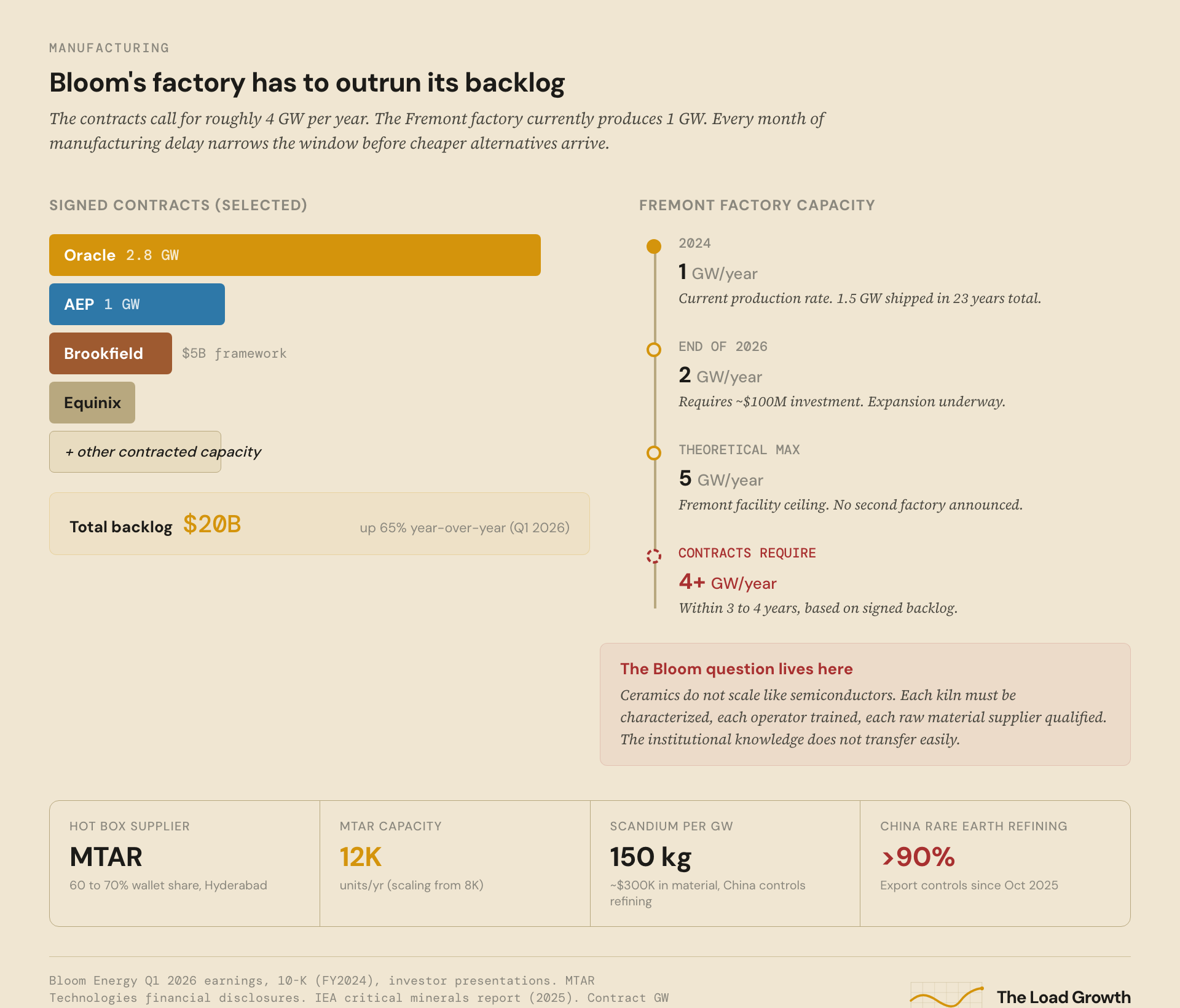

Bloom Energy's backlog went from modest to absurd in 90 days. Oracle signed for 2.8 GW. AEP committed $2.65 billion for 1 GW. Brookfield put up a $5 billion financing framework. By the end of Q1 2026, the company reported a total backlog of roughly $20 billion, up 65% from a year earlier1. It had shipped about 1.5 GW in its entire 23-year history. The contracts on the books call for multiples of that.

