2025 represented a turning point in many respects. The world has started to grapple with the fact that the physical growth of the world economy, an almost two hundred year long anomaly, might indeed be over. Of course no world leader would admit this openly, but there seems to be a tacit understanding that our material and energy consumption will not be able to grow forever and, in fact, has begun to shrink already in many places. Your mileage, of course, might differ, based on where you live or with whom you interact, but one thing is clear: the world has arrived at a tipping point.

What follows is a review of what we have learned during 2025, a summary of a year’s worth of research. I have prepared a list of wide ranging topics from resource extraction to energy production and from macro economics to geopolitics — feel free to jump between segments or skip to the most interesting part. If you, however, have the time, I suggest to read this article from top to bottom to get a full picture how these various topics interact, in order to have a better sense where the world is actually heading. I also provided links to my relevant articles I published this year in case you were interested in the details of a subject or would like to refresh your memory. Most likely I won’t have the time to publish a separate 2026 predictions article, so treat this one not only as an attempt to summarize this year, but also a window into next year. With that said, have at it and enjoy!

Thank you for reading The Honest Sorcerer. If you value this article or any others please share and consider a subscription, or perhaps buying a virtual coffee. At the same time allow me to express my eternal gratitude to those who already support my work — without you this site could not exist.

As a manufacturing guy, allow me to start with the basis of all industrial activities: metals and coal. So called “service economies” or “post-industrial nations” are just as reliant on manufactured products, raw materials and energy as any other industrial society on Earth—leaving them totally exposed to the whims of exporting nations. As for an example, look no further than the recent rare earth (REE) craze. But we don’t have to look at such exotic materials to understand: all developed nations rely on the availability of cheap raw materials and energy. In their study PricewaterhouseCoopers shed some much needed light on the role of commodities in growth , stating that “Minerals will catalyse value creation in the new domains of growth.” And what minerals have they placed on the top of their list? Neodymium? Silicon? Nah, good old coal, iron and copper. You see, while the availability of small magnets can and do disturb supply chains, the vast majority of industrial materials still come from “low value-added”, polluting businesses.

The coal and iron age has never ended

Problem is, that global steel production has peaked in 2021, and near the end of 2025 world steel production is still in a post peak decline. This is a very important, but much overlooked development. Iron and the steel we make from it is the most widely utilized and most versatile metal on Earth. Steel is used primarily in construction projects (building and infrastructure), taking up 52% of global output, or about a billion tons annually. Bridges, houses, railways, wind turbines, pipes etc. all take an immense amount of steel to make. Mechanical equipment (pumps, cranes, compressors, heavy machinery, industrial equipment, reactors, boilers etc.) take another 16% of global production, while the automotive sector is responsible for 12%. The rest goes to ship building, locomotive and rolling stock manufacturing, and metal consumer products (cans, cabinets, tools etc.). And while we still have vast deposits of iron ore and coal (which is necessary to turn it into steel), production of this vital raw material is on the decline for years now. This signals, more than any other economic metric out there, an end to the exponential phase of our material expansion on this planet. Again, take a look at the list above. And while some might argue that this is but a rough patch, as you read along you will discover that we are facing something much bigger than that.

At the heart of the issue we have a growing productivity problem, or dare I say predicament. When we look at the data, we see an almost exponential cost increase both in the case of iron and in case of coal. Both raw materials take energy—a ton of energy—to produce, and as easy-to-get deposits deplete, we have to dig deeper and go further to get the next batch of these materials. Yet, in the end we always get the same product, with the difference that we have spent a whole lot more energy and money to get it. This is especially so, if you consider that you need megawatts of increasingly expensive electricity and diesel fuel to mine and deliver these materials, or to re-melt steel in an arc furnace… It is due to this productivity trap, that The Mythical Return to Coal will remain just that: a myth.

Coal is not being phased out — we are running out of the accessible portion of this dirty but vital fuel. This is why coal mining is on the decline in most nations worldwide for decades now and this is why a worldwide peak in coal production is imminent. You see, resource depletion was never about consuming certain materials to the last atom on Earth, but about running out of all the easy-to-get, cheap-to-produce portion… Then having to face bankruptcy. The concerning part is that our various energy resources—coal, oil, gas, nuclear, “renewables”, etc.—are not interchangeable, but complementary. Oil needs machines and pipes to be extracted, refined and used. All of these equipment, however, is made mostly from steel, which in turn is made by burning copious amounts of coal. You kick one leg out of this stool, and the whole thing topples over. Similarly, in case of “renewables” you need tons of steel to build wind towers, and tons of coal to smelt and to make silicon. The ultra-clean wafer fabs are built on top of a dirty and highly polluting supply chain.

And its not only coal and steel where we face increasingly impossible odds. Copper supply, third on the PricewaterhouseCoopers chart above, is expected to peak later this decade (at around 24 million tons) before falling noticeably to less than 19 Mt by 2035. This will leave us with a supply gap of 10 Mt by the middle of the next decade—even as we would need more copper than ever to “electrify” the economy. The reasons, as with coal are geological in nature: ore grades decline, reserves become depleted and mines are retired; there are no more large copper deposits to be found, and mines cost more than ever to expand, let alone open. These issues won’t be, and frankly cannot be solved by the recent meteoric rise in the price of copper, nor by replacing the red metal with aluminum. Read the details in my recent article: Running on Empty: Copper.

