The two reactors at Tarapur Atomic Power Station were switched on in October 1969, eighteen months ahead of schedule, on a coastal stretch ninety kilometres north of Bombay that had been a fishing village a decade earlier. They were General Electric Boiling Water Reactors, engineered in San Jose, shipped in pieces, and assembled on site under the 1963 Indo-American agreement on civilian nuclear cooperation.

Each unit produced two hundred megawatts. They were, at the time of commissioning, the largest civilian power-generating units in Asia, larger than anything the state electricity boards were running on coal, larger than the hydropower stations of the Bhakra-Nangal complex. Tarapur was India's first commercial reactor, and it was also its biggest.

Fifty-seven years later, on the same coastline, the Nuclear Power Corporation of India is preparing the site for another reactor. The Bharat Small Modular Reactor of 220 megawatts, designed by the Bhabha Atomic Research Centre, has been chosen for its first-of-a-kind deployment at Tarapur. The capacity is almost identical to the 1969 units, but the thinking behind it is the opposite.

A forty-eight-page report published this April by the Centre for Accelerating India's Growth, housed at the Nation First Policy Research and Change Foundation, captures the shift in a single phrase. SMRs, the report observes, "rely on economies of multiples rather than economies of scale. For a vendor to be profitable, they must sell dozens of identical units globally."

The cost advantage of a small modular reactor comes from the factory that produces it, with the site where it runs being the simpler part of the job. India has spent six decades getting very good at building reactor sites, and has never built the kind of factory that produces small reactors at scale. The BSMR-200 is the first product of an industrial order, small and repetitive and factory-built, that the country's nuclear sector has never delivered. Whether India can build that order is the question on which everything else in the SMR roadmap turns.

The stakes go well beyond a single reactor at Tarapur. India's electricity demand grew thirty-three per cent between FY21 and FY25, faster than any major economy. Data-centre capacity is projected to grow from 1.5 gigawatts today to 45 gigawatts by 2050. Captive industrial power is on track to expand from 80 to 206 gigawatts by 2047. The Green Hydrogen Mission targets 5 million tonnes a year by 2030.

Steel, cement, fertiliser, semiconductor fabs, and the new generation of AI training clusters all need clean, round-the-clock electricity. Wind and solar cannot supply that on their own, coal is on a tight climate timeline, and large nuclear takes a decade to build. The SMR is the only option that fits both the timeline and the kind of demand the country is generating.

India's stated nuclear target is 100 gigawatts by 2047, a more than tenfold expansion from today's 8.8 gigawatts. Hitting that target needs 4.14 gigawatts of new nuclear capacity every year for twenty-two years, a rate the Nuclear Power Corporation of India cannot deliver alone. The CAIG-NFPRC report is, at its core, a roadmap for crowding in the private capital and the manufacturing ecosystem that timeline demands. SMRs are the asset class private capital can actually price, and they only work if they are cheap, and only cheap at scale.

The fiscal stake is also clear. The report's preferred policy package would cost the exchequer $1.09 billion to support the first ten reactors, through a mix of viability gap funding, GST cuts, customs waivers, and interest subvention. The next fifteen reactors would not need any direct subsidy. Both numbers depend on a single assumption that the manufacturing system delivers.

