At the beginning of July 2025, Windsurf was generating north of $100M in annual recurring revenue. Enterprise ARR was doubling quarter over quarter. OpenAI wanted to buy them for $3 billion. By any normal startup metric, this company was crushing.

When OpenAI’s deal fell through, Google moved fast. But what made Google’s move crazy was that they didn’t buy the company.

Instead, they paid $2.4 billion for a non-exclusive license to some of Windsurf’s technology and hired the co-founders and 40 senior engineers into DeepMind. Non-exclusive – meaning they didn’t even lock up the IP. And four months later, Google launched Antigravity – a competing IDE built by the people who built Windsurf, aimed directly at the users they’d left behind.

Google spent $2.4 billion, and a significant chunk of the return on that investment is a product designed to harvest Windsurf’s own user base. That bet only makes sense if you believe there’s nothing tying those users to the original product. No switching costs. No lock-in. No moat. Just users on an open field, waiting to use whatever’s best that week.

This isn’t just a Windsurf story. I think it’s the defining strategic reality for an entire generation of AI companies – the game has changed. Google bet $2.4 billion that traditional moats don’t matter in AI land. I think they’re right. And I think it breaks everything we know about strategy.

People throw around the term strategy all over the place in business, but there’s actually a more formalized definition to learn about if you go to business school. I didn’t go to business school, so I don’t have a clue what it is, but that’s fine. We’ll figure it out.

So there’s this guy, Hamilton Helmer, and he’s got this formula for the power of a business strategy: power = benefit + barrier. The benefit is the value a customer gets from your business. It saves them time or money or sparks joy or whatever. The barrier is all the reasons competitors and incumbents can’t easily copy the thing you do. The combination of those two things are your power. Helmer says there’s seven of these things.

Scale Economies: Make more stuff, pay cheaper prices for the individual pieces. Hyperscaler clouds like AWS and Azure are one of the most obvious examples of scale economies, and it’s why they can crush open-source businesses. Open-source businesses all inevitably offer a managed, hosted version of their software, but they have to handle the hosting. Almost always, they do that by hosting their services on the hyperscalers. And then the hyperscalers take note and realize there’s a big, growing business. They own bajillions of servers, get them for dirt cheap because they buy bajillions of them, and then can offer services at cheaper cost, because it costs them less to offer it up. Simple math. (And the hyperscaler is making money off the open-source company’s hosting the whole time. It’s basically a predatory business model where the hyperscalers get to double dip).

Network Economies (network effects): The canonical examples are social media. When all your friends are on Instagram, you have more incentive to join Instagram and engage. In the B2B world, ecosystems often drive network effects. I’d call out Salesforce, which is like a prison that everybody opts into. I detest Salesforce’s UX. It’s so clunky. Salesforce’s UX is proof that network effects can overcome literally any amount of human suffering. Businesses keep buying Salesforce not because it’s the best product out there, but because the ecosystem (partners, developers, users) around it is so damn valuable and hard to replicate. One really unusual example of a B2B network effect is Snowflake’s data sharing capabilities – Snowflake customers built revenue models off being able to share data really easily with their customers, and it makes Snowflake very sticky to be part of a company’s core value proposition.

Counter‑Positioning: Blockbuster vs. Netflix. That’s the standard example. Blockbuster made money off of late fees, and Netflix said simply “no late fees.” Blockbuster competing against that would have completely cannibalized their revenue stream, and they didn’t dare until it was way too late. The ClickHouse vs. Datadog fight is going to look similar. Datadog’s charging you per host, per GB ingested, per module. ClickHouse says “it’s cool, store all your data, we’re fast, cheap, and you can query it directly with your agents.” Datadog could totally do this too. They have talented engineers. But Datadog’s never going to adopt this model because it would fully crater their existing business. They’d effectively be telling their customers “you don’t really need our UIs or per-host pricing, just this database we built.”

Switching Costs: The thing that’s going to save Datadog’s hide is that leaving Datadog means losing all of the value of the years you’ve spent building dashboards, alerts, queries in their proprietary language, their integrations. You’d have to rebuild it all from scratch. In B2B sales, where I spend most of my time, switching costs often come up, because buyers regularly decide they want to switch off of a product, but still have to renew their contracts because they don’t have enough time to switch off, and end up double paying for products while they migrate.

Branding: Apple is one of the most obvious brand power examples – a massive chunk of their valuation is just the brand. My first job out of college was with a columnar database company called Vertica, and when they got acquired by HP, I was so bitter about it because it was one of the better products out there, and some of the other lower quality products (cough cough, Greenplum) got sold for way more. Not because of the strength of their technology, but because of the strength of their brand. Similarly, there’s the old trope: nobody gets fired for buying IBM (I mean they didn’t a couple decades ago. Today, maybe not so much).

