Let’s say you want to start a data center. You have the land for it, you have the permits to build your data center, the GPUs have been ordered and will arrive on schedule, and you have secured the capital. None of this matters, however, until you clear the interconnection queue: the federal process that every new power plant and every large electrical load must service before a single electron flows. If you were to start this process today, it would take you 5-7 years to clear it.

The interconnection queue is where energy projects die. And it is the single biggest bottleneck in the AI buildout that no one outside the industry is talking about.

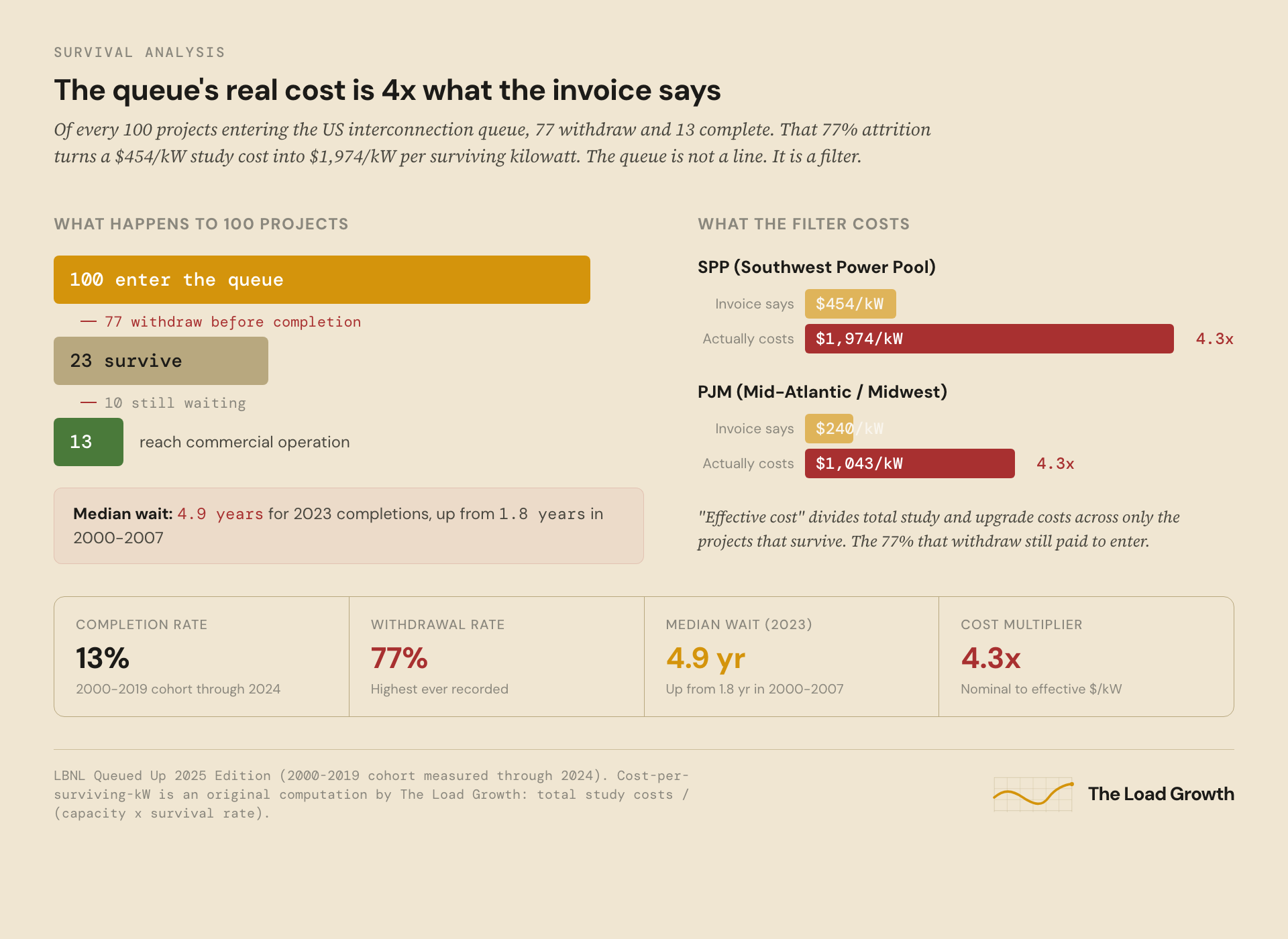

Here is what dying in the queue actually costs. In SPP (the Southwest Power Pool, the grid operator covering 14 states from the Dakotas to Oklahoma), the operator studies what transmission upgrades are needed to connect your project, and you, the developer, pay for them: $454 per kilowatt on average. But for every project that survives to completion, roughly three others paid study fees, waited years, and withdrew with nothing. When you spread the total cost the industry sinks into interconnection across only the projects that make it through, the effective price is $1,974 per kilowatt. A 200 MW solar farm’s invoice says $91 million. The true cost to the industry per project that reaches the grid is $395 million.

The queue is not a waiting room. It is a filter. And we can now measure exactly what that filter costs.

Between 2000 and 2019, thousands of generation projects entered the US interconnection queue. By the end of 2024, the outcomes break down as follows.

For every 100 projects that entered the queue

77 withdrew

13 reached commercial operations

10 are still waiting

That 13% completion rate is the headline, but the trend underneath is way worse. The median time from interconnection request to commercial operation was 1.8 years for projects entering in 2000-2007. For projects completing in 2023, it was 4.9 years. The queue got nearly three times slower in two decades.

Any new generator or large load that wants to connect to the bulk transmission system must file an interconnection request with the relevant operator. The request triggers a set of engineering studies that determine what the new injection or withdrawal does to every other power flow on the grid. This is not a permit application or a tariff negotiation. It is a physics exercise.