Depletion of cheap mineral resources is nowhere near more visible than in the heart of the European industry: Germany. Together with a complete lack of hydrocarbons, running out of easy-to-get, high quality coal was the sole reason why Germany had to import 50% of its coal, 55% of its natural gas and 31% of its crude oil from Russia, at least up until 2022. All of these former imports now fall under some sort of sanctions today, affecting 33% of Germany’s total energy consumption, resulting in a 20% drop in production in German energy intensive sectors compared to 2021. The lost access to cheap resources has led to an accelerating deindustrialization of Europe, a process which, however, has its own tipping points. Take, as a prime example, Volkswagen which is forced to shut down one of its factories in Germany for the first time in 88 years. As a study, discussed in my post No Escape from Fantasy Land, explains:

“Once disinvestments start, the solid looking Jenga tower will weaken and instigate other disinvestments, causing industrial ecosystems to unravel and collapse. This ‘Jengafication’ can cause irreversible deindustrialization and a diminishing ability to realise the industrial energy transition, security of supply and strategic autonomy.”

Seeing all this it is perhaps not terribly risky to state that we should expect more of the same in 2026. A deepening energy crisis, leading to further deindustrialization, layoffs and plant closures. And not only in Germany, but all throughout Europe, and perhaps in America as well. The energy and resource crises, crippling industrial economies, is here and can only expected to get worse with time. What we have seen so far was just a prelude.

Capitalism is just as prone to hit limits to growth as any other extractive system humans operate. The underlying reason is simple enough: all prevailing economic models are predicated on an ever faster drawdown of natural and mineral resources, leading not only to depletion—as we discussed above—but to mindless consumption, waste generation, pollution and the concentration of wealth at the hands of the few. Then, as limits hit and as the rate of extraction ceases to grow, stagnation and decline arrives in full force. From an economic perspective we are at The End Of The Road, the point beyond which progress or economic survival cannot continue.

Growth and progress happened because it could. Now, that all the factors enabling it slowly recede into memory, growth turns into decline, progress turns into regress.

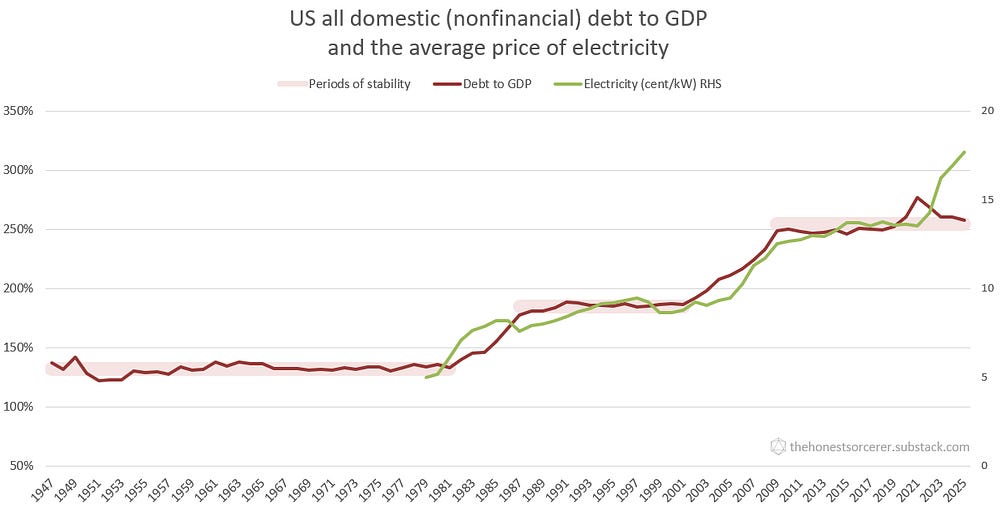

Western economies have reached an impasse. An inflection point, beyond which further increases in debt levels are no longer feasible — despite a slowing economy screaming for more investment. The onset of a long, protracted economic decline now seems to be inevitable, even to those who follow official GDP metrics alone. Watching real world economic indicators, such as the price of electricity, or the total domestic (private and government) debt to GDP ratio, however, the picture becomes chrsytal clear. In simple terms: every time the cost of electricity rose, the US economy got deeper and deeper into debt. No wonder: energy is the economy — money is just a claim on energy. Every economic activity from mining to manufacturing, or from services to trade, requires the spending of energy first (and not just electricity). Without power or liquid fuels the economy would grind to a standstill and economists would be sitting in the dark counting play money. Debts outstanding are thus a claim on future energy use: representing the amount of fuel we have to burn and the kilowatts of electricity we have to consume in order to earn the money with which we can settle our debts. Hence the tight correlation.

The electric grid, on the other hand, is a perfect microcosm of the entire material economy. The price of electricity not only builds into almost every product or service we buy, but gives an overall picture of the health of an economy. Since power generation involves burning large amounts of fossil fuels (natural gas and coal), and requires a great deal of material and energy investment in infrastructure expansion and maintenance (copper, aluminum, diesel fuel etc.), the price of electricity incorporates the entire energy and metals sector. Large scale deployment of nuclear, hydro and “renewables” adds further weight to this metric, as all of these “low-carbon” sources of electricity require mining ores, smelting metals, manufacturing turbines and other components. (Not to mention the pouring of thousands of tons of concrete, erecting towers of steel and much more.) If energy is the economy, then the price of electricity is it’s blood pressure.

But can we borrow our way out of this mess? Well, in a nutshell, no. In greater detail: hell no. Taking on a debt or paying with a credit card creates money out of thin air, which immediately starts circulating in the economy and begins to chase the same amount of goods and kilowatts. And while paying off these debts in small installments takes months or years (eventually destroying this newly minted money), the total amount of debts outstanding just keeps on growing with every dollar of loan issued. (Not to mention the vast sums corporations and governments borrow to finance their ongoing operations and spending.) You see, it is commercial banks who create 80% of the money in circulation by literally lending it into existence… Government “money printing” pales in comparison. Thus, if we keep on borrowing at this rate (let alone at a higher one) we will just keep increasing the amount of money in circulation and create more inflation, not less.