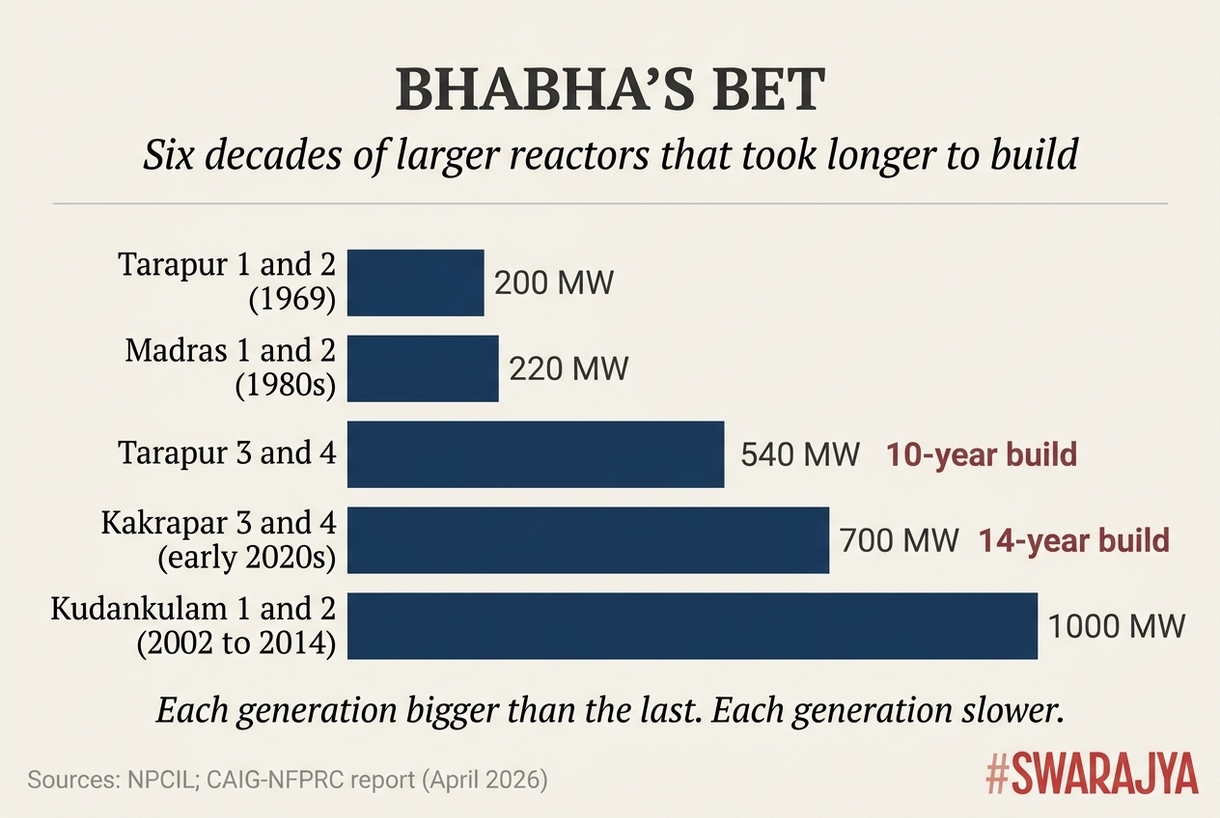

Tarapur is the right place to start. The 1969 reactors set the pattern that every nuclear unit in India would follow for the next fifty years, built one at a time, on its own site, with each new generation bigger than the last. The 220 megawatt pressurised heavy water reactors at Madras Atomic Power Station came online in the 1980s. The 540 megawatt design followed at Tarapur-3 and Tarapur-4. The 700 megawatt PHWR, India's largest indigenous design, entered the order book at Kakrapar, with units 3 and 4 reaching criticality in the early 2020s.

Each generation was bigger than the one before, and each took longer. The 540 megawatt build at Tarapur took ten years. The 700 megawatt build at Kakrapar took fourteen.

The Russian-supplied VVER-1000 units at Kudankulam were the high point of this size-chasing approach. Built between 2002 and 2014 for the first two units, with the third tipped for criticality late this decade, each Kudankulam unit produces a thousand megawatts. India spent six decades getting larger and slower at the same time.

Homi Bhabha's bet, sustained from 1956 onward, was that scale would beat cost. Make a reactor large enough and the per-unit cost would fall, because fixed engineering and licensing costs would be spread across more megawatts. Globally, the bet did not pay off. The cost of large nuclear has risen across the West for forty years, and India's domestic 700 megawatt build came in over budget and behind schedule.

Each generation of Indian reactor was larger than the one before, and each took longer to build. Tarapur's 540 MW units took ten years; Kakrapar's 700 MW build took fourteen.

The SMR thesis inverts Bhabha's bet. Build the reactor small and identical, produce many of them, and the per-unit cost falls because the factory's fixed costs are spread across hundreds of units instead of one. The arithmetic is one thing, and building the industrial machinery to run that arithmetic is another. India has done neither.

The legal framework for the shift arrived in 2025. The Sustainable Harnessing and Advancement of Nuclear Energy for Transforming India Act, known as SHANTI, replaced both the Atomic Energy Act of 1962 and the Civil Liability for Nuclear Damage Act of 2010 in a single move. Section 17(b) of the older liability law had exposed equipment suppliers to open-ended legal risk if an accident occurred, a clause that kept Westinghouse, GE-Hitachi, and Areva away from the Indian market for over a decade. SHANTI removed it.