The demand question is settled. Hyperscalers will pay a premium for fuel cells because the alternative is waiting five to seven years in the interconnection queue. That math was the subject of Piece 1. This piece is about the other side of the equation.

Can Bloom actually build them?

That is the Bloom question. It is also Leopold Aschenbrenner’s largest bet. His position was worth roughly $2.2 billion after the Oracle deal. The stock has since roughly doubled again, riding the backlog higher. If Bloom delivers, the position keeps compounding. If it cannot scale manufacturing from 1 GW per year to the 4+ GW per year its contracts imply, the company is a $65 billion market cap built on a promise.

The answer is not obvious. Scaling a ceramic electrochemistry business by 4x is not like scaling a software product, and it is not like scaling a gas turbine factory. It requires a supply chain that barely exists at the volume needed, a rare metal that mostly comes from China, and field reliability data at a scale no one has ever tested.

Here is what we know.

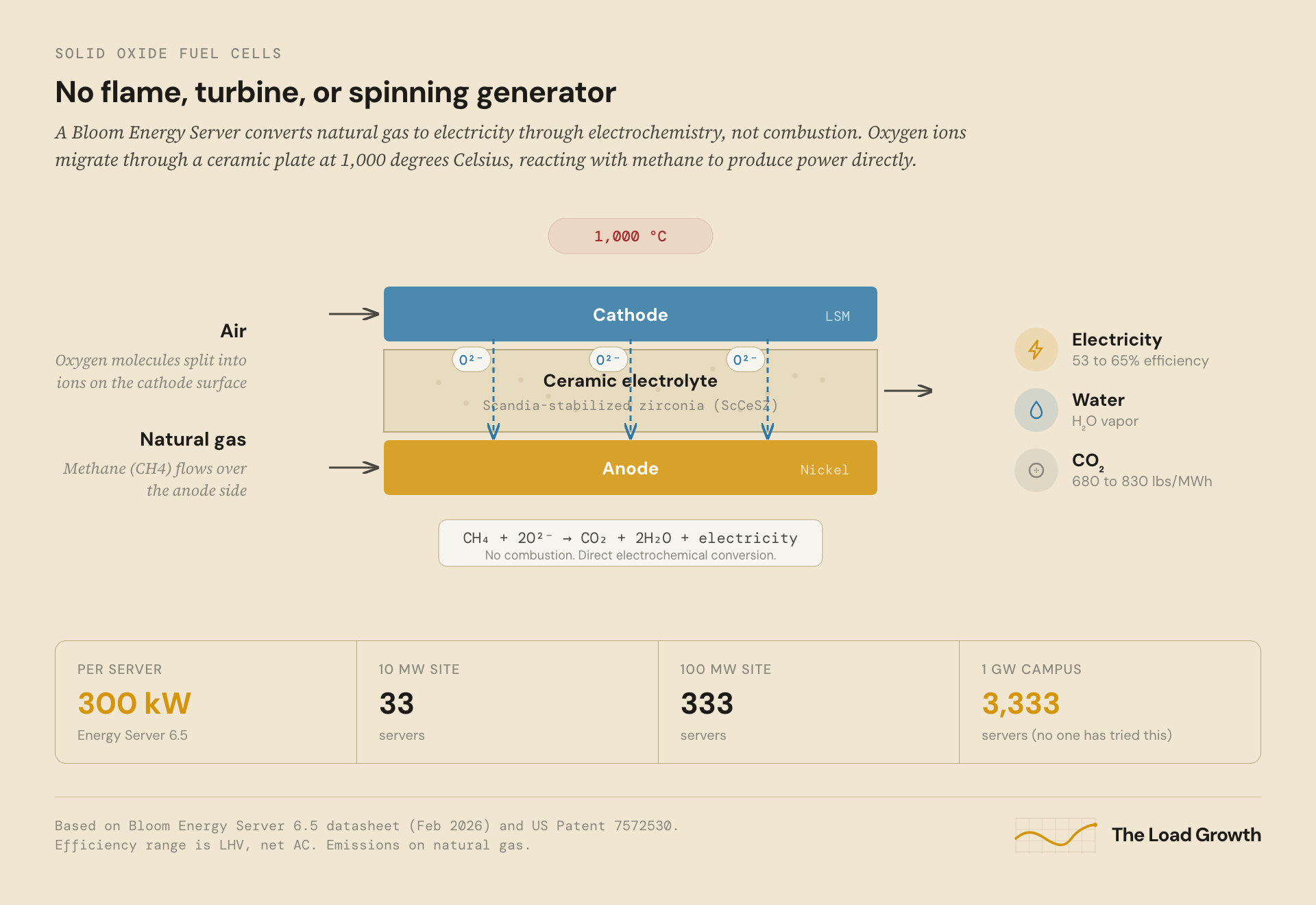

A Bloom Energy Server is a stack of solid oxide fuel cells. Each cell is a thin ceramic plate, roughly 100 by 100 millimeters, made primarily of scandia-stabilized zirconia (ScCeSZ). Scandium oxide, or scandia, is doped into the zirconia crystal structure because it provides higher ionic conductivity at operating temperatures than the more common yttria-stabilized alternative2. That conductivity is the entire mechanism.

Natural gas flows over one side of the plate. Air flows over the other. At roughly 1,000 degrees Celsius, oxygen molecules on the air side split into ions, migrate through the ceramic, and react with the methane on the fuel side. The reaction produces electricity, water, and carbon dioxide directly, without combustion. All without a flame, turbine, or spinning generator.

The result is 53 to 65% electrical efficiency, depending on conditions, roughly 50% better than a simple-cycle gas turbine and competitive with combined-cycle plants3. Capture the waste heat and total efficiency exceeds 90%. Because nothing burns, NOx and SOx emissions are near zero.

Each cell produces a small voltage. Bloom stacks cells into columns, coats them with a nickel-based anode on one side and a lanthanum strontium manganite cathode on the other, then assembles the columns into a “hot box” packaged inside a unit called an Energy Server. The current model, the Server 6.5, is rated at 300 kW. A 10 MW installation is 33 servers. A 100 MW installation is 333 servers. A gigawatt is 3,333 servers. The modularity is the point: you do not build a gigawatt plant, you deploy 3,333 identical units.