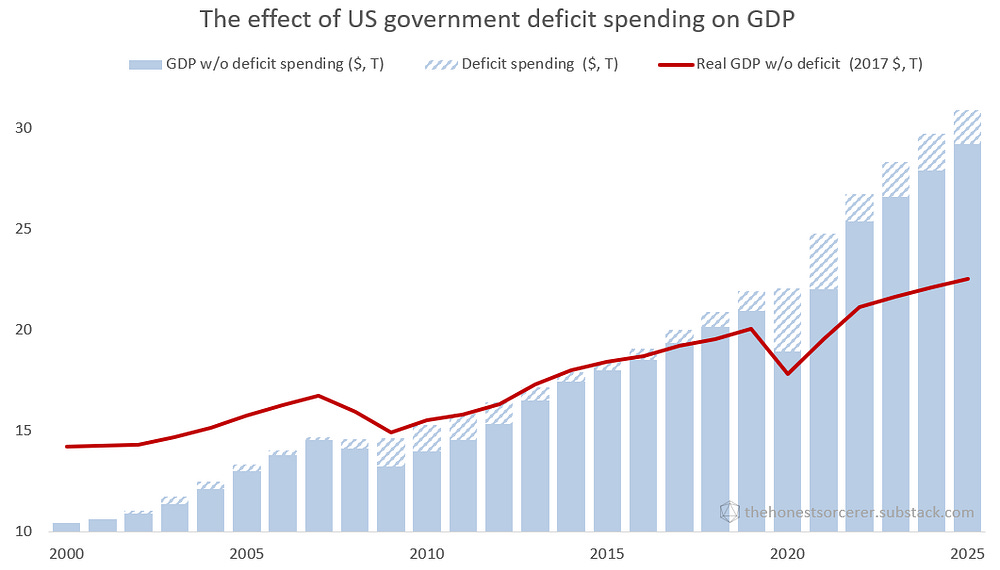

Private and government debt, however, has already reached a level where interest payments take away 8-10% of the gross domestic product, and where borrowers already struggle to keep paying their dues. The system has become totally unsustainable, unable to take on more debt but, at the same time, unable to live without it either. The economy has entered a doom-loop where rising prices and stagnating wages force households, businesses and the government alike to take out more credit, which in turn creates more money — fueling another round of inflation, followed by another round of debt increase. What’s worse, and mostly due to the productivity predicament of raw material extraction and energy production, the economy has become totally addicted to government deficit spending, resulting in artificially inflated GDP growth figures. Without this massive deficit spending, and using 2017 dollars (adjusted for inflation) to measure real GDP growth, the US economy would’ve barely grown over the past quarter of a century. Governments in the past 25 years, it seems, have done everything in their power to a) hide the true depth of each recession, and to b) show higher than normal GDP growth… And if inflation was just 2 percentage points higher every year (than the official figure used to calculate real 2017 dollars), all this growth would be zero. (Read more: The End of Degrowth.)

The cost of necessities (food, energy, housing, clothing) as well as services (insuarance, banking, healthcare, education) was on the rise for decades now, and have skyrocketed in the past five years. Real wages—while stagnating or even slightly growing on paper—now worth much less than 25 years ago, and in many cases not even enough to cover the bare basics. The result? More than two-thirds of Western citizens now live paycheck-to-paycheck. No wonder, that US consumer sentiment has hit at a record low level in 2025—plunging lower than it was during any crisis and recession since 1980. And yet, officially at least, 2025 was not a recession year, despite every indicator flashing red. Take, for example, the velocity of money. The number of times a dollar was spent to buy domestically produced goods and services per unit of time has been falling since 2007, and after a dip in 2020 it still failed to recover to 2019 (let alone pre-2007) levels. Consumers and firms are holding on to their cash, instead of spending it on goods and services or investing in new production capacity. Although this behavior slows down inflation, it also suggests that confidence in economic recovery is still very low. Gold, a safe haven during crises, on the other hand, was shooting upwards throughout the year, gaining 74% in just twelve months… Meanwhile the price of crude oil fell by 20% in 2025, resulting in a near record high gold to oil ratio, surpassed only by 2020 (when the price of oil has plummeted to record lows). If anything these indicators show how distressed the financial situation has become, suggesting economic uncertainty and weak oil demand ahead.

Over the pond, in Europe, the situation didn’t get any better either. “Today, 93 per cent of Europeans say they are seriously worried about making ends meet while 40 per cent of young people rank rising prices and living costs among their top concerns.” — one recent study found. German consumer expectations still haven’t recovered after falling 30 points in January, 2020. And it gets worse:

The DIHK forecasts a 0.3% recession for 2025, but adjusting for state spending, the real decline is closer to 4–5%. Daily surveys confirm the same message: Germany is being deindustrialized, losing hundreds of thousands of core-sector jobs. The social security deficits already emerging are just the beginning. Yet both politics and business refuse to conduct an honest diagnosis. The Green Deal remains sacrosanct. Energy costs for German industry are up to three times higher than for US competitors, double that of French firms—pushing energy-intensive sectors out of the country.