The new law also graded operator liability by reactor size. The graded ranges, replacing the old flat 1,500 crore rupee cap, run from 100 crore to 3,000 crore depending on installed capacity, with the smaller numbers transforming the insurance economics of small reactors at one stroke.

Three different reactor families followed in quick succession. India and France signed a letter of intent on the joint development of advanced modular reactors. Cooperation with Russia turned to setting up SMR equipment manufacturing inside India. The United States Department of Energy authorised Holtec International to transfer its SMR-300 design to India. Each is a bet on India becoming a fleet operator before any of these partners has finished its own first reactor.

The Bharat Small Modular Reactor is the flagship design under the Nuclear Energy Mission. The government has committed twenty thousand crore rupees to the mission, which targets five indigenously designed units by 2033, including one BSMR-200, four SMR-55s, and a high-temperature gas-cooled reactor at BARC Vizag for hydrogen production.

NPCIL's first commercial tender, issued for the Bharat Small Reactor, a complementary design optimised for private-sector deployment, has drawn expressions of interest from Reliance, Tata Power, Adani Power, Hindalco, JSW Energy, and Jindal Steel & Power. Adani Power has set up a dedicated subsidiary for nuclear generation, transmission, and distribution. None of the six firms has been awarded a contract yet.

The eventual builder will likely be one of them, three of which (Adani, JSW, Jindal) built their existing power businesses on coal, although public-sector contenders such as NTPC's Parmanu Urja Nigam are also in the frame. Six conglomerates see an opening at a moment when decarbonisation, captive industrial demand, and a manufacturing-driven cost curve all line up. Whether the volume actually materialises is the policy question.

The CAIG report is clear about what the multiples logic actually requires. Three things have to be in place.

The first is design freeze, meaning the same reactor repeated with no per-site customisation, so that supplier learning builds up across units instead of starting from zero each time.

The second is factory production, with more than ninety per cent of a reactor's components prefabricated in a controlled industrial environment, shipped to site as modules, and assembled in months rather than years.

The third is a credible demand pipeline, a multi-year order book that gives a private supplier a reason to build the factory in the first place. None of the three has a precedent in the way India's nuclear sector has worked since 1969.

The clearest example of where the supply chain stands today is a small component called the U-tube. These are precision-bent metal tubes that sit inside the steam generators of pressurised water reactors and transfer heat from the primary circuit to the secondary. India once made them, but domestic capacity has shut down because demand was too thin to keep a production line running.

Every U-tube in the BSMR-200's primary circuit will be imported from Argentina. The four-year lead time on an indigenous steam turbine is a similar story. The reactor pressure vessel, which India has the heavy-forging capability to manufacture, has not been ordered in volumes that would justify a dedicated production line.

This is the BHEL-and-L&T problem. India's nuclear engineering ecosystem was built around large, custom, site-assembled reactors. BHEL and Larsen & Toubro have served NPCIL for forty years on terms that look nothing like factory production. Each order has been bespoke, each contract specifies design changes, and each delivery runs months behind.

Switching to factory production needs a different industrial relationship, one in which the buyer commits in advance to twenty-five identical orders, the supplier commits to setting up a factory line, and both sides accept that the first ten units will be expensive while the factory works out its production process. India has done this in other sectors, just not in civilian nuclear.

The closest comparison is wide-body aircraft. A Boeing 787 is a precision machine assembled in months from parts produced in dozens of factories, each spreading its fixed costs across hundreds of orders. The way orders are aggregated, the way supplier networks are organised, the way the design is locked in so production can run, none of this was invented for SMRs.

The model exists, in mature form, elsewhere in heavy industry. India's nuclear sector has been running on a different model for so long that adopting this one means building a new industrial sector almost from scratch.