There are two flavors. A generation interconnection request is filed by a new power plant that wants to sell electricity into the wholesale market. A load interconnection request is filed by a large consumer, typically a data center campus, that wants to buy power directly from the transmission system. Most of the 2,290 GW backlog is generation (solar, wind, gas, storage). But large-load interconnection requests are surging: ERCOT (the Texas grid) alone saw a roughly 300% increase in large-load requests in 2024, driven almost entirely by data centers.

The interconnection study process is serial and interdependent. When the grid operator models your project, it models every other project ahead of you in the queue at the same time. If one of them withdraws, the entire study restarts. One departure can reset the clock for dozens of projects behind it. In PJM (the grid operator covering 13 states from New Jersey to Illinois, the largest power market in the US), a single withdrawal in a congested zone could add 18 months to every project behind it.

The result is a system that punishes patience. The longer you wait, the more likely someone ahead of you withdraws. More withdrawals = more studies = longer wait.

Until 2023, it cost almost nothing to enter the queue. A developer could file an interconnection request with a $50,000 deposit, tie up study capacity for years, and walk away with no consequences. Thousands did. The queue filled with speculative projects that were never going to get built, and the real projects behind them waited years for studies that had to restart every time a speculative one withdrew.

FERC (the Federal Energy Regulatory Commission) decided the fix was money. Order 2023, issued in July 2023, replaced the token deposit with a capital-at-risk structure designed to make entering the queue hurt. A 50 MW project facing SPP-level upgrade costs ($454/kW, the national high) now puts up $85,000 at entry, $1.1 million at the restudy milestone (5% of assigned network upgrades), and $2.3 million at the facilities stage (10%). So for a 50MW project, the skin in the game is $3.5 million.

For a 500MW project, the skin in the game is $34.3 million, 686 times the previous deposit requirements.

The logic is brutal but deliberate. If you cannot put up $34 million in non-refundable deposits, you are not serious, and you should not be in the queue consuming study resources that delay the projects behind you. FERC is weaponizing the filter: making it kill projects faster so the survivors get through sooner.

Is it working? Too early to say. PJM’s Transition Cluster 1, the first batch under the new rules, cleared 17.4 GW across 128 projects. At that throughput, PJM’s remaining 30 GW backlog will take about 5.2 years to process.

MISO (the Midcontinent Independent System Operator, covering 15 states from Montana to Louisiana) is targeting a 373-day study cycle for its DPP 2025 intake of 55 GW. If the target holds, MISO will clear its 170 GW backlog in 3.1 years.