Cornered Resource: If you own a mine, you own the land, and you own the resources on it. No one else can dig it up. In AI land, this is usually the proprietary dataset. Coding agents’ completions datasets (everything users say to coding agents and whether they accept or reject edits) is a solid example of this. This is also the reason so many publishers and actors are up in arms over AIs using their likeness or copyrighted works. Those are valuable cornered resources. The key is that these resources have to be genuinely unavailable to other competitors.

Process Power: This is really about how you build your product. Toyota’s legendary production systems are the standard B-school example. SpaceX has been able to iterate extremely rapidly because they’re not afraid to blow up a rocket here or there. In the AI world, one example would be the willingness of a company to have a roadmap that extends only out a month or two. Plan beyond a month, and you might miss the next big agent-building trend.

Ok, so those are the seven powers. Here’s the problem: agents are destroying most of them.

Let’s start with the most obvious casualty: switching costs. I tried a bunch of coding agents over the past year. I’ve used four or five at this point. And then I got to Claude Code. And I liked Claude Code better, so I switched to that. That’s it. There was nothing I lost by switching. There was no rebuilding of my systems, or reconfiguring of my settings. I just used the new thing. And most of the coding agents have that same dynamic. It costs you nothing to switch, so you just use whatever is best at the moment. A natural next step is for vendors to start fine-tuning, to make your product better at the more specific task. But the risk to any vertical AI business that’s started fine-tuning its own models is that if those models don’t keep up with what the frontier labs are offering, and there isn’t some other force driving switching cost, there’s actually a benefit to switching. That is a damning proposition. But Anthropic experiences these same switching cost issues. The other day, Claude had a serious outage. What did I do? Well, I opened up my ChatGPT Enterprise subscription, and kept working.

I’m not sure true network effects exist in AI applications yet. A lot of people point to coding completions data as one, drawing on a concept from Matt Turck called ‘data network effects‘ – the idea that your product becomes smarter as it gets more data from your users. Turck’s original examples were things like Google Search and Waze, where there’s a constant incorporation of new data to improve the underlying models. But the AI application version is seriously weaker. When more developers use a Cursor or a Replit, they get more training data, just like Google does – but that data doesn’t do anything on its own. Someone has to fine-tune a model on it, ship the model, and hope the frontier hasn’t moved in the meantime. It’s a flywheel that requires serious manual cranking every rotation, and each rotation is a bet that your fine-tune still matters by the time it ships. And here’s the thing that makes this fundamentally different from Google: Google’s search results just get better with more data. The completion dataset gets materially less valuable with every frontier model release.

Branding is another interesting casualty. Agents give zero shits about your brand. Their job is to fulfill a task, and they’ll use whatever tool does it best, fastest, and cheapest. The entire emotional layer of enterprise procurement – the ‘nobody gets fired for buying X’ premium – evaporates when the decision-maker is algorithmic.

It’s not all doom and gloom, though. Some powers persist, and some powers actually get stronger as AI agents come into the fray.

Scale economies are still a real thing. Anthropic, OpenAI, and Google can operate the most effectively at scale because they’ve got access to way more capital and GPUs than you do. Training a frontier model is…let’s call it non-trivially expensive, but it’s going to cost Joe Schmoe a lot more to train one than it does Anthropic, because of their scale.

Counter-positioning is an arena where strategies can actually get stronger, but only for the challengers. This is the Datadog paradox I mentioned previously: Datadog recognizes that they have to build AI features, or their customer base will churn, but if by building AI features, they kill the need for dashboards, they kill their own product. It opens the door for competitors to accelerate that cycle.

As for cornered resources, the question fundamentally comes down to whether the resource is genuinely cornered. The tricky situation for coding agents with their completions dataset is that it is a genuinely valuable dataset, and in some ways, it’s unique to their business, because it’s their data and they’ve collected it. However, if Claude Code generates a substantially similar dataset for Anthropic, we’re left asking the question: do Cursor or Cognition or Roo Code or Cline own a genuine cornered resource, or does it just have a head start against Anthropic in a race where Anthropic can accumulate the dataset at a much faster clip? This is a really important and complicated question, and I plan to dedicate a lot more space to it.

Lastly, process power is actually pretty darn resilient. Agents can’t erode your internal process from the outside – if anything, they can enhance it. The best AI companies have built organizations that can operate on radically compressed planning cycles, because a single model release can invalidate months of work. That kind of organizational muscle takes years to build, and it’s the one advantage a competitor can’t shortcut. Unfortunately, it’s also really hard to assess from the outside, which makes it tricky if you’re trying to evaluate a company as an equity bet.