And while large corporations can adjust or relocate production to sidestep regulation, and to avoid energy price increases, small and medium-sized enterprises are being crushed. This process naturally leads to a fall in tax revenues, forcing the German government to go deeper into debt. That, however, is not without its perils: according to Foreign Policy magazine, the Mother of All Currency Crises is on the horizon, as Canada, France, Italy, Japan, Spain, the United Kingdom, and the United States are all carrying debt equal to more than 100 percent of their GDP. As you can see, its not just about the Europeans. The British economy, for example, is also unraveling fast, the quality of public services is in a free-fall and democracy is slowly turning into autocracy. Regulations galore, complete with elite overreach, a two tier justice system, censorship and a nation slowly drifting into civil war.

China, a country which gave rise to the largest middle-class cohort in the world (some 400 million people), is having its own problems with growth, too. Income inequality, regional disparities, slowing social mobility, low birth rates and rising living costs all stand as obstacles to raising more people to the middle-income bracket. With population growth reversing and consumer sentiment remaining muted, growth in retail sales YoY is down to just 1% (compared to 8-9% growth before 2020). Due to weakening domestic demand, together with a massively subsidized production expansion and the resulting price wars, China is now facing a serious over-capacity and deflation crisis. On the other hand, China announced that its digital yuan cross-border settlement system will be fully connected to the ten ASEAN nations and six Middle Eastern countries, implying that about 38% of global trade could bypass the US dollar dominated SWIFT network when its done. De-dollarization is definitely gathering pace. How this will end is anyone’s guess at this point but personally I would not be surprised at all if we found ourselves in a global economic / financial debacle in 2026 as a result of all these converging crises (not resulting just from government debt alone, but from everything else combined).

But What Comes After The Current Financial System Ends? In my opinion the coming economic / financial / banking and debt crisis will most likely trigger a global deflationary gyre—just like the famous Wall Street crash of 1929 did. Back then, a downward spiral of falling demand, reduced production, wage cuts, increased unemployment, and business failures ultimately lead to an economic depression lasting a decade, put to an end only be the outbreak of World War II. In fact, I argue, many symptoms of this coming deflationary crisis are already here: manufacturing overcapacity, falling demand due to a cost of living crisis, lay-offs and increased unemployment… In the meantime both the velocity of money and copper to gold ratios have now fallen to their corresponding historic lows — just like a century ago — indicating a complete lack of confidence in economic recovery. ‘But hey, at least the stock market’s doing fine!’ Deja vu, anyone?

Looking at the economic and manufacturing data, we see stagnating economies failing to produce growth and unable to generate enough demand for oil. Not that this a is bad thing in an of itself: we already use and burn too much stuff. A smaller, truly and justly degrowing economy would be a whole lot better both for the planet and our future as a species as well. On the other hand, this crisis of chronic under-consumption and stagnation, will most likely cause a major economic and currency crisis, and will raise the potential for a global war to dangerously high levels.

Oil and gas extraction is no exception to the same productivity crisis already affecting coal and steel production: hydrocarbon production requires an ever increasing amount of energy and material input to maintain year after year. The rising energy cost of energy has set off a vicious cycle—called energy cannibalization—where more and more energy is diverted to maintaining existing levels of production, and where oil and gas producers find themselves in a competition for energy with the rest of the economy. And as energy prices rise (especially that of electricity and diesel fuel needed to drill for, pump and deliver oil) so does the cost of petroleum production increase—worsening the productivity crisis further still. Taken together with a simultaneous destruction of global oil demand, the end of a credit cycle, and a persistent cost of living crisis, we see a self-reinforcing feedback loop on the long run, where demand and supply goes down hand in hand. If living standards continue to falter across the West — and throughout much of the developing world — even cheap oil from existing wells could prove to be too expensive for consumers.

For now, however, we’ve found ourselves in a Wile E. Coyote moment, with oil production still rising against all odds: crude oil extraction worldwide has even surpassed it’s previous peak in 2018. Oil and gas operators rather pay lower dividends, fire staff, and implement other cost saving measures, than to reduce output. See, doing so would not only raise operating costs on a per barrel basis and lead to the under-utilization of assets, but would also require a sharp jump in spending just to get back to previous production levels should demand start to strengthen again. (Besides, cutting investment too sharply would also dent PDP (proved, developing and producing) volumes that generate cash flow and underpin valuations.) This departure from reality, however, cannot continue forever, and we will eventually say Bye-Bye to Saudi America. According to Chris Doyle, CEO of Civitas Resources “The Permian is much of a water and gas business with oil as a secondary product there” already. And just as it happened in the 1970’s a depletion induced increase in the energy demand of energy extraction will eventually force producers to stop fighting the inevitable:

“The decline in EROI among major fossil fuels suggests that in the race between technological advances and depletion, depletion is winning. Past attempts to rectify falling oil production i.e. the rapid increase of drilling after the 1970 peak in oil production and subsequent oil crises in the US only exacerbated the problem by lowering the net energy delivered from US oil production (Hall and Cleveland, 1981).”

Half a century ago less than 5% of the energy of a barrel of oil had to be reinvested into exploration and drilling, while companies now have to spend over 15% of the hard earned energy from crude on getting the next barrel. Now, this ever growing energy demand per barrel retrieved can be expected to increase to as high as 50% by the middle of this century... That level of energy cannibalization would, however, simply kill the economy and produce a slump in demand, which would leave us with extracting the existing, still relatively easy-to-produce barrels only, then call it a day. No matter how much more oil is said to be still in the ground—once the energy cost of extracting it surpasses an economic level, production decline will eventually set in.

