Call it a “vibe shift”, a “narrative reversal”, or a “reset”. Whatever you call it, 2025 was a rough year for “The Energy Transition”.

This essay is about how we might be able to get things back on track.

But first, it’s important to acknowledge how this collection of technology trends and policy goals that we call “the energy transition” arrived at such a low point.

Back in March of 2025, Dan Yergin — the godfather of energy industry analysts, everywhere — called the whole global endeavor “troubled”.1

In wealthy nations, Yergin argued that the voting public has soundly rejected the idea of paying a substantial premium for energy, or any other basic commodity; while in poor nations, access to low cost energy is existential.

Even more troubling, Yergin emphasized that the energy transition will scramble nearly every aspect of geopolitics. There will be some geopolitical winners whose economic & security positions are improved by a transition away from fossil fuel, but there is also a long list of presumptive losers, who are understandably resistant to change. (I wrote about these tensions myself in “A Tale of Two Energy Superpowers”.) Unfortunately, one of the potential losers is currently the United States, which is a hydrocarbon superpower.

Matt Yglesias, whose beat focuses on US politics, has put an even finer point on the situation here in America. In a recent essay for the New York Times, Yglesias argued that the political “left” has adopted such an uncompromising approach to climate policy that it has undermined the entire Democratic party agenda — including meaningful progress on carbon emissions:

“The benefits of oil & gas to the American economy are large. Natural resource extraction offers good-paying blue-collar jobs. It also generates useful tax revenue. In more abstract terms, it improves the country’s terms of trade — when foreigners are buying oil from us rather than us from them, it reduces the cost of our imports of foreign-made food, clothing and other products, in that way driving down the cost of living for everyone.

This approach makes the perfect the enemy of the good, makes it impossible for Democrats to fulfill their pledges around affordability and stands no chance of securing the congressional majorities that are needed to fund investments in tackling the hard problems of decarbonization.”

Yglesias also does a good job pointing out the practical near-term emissions benefits which can be achieved by expanding, not restricting, American oil & gas supply:

“American oil production is less carbon-intensive than its competitors in Russia, Iran, Iraq and Venezuela. Supplying it to global markets is a win-win for the economy and the global environment.

The case for natural gas is even clearer. It is much cleaner than coal, consumption of which is still high and rising globally. Increased gas production, by displacing coal, has been the single largest driver of American emissions reductions over time. To the extent that foreign countries can be persuaded to rely on American gas exports rather than coal to fill the gaps left by the ongoing build-out of intermittent wind and solar, that’s a climate win.”

Other prominent political analysts have laid out similar, compelling cases — see, for example Josh Barro and Ruy Teixeira.

Even Bill Gates, who for many years has been a prominent advocate for climate policy and investment, has softened his public tone:

Although climate change will have serious consequences—particularly for people in the poorest countries—it will not lead to humanity’s demise. People will be able to live and thrive in most places on Earth for the foreseeable future. Emissions projections have gone down, and with the right policies and investments, innovation will allow us to drive emissions down much further.

Unfortunately, the doomsday outlook is causing much of the climate community to focus too much on near-term emissions goals, and it’s diverting resources from the most effective things we should be doing to improve life in a warming world.

Although climate change will hurt poor people more than anyone else, for the vast majority of them it will not be the only or even the biggest threat to their lives and welfare. The biggest problems are poverty and disease, just as they always have been. Understanding this will let us focus our limited resources on interventions that will have the greatest impact for the most vulnerable people.

At the core of these arguments are three fundamental truths — one might even call them “inconvenient truths” — which have far too often been glossed over by those of us who view climate change as a significant global threat.

Hydrocarbons are extraordinary natural resources. Developing attractive substitutes with much lower carbon emissions is extremely difficult. It’s true that advances in technology have already enabled us to begin reducing emissions in some areas — principally, power generation and ground transportation. However, there are still many gaps in our ability to achieve “net-zero” emissions without imposing a significant drag on the economy. Some of those gaps are so vast that they may not be filled in any of our lifetimes. For example, I’m skeptical that there is a practical, affordable substitute for kerosene in commercial aviation.

There is a tremendous amount of inertia in the global energy system. Attempting to radically transform this system over the course of just a few decades would cause disruptive changes throughout the economy. That’s pretty much inevitable, regardless of how much new technology we develop and commercialize during that period. There will be economic winners and losers, and we should assume that the (presumptive) losers will resist such a rapid transition. Understandably so.

Energy “addition” is just as important as energy “transition”. Energy is at the foundation of human prosperity, and our global civilization will probably seek to consume much more of it for decades to come.

On a personal note, I’ve always prided myself on taking a pragmatic stance in my work as an energy industry analyst. I’m an optimist at heart, especially when it comes to technology, but I always try to be a realist. Even still, as I look in the mirror, I recognize that I have not always fully wrestled with the consequences of these truths.

On the other hand…

As the global zeitgeist has whipsawed from “net-zero” to “energy realism”, I’m afraid we’re at risk of neglecting a fourth truth, which is just as inconvenient:

Climate change remains a big global challenge that needs to be solved. Don’t take my word for it. Those are the words of Chris Wright, the current US Secretary of Energy, spoken during his confirmation hearing:

Energy is critical to human lives. Climate change is a global challenge that we need to solve, and the trade-offs between those two are the decisions politicians make and they’re the decisions that’ll impact the future of our world and the quality of life.

This challenge is not going away, because the risk of climate change is not going away. To be sure, the magnitude and timing of this risk are impossible to fully characterize, because the planetary systems involved are much too complex. There are many specific areas of climate science on which reasonable people disagree. But left unchecked, we have ample evidence that climate change has the potential to cause substantial harm over the course of this century. Gradually cutting greenhouse gas emissions remains a worthy goal — one which I expect to shape public policy around the world for many decades to come.

As usual, the first step is admitting that we have a problem.

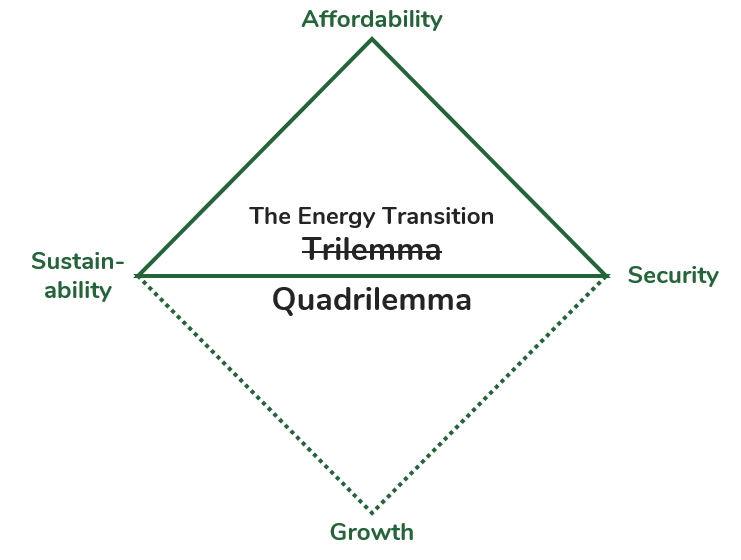

In the case of the energy transition, we have a real dilemma to solve, which I believe Secretary Wright put very succintly. In fact, the energy transition has often been described in recent years as a “trilemma”, which is like a dilemma but with three partially conflicting objectives instead of two: energy affordability, security, and sustainability.

Yet recently, booming power demand has revealed a fourth distinct objective — keeping up with rapid energy demand growth. This is clearly an objective for which our society needs to be better prepared. This addition has caused many of us at Energy Impact Partners to begin referring to our global predicament as a “quadrilemma”.

I really, truly don’t want to turn this into a “quintelemma”. But there is one more critical dimension of the problem that we need to keep in mind: timing.

Back in 2015, the Paris accords called for wealthy countries to pursue a goal of net-zero carbon emissions by roughly “mid-century”. Five years later, that notional target began to be taken seriously within the highest circles of policy & business. By 2022, Larry Fink, the CEO of the world’s largest asset manager Blackrock, asserted in his annual letter to shareholders:

“The next 1,000 unicorns won’t be search engines or social media companies, they’ll be sustainable, scalable innovators – startups that help the world decarbonize and make the energy transition affordable for all consumers.”

Academics began studying pathways to decarbonize the entire economy by 2050 — such as Princeton University’s famous “Net Zero America” project. Cities and states began drafting plans based on a similar mid-century deadline. Thousands of global companies began adopting so-called “science based targets”, which typically meant emissions reduction of 90% or more by 2050.

However, because of that second inconvenient truth — the inertia of the energy system — achieving net-zero emissions by 2050 was never a realistic goal. The energy transition was always going to be a marathon, not a sprint. It may take three or four more decades to reduce emissions by 80-90%. It may take seven or eight. For now, all I can say with certainty is that we’re still in the opening stretch, and voters around the world have made it clear that they tend to prioritize affordability, security, and growth over lower greenhouse gas emissions. There may be some room to maneuver on the margins of these objectives, and public priorities may change over time. But I think we need to assume that the quadrilemma will constrain collective action for the foreseeable future.

This is why I’m convinced that getting the energy transition back on track will require ruthless prioritization in order to determine which compromises are most acceptable for society, and on what timeline.

In the spirit of ruthless prioritization, I’ve narrowed my wish list down to five big themes.

These are the five areas in which I can best envision additional investment leading to significantly reduced emissions, without compromising too much on the other parameters of the quadrilemma. (What form this investment should take, and whether it comes from government or the private sector, are questions that need to be answered on a case-by-case basis.)

From my standpoint as an energy technology investor, I’m convinced that there is fertile ground in all five of these categories for both practical, near-term deployment, as well as big bets on technology moonshots which may take 10+ years to come to fruition.

Lean in to responsible gas

Bring on the nuclear renaissance

Keep pushing solar’s boundaries

2X the grid (at half the cost)

Bolster critical supply chains

For the remainder of this essay, I’ll discuss each of these priorities in turn.

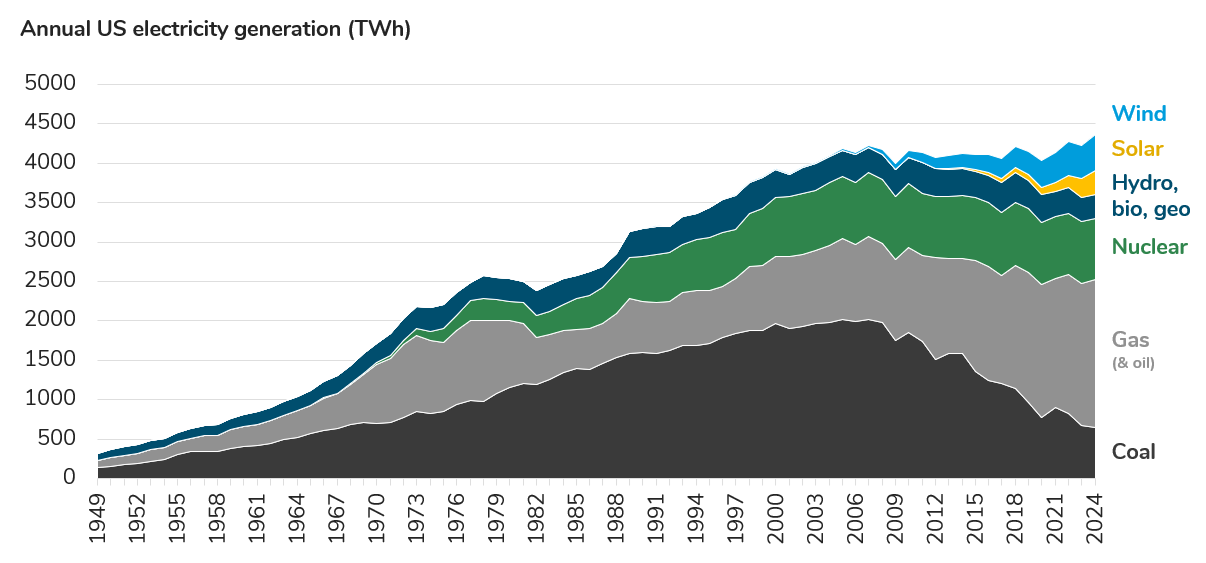

The single greatest success story in the energy transition, to date — when it comes to the sheer magnitude of aggregate emissions reduction — has been the substitution of natural gas for coal in the United States power sector. This trend has largely been a result of the US shale revolution (i.e. “fracking”) which has made North American natural gas into one of the world’s most scalable & affordable primary energy resources.