That sounds simple, but it’s not.

Every Bloom fuel cell starts as a powder. Scandia-stabilized zirconia is milled to a precise particle size, mixed with binders, tape-cast into thin sheets, and fired in a kiln at temperatures above 1,300 degrees Celsius. The firing process is where the physics gets unforgiving. Ceramic sintering is sensitive to temperature gradients, atmosphere composition, heating rate, and impurities at the parts-per-million level. A batch that fires 20 degrees too hot warps. A batch with slightly wrong humidity cracks. Quality control is not statistical sampling at the end of the line. It is control of every variable at every step.

Then each plate gets coated with electrode materials on both sides. These are applied as slurries, dried, and fired again. The interfaces between layers determine how efficiently ions transfer, which determines how much power the cell produces, which determines the economics of the entire system.

The cells go into hot boxes, the sealed high-temperature modules at the core of each Energy Server. Bloom does not make all of these in-house. MTAR Technologies, based in Hyderabad, India, manufactures the hot box assemblies and holds an estimated 60 to 70% wallet share of that critical component. MTAR is scaling from 8,000 to 12,000 hot box units per year. A single supplier in a different country making the core component of a product with a $20 billion backlog is a supply chain fact worth noting.

Bloom’s factory in Fremont, California produces roughly 1 GW of fuel cell capacity per year. The company has announced plans to reach 2 GW by the end of 2026, requiring approximately $100 million in investment. Bloom says the Fremont facility could theoretically scale to 5 GW with further expansion. No second factory has been announced. Its contracted pipeline implies needing 4 GW or more per year within the next three to four years.

The gap between 1 GW and 4 GW is where the Bloom question lives. The chemistry works. The question is whether a ceramic manufacturing process that has been tuned over two decades at one factory can be quadrupled in volume without the defect rates that killed earlier attempts at high-volume SOFC production.

Ceramics do not scale like semiconductors. You cannot just add shifts and buy more kilns. Each new kiln must be characterized, each operator trained, each raw material supplier qualified. The institutional knowledge in a ceramic production line is deep and largely unwritten. Bloom’s Fremont facility has been iterating on its process for over a decade. That institutional knowledge does not transfer easily.

There is a supply chain problem underneath the manufacturing problem, and it involves a metal most people have never heard of.