On top of the rising energy costs of extraction, a recently released IEA report has exposed those natural depletion rates to be a lot higher than expected. According to the report’s findings, as oil fields age, depletion becomes faster and faster, especially in case of unconventional (eg: shale or thight oil) resources, which tend to decline even faster. With profits drying up, demand stagnating and operational costs increasing, it’s not hard to see how the incentive to combat this accelerating decline will eventually slowly melt away. As a recent summary from RystadEnergy found: “Over the next decades, the capital needed will likely not be available to meet continuously increasing oil demand, service prices could skyrocket, and there will likely be limited appetite for innovations to sustain such high emissions from oil.” Without an ever growing investment in existing and new fields, however, depletion will simply take over and will most likely tip world oil production into decline, as seen on the chart below.

Finally, as energy analysts Goehring and Rozencwajg found:

Across all fields, our linearizations suggest that basins will roll over when approximately 28% of their reserves are produced. Our machine learning models show oil shales are now 28–32% depleted, while gas shales are 30–34% depleted. This points to a slowdown driven by depletion, not price or regulation.

But The Electrification of Road Transport Will Turn Out to Be… our savior, right? Well, apart from electrifying part of our car fleet, most likely not—there are a number of reasons Why Electric Vehicles Can’t Reduce Overall Oil Demand. And that’s just gasoline use, it will be A Shortage Of Diesel Fuel—used in mining, agriculture, shipping and construction—which will prove to be the true bottleneck. Even the most optimistic analysts admit that there are serious productivity concerns when it comes to switching to battery electric mining trucks. The same goes to electrified semis, which are ideal only for cycles with combinations of lower daily mileage, lower speeds, and predictable routes, not for long distance delivery consuming the vast majority of diesel fuel worldwide. No wonder that the demand for electric trucks is still in the 1–5% range — even in China—while demand for battery electric mining equipment is virtually non-existent at the moment… And we haven’t even touched on agriculture, where soil compaction, due to the weight of the machinery, is already a huge issue—even without having to carry 3 ton batteries. (Soil compacted by tractors can absorb less moisture and plant roots do not develop properly in them.) Ocean shipping, often covering thousands of miles, is also “hard” (read: impossible) to electrify, but for another reason. The length of a trip across the Pacific, or halfway around the world, simply prohibits the use of Li-ion or any other similar technology. And while wind sails and solar panels could reduce fuel consumption by a couple of percentage points, they cannot completely eliminate it, unless we are willing to reduce our consumption of goods from overseas to 19th century levels (that is to super-expensive spices and coffee). And remember, if Rystad’s and EIA’s calculations are correct, we are looking at a plunge in oil production in the years ahead as existing fields deplete and investment in exploration takes a nosedive. We don’t have decades to develop and to ramp up new battery technologies.

Should world oil supply indeed fall to half of its present value by mid century, in accordance with the forecasts above, oil importing regions are posed to lose 75% of their imports in a matter of 15–20 years. While today oil exporting regions produce 42 million barrels more than they consume every day, this export potential could drop to 11 million barrels per day in 2050. The Oil Import Curse would hit Europe especially hard, causing to to lose 90% of its oil supply in a matter of decades which, needless to say, would devastate its economy completely. In this scenario, thanks to it’s relatively low (and already shrinking) population size compared to the amount of its resources, Russia would remain the only country which could truly fend for itself in food, energy, raw materials, weapons, you name it. China and India, on the other hand, could find themselves at a hot war fought over access to Middle Eastern oil...

Atomic energy is often touted as another savior of civilization. As we have seen above though, there are number of issues with that hope (and we haven’t even talked about long term waste storage). Electrification cannot save us from the consequences of a shrinking diesel supply, nor solve the issues of depleting coal and copper mines. Synthetic fuels and hydrogen, on the other hand, are such an enormous waste of energy (literally) that implementing those in a large scale would simply push energy cannibalization to insane levels. Let’s face it: Nuclear Energy Is A Non-Solution. Besides, nuclear power is already on a flat plateau worldwide—it’s thus unreasonable to expect that it can take the place of fossil fuels at any meaningful scale. Electricity generation from nuclear has already peaked in many regions (2004 in Europe, 2018 in North America and 2021 in Eastern Europe and Russia). The only rapidly growing region is Asia.

The proximate cause for that is the ageing of the world’s nuclear reactor fleet. Most reactors were built in the 1960’s and 1970’s, when manufacturing industries, and energy returns on investment were much healthier. Atomic power plants take a lot of concrete, steel, a healthy industrial economy—and ultimately diesel fuel—to build and maintain, together with mining and processing uranium ore for fuel. This is why switching to Thorium or even fusion, would also be a non-solution, as all of these much touted new technologies would leave us equally exposed to the issues of mining, transportation and the industrial ecosystem collapse discussed above. What we see is a systemic failure, not a component missing.

With this in mind it’s perhaps not hard to understand why there are only 65 reactors under construction across the world (most of them in Asia), with 90 further reactors planned to be built. New plants coming online in recent years, however, were largely replacements for retired reactors: over the past 20 years, 106 units were retired as 102 started operation. The stagnation in nuclear power generation won’t likely to end in the coming decades, Small Modular Hallucinations, or not.

The Tale of Two Energy Transitions told a story of a transition which never was and the true shift in the balance of power. According to the latest numbers compiled in the Statistical Review of World Energy, 87% of the energy used by humanity in 2024 still came from fossil fuels. The remaining 13% was consumed in the form of nuclear, hydro and “renewable” energy. Based on these numbers, however, we barely moved the needle in the past ten years: the ratio of coal, oil and gas in the mix was reduced by a mere 2% under a decade. At this rate of “decarbonization”, fossil fuels would be still responsible for almost 80% of our energy consumption in 2050. We will run out of all affordable, easy-to-get coal, oil and gas far faster than we could replace just a half of them with photovoltaics and turbines.