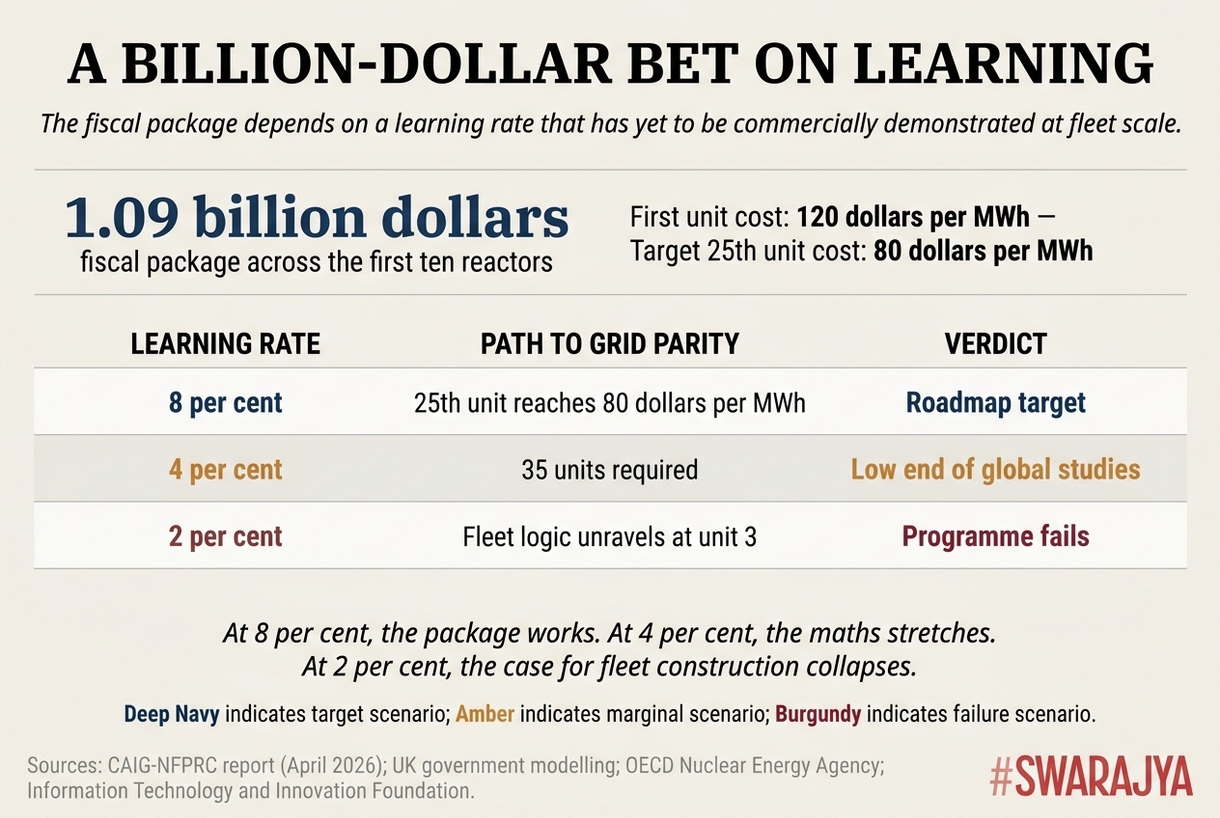

The economic case in the report is built around twenty-five units, deployed as a fleet, with an assumed eight per cent learning rate that brings per-unit cost down from $120 per megawatt-hour on the first reactor to roughly $80 per megawatt-hour on the twenty-fifth. The eight per cent figure is the central case in international SMR analyses, used as a base assumption by UK government modelling, the OECD's Nuclear Energy Agency, and the Information Technology and Innovation Foundation, with four per cent as the typical low-end.

The number is doing a great deal of work. If the rate is four per cent rather than eight, the twenty-fifth unit takes thirty-five units to reach grid parity. At two per cent, the case for fleet construction unravels at the third unit. The hybrid fiscal package of $1.09 billion across the first ten units is built on the eight per cent assumption. The package is a billion-dollar bet on a learning rate that has been modelled extensively across global studies but has yet to be commercially demonstrated at fleet scale.

The hybrid fiscal package is built on the eight per cent assumption. Two-thirds of it disappears at four per cent, and the case for fleet construction collapses at two.