Bloom is reportedly the world’s largest consumer of scandium. The company uses an estimated 130 to 150 kilograms of scandium per gigawatt of production. At 2 GW per year, that is 260 to 300 kilograms. At 4 GW per year, over half a metric ton. Scandium oxide at 99.9% purity costs $1,400 to $2,000 per kilogram. The total material cost is manageable. The supply concentration is not.

China controls roughly 60% of mined rare earth production and over 90% of global rare earth refining4. In October 2025, China announced new export controls on rare earth elements, requiring licenses for components containing Chinese-sourced materials. Scandium is not a high-profile target in the way that gallium or germanium have been, but it sits within the same export control regime.

If you are an investor sizing the Bloom position, this is the kind of risk that does not show up in a standard bull/bear framework. The technology works. The demand is firm. The factory exists. And the single most critical input to the ceramic electrolyte comes from a supply chain that a single government could restrict with one policy decision. Bloom has been working to diversify its scandium sourcing, but “working to diversify” and “diversified” are different states.

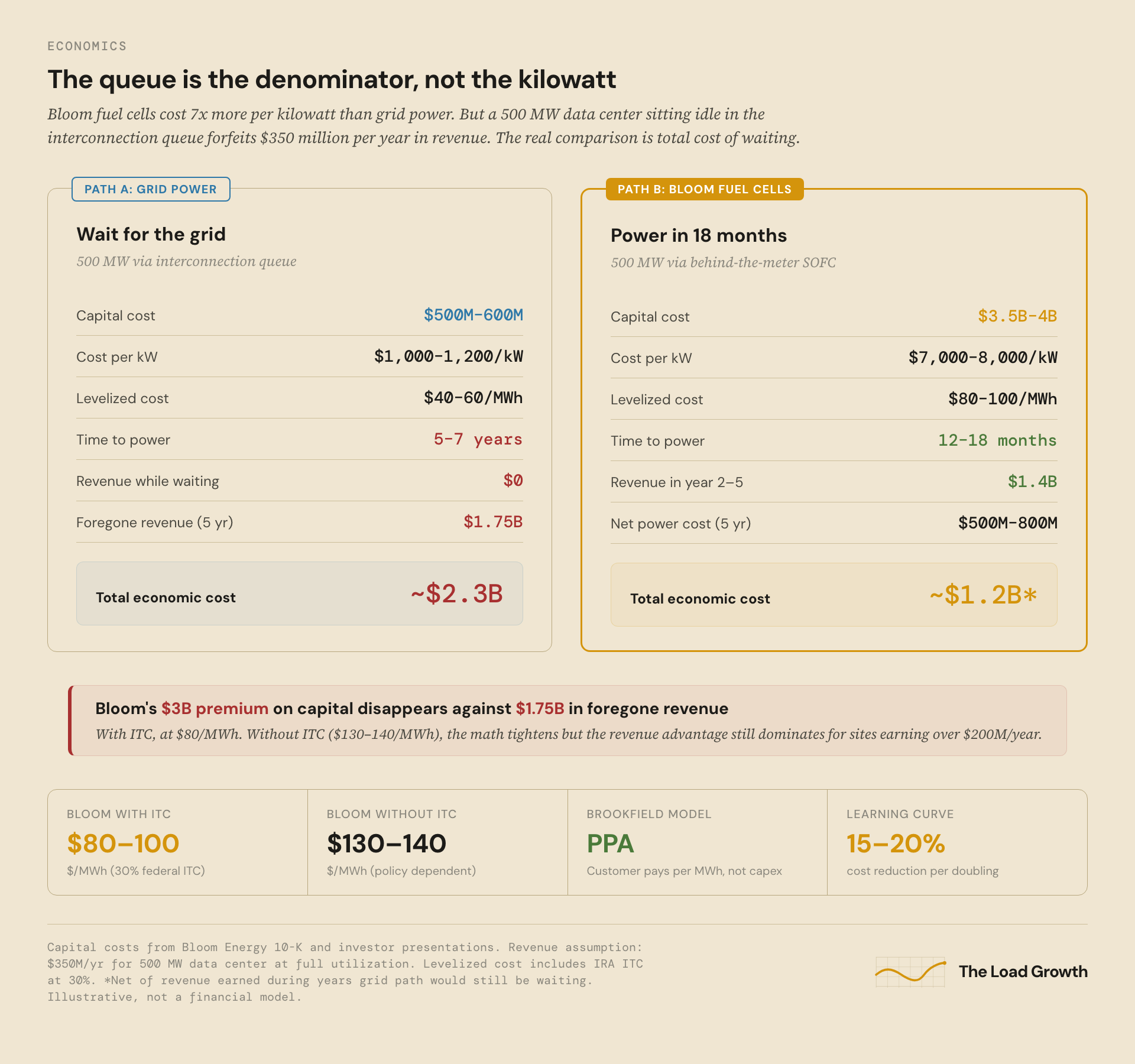

Bloom’s installed cost has historically been in the range of $7,000 to $8,000 per kilowatt for commercial installations. For comparison, a combined-cycle gas plant costs $800 to $1,200 per kilowatt. A simple-cycle peaker costs $400 to $700. By any conventional measure of capital cost per unit of capacity, fuel cells are expensive.

The comparison is misleading.

A combined-cycle gas plant at $1,000 per kilowatt requires a site, a gas interconnection, air quality permits, a state public utility commission review, and a grid interconnection agreement. Elapsed time: two to four years. Total cost including soft costs and permitting: often $1,500 to $2,000 per kilowatt by the time it actually produces power. And the five-to-seven-year interconnection queue timeline applies to the grid connection, not the plant construction.

A Bloom installation at $7,000 per kilowatt ships to a customer site, connects to an existing gas line, and produces power in 12 to 18 months. It skips the grid interconnection, the PUC review, and in most jurisdictions the air quality hearing, because there is no combustion. The customer pays more per kilowatt of capacity but gets power years sooner, and the levelized cost comparison shifts when you factor in the revenue a data center earns during those years of avoided waiting.

The Brookfield financing structure makes this explicit. Brookfield’s $5 billion framework is not a loan to Bloom. It is a project finance structure where Brookfield owns the fuel cell installations and sells power to the end customer under long-term agreements, the same power purchase agreement model that solar and wind developers use5. The customer pays per megawatt-hour, not per kilowatt of installed capacity. Brookfield takes the technology risk. The customer takes a power contract at a known price.

