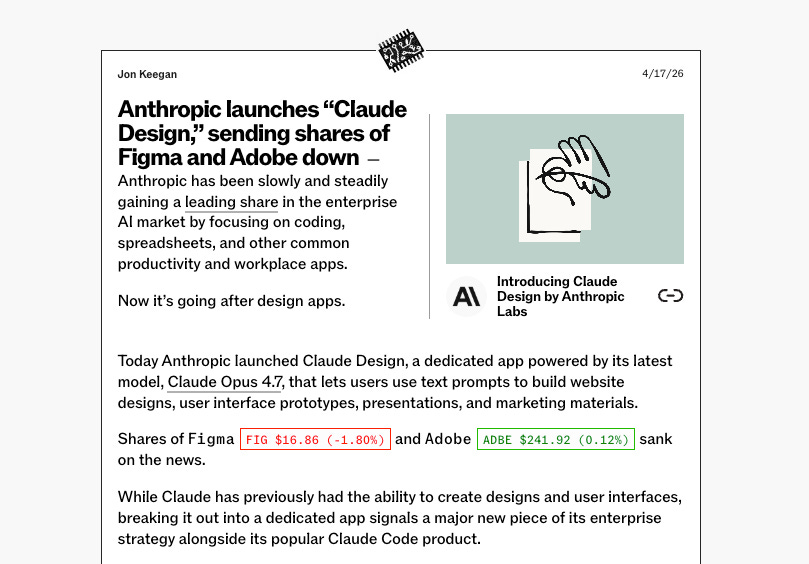

It was April 17. I was halfway through my second coffee when my phone buzzed. Someone in our Slack had pasted the Claude Design announcement.

I read it twice. Then I checked the stocks.

Figma had fallen 7% in the day, from $20.32 down to $18.84. Adobe was off about 2.7%. Wix down nearly 5%. GoDaddy down 3%.

The whole design-adjacent neighborhood took a hit on a single product announcement.

A few days before that, Anthropic’s CPO had quietly stepped off Figma’s board. In retrospect, that was the kind of move that only makes sense once you read the headline.

A category that took 14 years to build was suddenly worth a billion dollars less in a single afternoon.

Not because Figma got worse. Because the cost of building a credible alternative collapsed overnight.

I’ve been chewing on that morning for weeks now. Not because I was surprised, exactly.

I run a billing infra company. I think about defensibility every day, and I’ve had this conversation with Nikhil probably 40 times.

But April 17 crystallized something I’d been trying to put words around for a while.

Here’s the thing I want to be careful about, before I keep going. I am not saying Figma is dead. Figma is not dead.

People will still open Figma tomorrow morning. Designers will still ship work in it. Revenue will keep coming in. The product is not going anywhere.

What changed on April 17 is something subtler, and in some ways more important. The capital markets repriced what they think Figma is worth.

The growth story, the multiple, the assumed cash flows 10 years out, that’s what got cut. Not the product or the narrative around the product.

That’s the lens I want to hold for the rest of this piece. Most SaaS companies are not going to die in the next three years.

But a lot of them are going to be repriced, hard, by capital that no longer believes the future cash flows are protected. That repricing has already started. It will keep going.

And the ones that hold their valuations will hold them for three very specific, very unsexy reasons.

Is your core product a creative task, or a generative task?

If it is, design, writing, research, code, decks, marketing copy, illustrations, video, your capital story is the one most exposed.

Not your product but your story.

I’d give most of those categories 24 to 36 months before the market decides the future cash flows are no longer worth what they were paying for them.

Look at what’s already happened.

