The gasoil crisis, after simmering on the back burner for a while, seems to be ready to boil over again. What looks like a temporary price increase, however, signals preparations to something much more ominous in the near future.

Thank you for reading The Honest Sorcerer. If you value this article or any others please share and consider a subscription, or perhaps buying a virtual coffee. At the same time allow me to express my eternal gratitude to those who already support my work — without you this site could not exist.

We are witnessing a very strange anomaly with the price of diesel fuel rising, even as the US economy teeters on the edge of recession, and world diesel demand stays flat. Something is clearly amiss. While the world remains mired in the oil glut meme — stemming from the idea that the world market is oversupplied — numbers tell a very different story. At the same time when we seem to be awash with crude oil, there is a strange shortage of petroleum products. Commercial stocks of middle distillates in OECD countries are still below average. Diesel prices stay elevated at $3.83/gallon in the US and 1.65 EUR/liter for Germany at the time of writing. Curiously, these prices are 25% higher for the US and 40% steeper for Germany, than in November, 2019, when oil prices were at the same level as today. What’s going on?

Long time readers already know how critically important diesel (or gasoil) is to the economy. Agricultural and mining machinery, main battle tanks, ocean faring container ships and long haul trucks are all hopelessly dependent on this fuel. Less gasoil means less transport, less food, less raw materials, a smaller military, and an even smaller economy. Despite the hype around electric cars, hydrogen, and the rest, there is really no way around trucks running on this fuel.

Despite all the rhetoric, ours remains a diesel powered civilization.

In order to have a better understanding why the price of this fuel is so high, we must dig one level deeper and take a good hard look at refineries. The first thing to understand here, is that crude oil is not a magic substance; you cannot wish away parts of it, or increase output of certain products without limits. Yes, you can make adjustments, but these are in a couple of percentage points range, not 50% plus or minus. Second, every blend of crude oil is different, some are lighter — yielding less middle distillates, such as truck and jet fuel — while others are heavier, producing more bunker fuel, lubricants or asphalt. Third, every refinery is tuned to a certain type of oil; the best output can only be achieved when the right kind of crude was used as feedstock. The key to cheap diesel, a middle-distillate, is thus having unrestrained access to medium heavy crude oil, processed at the right refinery.

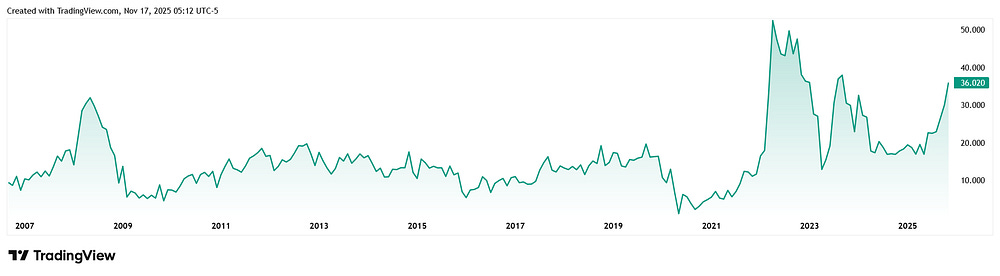

In order to quantify all this, a metric called “crack spread” is used, or the gross margin a refinery makes on distilling crude oil and selling a part of it as diesel fuel. If you take a look at the chart below, you can instantly have a grasp of what’s going on. When this metric is on the rise — or stay elevated above the historic $15–$20 range — there is a short supply of this essential fuel. When the crack spread is below this range, on the other hand, it indicates oversupply. Thus when crack spreads are low for a prolonged period of time, it signals that the real economy of goods and services is doing bad, as in 2009–2010 when the great financial crisis hit the economy hard, or in 2020–2021 when one country locked down its economy after the other.

Then surely a rising crack spread indicates a booming economy, right? Well, it used to. During the run-up to the financial crisis, during China’s rapid economic expansion to be precise, diesel fuel demand shot through the roof. Global trade, construction, manufacturing all boomed during this era, but global petroleum supply failed to catch up. This not only sent oil prices to record highs, but at the same time caused diesel refinery margins to soar as well — only to be brought down again by a good old economic crash. However, in late 2015, something has profoundly changed, although it made no headlines, and was not yet visible in any financial metric. World diesel fuel consumption — and thus production — has silently hit a flat plateau. The world seemingly did not want any more of this type of energy.