Plus, there’s the basic fact that natural gas has roughly half the carbon intensity of coal. (In terms of direct CO2 emissions per joule of embodied energy.)

Since the turn of the century, coal’s share of US power generation has fallen from 50% to 15%. As you can see, roughly half of this generation gap has been filled in by natural gas power, while the remainder has been supplied by solar and wind.

Source: United States Energy Information Administration

But in fact, this simplified narrative does not do natural gas justice. The reality is that gas power plants have shouldered most of the burden left by retiring coal plants. Renewables have mostly displaced marginal gas generation — because gas power plants can more easily ramp up and down to accommodate the intermittency of solar and wind power than coal. I’ve often described natural gas as solar and wind power’s “conservative, responsible cousin”, but the fact is, they make a great team.

One especially appealing option for natural gas power is distributed generation. Because natural gas infrastructure is so far-reaching and robust here in the United States, small gas ”gensets” can be deployed fairly efficiently on sites where power is consumed directly — ranging from grocery stores, to hospitals, to gigawatt-scale data centers. These generators can serve as backup power sources for operations that require an additional degree of reliability, while simultaneously offering up capacity to electricity grid operators as a means of balancing out variability in power supply and demand. At Energy Impact Partners, we’ve gotten to know this business well as an investor in Enchanted Rock — an early pioneer and now a leader in deploying & operating “microgrids” with a proprietary genset design.

Quoting my favorite sweatshirt: “Microgrids are dope”.2

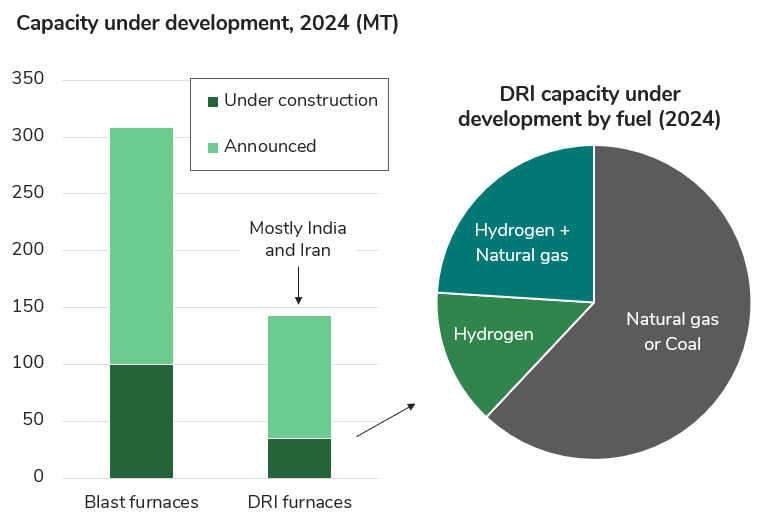

Additionally, natural gas has the potential to reduce emissions well beyond the power sector. Gas is particularly promising as a lower emission fuel in heavy industrial settings. Iron & steel production ought to be a high priority, given the scale of global emissions from coke-fired blast furnaces and the fact that there are reliable commercial alternatives which run on gas: “Direct Reduced Iron” (or “DRI”) furnaces, which are a mature technology. In fact, nearly a third of new steel production capacity under development worldwide is set to employ these furnaces. (As a bonus, the major equipment vendors in the space already offer designs capable of blending in hydrogen, which can potentially be produced in a variety of ways with lower carbon emissions.)

Source: Global Energy Monitor, “Global Iron & Steel Tracker”

Industrial settings are yet another area in which natural gas and renewables may be able to play nicely together. I recently wrote about “thermal battery” technology, which I view as the lowest-cost pathway for converting low-cost, intermittent solar electricity into continuous, high temperature heat — which is the form of energy that’s required in most industrial facilities.

Thermal batteries are not really “batteries” in the colloquial sense of the word, because they store and release energy in the form of heat, not electric power. This is obviously a disadvantage if you need electricity. But, if you’re looking to convert wind or solar electricity into heat — say, to displace natural gas combustion in an industrial process — then thermal storage can be an extremely low-cost, hyper-efficient option.

At Energy Impact Partners, Rondo Energy is our bet in this category. Since we initially invested back in 2021, I’m proud to say that the company has successfully crossed the chasm of full-scale commercial deployment, and has begun lining up real commercial orders. Rondo stores energy in the form of extremely hot bricks reaching well over 1,000 degrees Celsius. This high temperature enables the product to serve nearly all industrial heating loads directly, and bricks are about as cheap as it gets as a thermal storage material.

For an industrial facility with access to ultra-low-cost solar power, the ideal energy solution could very well be a combination of solar energy, thermal storage, and natural gas. The inclusion of a gas boiler in this setup avoids the need to substantially ‘overbuild’ solar and storage in order to supply the facility during occasional lulls in solar output.

Lastly, natural gas has one more obvious virtue as a resource to sustain the global energy transition. This one isn’t techno-economic — it’s geopolitical.

The energy transition is unavoidably going to require some degree of global cooperation, because ultimately that’s the only way for the world to manage a global emissions problem. (For all of you economists out there, we need to find a reasonably fair way to “internalize the externality” across national boundaries.) The United States is a hydrocarbon superpower, but these days we’re especially well known as a natural gas superpower. Hence, expanding the role for natural gas is one of the best ways to give the United States more skin in the energy transition game.

Source: New York Times, “How the US became the world’s biggest gas supplier”, Feb 2024.

There’s always a catch.

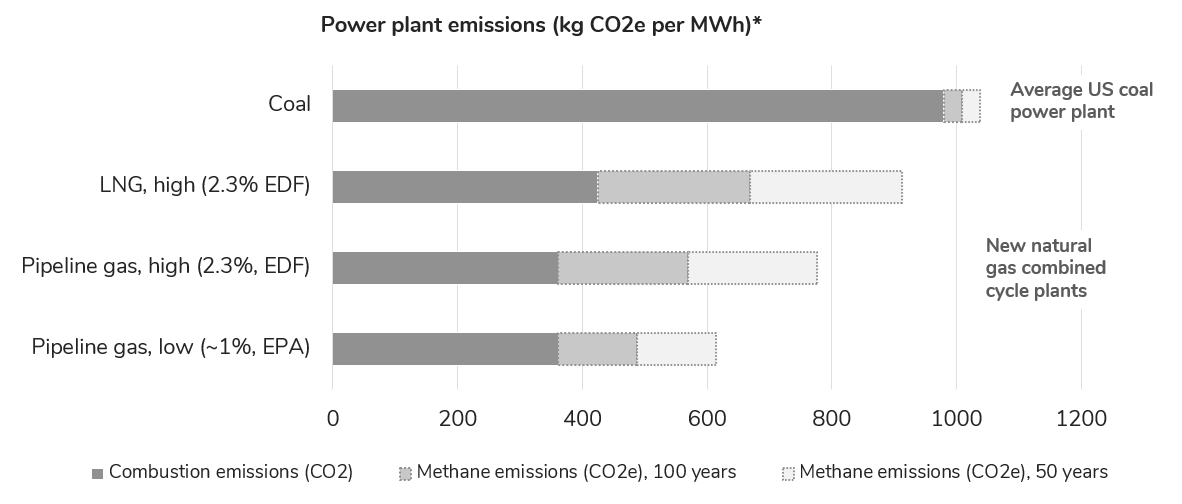

If switching from coal to gas is going to be such a big part of our emissions reduction strategy, we need to make sure that this strategy really, truly reduces greenhouse gas emissions.

This is always the case for natural gas (relative to coal) at the point of combustion. But the energy in natural gas comes from methane, which is itself a powerful greenhouse gas. In fact, a molecule of methane traps about 25 times more heat in the atmosphere than a molecule of carbon-dioxide over the course of the next 100 years, and about 50 times more over the course of the next 50 years.

Unfortunately, methane sometimes leaks.

In some cases, methane is emitted when it’s simply too difficult to capture at a wellhead. In some cases, it leaks by accident from a pipeline or a compressor station. (These emissions are often described as “fugitive”.) Whatever the cause, even a methane leak rate of just 2-3% materially undermines the climate advantage of gas relative to coal. And 2-3% happens to be a reasonable estimate of the average rate of methane emissions from a wellhead to a power plant here in the US.

Sources: US EIA. “Assessment of methane emissions from the U.S. oil and gas supply chain”, Alvarez, et al, Science, June 2018. EPA Inventory of US Greenhouse Gas Emissions and Sinks. Clean Air Task Force, “Analysis of Lifecycle Greenhouse Gas Emissions of Natural Gas and Coal Powered Electricity”, March 2024. “Methane emissions: choosing the right climate metric and time horizon” Balcombe et al, Environmental Science, 2018.

The impact of methane leakage is amplified for liquefied natural gas (or “LNG”), which is the only way in which the US can export natural gas by ship to Europe and Asia. The reason is simple: the process of liquefying gas on one continent and then regasifying it on another consumes about 15% of the gas that’s transported. More gas consumed means more gas lost to leaks. Additionally, more process steps means more locations where those leaks can occur.

So, if we’re going to keep leaning on gas as a major pillar of the energy transition, we need to make sure that our gas is responsibly sourced and delivered. Simply put: that means reducing methane leaks as much as humanly possible. Some leading oil & gas producers have already taken up this charge, even going beyond what’s required by government regulation. My hope is that the industry keeps on pushing the boundaries of what’s possible.

I do have one recommendation: a company in our portfolio at EIP called Oxford Flow.

When you hear the words “revolutionary technology”, my guess is you don’t think about valve technology. But that’s exactly what Oxford Flow has developed: a revolutionary, leak-free valve and regulator design, which also has significant maintenance and reliability benefits. Given that leaky valves and regulators are responsible for more than half of methane emissions from gas pipeline infrastructure, I view this as an especially strong value proposition.

In my role at Energy Impact Partners, I’ve been fortunate to get to know a lot of very experienced power system planners. In my experience with this group, I’ve found that there is near-universal consensus on the need for more nuclear energy in order to achieve ambitious emissions reduction goals.