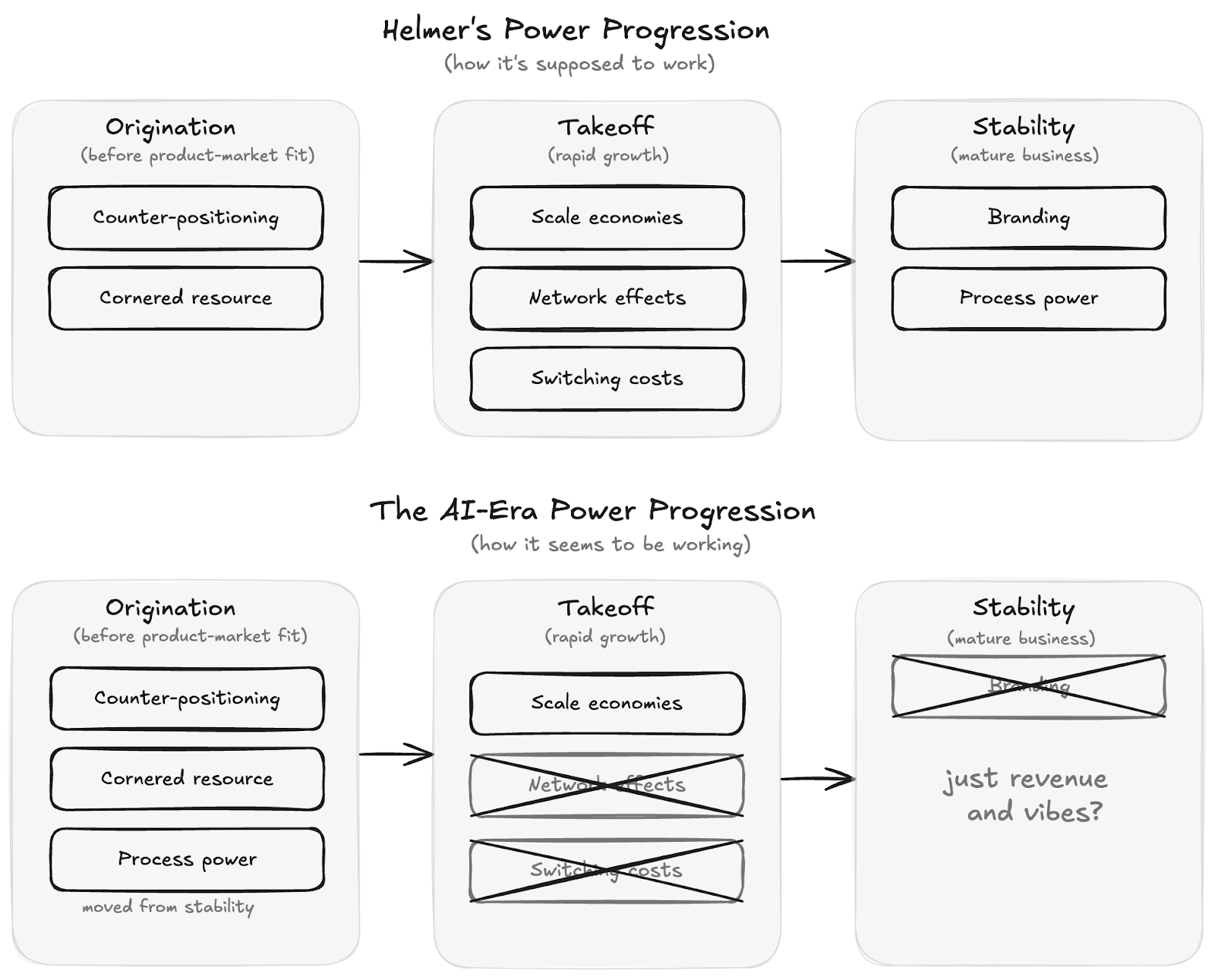

The other big component of Helmer’s theory is the idea of Power Progression, that each power can only be developed at certain points in a company’s maturation cycle. Specifically, there’s a pre-PMF Origination phase where you can develop cornered resources and counter-positioning, an early-PMF Takeoff phase where you can develop scale economies, network effects, and switching costs, and finally a Stability phase where you develop branding and process power.

Here’s what’s strange: Helmer’s Power Progression says you build scale, network effects, and switching costs during takeoff, and branding and process power come later, during stability. AI-native companies have inverted this entirely. The best ones have process power from day one – organizational DNA built for compressed planning cycles and constant pivots. Open-source companies have brand equity from origination. But the takeoff-phase Powers – the ones you’re supposed to be building right now – aren’t forming, because agents are dissolving them as fast as companies can construct them. These companies might arrive at maturity with branding and process power but no scale economies, no network effects, and no switching costs. That’s an unprecedented strategic position, and honestly, I’m not sure anyone knows what it means yet.

So if traditional moats are being dissolved in real-time, what do you actually build to create a lasting business? Stay tuned for my thoughts next week.