On a levelized basis, Bloom power for data centers runs $130 to $140 per megawatt-hour without government incentives, or $80 to $100 per MWh with the 30% federal investment tax credit from the Inflation Reduction Act. The ITC matters. Without it, fuel cells are expensive power. With it, they are competitive with grid power in some constrained markets. That policy dependency is worth flagging: the ITC has bipartisan support today, but “today” is the only day that counts in Washington.

For a 500 MW data center that generates $350 million per year in revenue at full utilization, a $130/MWh power cost looks different when the alternative is $0 in revenue for five years while waiting for a grid connection. The opportunity cost of the queue is the real denominator.

As Bloom scales production, unit costs should fall. Ceramic manufacturing has well-documented learning curves: each doubling of cumulative production historically reduces unit cost by 15 to 20%. Bloom’s newer Packaged Energy Server platform has already reduced installation costs by roughly $500 per kilowatt. If cumulative deployment doubles from 1.5 GW to 3 GW over the next two years, which the backlog implies, installed cost should come down toward the $5,000 to $6,000 per kilowatt range.

Every Bloom fuel cell runs on natural gas. At a heat rate of roughly 6,500 BTU per kilowatt-hour (the midpoint of Bloom’s published range), a 1 GW installation consumes approximately 156 million cubic feet of gas per day. The Oracle contract alone, at 2.8 GW, would require roughly 437 million cubic feet per day, or about 0.4% of total US daily natural gas production.

That is not an enormous number in the context of US gas markets. The US produces about 104 billion cubic feet per day. The gas is available. The question is whether the pipeline is.

Natural gas does not teleport. It flows through a network of interstate and intrastate pipelines, and securing capacity on those pipelines for a new large industrial load requires its own process of applications, studies, and sometimes new construction. In regions with excess pipeline capacity (parts of Texas, Louisiana, the Permian Basin corridor), connecting a fuel cell installation to gas is straightforward. In the Northeast, where pipeline capacity has been constrained for a decade due to opposition to new construction, it is a bottleneck.

This is the irony of the fuel cell value proposition. Bloom installations bypass the electrical interconnection queue. They do not bypass the gas system. In regions where pipeline capacity is tight, you are trading one queue for another. The gas queue is generally shorter (months, not years) and less encumbered by federal study processes, but it is not zero. Oracle’s Project Jupiter, for example, is sited in Dona Ana County, New Mexico, where Permian Basin gas infrastructure is accessible. That is not a coincidence6.