I wish it weren’t so, but I’ve grown increasingly confident that bottlenecks on electric transmission development and other constraints on siting wind & solar projects are likely to become major limiting factors on the growth of renewables. I believe these limitations will grow increasingly apparent through the 2020s, and will be undeniable by the early 2030s. By then, the world will realize that complete global decarbonization will require another globally-scalable, zero-carbon primary energy resource. Ideally, this resource ought to provide firm, reliable, 24/7 energy supply; even more crucially, it must be extremely power dense. We need to be able to plop it down easily in & around large population centers. What we’re looking for is basically a one-for-one replacement for all of our coal-fired power plants… just without the emissions.

Of course, you know I’m teasing: we already have this magical resource. We have for a long time. In fact, we built the first nuclear plants before the invention of the computerized spreadsheet, and most of those plants are still operating at 90% capacity factors today.2 I repeat: we currently rely on a fleet of nuclear power plants for which key operational and safety calculations were done by hand. By people who thought margarine was the future! And this fleet is arguably the safest source of energy, per joule of energy produced, by nearly any reasonable definition of “safe”. Apart from Chernobyl, there are zero deaths directly attributable to nuclear power plants, globally.

My conviction in the need for a “nuclear renaissance” has only deepened in the past three years since writing that post — not only that a renaissance ought to happen, but that it is happening. Fortunately, more and more people across continents and political lines seem to be coming to the same conclusion.

Here in America, nuclear energy has become one of the vanishingly rare issues on which you’ll find substantial bipartisan consensus. In fact, it’s the only major form of energy for which the two major parties appear to be competing to be more supportive. Signs of a nascent renaissance abound in recent policy headlines.

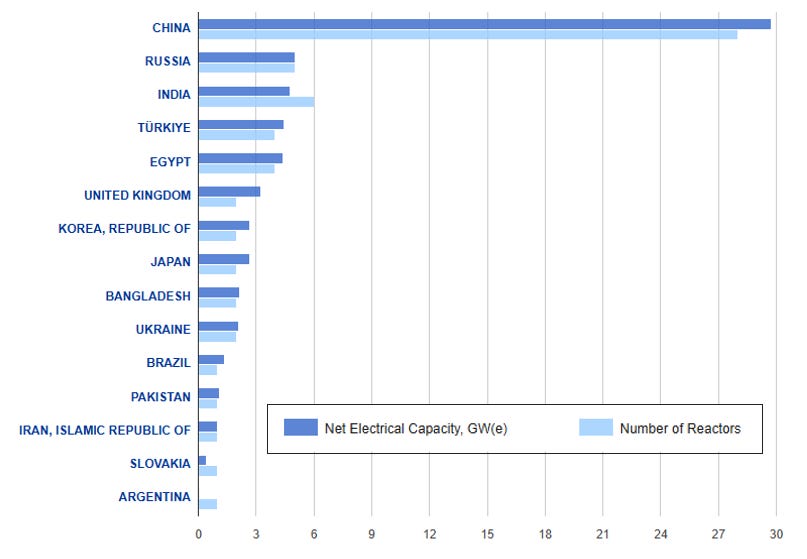

Even more importantly, there are now dozens of new nuclear power plants under construction worldwide. Nearly half are in China, which is unsurprising given the country is building more of just about every form of power generation than any other country in the world. (I was surprised to learn that this boom in power generation even includes natural gas — although this is unfortunately not leading to stronger ties with America.) The remainder of the world’s nuclear projects are fairly widely distributed, but the highest concentration is in poor and middle-income nations — e.g. India, Turkey, Egypt, Bangladesh. This is a very positive sign, because in most cases the only realistic alternative for these countries is coal power.

International Atomic Energy Agency, Power Reactor Information System, Reactors under construction, accessed Jan 2026.

It’s important to note that practically all of these projects are relying on proven, gigawatt-scale, “Gen III+” reactor technology which uses ordinary water as a coolant — just like all of the commercial reactors which have been operating safely, for decades around the world. This is a good reminder that “advanced" nuclear technology such as small, modular reactors (known as “SMRs”) might someday play a big role. However, new technology is not strictly necessary for the next big wave of nuclear deployment.

There are still some major stumbling blocks which could trip up this nascent nuclear renaissance in many parts of the world. Even setting aside nuclear safety and proliferation concerns, there are still three big, interrelated arguments against investing too heavily in nuclear expansion:

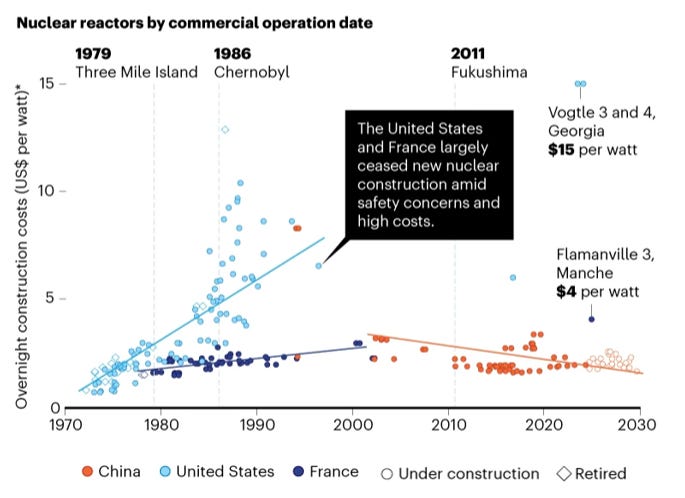

Nuclear energy costs too much. The first new nuclear units brought online in the US in decades, at the Vogtle power plant in Georgia, cost somewhere in the range of $150-200 per MWh. Meanwhile, the cost of energy from new gas power plants has historically been in the range of $50-100 per MWh. (Current gas power costs are at the upper end of this range, given tight constraints on turbine supply and other inflationary factors.)

Nuclear takes too long to build. The Vogtle units took about 15 years to complete, from breaking ground to producing power. This is a big part of the reason that costs spiraled out of control. Construction financing alone amounted to roughly 20% of the total cost of the project! Additionally, so much can change over such a long project timeline… This makes nuclear an enormous bet on energy market conditions that are much too far in the future to predict with any degree of confidence.

It’s not just the magnitude of the cost and construction timelines that weighs on nuclear development — it’s also the uncertainty. The Vogtle project infamously took seven years longer to complete than Southern Company initially projected, and came in about 150% over budget. This is simply too much risk for any major financial institution to stomach. Hence, marshalling private capital is nearly impossible without a rock-solid financial backstop — for example: the government; or a public utility whose regulators are fully on board; or a hyperscaler with an enormous balance sheet.

It doesn’t have to be this way.

I’m convinced that all three of these arguments can be countered, if we can counter them at the root. Nuclear comes with an exceptionally high degree of engineering, supply chain, safety, and security requirements. All together, these requirements make nuclear more reliant than any other form of energy on predictability, uniformity, and repeatability at every step in the project development and construction process. This means that nuclear is inherently much more of a collective action problem than a technology problem.

Hence, in my view, there are three critical conditions which would greatly improve the odds of a successful nuclear renaissance:

A very limited number of reactor designs. Two or three per continent is probably the maximum number that can be made viable in the next twenty years. (Hence, we need to acknowledge that this market is going to be an oligopoly.)

A substantial pipeline of projects, deliberately staged over a long enough period that we can cultivate a robust supply chain, and develop enough human capital to carry the lessons from one project to the next. How substantial does this “substantial” project pipeline need to be, exactly? I have high confidence that the answer is higher than one. Five may be enough. But my best guess is that making rapid progress requires line of sight to at least 10 projects in any given region, staggered to commence construction over a period of about a decade.

The right level of regulatory oversight. Of course, everyone wants to maintain high safety standards for nuclear facilities. Buthistorically, the rules promulgated by the US Nuclear Regulatory Commission (the “NRC”) have been widely perceived as excessively burdensome. Since the turn of the century there have been several attempts to make nuclear regulation more conducive to affordable nuclear deployment — most recently the ADVANCE Act signed by President Biden, and several executive orders issued by President Trump. Hopefully these policy changes begin to make a difference soon.

Unfortunately, these three conditions require the kind of coordination that does not exist in a normal, competitive market environment. Hence, I’m convinced that some degree of ‘central planning’ among stakeholders in government, the nuclear industry, and the power sector will be necessary to get this done.

There’s mounting evidence that success is possible. In countries where the government has made nuclear energy a national priority, nuclear plants are now being completed on time, and on budget, just like they were in America back in the 60’s and 70’s. China in particular has demonstrated the power of a concerted national nuclear program, with recent projects completed at less than a fifth of the cost of Vogtle 3 & 4.

Source: “China reins in the spiraling construction costs of nuclear power — what can other countries learn?”, Liu et al, Nature, July 2025.

I’ve already emphasized that I don’t believe any of this advanced nuclear technology will be necessary for the foreseeable future. Yet it’s still important to consider the potential impact of nascent reactor designs. “Gen IV” concepts, SMRs, and even smaller “microreactors” all boast some interesting theoretical advantages — especially when it comes to their power density and fuel cycle.3 For example, fast reactors like Oklo can run on recycled fuel, which is crucial for reducing long-term demand for primary uranium.

However, the argument that smaller, more modular reactors have an inherent cost advantage over conventional, large units is still entirely theoretical… and debatable.

According to the theory, serial production of key reactor components in controlled, factory settings will make SMRs cheaper & faster to deploy. This is, after all, the case for most goods in the economy. Mass production has an excellent track record.

However, we also know from decades of experience in the electric power sector that there are major economies of scale in building and operating large, individual power plants. The same is true in most other heavy industries, like refining, smelting, and chemical manufacturing. So far, this phenomenon has applied just as much to inherently modular forms of power generation (i.e. solar and wind power) as it has to coal and gas power plants.

And when it comes to nuclear, I’d expect that economies of scale will be even more important, because nuclear plants are invariably going to be burdened by a number of high fixed cost drivers, regardless of whether they generate 10 megawtts or 1,000 megawatts. For example, nuclear projects are always going to be relatively expensive to design and permit, and require outsized investment in physical security. Until we come up with a long-term radioactive waste disposal solution, each plant will also require on-site or near-site storage.

That leaves two big outstanding questions for SMRs. First: What volume of orders does a “reactor factory” need in order to realize the benefits of serial manufacturing. Second: At what point do the advantages of mass production outweigh the advantages of building one big project?

I don’t think there’s any way to answer these questionsbased on theory alone.The only way to discover the answers is by trying to build a bunch of SMRs.

That brings us to one more question: What’s the best way to secure a sufficiently large pipeline of SMR orders to get started?

Once again, I believe the answer probably comes back to coordination. We’re going to need government agencies, nuclear industry leaders, electric utilities, financial institutions, and large energy consumers to all join hands and reach some degree of consensus on a shared roadmap.

So far, I’m sorry to say, the fastest growing group of large energy consumers appear be going in the opposite direction. Of course I’m talking about the hyperscaler data center operators. Each of the largest hyperscalers appears to have selected a different favored SMR technologies to pursue: Meta (Terrapower and Oklo), Google (Kairos), and Amazon (X-Energy).

Notably, none of these splashy announcements features the sole SMR technology that’s already being deployed commercially in North America: the BWRX-300, which is the product of a joint venture between GE Vernova and Hitachi. The first BWRX-300 project just recently broke ground at a site in Ontario.