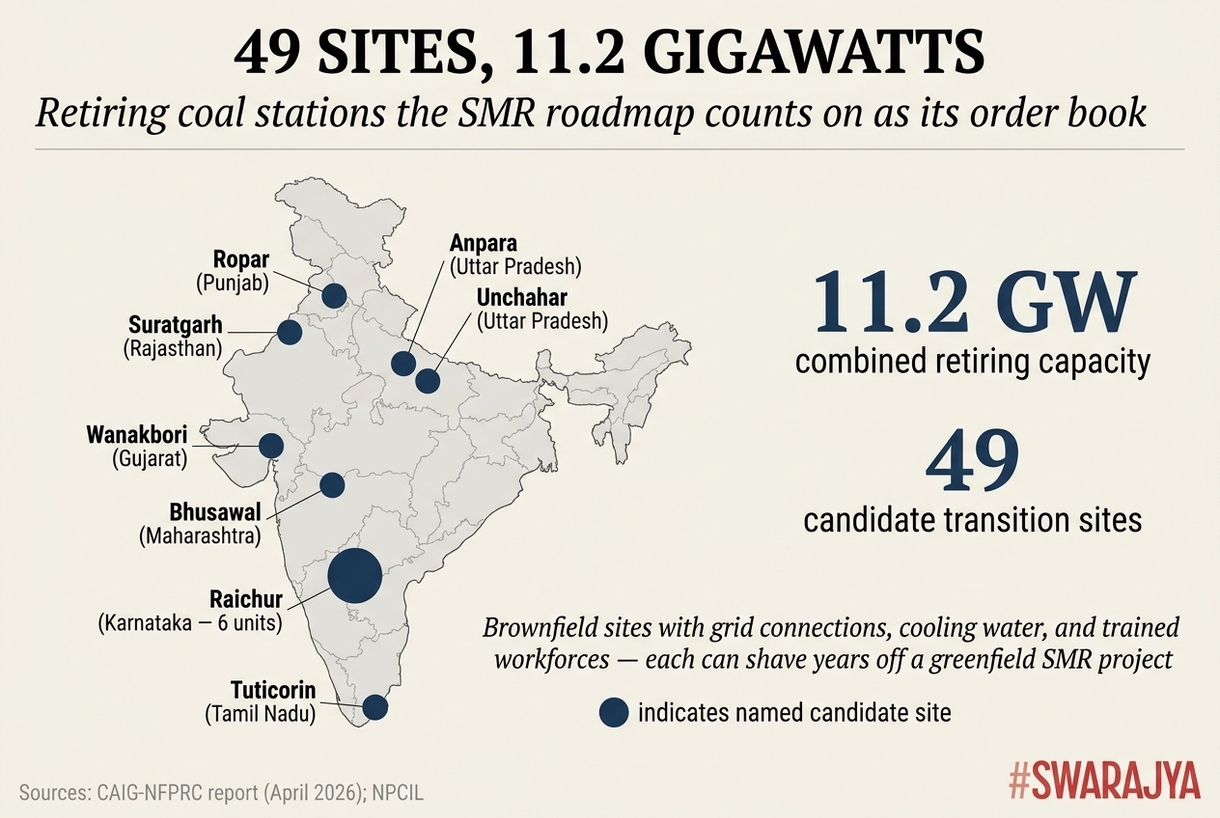

The site map gives the demand side something concrete. The report identifies forty-nine candidate coal-to-SMR transition sites with a combined retirement capacity of 11.2 gigawatts. Anpara in Sonbhadra. Bhusawal in Maharashtra. Wanakbori in Kheda. Raichur in Karnataka, six units. Tuticorin in Thoothukudi. Ropar, Suratgarh, Unchahar.

These are decommissioning thermal stations that come with grid connections, cooling water, and trained workforces, and each can shave several years off a greenfield SMR project. The forty-nine sites are the closest thing India has to a ready-made order book, provided the BSMR-200 and its successors are designed to drop into all of them as identical units, with the design locked in across the fleet.

Forty-nine retiring thermal stations form the closest thing India has to a ready-made SMR order book — provided the BSMR-200 is designed to drop into all of them as identical units.

Whether the forty-nine sites are usable depends on a regulatory architecture the report argues will need to be built almost from scratch for SMRs. Today's atomic siting code requires a 1.6 kilometre exclusion zone and a five kilometre sterile zone around each reactor, a perimeter sized for the 700 megawatt PHWR and the thousand megawatt VVER, drafted before passive-safety designs existed.

Most of the brownfield coal sites lie within five kilometres of villages, schools, irrigation canals, and small industrial estates. Applying the legacy buffer rules to a BSMR-200 deployment at Anpara or Wanakbori would either rule those sites out or trigger a fresh round of land acquisition that the SMR's small footprint was meant to avoid. The report recommends amending the AERB safety code to replace the fixed sixteen kilometre emergency planning zone with a risk-informed range of four hundred to eight hundred metres for SMRs.

The exclusion zone is one piece of a wider regulatory shift. As nuclear scales toward 100 gigawatts and starts trading in competitive electricity markets, the report recommends a formal protocol between the AERB and the Central Electricity Regulatory Commission covering grid integration, dispatch scheduling, and tariff determination.