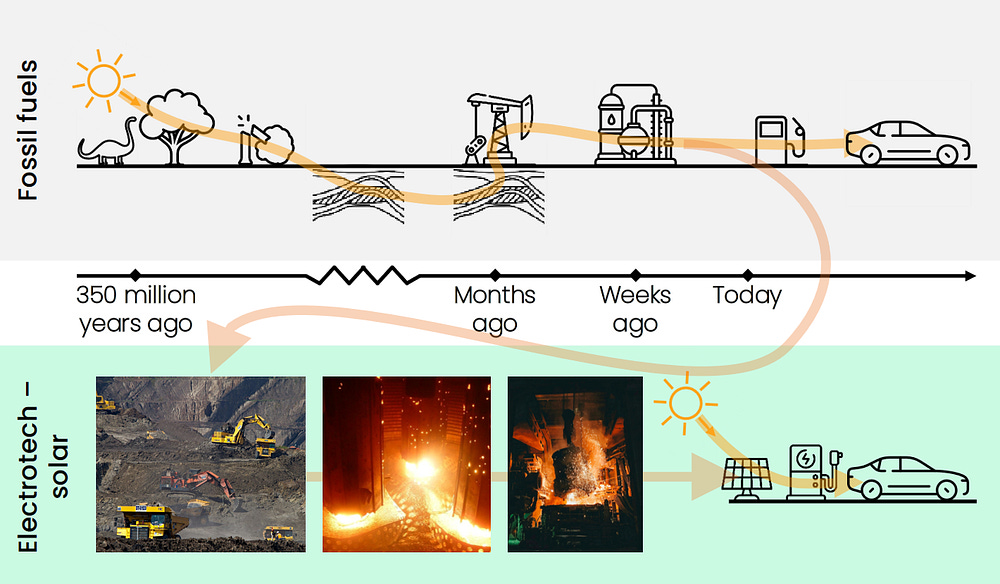

Problem is, that without fossil fuels there are no wind turbines or solar panels either. What’s Missing In This Picture of a “green transition” is that it’s technically not feasible: these so called “renewables” are just a “smarter” way of burning fossil fuels. Instead of using coal to generate electricity at a 30% efficiency, we now increasingly convert fossil fuels and Earth’s finite mineral reserves into solar panels and wind turbines in gas powered furnaces and coal burning smelters. That, by definition, just locks us more firmly in a now dying industrial paradigm. And just as we did not stop burning wood after coal came into the picture, or just as we kept burning coal after oil entered the scene, we will not stop burning fossil fuels — even if “renewables” were deployed en masse.

Not that “renewables” could replace fossil fuels, even if solar panels were to be teleported to Earth from outer space. As we have discussed in the case of nuclear, oil and gas: there is still no replacement to diesel, let alone the high heat processes making cement, steel, glass (among many other things) possible to make. Intermittent wind and solar are not a true replacement to coal and gas fired power plants either. By commencing construction on a $6 billion solar project, combining a 5.2 GW solar plant with a 19 GWh battery storage this year, The Emirates Showed Us How Not To Build Solar. There are several lessons to be learned for sure:

Solar can only deliver less than a quarter of it’s rated capacity on an annual basis; even in the middle of the sunniest of deserts

The proposed solar power plant in the U.A.E. is simply nowhere near technically feasible elsewhere — especially not in Europe (where solar projects deliver 11% of their nameplate capacity, and where winter storage has no scalable solution)

Realizing a return on investment in a 24/7 solar plus battery project is highly unlikely without resorting to heavy government subsidies.

The cost of wind turbines, solar panels and battery cells now seem to have reached their minimum, and rely on one major supplier, China. As energy and raw materials become scarcer, and geopolitical tension grows, costs can be expected to rise in the years and decades ahead.

Moving away from a grid supported and stabilized by fossil fuel use seems highly unlikely. As fossil fuel supply becomes scarcer still, grids relying heavily on “renewables” can be expected to experience frequent blackouts and power rationing.

Gulf states already experience limitations in oil production and clearly see that demand might soon outstrip supply, as world oil output peaks then rolls over. Hence the recent multi-billion surge in solar investment to free up as much oil for export as possible.

There are so many things which are possible using the power of the Sun, but running a 24/7 high consumption lifestyle, unfortunately, is not one of those.

Well, as Dries Acke from SolarPower Europe commented on the repeated renewable auction flops in Europe:

“You cannot have a green transition with red numbers. The sector needs to be profitable.”

The case of the April blackout in the Iberian peninsula has showed us something else, beyond financial and economic metrics. It exposed The Two Achilles Heels of Complex Systems: tight coupling and limits to human comprehension. The addition of large number of “renewables” to an old grid designed to run on AC generators has increased complexity — and thus vulnerability — beyond the point of human comprehension. As the ratio of “renewable” electricity rose, engineers tasked with maintaining grid stability had to intervene ever more often by curtailing or rerouting excess wind and solar power, and by firing up gas power plants in anticipation of bad weather. But weather is notoriously hard to predict, especially in a rapidly shifting climate regime, forcing operators to come up with emergency measures often within minutes, and sometimes in a matter of seconds. All this at the same time when much needed inertia from spinning AC generators have been removed to allow room for the addition of yet another batch of wind and solar… See, adding more individual pieces of equipment (solar panels, turbines, grid scale batteries, transformers, high voltage lines etc.) is not only costly, but also raises complexity to a whole new level—making a cascading grid collapse spreading the entire continent harder and harder to avoid.