At Energy Impact Partners, we’ve been obsessed with the challenge of coordination in the nuclear project development process. We’re so convinced that this is the crucial problem in the nuclear industry to solve that we’ve made it the focus of our biggest bet in the nuclear space (so far). Instead of investing in a specific technology, we’ve invested in a project development company — Elementl Power — whose mission is to play a crucial coordination function among all of the key stakeholders in a project, or even better a portfolio of projects. The company is built to support every stage of project development and capital formation, beginning with site selection, permitting, and engineering — and progressing all the way through financing, procurement, and construction.

Lastly, I want to highlight just one more promising pathway for SMRs, which is the maritime propulsion market. As I wrote in a previous post:

There’s a reason that the most important ships in the US Navy — submarines and aircraft carriers, whose missions involve long periods out at sea without a chance to refuel — are nuclear powered.

I’m convinced that nuclear fission is a much better decarbonization pathway for global shipping — as well as intercontinental energy trade — than any of the alternative fuels that are most often proposed. It’s much easier to imagine countries without robust natural energy resources — e.g. Japan & Korea — increasing their reliance on nuclear energy than importing massive amounts of liquefied hydrogen, ammonia, or methanol.

There’s a good case to be made that the maritime sector could be a superior initial market for advanced nuclear technology than stationary power generation.

The shipping industry needs to comply with emissions requirements all around the world.

The incumbent competition, heavy fuel oil, has several weaknesses which give nuclear an edge — namely high fuel costs, logistics challenges, and local air quality impacts (e.g. NOx and particulates).

Hundreds of new cargo ships are built each year, and shipyards could be ideal locations for reactor manufacturing.

The company to watch in this sector is Core Power, whose team has assembled a who’s who of investors and senior advisors from the global shipping industry. I’ll be following their progress closely.

One way in which I believe the climate ‘movement’ (such as it is) has often over-reached in the past five years is by declaring the competition for the “world’s best energy resource” effectively over, with solar and wind power as the obvious winners.

Even Noah Smith, one of my favorite writers on economics and geopolitics, has gotten himself a little too carried away when it comes to renewables. (Example headlines include: “Solar and storage to the rescue”, and “The magic of cheap energy”.)

The reality is much more complicated, because renewables suffer from two major weaknesses. These weaknesses are pretty easy to ignore when the share of solar and wind power in the energy mix is low. But they all become more problematic as we seek to add more and more renewables to the energy mix. Eventually, they become exponentially more problematic.

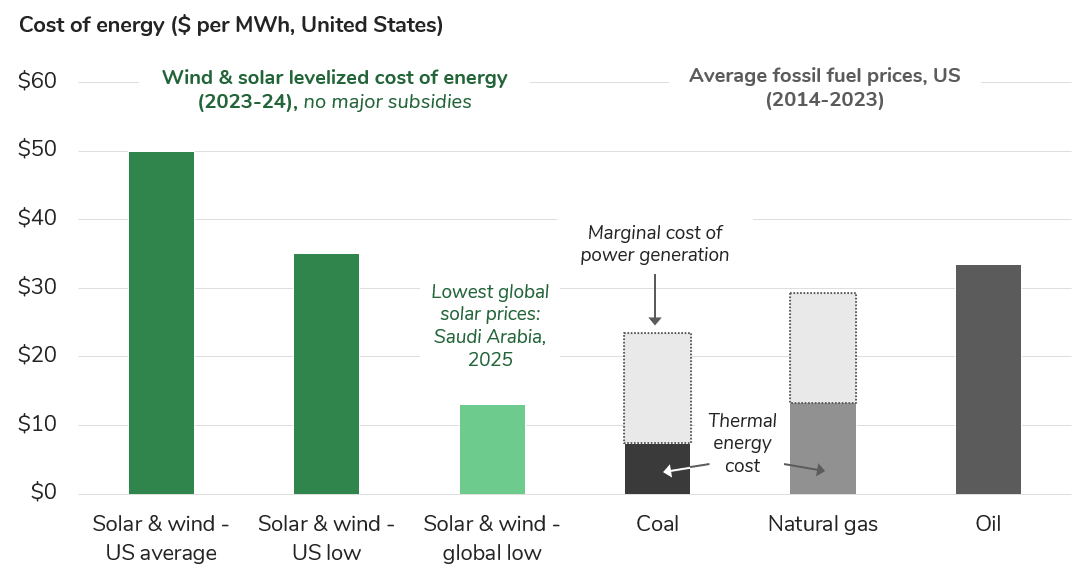

I. Renewables are intermittent. The sun doesn’t shine all the time, and the wind doesn’t blow all the time. Obvious, right? Yet still, the first mistake that many casual reporters make is attempting to compare renewable energy with fossil fuel power generation on the basis of a single metric — the Levelized Cost of Energy, or “LCOE”. This metric aims to capture all of the capital expenditures, fuel, and maintenance costs over the lifetime of a power plant in a single blended price of energy: the price per megawatt-hour.

On that basis, there are indeed many parts of the world where solar and wind power are now cheaper than coal or gas power — when comparing LCOE versus LCOE.

However, because solar and wind power are intermittent, LCOE is not really an appropriate metric for comparison. Broadly speaking, power generated by coal and natural gas combustion provides reliable, “firm” capacity — meaning the ability to produce electricity whenever you need it, for as long as you need it. Solar and wind power, obviously, do not. This is getting a little wonky, but the upshot is that the better economic comparison to make is the LCOE of renewables versus the marginal “burn” cost of coal or gas power generation. On that metric, coal and gas still win pretty handily — even against the cheapest renewables in America (without subsidies).

What about energy storage? (I hear you asking.)

I’m heartened by the pace of progress. As the cost of lithium-ion batteries has declined, we’ve learned how to use batteries to manage some of the short-term variability in renewable generation and energy demand. I’m also convinced that fundamentally lower-cost, safer sodium-ion battery technology is on the fast track to deployment. And I also see even cheaper storage technology on the cusp of commercialization — including technology which can potentially balance supply and demand over multiple days. See: Form Energy, one of our portfolio companies at EIP, which just announced the world’s biggest battery project with Xcel Energy and Google in Minnesota.

So yes, the combination of renewables and storage, or even just storage by itself (renewables optional) can now sometimes compete with gas power to provide a share of the dispatchable capacity needs of the power system. This makes economic comparisons increasingly complicated. It’s easy to get lost in the weeds. The right methodology for selecting an optimal mix of resources is still a live question among people who model the dynamics of the energy system for a living.

My take-away is that low-cost storage can make renewables more competitive in most scenarios. But it’s far from a panacea, because storage always represents additional cost. The more storage you need to add to the system, the more additional expense you need to tack on to every incremental megawatt of solar or wind.

II. Renewables are geographically constrained.

It’s much sunnier and windier in some places than others.

There is much more open land in some places than others.

There is also much more transmission infrastructure in some places than others.

Some places have more litigious neighbors than others.

Etc, etc.

Here’s how I recently summed up the state of play:

Today, pretty much anywhere in the world where you can find plentiful sun or wind, plenty of open space to build on, and transmission capacity to deliver power to population centers, solar and wind energy are now fairly attractive energy resources. Yet even in the very best locations in the United States, they’re not quite competitive with the marginal cost of burning fossil fuel to generate electricity, today, without relying on subsidies.

As you can see, there are indeed parts of the world where the LCOE of solar and wind can undercut the marginal cost of fossil fuel generation. For example, in Saudi Arabia…

It’s fair to say that solar power is already the cheapest source of electricity in the world… in a region with the best solar resources on the planet, practically endless open space, low-cost labor largely imported from developing countries, and a strong (ahem…) central government which has made solar a priority.

Moreover, regardless of where they’re built, solar and wind projects take up vast amounts of space. Their low “power density” and bulky physical footprints invariably raise objections on environmental and aesthetic grounds. The more renewables we add, the farther afield we need to travel to find viable sites. In the US, this cycle has led to increasing pushback from communities and conservation groups concerned about the loss of natural landscapes and wildlife habitat. (See my prior post, “Locals Against Renewables”.)

Those of us advocating for more renewable energy need to acknowledge the weight of these downsides, I believe, with much more gravity than we have in the past. I suspect we’ll be wrestling with this set of trade-offs for decades to come.

And yet, despite these glaring weaknesses, I’m still optimistic about the future of renewable energy — especially solar.

Solar is the only primary energy resource we have that is proven in the terawatts, infinitely scalable, zero emissions, and has a pathway to competitiveness on every continent.4 Wind energy, while also extremely attractive in some parts of the world, is more beholden to geography, and less likely to become much cheaper than it is today. Case in point: While there is an extraordinary amount of wind energy available in the Great Plains of North America, Europe has already been forced to turn offshore for more viable wind resources. And even the cheapest offshore wind energy is currently three to five times more expensive than the cheapest wind power on land.

If you take the long view — the civilizational view, as I’m trying to do in this series — then I believe the cost of energy embodied in a lump of coal is the ultimate target for renewables, or any other low-carbon primary energy resource. I believe that solar is the only option we have with a fighting chance of accomplishing this mission.

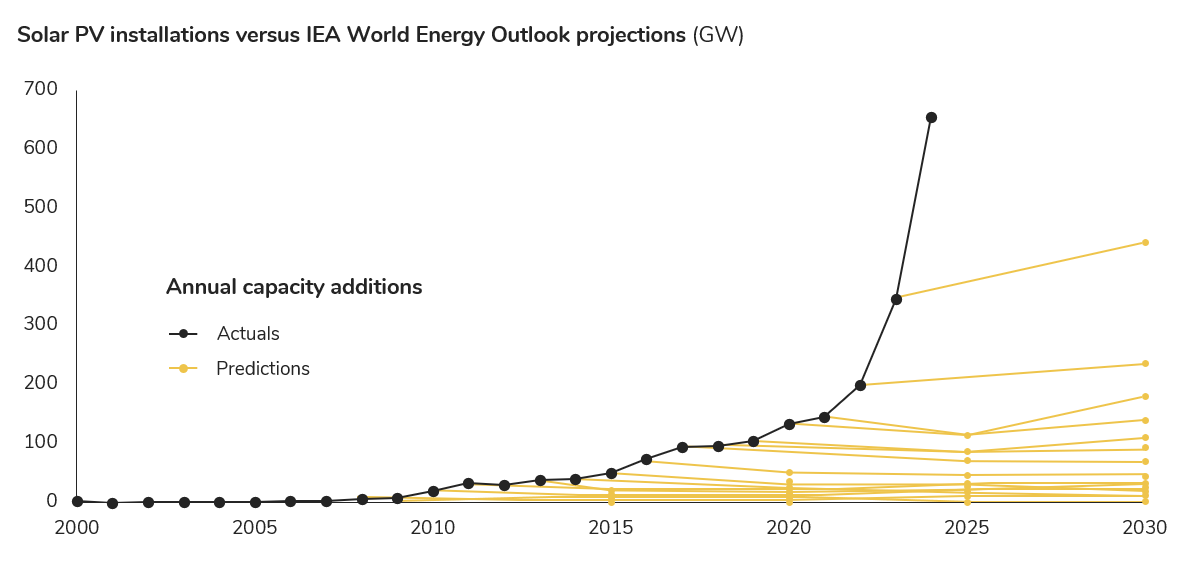

This chart from The Economist — destined to be a modern classic — illustrates solar’s track record to date. Solar has been on a fifteen year streak, proving doubters wrong. (At least, doubters at the International Energy Agency…)

Source: The Economist, “Sun Machines”, June 2024

So what does all of this mean for the future of the energy transition?