A Nuclear Energy Single Window, modelled on the National Single Window System, would consolidate environmental, land, water, construction, and grid-connectivity clearances for SMRs into a 180-day track, with only nuclear safety remaining outside its deemed-approval framework. The SHANTI Act's graded liability also needs a further tier for microreactors and portable power modules, with caps in the ten-to-fifty crore range, so that small reactors at remote and captive sites compete with diesel generators rather than thousand-megawatt plants.

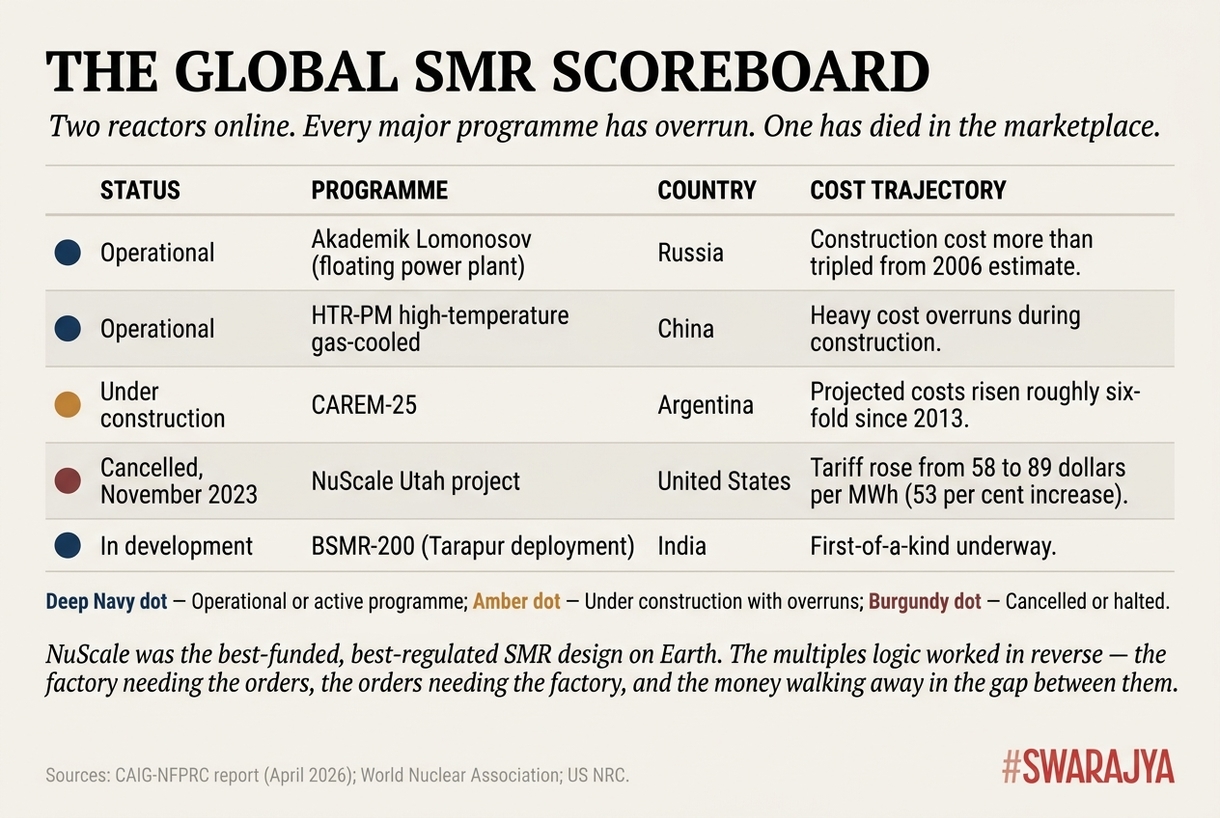

The case for skepticism is strong, and the report acknowledges it. Two SMRs are in commercial operation anywhere in the world today, namely Russia's Akademik Lomonosov floating power plant, online since 2020, and China's HTR-PM high-temperature gas-cooled reactor, online since 2023. Outside those two, every major SMR programme has run into the same wall. Argentina's CAREM-25 has seen its projected costs rise roughly six-fold since work began in 2013.

