Banks win when the poor lose. Credit cards can trap people in debt and bleed them dry with late fees. But it’s this exploitative experience that makes banks vulnerable to fintech startups like LendUp that are willing to undercut them and make up margin with software efficiency.

It’s that strategy of building an enduring consumer banking brand on the principle of compassion that let LendUp raise a new $47.5 million round led by Y Combinator’s growth fund. This Series C values LendUp “substantially higher than the last time” it raised in January 2016, says CEO Sasha Orloff. That’s an impressive feat during a rough season for late-stage fundraising.

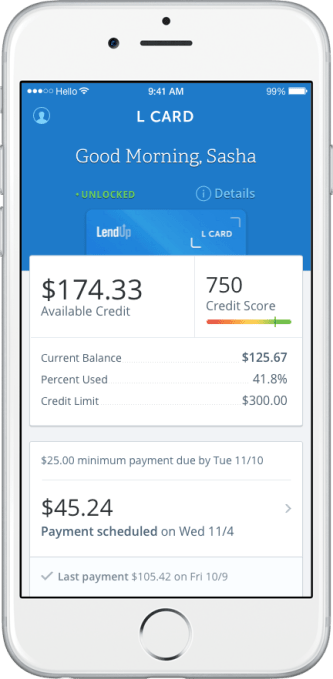

LendUp will apply the cash toward scaling out its L Card, a credit card with no hidden fees and a flexible payback schedule. It also sports modern features through its companion smartphone app, which lets users instantly halt charges in case of loss or theft, and a financial health meter that clearly shows how much credit the customer has left to spend. LendUp is already signing up thousands of accounts per month, even though it hasn’t been ready to aggressively market itself just yet.

LendUp will apply the cash toward scaling out its L Card, a credit card with no hidden fees and a flexible payback schedule. It also sports modern features through its companion smartphone app, which lets users instantly halt charges in case of loss or theft, and a financial health meter that clearly shows how much credit the customer has left to spend. LendUp is already signing up thousands of accounts per month, even though it hasn’t been ready to aggressively market itself just yet.

“We have no interest in keeping people in debt,” says Orloff. Harshly punishing customers for late repayment might score banks quick revenue, but it makes people hate them. Historically, there weren’t many alternatives. But data-driven risk assessment and the elimination of overhead by building an app instead of bank branches allows LendUp to break into the market.

Loan dolphins, not loan sharks

LendUp was founded in 2011, and first attacked the scammy payday-loan business. It stole customers from the cash-advance storefronts that blanket low-income neighborhoods, and retained them by providing financial education.

Credit cards are 100X larger market, though, so earlier this year it raised $100 million in debt to fund the lending, and $50 million in a Series B. Even though it still had plenty of money left from that, LendUp chose to accelerate its plan with today’s $47.5 million led by Y Combinator Continuity and joined by Google Ventures, Thomvest Ventures, QED Investors, Data Collective, Susa Ventures, Radicle Impact, Bronze Investments, SV Angel and some angels.

Techcrunch event

Boston, MA | June 9, 2026

YC Continuity’s Ali Rowghani will be joining LendUp’s board as an observer. He tells TechCrunch:

“LendUp is well on its way to building not only a very successful company but also a very important one. By combining true software innovation with a strong values-based culture, LendUp brings essential financial services to nearly half of the US population that currently cannot access credit in a sufficient way. In the process, LendUp endeavors to help its customers improve their credit scores, gain access to more financial services, and ultimately improve their lives.”

Battling the big banks will be no simple feat, though. LendUp will have to change financial behavior patterns instilled in customers for generations while competing with the banks’ giant marketing arms. It will have to balance its mission with financial solvency as revenue continues “growing consistently month on month,” says Orloff.

And LendUp will have meticulously screened employees to ensure no one does anything shady. There’s added scrutiny after online loan marketplace Lending Club had to fire 179 employees and force its CEO to resign after he and his family were discovered to have taken out loans to boost the startup’s numbers.

Luckily, LendUp is doing one thing to make it more nimble than its competitors: It’s building its whole tech stack in-house. “Everyone else outsources their tech,” Orloff notes.

Fintech is poised for massive growth. Few industries seem as fundamentally misaligned with their customers as banks boasting low rates while hiding the wallet-crippling fees. If the financial giants don’t adopt a more sympathetic approach, their customers will adopt startups like LendUp.

Josh Constine is a Venture Partner at ~$3 billion AUM early-stage VC fund SignalFire where he invests in pre-seed startups with a focus on consumer. He teaches startup pitch writing and fundraising strategy as a recurring lecturer at the Stanford Graduate School Of Business, and with accelerators like Z Fellows, Inception Studios, and Stanford ASES. Previously, Constine was Editor-At-Large for TechCrunch where he wrote 4000 articles and was ranked the #1 most cited tech journalist in the world from 2016-2020 by Techmeme. Constine has led 300+ on-stage interviews and keynotes in 18 countries with luminaries including Mark Zuckerberg and the CEOs of Shopify, DoorDash, Snapchat, Instagram, and more. Constine graduated from Stanford University with a Master’s degree he designed in Cybersociology, and wrote his thesis in 2008 on why remixable memes would be the future of marketing. He has been quoted in the NYT and WSJ, is regularly featured on CNN for his thoughts on AI and Silicon Valley, and advises startups on PR, fundraising, and organic growth.