It means that solar will almost certainly continue to be a growing contributor to the energy system in many parts of the world. However, solar’s cost curve will not just keep on trending asymptotically downwards, nor will solar deployment keep on trending exponentially upwards, because of some natural law. In fact, we should generally anticipate that adding more solar energy will become more difficult over time. So if we want to keep pushing solar’s boundaries, we’re going to need to invest in making solar energy cheaper to deploy.

What does this mean in practice? I’d recommend three priorities:

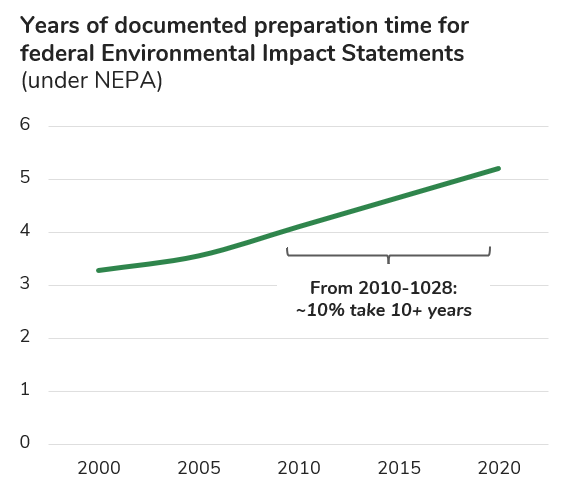

Clear a path to tap into the best solar resources in every region. This largely means investing in power grid expansion — a theme I’ll return to in the next section. However, this can also mean regulatory reform — targeting policies which put an undue burden on solar energy development. We absolutely need to be thoughtful about solar’s land use impacts. In some cases, however, the solar industry now has nearly as much reason to complain about excessive environmental regulation as the fossil fuel industry. Here in the US, the National Environmental Policy Act (or “NEPA”) has been a frequent culprit. Fortunately, I believe this is yet another area of national policy in which there is a strong foundation of bipartisan support… just waiting for the right political breakthrough.

Source: “2018 ANNUAL NEPA REPORT of the National Environmental Policy Act (NEPA) Practice”, National Association of Environmental Professionals, Nov 2019.

Instead of bringing the cheapest solar energy to demand centers, by building more transmission lines, consider bringing demand centers to the cheapest solar. I expect that the lowest cost solar resources in the world may begin to lure energy-intensive industrial activities away from large population centers. Perhaps, they might even begin to lure some large consumers, like data centers or industrial facilities, away from the electricity grid. This prospect has caused a small but growing group of schemers to wonder: “Is the future of low-carbon industry off-grid?”

Invest in technology to continue pushing solar energy down the cost curve. I won’t go into depth on this topic here, because I recently did so in another post on “crazy cheap solar”. In short: I’m confident that there are multiple strategies for chipping away at the cost of solar over time. I believe there may even be a path to cutting the cost of solar by another 50% or more, but there is unlikely to be a single breakthrough that gets us there. Instead, our best bet may be a paradigm shift that spans the entire architecture of a solar project, from photovoltaic materials, to structural elements, and installation labor. (We have a thesis on what this might look like at EIP, and an investment that I look forward to sharing when I can! Hint: perovskites.)

Electric power grids are wonders of the modern world — the biggest interconnected machines humans have ever built, by nearly any definition of the words “biggest”, “interconnected”, and “machine”. They’re the unsung heroes of civilization.

We use electricity every second of every day. Water falls on one side of a dam. Turbines spin. Copper moves through magnetic fields. Electrons get pushed. The push travels through hundreds of miles of wire at nearly light speed. It reaches your house. It makes electrons move through a motor. Your fan turns on. Water falling in one place makes a motor spin in another place, miles away, connected by nothing but thin, metal wire. That’s insane.

Think about how extraordinary this is. Two hundred years ago, none of this existed. Then we discovered these forces. We figured out how to manipulate them. We built machines that could generate electricity, transmit it across vast distances, and use it to do useful work. And in doing so, we completely transformed human civilization.

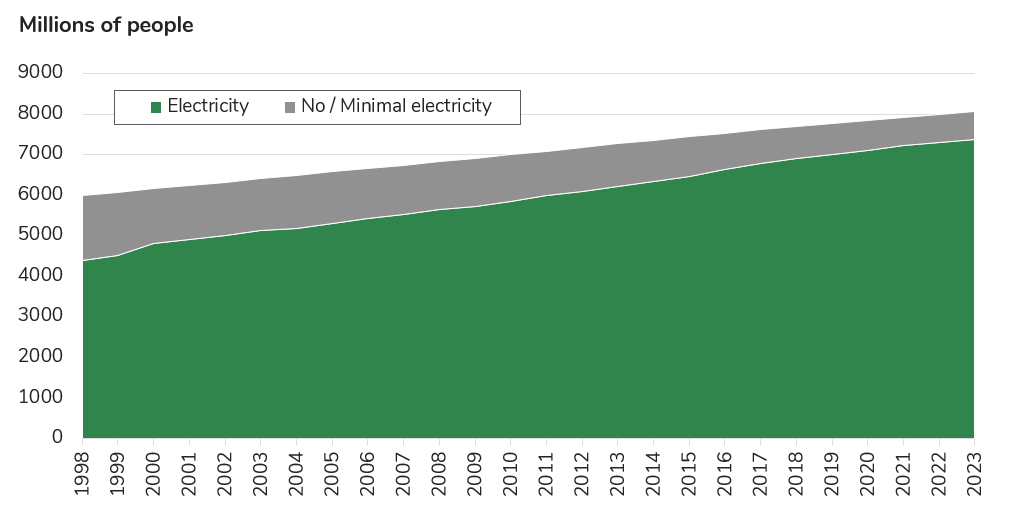

Building out power grids around the world was one of the greatest human achievements of the last century, and the project continues to this day. We’re continuing to make progress on reducing the share of humanity without access to the miracle of electric power, which has fallen by more than 50% since the turn of the century. India deserves special recognition for an extremely ambitious push to expand & strengthen the grid. The country now has the world’s third largest high voltage transmission system and nearly 100% electricity access.

Source: Our World in Data

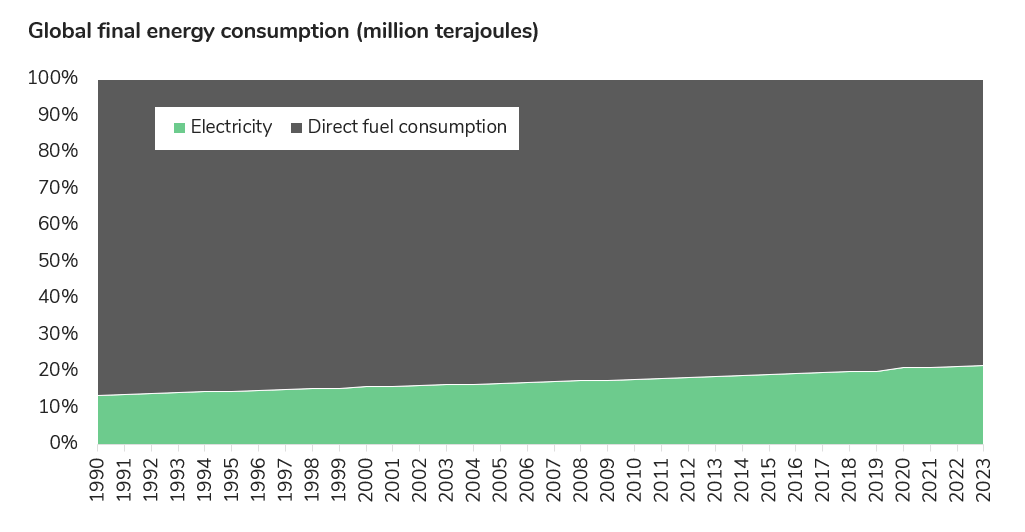

Expanding access to the power grid in poor countries has enabled electricity to gradually increase its share of total “final” energy consumption since the turn of the century. For the most part, electricity’s gain has come at the expense of traditional biomass energy resources — e.g. agricultural waste. But electricity is also beginning to claim additional market share from fossil fuel in two areas: ground transportation (electric vehicles), and space heating (electric heat pumps).

And of course, there’s now an even higher-profile source of additional electricity demand growth: AI data centers. The potential scale of AI demand is enormous, although there is still an extremely high degree of uncertainty in the trajectory of demand growth beyond the next few years.

However, we have yet to see any of these new sources of electricity demand make a material difference when it comes to the global rate of “electrification”, which has remained fairly steady for decades. Electricity now makes up just over a fifth of all global energy consumption.

Source: IEA, “Total final consumption (TFC) by source, World, 1990-2023”

If you spend any time in energy transition circles, you’ve probably heard the slogan "Electrify Everything” — a rallying cry for the rapid transition away from fossil fuel in every sector of the economy. I suspect that this is one of those slogans which was initially intended to be taken “seriously, not literally”, but spun out of control. In any case, I believe this is another example of overreach on the part of many climate advocacy groups, which has probably done more harm than good.

On the other hand, I also believe that electrification is crucial for the energy transition, and one of the most inevitable mega-trends we’re living through today.

I say “inevitable”, because I’m convinced that there are multiple sectors in which electrification is on track to win on the merits, even if you forget all about carbon emissions.

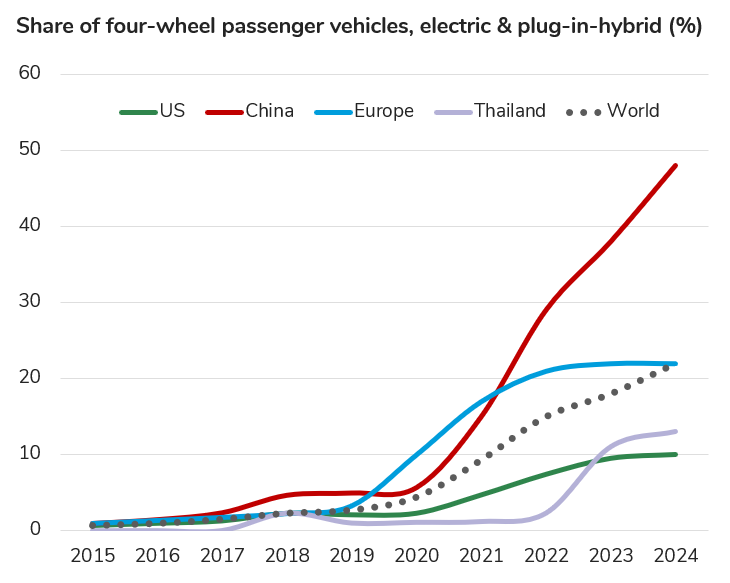

Electric vehicle adoption has stalled out in North America. But globally speaking, the transition to EVs is still underway — beginning with passenger vehicles, but already progressing into the medium and heavy duty segments. Around the world, more than 30% of passenger vehicles sold are now electric; and EVs are only becoming more attractive as battery technology improves and the electric drivetrain flexes demonstrates its fundamental advantages over the internal combustion engine. For example, EVs are an especially good fit for autonomous vehicles, which are just beginning to take off. (“Autonomy is real now”.)

Source: IEA

Electric heat pump technology is also steadily improving. There are still some major obstacles to widespread deployment in colder climates. However, heat pumps are still my primary answer to the question “How will we keep warm in the winter?”. Products like the Quilt ductless heat pump make this an easier choice for homeowners. And I’m convinced that ground-source heat pumps are on track to capture an increasing share of the market for heating and cooling larger buildings. (See: Bedrock Energy, an EIP portfolio company, whose drilling technology has begun to reduce the cost of ground-source projects.)