Bloom’s fuel cells can run on hydrogen or biogas without hardware modifications, just a change in the fuel feed. On hydrogen, Bloom claims 60% electrical efficiency and zero carbon emissions. This is technically true and commercially irrelevant at the scales being discussed. There is not enough green hydrogen or biogas in the United States to fuel a single 500 MW installation, let alone the gigawatts in Bloom’s pipeline. The theoretical fuel flexibility is a hedge for a future that is years away. The present reality is natural gas.

The emissions math follows. A Bloom SOFC produces roughly 680 to 830 pounds of CO2 per megawatt-hour from natural gas, depending on the specific efficiency of the installation7. A combined-cycle gas turbine produces roughly 800 to 900 pounds per MWh. A simple-cycle peaker produces 1,200 or more. The US grid average is around 1,000 pounds per MWh. Bloom is cleaner than a peaker and cleaner than the grid average, but comparable to a combined-cycle plant on carbon. The environmental advantage is local air quality (no NOx, no SOx, no particulates), not greenhouse gas emissions.

Every hyperscaler buying Bloom fuel cells has a net-zero carbon pledge. Every one of them will meet it through purchased offsets and renewable energy credits, not through the fuel cells themselves. The fuel cells produce power. The offsets produce the narrative.

The honest answer is: nobody at Bloom’s scale for this application.