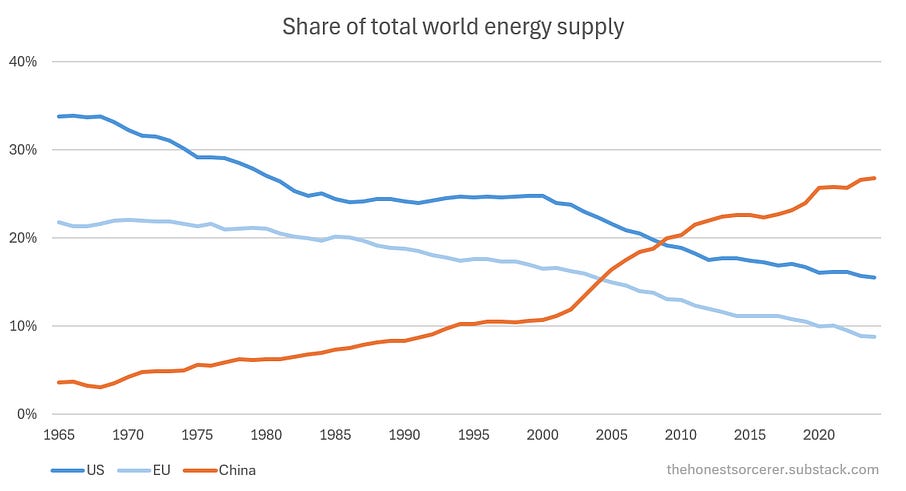

Instead of an imaginary, technically infeasible energy transition, the real shift in power thus happens between economies. This is really no rocket science: those who consume the most fossil fuels and electricity produce more products, more food, more weapons, transport more people and goods. Those who don’t, lag behind and will eventually be outcompeted. According to the Chinese National Bureau of Statistics, in 2024, China’s total value-added industrial output reached $5.65 trillion, while the US stood at $3.35 trillion. More energy, bigger economy. (In fact, growth in US industrial output stopped in 2008 already, and is stagnating ever since, while Asia just kept expanding its capacity ever since.) But China Is Busy Repeating the Same Fundamental Mistake the West Made by presuming that economic growth and energy consumption could on forever. Back in the 1960’s Europe and America dominated the global economic landscape, with a 55% combined share of world energy supplied to their industries and population. China first surpassed Europe in the early 2000’s, then the US in 2009. Now, it has an absolutely dominating share of world energy use, outstripping the combined West by a widening margin. Other than a thermonuclear exchange, there is no way on Earth that this trend could be turned around.

Overall energy consumption in OECD countries (the combined West plus some Latin American states), in 2024, decreased by 3% compared to 2014. A declining trend can be observed not only on a relative share basis, but in absolute terms also. Notwithstanding all that, the economic block’s GDP just kept growing from $50.5 trillion in 2014 to $67.5 trillion in 2024. The math clearly doesn’t add up here: a 33% increase in their gross domestic product clearly cannot be supported by a 3% fall in energy consumption... And don’t tell me that they’ve got that much more energy efficient. Trucks, ships, cars, smelters, power plants, factories are all operating on mature technologies already, developed and perfected decades ago. The only way to materially grow the economy and prosperity is to invest in more capacity, and by providing more energy intensive services—exactly the way China does by expanding their grid, transport infrastructure, and by creating new jobs in productive industries. Artificially inflating GDP with overpriced “services” such as insurance, banking, education and healthcare, or blowing housing and stock market bubbles sky high, only creates an illusion of wealth at the top, at the cost of pushing everyday people into poverty.

{kind=link}

Given these circumstances—deindustrialization and falling standards of living, combined with an overcapacity crisis—it’s not hard to see how globalization’s recent uptick has ended in the 2010’s. The 2020 pandemic and the ensuing lock downs have delivered another blow and now, with trade wars escalating, a decline in globalization seems all but inevitable. If history is any guide as to what comes next, we are about to enter yet another era of protectionism, and quite possibly: global warfare.

The US is already arming the Philippines with long-range missiles and busy turning Taiwan into a porcupine, despite the fact that the whole world officially recognizes Taiwan as part of China and not a separate country. Japan, on the other hand, and still firmly under US control with 55,000 American military personnel present on a number of bases, is deepening security ties with NATO further still. The US military itself is in the process of deploying large numbers of drones in the Pacific, with an aim of “increasing overall force readiness in preparation for a potential 2027 war with China.” Bloomberg goes one step further still, acknowledging that tariffs were in fact a dress-rehearsal for a war with China—a fight which “nobody” wants, at least according to mainstream media. From this perspective tariffs can be interpreted as an attempt to simulate the effect of a conflagration between the two superpowers in preparation for the real one. It’s hard not to notice the eerie resemblance to the preparation of Ukraine to join NATO, which has ultimately led to a war with Russia. A conflict, which has turned out to be, as US Secretary of State Marco Rubio admitted on camera: “a proxy war between nuclear powers, the United States helping Ukraine, and Russia” carried out under full US military supervision, using US and NATO weaponry, tactics, training, surveillance and targeting data. So, why do we expect things to unfold differently this time? Paraphrasing the Russian playwright Chekhov:

„One must never place a loaded rifle on the stage if it isn’t going to go off.”

For context, just imagine the same thing happening in the Caribbean: the Chinese turning Puerto Rico into an armed porcupine, while stationing fifty-thousand military personnel on a number of military bases in Mexico, and equipping Cuba with long range missiles capable of hitting not only ships, but cities across the lower 48 states… Oh, wait, that happened once already and the world almost went up in flames... Is it any wonder then that 79% of the world now favors China over the US according to the Democracy Perception Index (p43), with 55% of them having a net negative perception of America?