Source: Bedrock Energy.

Industrial process heat, which accounts for about a quarter of all global energy consumption, is also a candidate for electrification in some circumstances. High-temperature heat pumps and thermal storage technology both show great promise in this domain. Meanwhile, the vast majority of modern manufacturing processes which demand a high degree of precision — such as semiconductor fabrication and battery cell production — are already highly electrified. The same goes for the whole field of robotics.

When you add up all of these growing sources of power demand, plus consider the need to build more transmission lines to access cheap renewable energy… I trust you’ll agree that “2X” is probably a conservative estimate of how much more grid capacity we’ll need.

Yet even just doubling the grid is an extremely daunting proposition.

One of the biggest themes of Steel For Fuel over the past three years has been “The Electricity Gauntlet” — a metaphor I’ve been using to describe the precarious path that the electric power sector needs to navigate amidst surging demand for energy, and critical bottlenecks in nearly every step in the supply chain.

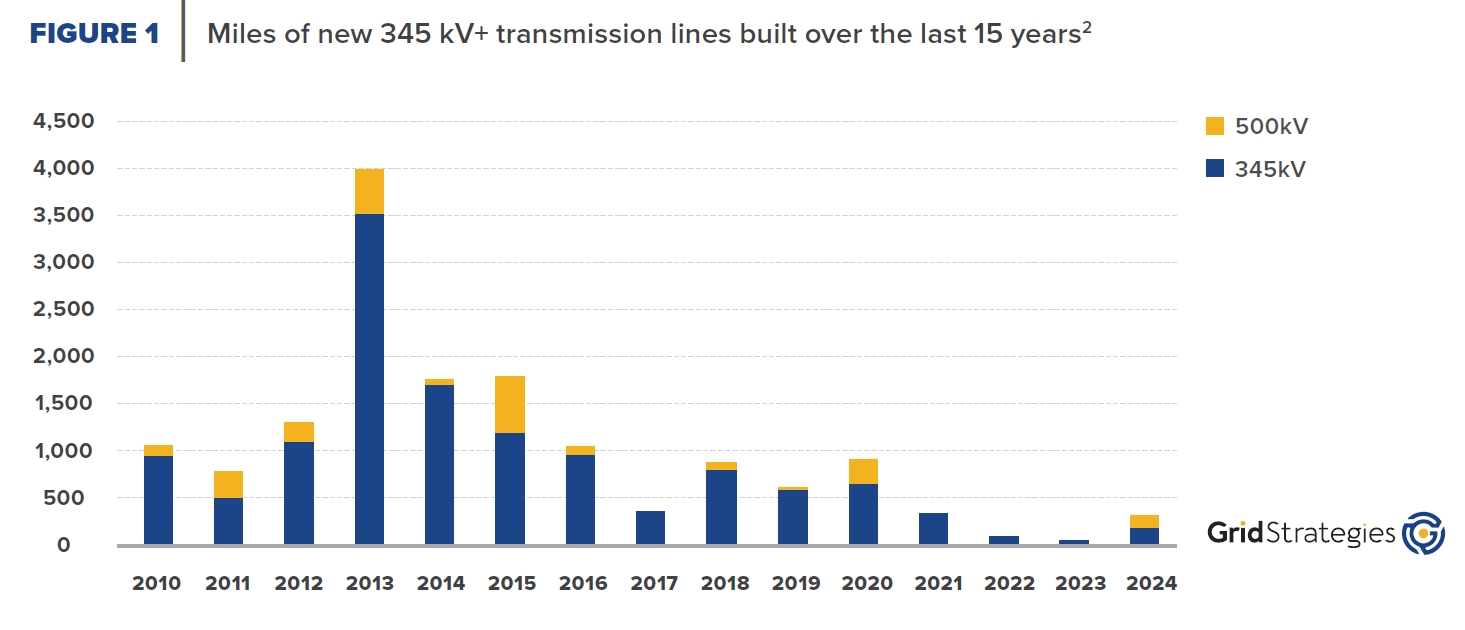

In “Where Have All the Transmission Lines Gone?” I chronicled the slowdown in electric transmission construction over the past decade, which is now beginning to stymie both large power generation and large load interconnection. Here’s some fresh data from the top-notch research team at Grid Strategies.

Source: Grid Strategies, “FEWER NEW MILES”, July 2025.

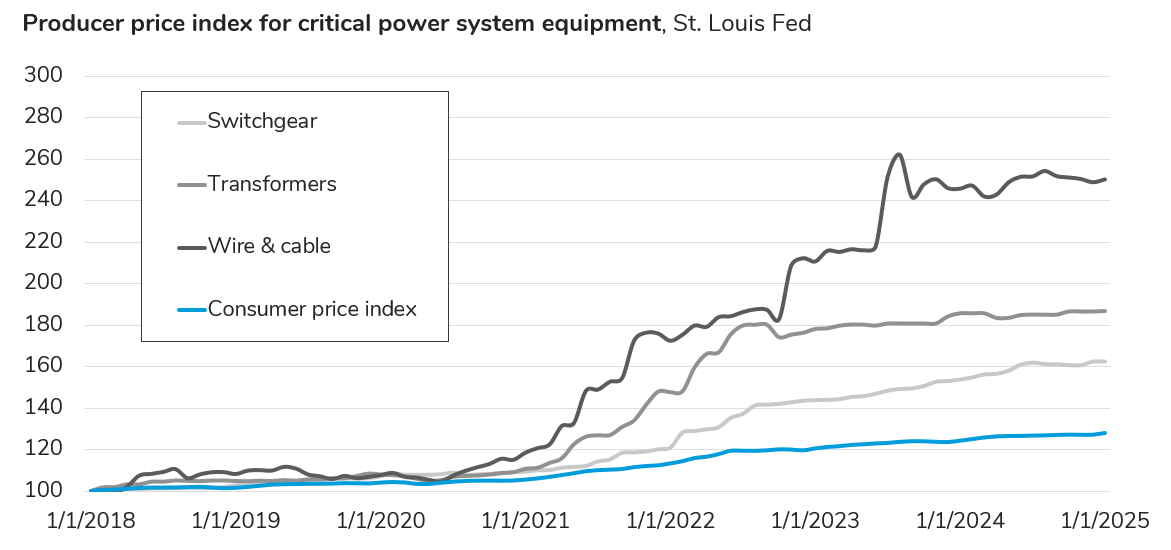

In “The Price of Power Grids” I charted the rising cost of critical power delivery equipment, including transformers, switchgear, and conductors.

Source: St. Louis Federal Reserve FRED database, Producer Price Indices

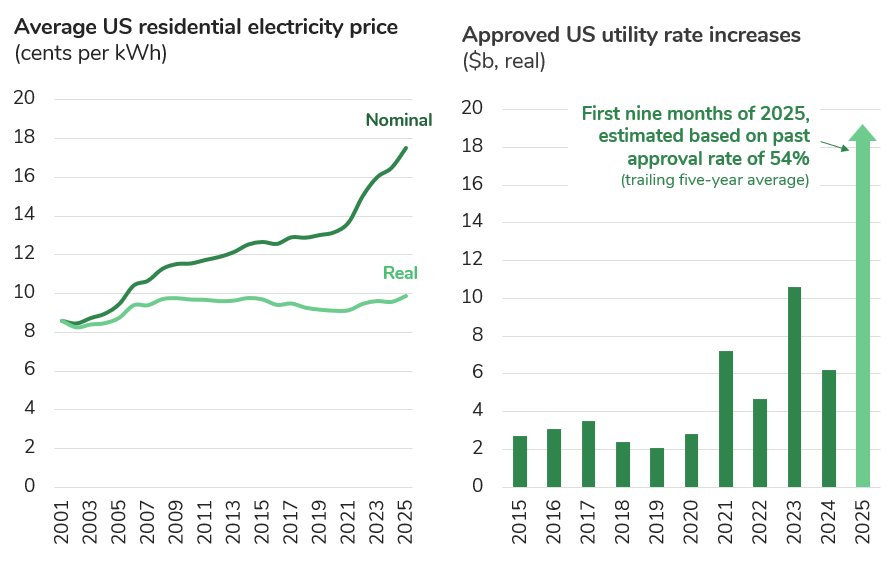

Meanwhile, pressure on electric utilities is mounting as energy affordability has become a more politically salient issue. The truth is that electricity prices have not been rising much faster than general inflation. However, as an essential good delivered with a monthly bill, electricity prices tend to be top of mind for many consumers. Plus, utility rate increases are continuing to surge even as the overall rate of inflation has been tamed.

Sources: S&P Global, Regulatory Research Associates “Rate Case History” database. Powerlines, “Utility Bills Are Rising, Q2 2025 Update”, July 2025.

Against this backdrop, it’s not enough to say that we need to 2X the grid. We need to figure out how to 2X the grid at a much lower cost. (Roughly half the cost seems like a reasonable north star.)

Better technology will definitely need to play a role. There are a wide range of nascent solutions in the market — often labeled “grid enhancing technologies” (or “GETS”) — which aim to increase the throughput of the grid without having to put a lot more “steel in the ground”. (Or aluminum, or copper, for that matter.) Some of these solutions, like “dynamic line ratings” are finally beginning to gain some real commercial traction.

My personal favorite among these solutions is conductor coatings. Admittedly I’m a bit biased, because EIP was an early investor in AssetCool, a startup company with a proprietary coating material, which as the name suggests, keeps power lines cooler. This enables transmission lines to carry more power regardless of the weather. AssetCool has made this solution especially compelling by developing a robotic “crawler” solution which means that the coating can be applied cheaply and safely to existing lines. Out of all the various categories of GETS I’ve encountered, I believe this solution offers the greatest amount of additional capacity per dollar of investment, and it might also be the fastest to deploy.

Source: AssetCool

Another promising area of grid technology is a domain referred to as “power electronics”.

Essentially, this means semiconductor technology applied to the conversion and control of electricity, rather than manipulating data. Historically, these specialized chips were used in consumer electronics, not “grid scale” applications. But the rise of solar and battery storage led to initial experimentation, and now widespread deployment in grid settings. The reason is that the grid runs on alternating current, while solar panels and batteries run on direct current; and power electronics happen to be the most efficient means of converting from AC to DC power flow, and back again. Now we’re seeing demand for power conversion equipment surge even higher, as microchips and all sorts of high-precision industrial equipment are also native to DC.