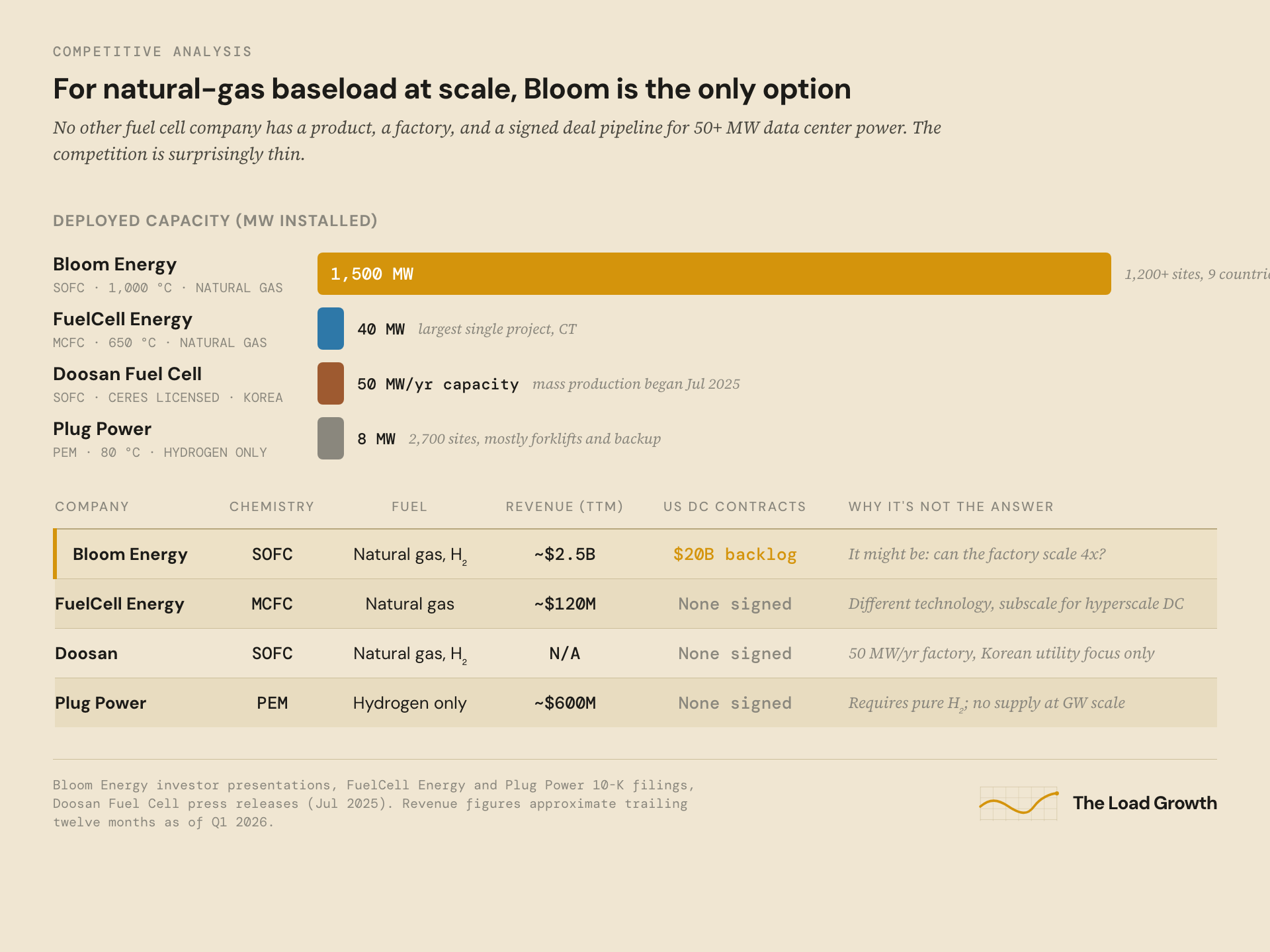

Per industry estimates, Bloom holds roughly 60% of global stationary SOFC shipments. It has 1.5 GW installed across more than 1,200 sites in nine countries. The next largest SOFC competitor is not close.

FuelCell Energy in Danbury, Connecticut, makes molten carbonate fuel cells. Different chemistry and operating temperature (650 degrees Celsius versus Bloom’s 1,000), different economics. FuelCell Energy has demonstrated a 40 MW project in Connecticut, but its annual revenue is a fraction of Bloom’s $2 billion, and its product is oriented toward distributed generation and carbon capture, not hyperscale data center power.

Plug Power makes PEM (proton exchange membrane) fuel cells, which run on hydrogen at much lower temperatures (80 degrees Celsius). PEM cells are efficient at small scales and respond quickly to load changes, which makes them suited for forklifts and backup power. They are not suited for baseload power at the hundreds-of-megawatts scale because they require pure hydrogen as fuel. Plug’s stationary installed base is about 8 MW across 2,700 sites, orders of magnitude smaller than Bloom’s.

The most credible challenger is Doosan Fuel Cell in South Korea, which began mass production of SOFCs in July 2025 using technology licensed from Ceres Power. Doosan’s new factory in Jeollabuk-do has a capacity of 50 MW per year8. That is one-twentieth of Bloom’s current 1 GW. Doosan has signed a 20-year power purchase agreement with KEPCO, the Korean utility, but has no signed contracts in the US data center market.

The competition is surprisingly thin. For natural-gas-fueled, baseload power at the 50 MW to multi-gigawatt scale, with deployments measured in months rather than years, Bloom is effectively the only option with proven product, a manufacturing line, and a signed deal pipeline. That is a bull case (pricing power, margin expansion) and a bear case (single point of failure for the entire fuel cell path) at the same time.

Solid oxide fuel cells degrade. The ceramic electrolyte, the electrode interfaces, the seals between cells in a stack: all of them accumulate damage over thousands of hours of operation at 1,000 degrees Celsius. Industry benchmarks for comparable SOFCs suggest degradation rates of roughly 0.6% per thousand hours of operation at 750 degrees Celsius; at Bloom’s higher operating temperature, rates may differ. Bloom does not publicly disclose its specific degradation data.

Bloom’s Energy Servers are designed for stack replacement. The company’s service contracts, which run up to 25 years, include periodic swaps of the fuel cell stacks, typically every five to ten years, while the balance-of-plant infrastructure (gas connections, power conditioning, enclosures) remains in place. The all-in operation and maintenance cost runs $0.08 to $0.12 per kilowatt-hour under these agreements, which means stack replacement costs are baked into the per-MWh price the customer pays.

At 80 MW, Bloom has field data. Its largest single-site installation, the SK Eternix ecopark in South Korea, is 80 MW and has been operating9. At 500 MW or 1 GW, no one knows. A gigawatt is 3,333 Energy Servers operating simultaneously, each with its own thermal management, fuel flow, and electrical output. The question is not whether individual cells degrade predictably, but whether managing degradation across thousands of units at a single site introduces failure modes that do not appear at smaller scales: cascading maintenance schedules, supply chain bottlenecks for replacement stacks, or correlated failures from a shared gas supply or ambient conditions.