Russia's Akademik Lomonosov saw its construction costs more than triple from the original 2006 estimate. China's HTR-PM ran heavily over its planned cost during construction. The CAIG report cites all of these and treats them as risks to be managed through fiscal calibration, modular procurement standards, and regulatory adaptation. Whether they are simply risks, or features of the technology that no programme has yet escaped, is the question that hangs over the entire roadmap.

The most instructive failure is American. NuScale Power had the best-funded, best-regulated, most-blessed SMR design on Earth. It was the first SMR design certified by the United States Nuclear Regulatory Commission, in 2023, and it carried Department of Energy cost-share funding. It had twenty-seven utility offtakers signed up through the Utah Associated Municipal Power Systems consortium.

Between 2020 and 2023, the project's contracted tariff rose from $58 per megawatt-hour to $89, an increase of roughly fifty-three per cent as steel, concrete, copper, labour, and interest rates all moved against it. The utility offtakers walked. NuScale's Utah project was cancelled in November 2023, the first SMR programme of any size in any country to die in the marketplace. It died because the multiples logic worked in reverse, with the factory needing the orders, the orders needing the factory, and the money walking away in the gap between them.

Only two SMRs run commercially anywhere. Every major programme has overrun. NuScale's Utah project — the best-funded SMR on Earth — was the first to die in the marketplace.

The skeptic's case is straightforward. The economies-of-multiples logic only works once the multiples appear. A factory only produces units cheaply once it has spread its costs across hundreds of units. Until then, every reactor is a custom build, costing what custom builds cost, with the additional disadvantage that the design has been frozen for production at a stage where engineering changes would still make it cheaper.

In the gap between the first unit and the hundredth, investors leave. NuScale's gap was about thirty dollars per megawatt-hour wide. India is being asked to put up a billion dollars of public money and reform six statutes on the bet that this gap will close in India in ways it has not closed elsewhere.

The strongest part of the report's answer goes beyond engineering and into how demand aggregation can underwrite the manufacturing ecosystem. NuScale died because its American utility customers walked away, and American utility procurement is a thousand independent decisions across a fragmented regulatory environment. India's situation is structurally different. The candidate demand is concentrated and easier for policy to organise.

There are forty-nine retiring coal sites under public-sector ownership. The Railway Energy Management Company has been designated as the anchor demand aggregator for Indian Railways' electricity load. Data centres and semiconductor fabs are offered statutory tax holidays of up to seven years for SMR-sourced electricity, and the Clean Firm Power Obligation phases into a mandate for large industrial consumers by the early 2030s.

The fiscal package of $1.09 billion across ten units, plus customs and GST waivers, covers the gap that NuScale could not get its U.S. utilities to fund. The demand exists, and the open question is whether SMRs capture it.

The harder concession is that the multiples logic still has to be earned. India's domestic enrichment for civilian reactors does not yet exist at commercial scale, and until it does, the BSMR-200 runs on imported slightly enriched uranium from Kazakhstan, Canada, and Russia. The U-tube line in Argentina remains the only line. The bidders responding to NPCIL's tender have never built a reactor, and while their balance sheets are strong, their nuclear engineering experience is zero.

The first ten units will be the hardest, and that is precisely the stretch at which NuScale lost its private capital. What India has, and what NuScale did not, is the room to push the first ten through. The Indian state has built nuclear in this country when private capital wouldn't touch it, and now private capital wants in for the first time. The combination is rare, and it gives the SMR plan its best shot.

Tarapur returns the argument to the same coastline where it began. The two General Electric units of 1969 are still running today, the oldest civilian reactors in India, on a coastline that has now been chosen to host the first BSMR-200. The third reactor on the site will resemble its 1969 siblings in only one respect, which is the megawatts. In every other respect, in its design, its fuel, its supply chain, and its industrial premise, it will represent a different country.

If India builds twenty-five of them, the next twenty-four will be siblings of the third, designed in Mumbai, forged in dedicated production lines that do not yet exist, shipped by rail to sites at Anpara and Wanakbori and Raichur, and assembled in months. Whether India can become that country is now a question for the factory floor, where Bhabha's bet is being tested against its opposite.

Six decades of Indian nuclear engineering have produced reactors. The next decade will have to produce a manufacturing system that produces them in numbers, if the logic of the CAIG report holds. The two skills are different. The first is what India has. The second is what the SMR roadmap is asking it to acquire on a deadline, with a billion dollars of public capital and the plans of six conglomerates riding on whether it does.

A public policy consultant and student of economics.