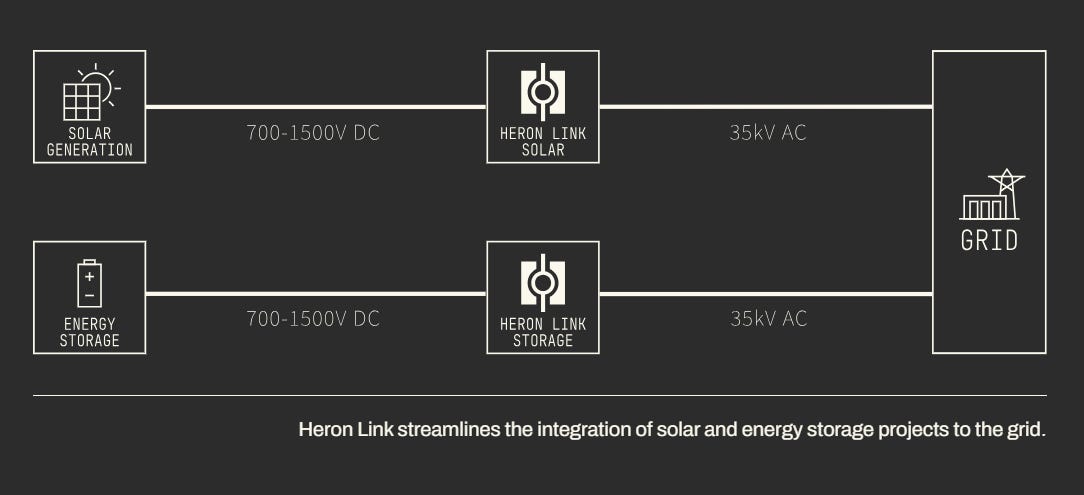

Skyrocketing demand, falling costs, and steadily improving performance: power electronics have quietly followed the same trajectory as solar and batteries in the past fifteen years. Most importantly, from a technical standpoint, the industry has scaled up manufacturing of “wide bandgap” semiconductor materials, which can handle higher voltages and frequencies. This means that we can now take advantage of the inherent advantages of power electronics in a wider range of settings. The company to watch in this space is Heron Power, one of our portfolio companies at EIP. Heron has assembled an unparalleled team to develop a new class of product — a hybrid electric transformer and converter — which essentially combines two big, expensive pieces of critical power supply equipment into one. The result is a smaller, cheaper solution which can offer a much higher degree of control to power grid operators.

Source: Heron Power

Suffice to say I’m growing more & more optimistic about electric transmission & distribution technology.

I wish I could say the same for T&D policy here in America. Because, ultimately, just like nuclear energy, I believe that electric transmission is more of a collective action problem for governments and citizens than it is a puzzle for engineers. Long-distance transmission, in particular, often needs to cut across state lines and even regional planning boundaries. This is the most crucial category of transmission expansion for tapping into more low-cost renewable power, and improving our resilience against extreme weather or security events. These lines also tend to be very good for energy consumers. Studies have historically found that major new inter-regional lines would have benefit cost ratios of 2:1 or higher.

The challenge, of course, is that consumers are not necessarily aware of these benefits, but they are certainly aware of the costs. As I wrote all the way back in my first post here at Steel For Fuel:

Building a large-scale electrical grid the first time around certainly wasn’t easy, but at least it was fairly obvious to the early 20th century public that the benefits of electrification would outweigh the costs. The second time around, the typical public response to expanding the grid seems to be: “I already have my washing machine and flat screen TV, thank you very much. Not in MY backyard!”

Hence, hurdles to siting & permitting big infrastructure projects have come to impose a heavy burden on new transmission development – particularly in the case of long lines that need to cross multiple jurisdictions. In every county you cross, there’s a commissioner who demands to know how his or her town will benefit from the “eyesore” you’re planning to erect.

Fortunately, this is another area in which I’ve seen political consensus beginning to build across party lines. I’m cautiously optimistic about some recent activity, particularly Order 1977 from the Federal Energy Regulatory Commission, or FERC, in which the agency asserted its “backstop” siting authority in a small number of designated National Interest Electric Transmission Corridors. Transmission permitting would also be well served by the kinds of reforms to environmental permitting (e.g. NEPA) which I touched on earlier.

There are clearly political compromises to be forged here. But once again, I believe that compromise requires us all to take a pragmatic stance — one which acknowledges the need for continued investment in fossil fuel infrastructure, including new oil & gas pipelines, alongside the power grid.

There is no greater testament to our ability to think and plan long-term, to cooperate at continental scale, and to share in the costs and benefits of large capital investments than the electricity grid. We now face a new generational test of those abilities. We need to pass!

Arguably, the energy transition should really be referred to as a “mineral transition”.

Today we mine hydrocarbons from beneath the earth. Over time, we’ll need to mine more of practically everything else in order to manufacture their substitutes.

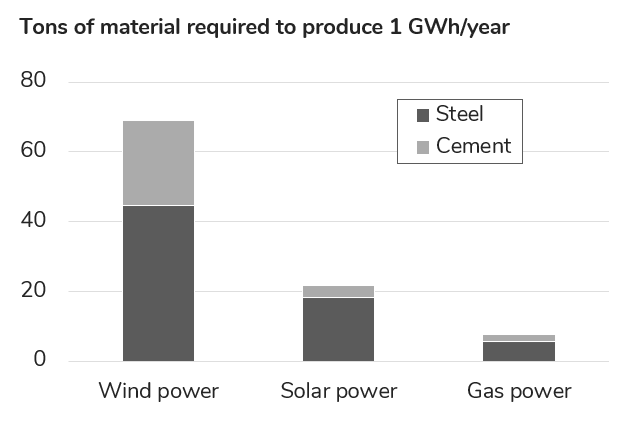

The name of this blog, Steel For Fuel, refers to the most prominent of these mineral substitutions: swapping out fossil fuel in favor of the world’s number one construction material, steel. Steel is used to build wind turbine towers, solar foundations, and nuclear reactors. Steel constitutes most of the mass of the power grid. (The most common conductor material, ACSR, is aluminum reinforced with steel, and nearly every transformer has a core made of specialized electrical steel.)

Hence, from a bird’s eye view, the energy transition is mostly a transition from hydrogen & carbon to iron.

Sources: “Raw materials demand for wind and solar PV technologies in the transition towards a decarbonised energy system”, European Commission, 2020. “Life Cycle Environmental Impact of Onshore and Offshore Wind Farms in Texas”, Chipindula et al, Sustainability, June 2018. “Life cycle Assessment of a Natural Gas Combined Cycle Power Generation System”, NREL, Sept 2000.

But iron is the least of our problems.

There are a whole host of other minerals which are required for solar, wind, batteries, and electric vehicles. Most are much less abundant than iron. Some have no practical substitutes. Back in 2021, the International Energy Agency published a landmark report assessing the impact of various decarbonization scenarios on demand for these critical minerals — ranging from heavy hitters like copper and lithium to more highly specialized role players like manganese, molybdenum, and zinc. The headline conclusion was that the agency’s benchmark “sustainable development” scenario would require about four times as much total mass of these minerals within twenty years.

In my view, the three most important minerals to watch are:

Copper, often lauded as “the element of electrification” because of its crucial role in electrical generators, motors, and lightweight, high conductivity wires. (An electric vehicle uses more than twice as much copper as a gasoline or diesel vehicle.)

Lithium, which is the foundational element in lithium-ion batteries — which are almost certainly going to remain the dominant battery technology from here on out. (Lithium’s position as the lightest metal on the periodic table gives lithium-based batteries an inherent energy density advantage.)

“Rare earth elements” — a group of heavy metals with especially useful properties for producing permanent magnet motors. This makes rare earths especially valuable for electric vehicles, and all kinds of robotics. (Some of these elements also play crucial roles in other important products, such as defense systems.)

[One note: Uranium would probably be fourth on my list: yet another critical energy transition mineral facing a potential imbalance in supply and demand.]

Each of these critical minerals comes with its own distinct set of challenges, but they share a common big picture predicament:

We’re going to need a lot more aggregate mining capacity. Unfortunately, developing entirely new mines is difficult, risky, and usually takes more than a decade from discovery to production.

Regardless of where these minerals are extracted from the earth, China has developed a dominant position in the refining and processing steps in the supply chain. In part, that’s because these steps often require intensive thermal or chemical processes which cause major permitting headaches in other countries. But it’s also because China has clearly become the industrial center of gravity and the biggest locus of demand for the products that emerge from these supply chains.

Copper is a good case study. Frankly, in my view, copper mining is probably the most worrisome of all the possible bottlenecks in the energy transition. This is partially due to the sheer magnitude of the problem. Copper is already the world’s fourth most important metal by aggregate tonnage. Every 1% increase in copper demand is equivalent to nearly 10,000 times the amount of copper embodied in the statue of liberty!

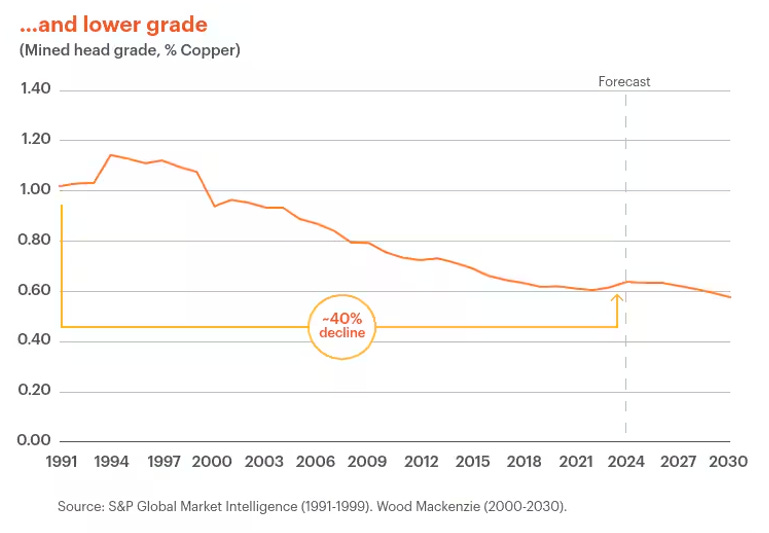

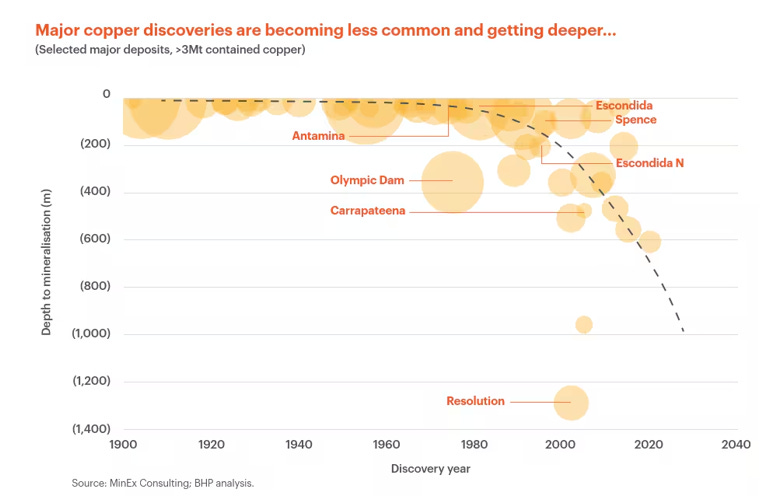

There are also glaring constraints on the supply side of the equation. In the past two years, the global mining giant BHP and the industry analyst firm S&P Global both published analyses on the challenges ahead for copper supply. If you’d like to delve deeper, they are both well worth a read.5 Summarizing the conclusions: Over the course of the past few decades, major new copper deposits have been taking longer to discover, and mines have taken a lot longer to bring online. The ore that we do find tends to be lower-grade, and buried deeper underground. Hence, in the words of BHP’s lead analysts:

We think the price setting marginal tonne will come from either a lower-grade brownfield expansion in a mature jurisdiction, or a higher-grade greenfield in a higher risk and/or emerging jurisdiction. None of these sources of metal is likely to come cheaply, easily, or unfortunately — promptly. [Emphasis added.]

BHP Insights, Sam Farrell and Laura Whitton, “How copper will shape our future”, Sept 2024.