On the other side of the Atlantic, NATO has already put forward its vision of its coming direct clash with Russia. The Secretary General, together with French and UK admirals warned that “We must be prepared for the scale of war our grandparents or great-grandparents endured.” And this was just the latest attempt to manufacture fear, together with the German Foreign Office envisioning war by 2029… And if Russia doesn’t attack by then, then how about NATO launching a preemptive strike instead? Make no mistake, such an act would inevitably provoke a full-scale response from Moscow. Nevertheless NATO states keep laying out plans, ramping up their recruitment campaigns and considering the possibility of striking the Kaliningrad region. Meanwhile the German landscape is being militarized under the classified ‘Operationsplan Deutschland’ together with Poland under the code name ‘East Shield.’ There is, however, no technical, military or strategic way for Europe to complete any of these projects properly, nor to pose a credible deterrence. (Sorry, a few rented nukes on outdated missiles and onboard ageing aircraft or submarines will not cut it.) Europe is completely demilitarized, lacking both the mineral and the industrial resources — not to mention a young and willing population to fight another world war. The sooner this reality sets in, the sooner lasting peace can be achieved on realistic terms.

This doesn’t mean, that the conflict could not be continued on other fronts. Take, for example, the already raging energy war, with attacks on refineries, pipelines and as of recent: oil tankers, for example. None of these steps could have been taken without NATO intelligence and weapons technology, let alone targeting and the infrastructure provided. (And we haven’t even mentioned sweeping sanctions or the recent seizing of ships based on unilateral sanctions around Venezuela on the other side of the planet…) For now, these actions have only resulted in surging tanker price premiums, but on the long term such moves are a dangerous form of escalation, setting the precedence for waging war on global trade and potentially providing yet another casus belli for a full scale one.

If this is not a “pre-war” stage, I don’t know what is. And even if all these moves were for “just for deterrence,” it would take just one misinterpreted military exercise, one incursion too deep into each others airspace, and we would immediately have a hot war on hand, either in Europe or in the Asia Pacific. It is high time we all start de-escalating tensions, and initiate honest discussions on arms control on the highest levels possible, mutually reducing the number of troops and offensive weapons deployed on both sides all across Eastern Europe (as it was proposed in 2021 already) and throughout the Pacific. But What if the ruling class finally realized that this civilization is over?

If we survive the coming 4-5 years without starting World War III in earnest, it will mean that geopolitics have fundamentally changed. Global power relations won’t be any longer about maintaining Western military hegemony across the globe, but about reaching and maintaining a fragile equilibrium between four great powers: the US, China, India and Russia. The EU and NATO will eventually disintegrate into its constituent states under the mounting pressures of their many internal contradictions: the lack of affordable energy, a viable industry and an economy worth saving (not to mention democracy itself, which will be long gone by then). Thus, on the long run at least, world politics will increasingly revolve around the relationship/rivalry of two 1.4 billion strong nations: China and India, with Russia and the US retreating to their own (shrinking) spheres of interest.

In America, now free from its world policemen role and after getting rid of its global aspirations, a new generation of counter elites could finally upend what remains of the already rapidly eroding democracy. Silicon valley whiz kids, social media and online retail moguls already hold not only the vast majority of stocks and bonds, but a considerable sway over US politics in their hands. The techno-financial elite has become the main beneficiary of the system — securing government contracts on AI, cloud software, or space programs installing spy satellites en masse — and has begun to replace the old capitalist class at the helm, giving rise to the Network State. Not a warm and fuzzy image of the future, I know, but this is what happens when capitalism turns into decay. Again, I urge you to look at all of these developments as a process spanning decades, not as something what’s happened recently. All this, from the steady depletion of resources, de-industrialization and a debt crisis to a rising threat of war to the degradation of democracies was long in the making. What we see today is just the culmination of events.

Socioeconomic factors, such as income, education, employment, community safety and democracy are all downstream to our material reality outlined above. Human ecological overshoot and it’s many symptoms from the depletion of economically viable resources to climate change, has upended a centuries-long increase in living standards; giving rise to stubborn inflation, political polarization and geopolitical instability. What comes is a return to “normal”, it was the relentless expansion of economic activity over the past century what was in fact a historical anomaly. But not only the rate of growth was unsustainable throughout the past decades, but also the resulting level of consumption; as both were predicated on a steadily increasing draw-down of non-renewable mineral resources. Civilizations are by definition unsustainable.

Just like with any complex adaptive system, from living organisms to Earth’s climate or the global economy, things get increasingly wobbly at the turning point from growth to decline. The end of growth in such systems is much like leaning back in your chair: on the rising side of the action things are fully under your control, setbacks can quickly recovered from, and even a total reset (back to a fully upright position) can be managed easily. However, when the tipping point is getting closer, it’s becoming harder and harder to maintain balance, recovery takes much longer and your future prospects look riskier than ever. Pushing things just a little too far risks an unstoppable fall. This is where we are at the moment: on the knife’s edge, and things do not look to be more stable in 2026, either. With that said, however, we must strive to maintain balance in our lives and provide much needed support and stability to those around us no matter what comes. Resilience and resourcefulness will be increasingly important as we go through this massive turning point in history. Stay strong.

See you in 2026.

Until next time,

B

P.S.: Here is my latest chat with Shane from Recombination Nation. Listen in here or in the window below.

Thank you for reading The Honest Sorcerer. If you value this article or any others please share and consider a subscription, or perhaps buying a virtual coffee. At the same time allow me to express my eternal gratitude to those who already support my work — without you this site could not exist.