, MISO, ERCOT, or one of the other ISOs). The grid operator has to model what happens to power flows across the entire system when the new project plugs in. Does any transmission line overload? Does any substation exceed its rating? The study identifies every piece of equipment that needs to be upgraded before the project can connect, and the applicant typically pays for those upgrades. The process has three sequential stages (feasibility study, system impact study, facilities study), each taking months to more than a year. The total timeline, from application to an executed interconnection agreement, averages five to seven years in congested regions like PJM5.

There are currently about 2,600 GW of projects waiting in interconnection queues nationwide. For context, total US installed generation capacity is about 1,300 GW. The queue is roughly twice the size of the entire existing system. Most of those projects will never be built (completion rates run 20 to 30 percent), but the real ones still have to wait behind the speculative ones while studies proceed. FERC Order 2023 attempted to fix this by shifting from serial studies to cluster studies and requiring financial deposits upfront to deter speculative filings, but the reform is still being implemented and the backlog is measured in years.

This is why Bitcoin miners are valuable to Leopold’s thesis. Miners arrived early. They applied for grid connections years ago, endured the study process, signed interconnection agreements, and built substations and cooling systems on land they own. They have the three things an AI data center needs most: a signed interconnection agreement (the legal right to pull power from the grid), physical infrastructure (land, substations, cooling), and a power contract with known pricing. Each of those took years to obtain. You cannot replicate them quickly.

Core Scientific has already pivoted significantly toward AI hosting. It signed a 12-year, 200 MW deal with CoreWeave in 2024 to convert mining capacity to AI compute hosting6. The economics make sense: AI hosting generates higher and more stable revenue per megawatt than Bitcoin mining. The rest of the mining companies face the same calculation. They can mine Bitcoin at thin margins, or they can lease their power and infrastructure to AI companies at a premium. The interconnection agreement is the asset. The Bitcoin mining was just the original use case.

Behind the meter refers to the arrangement where power is generated at the same site that it’s used, effectively bypassing the grid altogether. If time is the biggest cost, behind the meter is a tempting setup. A new interconnection to the grid takes 3-5 years. Behind the meter generation short circuits that (no pun intended), and the limiting function becomes simply how long it takes to fire up the power generation.

Meta is building ten gas plants at its Richland Parish campus in Louisiana alone7. A 200 MW plant at its New Albany, Ohio, campus, approved in 20258. A $473 million, 366 MW plant in El Paso that will exclusively serve Meta’s data center for its first five years.

The economics are straightforward. A combined-cycle gas plant costs $800 to $1,200 per kilowatt to build and produces electricity at $50 to $80 per megawatt-hour depending on gas prices. It takes two to three years from decision to first power. That is too slow for the AI training cycle (which moves in 18-month increments) but far faster than a grid interconnection. And because the plants sit behind the meter on the data center site, they bypass the queue entirely.

The constraint on this path is the gas pipeline, not the power grid. Securing a new gas interconnection is its own multi-year process, and pipeline capacity in many regions is already committed. But in Louisiana, Texas, and parts of the Midwest where pipeline infrastructure is dense, the path from decision to power is as direct as it gets for large-scale generation.

This is the ugly bridge. Burning gas to power AI while claiming carbon neutrality through offsets and renewable energy credits is not a story anyone wants to tell, but it is the story that is actually happening. For the current demand shock, behind-the-meter gas is the fastest path to hundreds of megawatts of reliable power. The hyperscalers know it. Their procurement teams are acting accordingly.

Small modular reactors (SMRs) are nuclear reactors with output under ~300 MW, designed to be factory-built in modules and shipped to site on trucks rather than custom-constructed on location like traditional gigawatt-scale plants (Vogtle, for example). Think: Ikea furniture equivalent of nuclear power plants. The pitch is shorter construction timelines, lower upfront capital, and standardized designs that get cheaper with each unit.

NuScale was the furthest along. It had an NRC design certification, a customer (Utah Associated Municipal Power Systems), and a site. In late 2023, the project was canceled when costs rose from $58 to $89 per megawatt-hour and the customer walked away9.