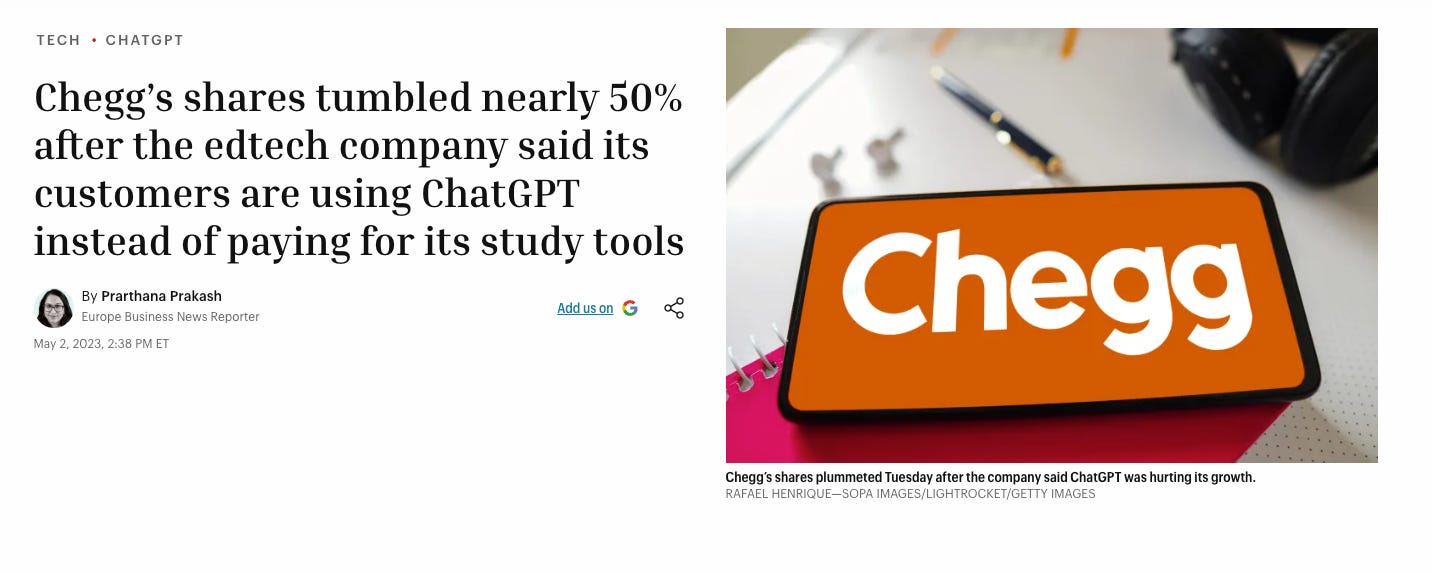

Chegg dropped 48% in a single trading day in May 2023 after admitting on its own earnings call that students were using ChatGPT instead of paying for their study tools.

The stock is down roughly 99% from its pre-ChatGPT peak. Chegg the company still exists. Chegg the capital story is gone. That’s a $14.5B repricing in 36 months by a free chatbot.

Grammarly, less dramatic but the same shape. YoY growth dropped from about 43% at $500M ARR in 2022 to roughly 10% at $650M ARR in 2024 as ChatGPT and bundled AI writing tools chewed at the standalone-grammar-checker thesis.

They’re still a real company, they acquired Coda and they raised a billion in non-dilutive financing.

But the growth story, the thing capital was actually paying for, cracked.

Here’s the part about Grammarly that I think matters more, though, and we’ll come back to it later.

Grammarly is not going anywhere. Because it’s installed across Fortune 500 companies in a way that’s painful to rip out.

It sits inside Slack, inside Gmail, inside every internal comms surface. You don’t uninstall Grammarly across 40,000 employees because Anthropic shipped a model.

You uninstall it when the IT director retires and someone else takes the call. That’s the kind of thing that buys a company another decade. Hold that idea, it’s the thing that actually saves you in this market.

And on the other side of the same coin is Cursor. It went from a 2022 student project to a $29B valuation by November 2025, and is reportedly raising at $50B+ as I write this.

The capital flowed out of the old wrappers and into the new substrate. That’s the move you should be watching.

The pattern is consistent. Wherever the output is “make me a thing that looks right,” the model becomes the product, and the wrapper’s multiple compresses toward zero.

Sometimes the fastest-moving wrapper becomes the new model and the multiple goes the other way.

Either way, the middle of the market, the careful incumbents whose moat was design and brand and a five-year head start, is where the air is leaving the room.

So what doesn’t get repriced?

The first cohort that survives is the boring one. Think like Stripe, Airwallex, Plaid and Adyen etc.

Claude can write you a payments processor in an afternoon. Cursor can probably ship one in a weekend.

Neither of them can give you 15 years of acquired bank relationships, PCI DSS Level 1 certification across forty jurisdictions, the licenses, the compliance staff, the legal precedents, the liability coverage.

Stripe’s moat isn’t code. Stripe’s moat is 15 years of regulatory compounding. Every audit they’ve passed, every license they’ve earned, every edge case their lawyers have argued, that’s the product. The API is the friendly part on top.

You cannot vibe-code your way past a banking regulator. I keep saying this to founders and most of them nod and then go build a creative tool anyway.

The second cohort is the one I think about most, because it’s where Flexprice lives.