As I explained elsewhere, however, this had nothing to do with electrification — as neither heavy mining or agricultural machinery, nor long distance freight could ever switch to heavy batteries. Instead, the world simply stopped growing in real economic terms. It no longer needed more fuel to build more houses, roads and bridges, bring more metal ores to the surface, grow more food, or deliver more goods in aggregate. At least, so it seemed. Crack spreads, as a result, remained flat and stayed within the normal $15–$20 range. The world yawned and chugged along.

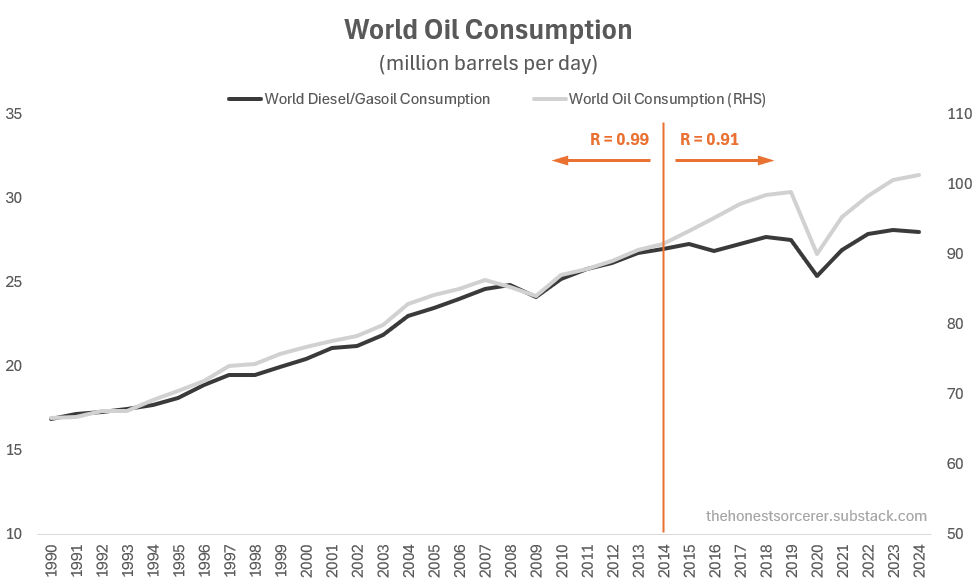

In the meantime, however, profound changes were underway in the oil industry. Conventional onshore and shallow water crude oil production peaked in 2005, and thus the best feedstock to make diesel from became geologically constrained. This fact was conveniently masked by the GFC and it’s aftermath, plus the advent of the shale oil revolution. The correlation between oil and diesel production, on the other hand, has started to break down. No matter how much more “oil” we brought to the surface, very little of it was suitable to make diesel from: adding natural gas liquids, ultra heavy tar sands and Venezuelan oil, or ultra-light shale oil to the mix did nothing to alleviate the diesel situation. The world, it seems, could not produce more diesel, even if it wanted to. With the real economy being stuck, though, no one seemed to be worried about this fact.

World crude oil production peaked in November, 2018 but that, too, came and went unnoticed. After five years of stagnation, recessionary signals were flashing red in 2019 already. Western automakers were complaining about overcapacity and a lack of demand for cars. Diesel fuel demand began to fall. Then came COVID, oil prices went negative, and no one could care less about crude, or diesel. Nobody went anywhere, containers clogged up western ports, the world economy went into recession. Then, in 2021, as countries were re-opening their boarders and restarted trade, gasoil crack spreads were on the rise again, but still remained in the normal range. At least until February, 2022.

Russia’s invasion of Ukraine has triggered a series of unprecedented sanctions against one of the largest exporter of medium heavy crude. European refineries, finetuned to process Urals crude, suddenly found themselves scrambling for feedstock. Needless to say, diesel refinery yields plummeted and created an acute diesel shortage in the world’s biggest fuel import market, Europe. And since diesel is such a universal, easy to ship, high value commodity, the EU’s self-imposed crisis quickly became a worldwide shortage, shooting crack spreads into the stratosphere. As India took Europe’s role in refining Russian oil, later in 2023, however, the crisis slowly subsided — but never really went away.