Kairos Power, X-energy, and TerraPower are still developing their designs. Kairos uses fluoride salt cooling. X-energy uses high-temperature gas. TerraPower’s Natrium design uses liquid sodium. All three are technically interesting, however none will produce commercial power before 2030 at the earliest. NRC licensing alone takes years. First-of-a-kind construction risk is severe, as every nuclear project in recent US history has demonstrated.

An obvious question: if you can put a gas plant behind the meter, why not a reactor? Skip the grid entirely, put an SMR on your data center campus. Some micro-reactor companies, like Sam Altman’s Oklo, are pitching exactly this. The problem is that a behind-the-meter gas plant needs air quality permits. A behind-the-meter nuclear reactor needs NRC site-specific licensing, a security perimeter, an emergency planning zone, armed guards, spent fuel storage, and a decommissioning bond. The physical footprint might be small, but the regulatory footprint is anything but.

For the demand shock happening right now, between 2024 and 2028, small modular reactors will unfortunately not contribute anything. The technology may matter in the 2030s, but it does not matter for the capital allocation decisions being made today. This is relevant because nuclear power purchase agreements (PPAs) are being signed by hyperscalers (Microsoft with Constellation for Three Mile Island Unit 1 restart, Google with Kairos, Amazon with X-energy and Talen), but the power from these won’t get delivered for a few years.

Traditional geothermal requires naturally occurring underground heat near the surface, limiting it to Iceland, parts of California, and a few spots in Nevada. Fervo Energy changed the question by applying horizontal drilling techniques from the fracking revolution to geothermal wells. Drill deep, fracture hot rock, circulate fluid, extract heat. Their insight was that the oil and gas industry have spent decades perfecting precision drilling and hydraulic stimulation. That entire workforce and technology base transfers to generating geothermal energy.

Google is the signal to watch here. In 2023, Fervo’s pilot project in Nevada (Project Red) delivered 3.5 MW of 24/7 carbon-free energy to the grid supplying Google’s data centers. That was proof of concept. Then Google kept going: a 400 MW project in Beaver County, Utah (Cape Station), with first power expected by 2026 and full operation by 2028. Fervo raised $462 million Series E round in December 2025, with Google participating. In April 2026, a non-binding framework agreement for up to 3 GW of geothermal capacity by 2033 was signed between Google and Fervo10.

Three gigawatts is serious. That is more than the entire existing US geothermal fleet. Google is not doing this for the press release — it has access to better energy market data than most utilities, and it is writing checks that only make sense if the technology works at scale.

Fervo’s pilot results suggest costs could reach $50 to $70 per megawatt-hour. The output is baseload (runs 24/7, unlike solar or wind), carbon-free, and has a small physical footprint. Scaling from a pilot well field to gigawatts requires proving that the drilling economics hold across different geologies, that reservoir performance sustains over years, and that the supply chain for deep drilling rigs can support dozens of simultaneous projects. Those are real questions. But if the answers come back positive, geothermal is the only option that runs 24/7, produces zero carbon, and does not need the grid.

This is the path nobody talks about.

The rated capacity of a transmission line is based on worst-case assumptions: hottest day of the year, no wind, maximum conductor sag. In reality, conditions are usually better. Dynamic line rating (DLR) systems, built by companies like LineVision, attach sensors to existing lines that measure actual conductor temperature and wind conditions in real time, allowing operators to push 20 to 40% more power through the same wires. Advanced power flow controllers from companies like Smart Wires actively redirect electricity across parallel transmission paths, reducing congestion on overloaded lines by shifting load to underutilized ones. Topology optimization software reconfigures switching patterns to improve flows with no new hardware at all.

DLR sensors cost thousands of dollars per mile. A new transmission line costs millions per mile. The capacity gain is immediate. Installation takes months. Permitting is trivial compared to new construction. By any rational engineering or economic metric, grid-enhancing technologies should be deployed across every congested transmission corridor in the country.