BHP Insights, Sam Farrell and Laura Whitton, “How copper will shape our future”, Sept 2024.

One potential solution to this kind of problem is novel refining technology. Better solutions for extracting metal from lower quality ores (or brines) are especially valuable, because they can enable more production from existing mines. In the case of copper, some of the world’s biggest mines are sitting on a wealth of “primary sulfides”. This is an ore from which copper has historically been too expensive to extract, yet these sulfides make up about 70% of known copper resources worldwide.

At EIP, we invested in a company with a novel chemical process for leaching copper from these sulfide ores, called Ceibo. We believe Ceibo’s technology could be a game changer for this overlooked source of new copper supply. Last June, the company produced its first copper output from a demonstration plant in Chile. (Chile is the world’s leading copper producer, and unsurprisingly, also a wellspring of the best technical talent in the field.)

Another option for copper — along with lithium, rare earths, and all the rest — is to improve the rate of recycling.

To be clear, recycling can’t solve the whole problem for any of these minerals, because demand is growing too quickly. However, the recycling rate for most of these minerals leaves a lot of room for improvement. Copper is actually doing okay in this respect, with a global recycling rate above 50%. But the rates of recycling for lithium and rare earths — both still in the early days of a massive, global growth cycle — are much, much lower. Current estimates for rare earth recycling are in the range of 1-3%. Hence, I’m excited about the rapid progress clocked by another EIP portfolio company, Cyclic Materials, which has developed a better hydrometallurgical process for recovering rare earth metals from both scrap and end-of-life products. Cyclic is aready beginning to reclaim valuable material from the motors in electric vehicles, drones, hard disc drives, and wind turbine blades.

Source: Cyclic Materials

Let’s imagine that the world gets a handle on these critical mineral supply challenges. Not only are we able to increase our aggregate supply of raw material; we’re also able to open some new mines closer to home in North America and Europe, and establish more processing capacity outside of China…

Unfortunately, that would only address the first half of the energy transition’s supply chain security predicament.

We also need the ability to convert these raw materials into finished goods: solar panels, batteries, and permanent magnet motors. As much as possible, any nation or ‘bloc’ pursuing a greater degree of geopolitical autonomy needs to be able to produce these goods within their borders — not all of what they need, but at least a meaningful share. Otherwise, I fear that the energy transition will always be vulnerable to geopolitical whiplash.

Moreover, these products are quickly becoming more “critical” well beyond the context of the energy transition.

Solar panels are a cheap, quick-to-deploy source of energy for AI.

Batteries are the power source of choice for cheap, agile military drones.

Servo motors are the literal prime movers of the robotics revolution, which has obvious implications for both defense and nearly every civilian industry.

The United States has made modest progress building the capacity to manufacture these products in recent years. Substantial incentives for solar and battery manufacturing were introduced by the Inflation Reduction Act under President Biden, and were retained in the One Big Beautiful Bill Act under President Trump. In fact, the OBBBA strengthened the requirements for sourcing components from outside of China — and added an incentive for domestic content.

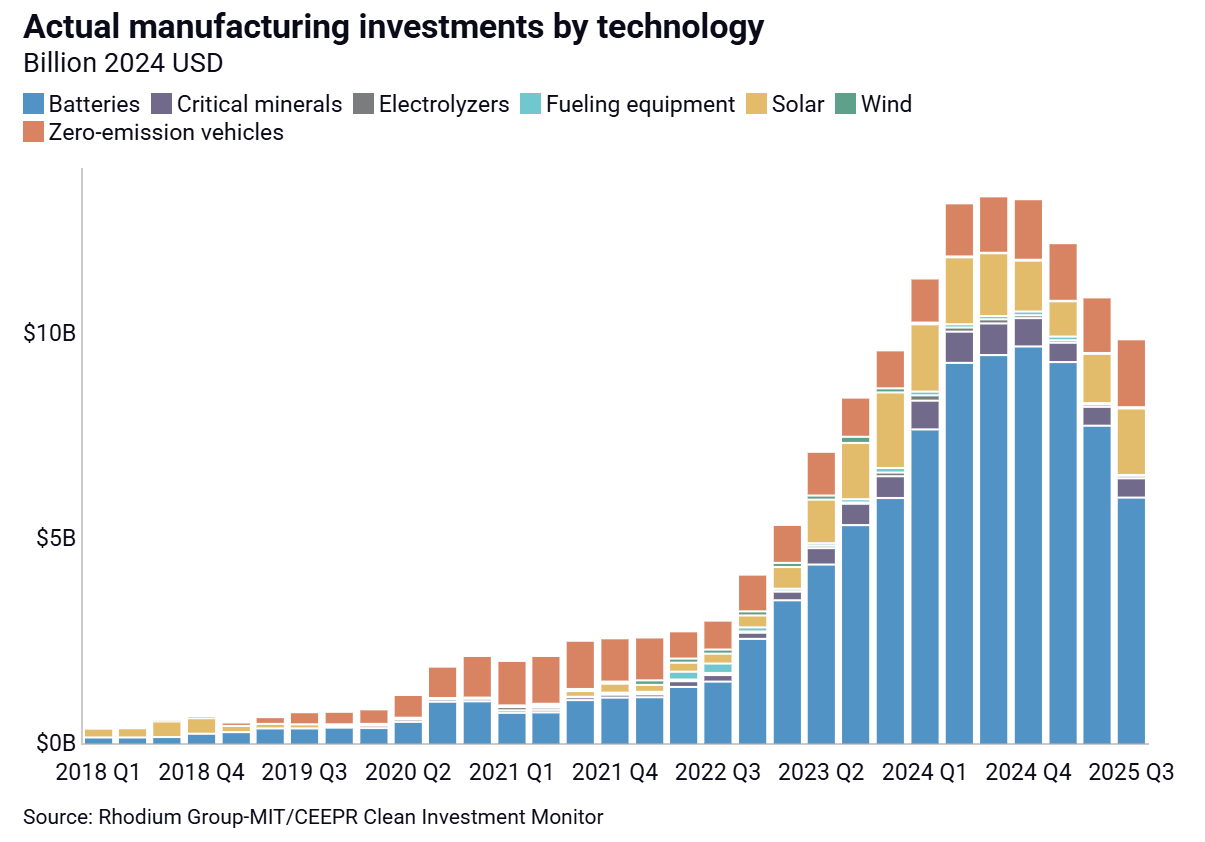

On the other hand, there have already also been some major bumps in the road for Western supply chains. (And “bumps in the road” is putting it lightly…) In Europe, Northvolt raised billions of dollars by positioning itself as the continent’s battery manufacturing champion. But the company struggled to scale up production while hitting crucial cost and performance metrics, and was ultimately forced to declare bankruptcy. Meanwhile, all three major American automakers have been forced to write off billions of dollars of investment in battery and electric vehicle manufacturing as demand growth failed to materialize: $26 billion for Stellantis; $19.5 billion for Ford; and $7.6 billion for GM. That amounts to a little less than half of the total capital invested in those segments in the past five years (as tracked by the Rhodium Group). The same dataset shows a marked decline in battery manufacturing investment in particular since the US government changed hands in January 2025.

Source: Rhodium Group Clean Energy Investment Monitor, Q3 2025, November 2025.

But on the other, other hand, I still see a positive signal in the data on energy transition manufacturing in America. Tens of billions of dollars in investment are still in play. Most of the new factories erected with this capital are just beginning to ramp up production. For example, LG Energy recently opened America’s first major domestic lithium-iron-phosphate (LFP) gigafactory. Hyundai (also in partnership with LG) opened America’s biggest “gigafactory” for manufacturing lithium-ion batteries and electric vehicles to date, in rural Georgia.6 This enormous campus is now one of the most highly automated factories in the entire country, with more than one “robot” for every two human workers. America is going to need a lot more of this kind of automation in order to contest China’s industrial might.

These examples illustrate an important lesson for Americans and Europeans seeking to wean themselves off of Chinese manufacturing, without sacrificing too much energy transition momentum: We can’t do this alone.

China has developed multiple tech-industrial ecosystems that overlap... China doesn’t just have a smartphone industry or a battery industry or an electric vehicle industry. It has all of these industries and more. China’s strength across multiple overlapping industries creates a compounding effect for its industrial policy efforts.

Source: Kyle Chan, High Capacity, Jan 2025.

The odds that either America or Europe can set up entirely independent, competitive ecosystems, all on their own, is very low. Hence, I believe that Americans and Europeans will need to collaborate closely with the only entities which currently approach China’s technical mastery: mostly Korean & Japanese firms, such as LG Energy, Samsung, SK ON, and Panasonic. These partnerships will be especially crucial when it comes to the most difficult manufacturing processes, which tend to be the intermediate steps in between the production of critical minerals and finished products. For example: forming perfect cyrstaline silicon ingots and then slicing them into razor thin photovoltaic wafers; or synthesizing battery electrode materials with just the right formula and particle structure.

Historically it has proven fiendishly difficult to get these processes right without years of real operational experience. As the saying goes: “You need to megawatt before you can gigawatt”.

I’d also suggest that Americans and Europeans ought to double or triple down on our pursuit of differentiated technology pathways which could theoretically bypass China’s incumbent supply chains.

I acknowledge that this is no easy feat. In the history of the solar market, there has been exactly one major success story for any “alternative” photoltaic technology: the thin film cells developed by First Solar. But I believe this is an exception that ought to dispel the rule. Of course this kind of technology success story is vanishingly rare — that doesn’t make them less important. First Solar’s technology has proven to be an invaluable hedge against geopolitical risk — it’s clear as day in the company’s stock price. In this period of mounting tension, First Solar is already bolstering America’s domestic solar manufacturing capabilities, having recently opened a new $1.1 billion manufacturing facility in Louisiana.

We should prioritize a lot more big bets on alternative processes or materials which have the potential to leapfrog incumbent approaches. (Once again I’ll gesture towards perovskites.) I’m especially interested in leaner, cleaner manufacturing processes, because what works for China is often unlikely to work for wealthier democracies with higher labor and environmental standards.

One final word on geopolitics: I want to emphasize that I’d prefer a world in which America, Europe, China, and other major geopolitical players regain enough mutual trust to collaborate on technology transfer and cross-border investment in all of these areas.

But the purpose of this essay is to accept the world as it is, not as I wish it were.

All of the above may sound like a “five point plan”. I assure you it’s not intended to be. Five point plans are dangerous things, and you should always be wary of people trying to sell you one.

In fact, my biggest lesson from over fifteen years as an energy industry analyst is that sticking to any kind of “plan” will probably put you in the wrong head space. Plans are meant to be followed, and the path of the energy transition is simply too long and winding to map out ahead of time. It’s impossible to see just a single decade into the future, let alone five or six of them.

Priorities are different from plans. They’re temporary stances, not maps. They’re meant to evolve over time. They still require us to make difficult choices, because prioritization always implies deprioritization. However, those choices are not intended to be set in stone. For example, you’ll notice that the idea of “carbon removal” doesn’t feature in my current list of priorities. That’s because I don’t believe it has a big role to play in this decade or the next. But my bet is that it will become a priority, at some point, before the end of the century.

I remain convinced that transitioning our global civilization towards lower-carbon energy will be an important priority for decades to come. But in order to make sure this task remains a priority for the majority of the population, we need to respect the quadrilemma. We need to be focused, but flexible.

I hope you’ll join me in refocusing on a set of priorities which can set us up for a triumphant Return of the Energy Transition.