If your product holds the customer’s revenue data, usage data, contract terms, entitlements, credit balances, and the historical record of how all of those have moved over the last 36 months, you are not getting replaced over a weekend.

The migration cost alone is brutal.

Think about what billing actually is. It’s not just “send an invoice.”

It’s the system of record for how much money your customer is making, how their pricing has evolved, which deals have custom terms, what counts as usage, what doesn’t, and how every one of those decisions reconciles back to the GL.

36 months of that data, owned correctly, becomes the company’s central nervous system.

You don’t rip that out because Anthropic shipped a new model. You rip it out when the entire company is being acquired, and even then it takes a year.

The same logic holds for CRMs with eight years of pipeline history, ERPs with decade-old chart-of-accounts mappings, observability platforms that have indexed billions of historical events. The data has weight. Weight is a moat.

A wrapper does not have weight. A wrapper has a prompt and a logo.

This is the one Nikhil and I argue about the most. I think it’s the most underrated of the three.

Some products can afford to be 95% right. A chatbot. A first-pass email. A draft design. If it’s wrong, you regenerate. The cost of being wrong is one click and four seconds.

Now imagine your billing system is 99.9% right.

If you’re a $100M revenue company, that 0.1% delta is $100,000 a year. If you’re a $1B company, it’s a million. That’s not “regenerate and try again.” That’s a board-level conversation.

That’s a finance team that no longer trusts the system. That’s six months of forensic accounting to figure out what got missed.

The same logic applies to anything mission-critical. Health records. Tax filing. Trade execution. Identity verification. Air traffic control, obviously, but also the much wider category of B2B systems where the margin of error is paid for in dollars and lawyers, not user complaints.

You can’t vibe-code these. Not because the code is hard, but because the consequences of being wrong don’t get socialized away by “the AI did it.”

Someone is on the hook. Someone is signing the SOC 2. Someone is the one explaining to the auditor why the recognized revenue doesn’t tie out.

I’m not pretending I know exactly which companies sit in which bucket. The lines are blurry.

Notion has deep customer data and a creative product surface.

Salesforce has both compliance and data, and also a thousand surface areas where AI is going to chew at the edges.

Stripe has an enormous compliance moat and is simultaneously building so much of its own AI surface that they might end up eating their platform partners.

What I’m saying is that the three filters, compliance depth, data ownership, and cost-of-being-wrong, are the only filters I trust right now.

If I were starting a company in 2026 and someone pitched me an “AI-powered presentation tool” or an “AI-powered marketing copy generator,” I’d politely change the subject. Those are not companies. Those are features inside someone else’s roadmap.

If someone pitched me an AI-native system that lives inside the customer’s revenue stack, owns their contract data, and becomes the source of truth for what they bill, I’d want to invest. That’s a company.

A friend in Bangalore pinged me last month asking whether his AI-powered legal contract drafting startup was defensible. I told him it depends. If he was competing with Claude on draft quality, no. If he was competing with Claude on “we sit inside the customer’s contract repository, integrate with their CLM, and own nine months of their negotiation history,” yes. The product is the substrate, not the generation.

That’s the lens. Not “is AI in my product?” but “what holds its multiple when the model improves 100x and costs a tenth?”

Compliance holds. Data and workflow weight hold. Margin-of-error pain holds.

Most everything else is going to feel what Figma felt on April 17. The product will still be there. The capital will not.

I’ll be honest, this isn’t a comforting framework. It’s the one I’m using to make actual bets, including the bet I’m making with my own years on Flexprice. We are deliberately picking the boring middle.

Deep customer data. Mission-critical. The kind of system you don’t replace because the math doesn’t math.

If that sounds defensive, it’s because it is. The defensible part is the whole point.

—Manish

Thanks for reading The Founder’s Draft! And if you liked it, then do share it with your network

Two things I’ve been reading and genuinely loved!

Yash Tekriwal on LinkedIn this week calling out “build vs. buy” as a false dichotomy. His point is that “build” is never just build, it’s build plus maintain plus debug plus document plus staff plus the context-switching your engineering team has to do away from the core product they’re supposed to be selling. He’s right, and it’s the part most founders are underestimating right now, especially when “just vibe-code it” makes building feel free. It’s not free. It’s the cost of focus, and focus is the single most expensive thing a young company has.

Ivan Landabaso’s Startup Riders breakdown of how Granola went from $0 to a $1.5B valuation in three years. The line that made me stop and read it twice was about why Granola ran frontier models from day one even when the unit economics didn’t work “running expensive products today is a temporary disadvantage that becomes a permanent advantage.”