They are not deployed at scale, and the reason is structural. US utilities operate under cost-of-service regulation: they earn a rate of return on capital they invest. Build a $2 billion transmission line, earn a regulated return on $2 billion for 40 years. Install $20 million in DLR sensors that deliver comparable capacity gains, earn a return on $20 million. The utility’s financial incentive is to build new expensive things, not to optimize existing ones. This is not a conspiracy; it is the predictable outcome of a regulatory structure designed for a different era.

FERC Order 1920 (2024) included provisions encouraging the adoption of such grid enhancing tech, but “encouraging” is not “requiring,” and utility incentive structures remain unchanged. This is a pure market failure: a proven, cheap, fast technology that does not get deployed because the entities responsible for deployment are financially penalized for using it.

Readers familiar with power transmission likely know that most of the world transmits power in the form of AC (alternating current). The reasons are mostly rooted in history, but recent advances in technology have made possible the transmission of high voltage power in a DC (direct current) form.

China has built over 10,000 miles of high-voltage direct current transmission lines, carrying hydropower from western provinces to eastern load centers across distances that would lose unacceptable amounts of energy on AC lines. The US has almost none.

HVDC converts alternating current to direct current at one end, transmits it over long distances with very low losses, and converts back at the other end. It also allows connecting the three US interconnections (Eastern, Western, ERCOT) that cannot share AC power directly. The total transfer capacity between the Eastern and Western Interconnections today is approximately 1,300 MW, carried by a handful of small DC links. A single hyperscale campus now draws 300 to 500 MW. The bridges between the three machines are smaller than one announced campus.

Two major US HVDC projects are under construction. SunZia, 550 miles from New Mexico to Arizona, will deliver 3,500 MW and is the largest clean energy infrastructure project in US history. Champlain Hudson Power Express will carry Canadian hydropower to New York City. Each took roughly a decade from conception to construction start. The Clean Line Energy projects, well-funded and well-designed HVDC proposals, failed entirely due to permitting opposition and state-by-state siting fights.

The pattern is clear. HVDC is the right long-term technology for moving large amounts of power across the US. The US institutional and regulatory environment makes building it extraordinarily difficult. Each project faces NEPA review, state siting authority in every state it crosses, eminent domain battles, and cost allocation disputes. A single landowner or a single state commission can delay a billion-dollar project for years.

A microgrid assembles solar panels, batteries, small generators, and sometimes fuel cells into a locally managed power system that can operate independently of the main grid. This works well at the 1 to 20 MW scale: a military base, a hospital complex, a remote facility.

It does not work at hyperscale. An AI training cluster needs hundreds of megawatts to gigawatts of continuous, perfectly reliable power. Assembling that from dozens of small distributed sources, each with its own intermittency profile and failure mode, does not match the reliability requirement. No hyperscaler is building a gigawatt-scale microgrid. The concept solves a different problem.

Leopold’s portfolio is a thesis about time.

Fuel cells deliver power in 12 to 18 months. Bitcoin miner conversions deliver power now, because the infrastructure already exists. Gas plants deliver in two to three years. Geothermal might deliver in five. Nuclear might deliver in ten. Grid reform and HVDC might deliver in twenty. He is concentrated in the paths that produce megawatts on the timescale AI companies will pay for them, not the timescale regulators, utilities, and construction crews operate on.

You can disagree with his specific positions. Maybe Bloom cannot scale manufacturing fast enough. Maybe the Bitcoin miners are overvalued relative to their power contracts. Maybe gas plants face emissions regulations that slow them down. But the structural read is hard to argue with: the market has spent two years pricing in AI compute demand and almost no time pricing in the physical infrastructure that makes compute possible. The semiconductor supply chain responds to price signals on 18-month cycles. The power grid responds on 10-to-20-year cycles. That mismatch is the trade.

This newsletter covers the plumbing. Each piece that follows goes deeper into these questions.

If the power problem determines who wins the AI buildout, understanding it early is worth real money. That goes for hedge funds sizing infrastructure bets, developers choosing sites, and regulators deciding how fast to let it all happen. The demand is here. The grid is not.