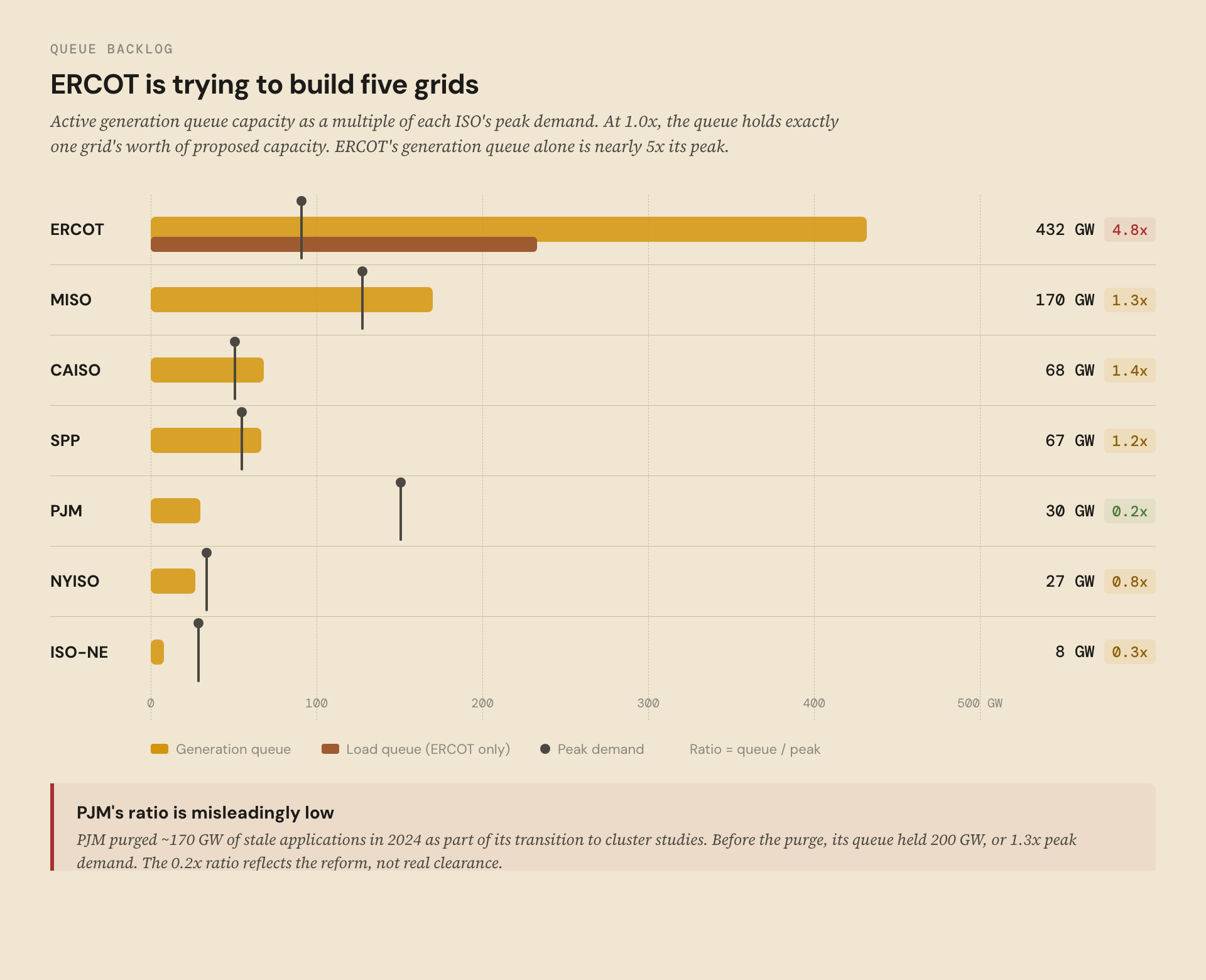

The backlog is not distributed evenly. The US grid is operated by seven regional bodies called ISOs (Independent System Operators) or RTOs (Regional Transmission Organizations). Some are drowning. Others have cleared the decks.

ERCOT (the Electric Reliability Council of Texas, the only major US grid operator not under federal jurisdiction) has a generation queue holding 432 GW of proposed projects against a system with 90 GW of (current) peak demand. That is 4.8x oversubscription: nearly five grids’ worth of capacity trying to plug into one. ERCOT also carries a separate load queue of 233 GW (2.6x peak), roughly 70% of which is data centers.

MISO’s queue holds 170 GW against 127 GW of peak demand (1.3x). SPP holds 67 GW against 54 GW (1.2x). Both are manageable if the new cluster study timelines hold, unmanageable if they do not.