This is not a theoretical concern. Large industrial installations of any technology encounter emergent reliability issues at scale that do not appear in smaller deployments. Bloom has never operated at the scale its new contracts require. The first gigawatt-scale campus will be the experiment.

Bloom posted its first GAAP-profitable quarter in Q1 2026: $70.7 million in net income on $751 million in revenue, more than double the year-ago quarter. Revenue guidance for full-year 2026 is $3.4 to $3.8 billion, raised from an initial $3.1 to $3.3 billion after the Q1 beat. Cash on hand: $2.52 billion. Non-GAAP gross margin: 31.5%, trending toward 34% by year-end.

The business is inflecting. For the first time in 23 years, Bloom is generating cash. Revenue more than doubled year-over-year. Margins are expanding. The $20 billion backlog with creditworthy counterparties (Oracle, AEP, Brookfield, Equinix) gives multi-year revenue visibility that most energy companies would envy. The Brookfield financing structure shifts Bloom’s model from hardware sales toward energy-as-a-service, which means recurring revenue and higher lifetime value per installation.

The real bull case is simpler: there is no alternative. For a hyperscaler that needs 500 MW in 18 months, the choice is Bloom or wait. Grid interconnection takes five to seven years. Gas plants take two to three years and require permits. Nuclear takes a decade. Bloom’s pricing power comes from the absence of competition on the timeline axis.

Bloom trades at roughly $290, implying a market capitalization near $65 billion on trailing twelve-month revenue of about $2.5 billion. That is a price-to-sales ratio above 25x. The stock has appreciated roughly 15x in the past year. A lot of good news is priced in. Possibly all of it.

Bloom has never been profitable on a full-year GAAP basis. The Q1 2026 profit was the first GAAP-positive quarter in the company’s history. One quarter does not make a trend. The manufacturing ramp from 1 GW to 2 GW requires roughly $100 million in capital expenditure, and reaching the 4 GW implied by the backlog would require substantially more, funded either by operating cash flow that is only just turning positive or by dilutive equity offerings.

Customer concentration is severe and getting worse. In the 2024 10-K, three customers accounted for 53% of total revenue. In Q1 2026, two customers accounted for roughly 62%. Oracle is on track to become the dominant customer by a wide margin. Oracle also received a warrant to purchase 3.53 million Bloom shares at $113.28 per share, a roughly $400 million embedded incentive that ties Oracle’s financial interests to the stock price. That alignment cuts both ways: if Oracle delays, scales back, or finds an alternative, the impact on Bloom’s revenue, factory utilization, and stock would be disproportionate.

The gas dependency is a regulatory risk. The same political environment that created permitting advantages for fuel cells (no combustion, no NOx) could turn hostile to the gas supply underneath them. A federal carbon tax, stricter methane regulations, or state-level moratoria on new gas infrastructure would raise Bloom’s input costs and erode the timeline advantage.

And then there is execution. Building ceramics at scale is hard. The history of fuel cell companies is littered with firms that proved the technology at small scales and failed to scale manufacturing: Ceres Power, LG Fuel Cell Systems, Westinghouse’s SOFC program. Bloom has survived longer than all of them. That does not mean the scaling challenge is solved. It means the scaling challenge is next.

Fuel cells are a bridge, not a destination.

The value proposition is speed, not price. For the specific window of 2025 to 2030, when AI demand is growing faster than grid infrastructure can respond, fuel cells fill a gap that no other technology can fill on the required timeline. After that window, grid capacity catches up (if FERC reform works), geothermal scales (if Fervo delivers), and the economics tilt back toward lower-cost generation sources.

Bloom does not need to power data centers forever. It needs to power them for the five to eight years between now and when the grid catches up. The question is whether manufacturing scales fast enough to fill that gap, and whether the margins hold long enough to make the company self-sustaining before cheaper alternatives arrive.

Leopold’s bet is that the gap is wide enough and the competition thin enough that Bloom captures a dominant share of the interim market. He is betting on the factory as much as the fuel cell.

The answer to the Bloom question is not yes or no. It is: how fast? Every month of manufacturing delay narrows the window. Every successfully deployed gigawatt widens it. The Oracle contract is a demand signal, not a delivery receipt. The factory in Fremont has to run.