Conventional wisdom holds that if a price of a commodity rises, or in this case crack spreads increase, new supply would magically pop up to fill the gap. That, however, is only partially true. While Indian refiners did help to alleviate the diesel shortage, world diesel output could not grow beyond a point, despite a return to 2019 oil production levels. In fact, world diesel consumption started to shrink again in 2024. Demand was killed by persistently high fuel prices, combined with a cost of living crisis across the entire West, the stagnation of the US and the recession of the EU economies. The German industry has embarked on a journey towards slow motion collapse and EU corporate profitability followed suit. All this came on top of a Chinese housing and manufacturing overcapacity crisis, putting an end to decades of material economic growth over there as well.

Self harming policies did not stop with European sanctions, though— the US placed levies on steel and equipment imports (among other things) in March and April this year. The resulting price increase of these two inputs, however, have proven to be fateful to the US oil industry. Drilling wells, maintaining refineries, building pipelines all require vast quantities of steel and machinery — both of which has to be imported to America as domestic industrial / smelter capacity can only supply a third of what the US economy needs. Rising costs have resulted in deferred maintenance, refinery shut downs — and yes, rising crack spreads. As an article in Oilprice.com explains:

Refinery closures in recent years, planned maintenance after the summer, unplanned repairs due to outages, and Ukrainian attacks crippling Russia’s oil product exports have tightened the refined petroleum markets everywhere.

Refining margins in North America and Asia are now at their highest since late 2023 and early 2024, while European margins are even higher as the market braces for a significant disruption early next year when the EU will ban, effective January 21, imports of products made from Russian crude oil, per the July sanctions package against Russia.

India’s pivot away from Russian oil, sanctions on Rosneft and Lukoil forcing them to sell their assets abroad, all seemed to make things worse. At least on the short term. Oil, the most sought after commodity in the world, will eventually find its way to buyers — if not in Europe, then in Africa, Latin America or Asia. A further decline in European and North American demand for diesel is already in the offing. Take, for example, how US trucking freight demand fell by roughly a third between April and October, despite the latter half of that period representing what should be the peak shipping season ahead of the holidays:

According to a survey of more than 270 U.S. logistics professionals from technology media outlet Tech.co, just 26% of respondents reported a high level of trucking freight demand in October, compared to 41% in April. That drop reflects a market where shippers are moving fewer loads than expected, and where the traditional rhythms of logistics are no longer dependable, Tech.co said in its report.

“Our latest research should set alarm bells ringing for the logistics industry,” said Tech.co editor Jack Turner in a November 19 release, noting that 20% of respondents said that “managing financial pressure” was their top priority, particularly as tariffs have strained global trade and tightened margins for a range of business sectors.

There is much more to the topic of the coming US economic decline than tariffs, though. Consumption, together with consumer expectations, are on the fall, driven by heightened fear of job losses. Companies can no longer push their tariff induced cost increases on consumers, and are forced to take a hit to their bottom line. Just like in late 2006, 2014 and now — since 2023 at least — corporate profits stopped growing then began to decline. Everyone knows the drill: this is exactly what precedes job cuts, resulting in yet another decline in consumption. Rinse and repeat and voila: recession! AI is a mere fig leaf in this story, used to mask the real reasons of the crisis: a lack of demand and an end to a private credit cycle. ‘But hey, the stock market is doing great!’ — yeah, sure.