PJM’s ratio is misleadingly low at 0.2x. In 2024, PJM purged roughly 170 GW of stale applications as part of its transition to cluster studies. Before the purge, its queue held 200 GW, or 1.3x peak demand. The 0.2x ratio reflects the reform, not real clearance. Those 170 GW of projects did not get built. They got deleted.

CAISO (the California Independent System Operator) received 347 GW of applications in its Cluster 15 study, of which 68 GW survived the initial screening. Even the survived figure (1.4x peak demand) understates the pressure: California’s queue is dominated by solar-plus-storage projects competing for the same transmission corridors in the Central Valley and Mojave Desert, creating localized congestion that the aggregate ratio does not capture.

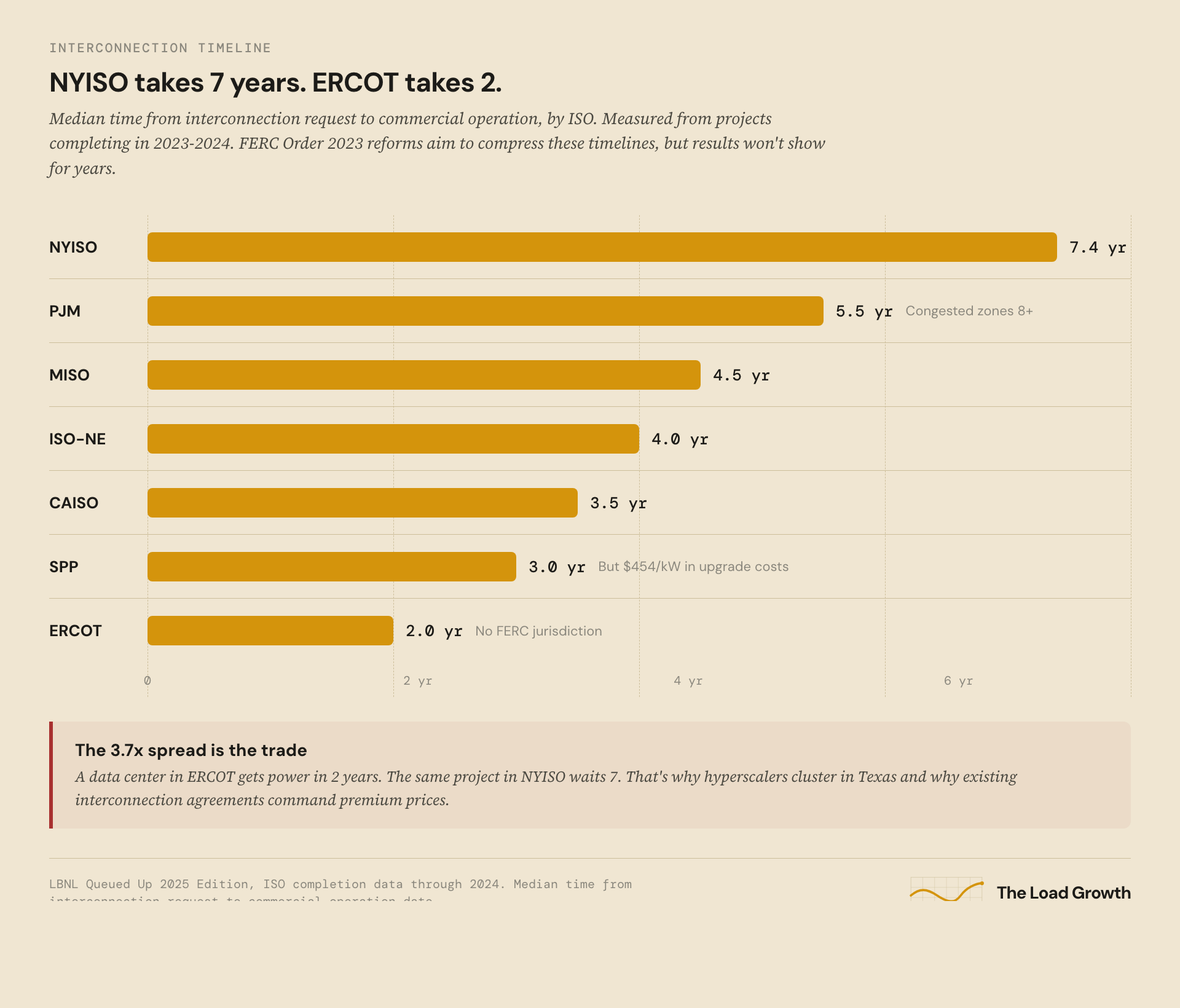

The consequence of the filter is time, which varies enormously by geography.

A project completing in NYISO (the New York Independent System Operator) in 2024 waited a median of 7.4 years from its interconnection request. In PJM, 5.5 years (longer in congested zones, where waits exceed 8 years). In ERCOT, 2 years.

The 3.7x spread between NYISO and ERCOT explains the geography of the AI buildout. It is why Meta, Google, and Amazon are clustered in Texas. It is why ERCOT’s data center load queue has exploded to 233 GW. And it is why existing interconnection agreements in congested ISOs command premium prices: they represent years of waiting that cannot be replicated.

SPP offers an interesting case. At 3 years, it is among the fastest of the FERC-jurisdictional ISOs. But its speed comes at a price: $454/kW in network upgrade costs, the highest in the country. The grid in SPP’s territory (the Great Plains) was built for light loads and long distances. Every new wind or solar farm in western Kansas, for example, needs hundreds of miles of new transmission to reach demand centers. SPP is fast because it charges enough to make speculative projects withdraw early. The filter is explicit there; it is just priced into the study invoice rather than the waiting time.

If the queue is a filter, then the output of the filter (a completed interconnection agreement) is a scarce asset with a measurable value.

In 2024, Amazon paid $650 million for a data center campus adjacent to the Susquehanna nuclear plant in Pennsylvania. The deal included 300 MW of capacity, existing site infrastructure, and, critically, a signed interconnection agreement in one of PJM’s most congested zones. That works out to $2,167 per kilowatt. A new project entering PJM’s queue today would face 5-7 years of studies plus $240/kW in upgrade costs (if it is one of the 23% that survives). Amazon paid a premium to skip the line entirely.

Core Scientific, the Bitcoin miner in Leopold Aschenbrenner’s portfolio, signed a 12-year, 200 MW hosting deal with CoreWeave. The deal works because Core Scientific already has the interconnection agreement. The mining operation was the original use case; the AI hosting deal monetizes the infrastructure at a higher margin.

The opportunity cost math makes these premiums rational. A 500 MW data center waiting five years in the queue foregoes roughly $350 million per year in potential revenue at $100/MWh and 80% capacity factor. That is $1.8 billion in foregone revenue over the wait. Against that number, paying $650 million for an existing agreement is a discount, not a premium.

The interconnection queue decides which of the nine paths to powering AI data centers actually gets built. It is the mechanism through which the 2,290 GW of proposed US generation capacity gets reduced to the roughly 300 GW that will reach commercial operation. Everything upstream of the queue (project development, financing, equipment procurement) is contingent on clearing it. Everything downstream (construction, commissioning, revenue) cannot begin until it clears.

The filter has three consequences for anyone allocating capital to the AI power buildout:

Behind-the-meter generation (fuel cells, on-site gas plants) is not an inferior alternative to grid power. It is a rational response to a broken queue. The premium you pay for BTM electricity ($120-180/MWh for fuel cells versus $40-60/MWh for grid power) is less than the opportunity cost of waiting 5-7 years for a grid connection. Leopold Aschenbrenner’s portfolio is a bet on this math.

Existing interconnection agreements are the new scarce asset in the energy transition. Their value will increase as AI load grows faster than the queue can process it. The Bitcoin miners, nuclear plant adjacencies, and industrial sites with legacy grid connections are all trading at premiums that reflect this scarcity.

FERC Order 2023 will make the filter more efficient but not faster in aggregate. The increased deposit will kill speculative projects and reduce the withdrawal rate over time. But the backlog of projects already in the queue still has to be processed, and the upgrade costs for real projects are not getting cheaper. The queue will get more selective, not shorter.

The wires problem is not a backlog that clears with better process. It is a structural mismatch between how fast the semiconductor industry can build demand for power and how fast the transmission system can deliver it. The queue is where that mismatch becomes visible, and where its cost becomes measurable.

But as with everything, nature finds a way. More on that in the next post.