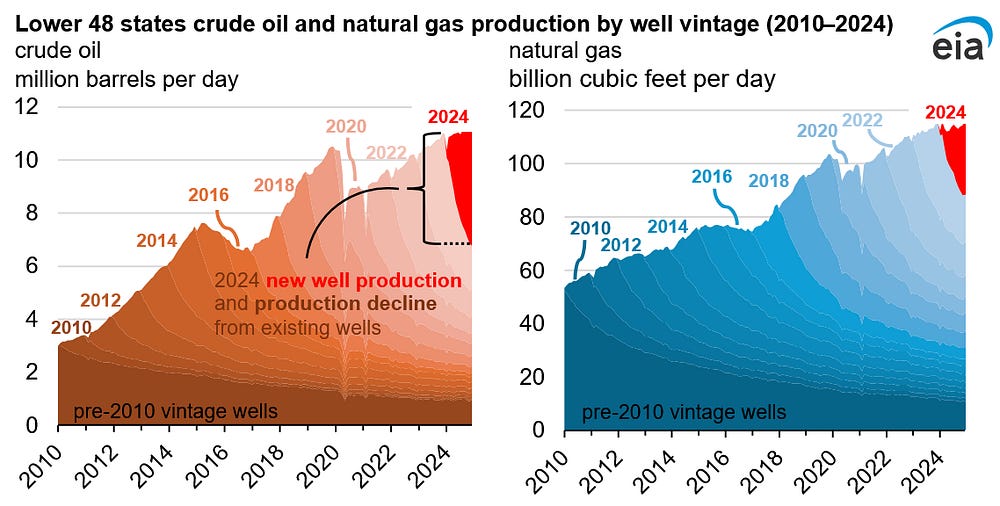

US oil majors are already cutting jobs, and since US oil wells continue to decline at an ever faster rate, this practically guarantees a lack of crude to make diesel from on the long run. Were it not for the frantic drilling in Texas, New Mexico and elsewhere — just to keep US oil production flat — we would have already seen roughly 4 million barrels a day lost in a single year. And its not just the US. As Russia’s Alexander Novak warned OPEC members:

“We are now seeing traditional accessible reserves being depleted, while hard-to-recover reserves require significantly higher costs. Therefore, if investment in the oil industry is not renewed in the near future, consumption will outpace supply”

Not that any of them could do much about it, mind you — we are talking about the depletion of a finite resource after all. Increasing investment in an already heavily indebted, stagnating world economy which is teetering on the edge of a deflationary depression for a decade now, is nothing but a pipe dream. Oil is now rapidly becoming increasingly unaffordable for a growing share of the population while, at the same time, becoming too cheap to continue extracting at present rates. So no, we are not sleepwalking into another diesel crisis — this is how the oil age ends, once all the cheap, easy-to-get stuff is gone.

The remaining, increasingly expensive to get petroleum will be simply left underground, as the now decade long stagnation of the world economy tips into a decline. In this sense, the diesel crisis will take care of itself by means of demand destruction — hitting European citizens especially hard. As we continue to run out of cheap, easy-to-get, medium heavy oil — first slowly, then ever faster — the global mad scramble for diesel fuel will reignite, though, with consequences to match. What we see today is thus but a prelude — a strategic preparation to a much bigger conflict at the cost of sacrificing Western prosperity and, eventually, much more. In an attempt to preserve its rapidly waning world dominance, America tries to take as much oil production (1), refinery capacity (2) and maritime choke points as possible under its control before it loses its last remaining bits of credible deterrence.

China does not sit idle either; they are militarizing fast, while drilling for and stockpiling oil like crazy (building an inventory between 1.2 and 1.3 billion barrels), as a preparation for the turbulent times ahead. Trying to choke an emerging power, comes with its own risks, though. If Pearl Harbor had any lessons it is this:

“As the noose tightens on a state’s economy, the victim may pursue a highly risky course of action — such as Germany’s decision to resume unrestricted submarine warfare or Japan’s decision to attack Pearl Harbor — that it otherwise may not have hazarded. . . . [H]istorical experience suggests that embargoes may include actions or reactions that are neither orderly nor predictable and that they are not simple, safe, and controllable substitutes for war.”

ROBERT A. DOUGHTY AND HAROLD E. RAUGH JR.,

“EMBARGOES IN HISTORICAL PERSPECTIVE”

With a consolidating and ever more aggressive antagonism toward China, and with Western powers preparing for a long drawn out conflict, Doughty’s warning might actually end up being used as a recipe for starting yet another devastating conflict without a shot being fired… With the only caveat that this is not 1941 when America was still on the rise, had a strong industry, and held all the aces.

Until next time,

B

Thank you for reading The Honest Sorcerer. If you value this article or any others please share and consider a subscription, or perhaps buying a virtual coffee. At the same time allow me to express my eternal gratitude to those who already support my work — without you this site could not exist.

Notes:

(1) Consider threats on Venezuela and Iran — both major oil producers with huge reserves — or the latest developments in the Middle East, bringing the Saudies firmly back into the US fold.

(2) Take the forced divestment of Russian refineries due to deliberate US sanctions (most notably in Serbia and Bulgaria), together with the mysterious explosions in Hungarian and Romanian facilities processing Russian oil. (Note, that German refineries were seized years ago already, and their pipelines were blown up or shut off completely.)