Insider trading on prediction markets is turning into a dog-bites-man type of story.

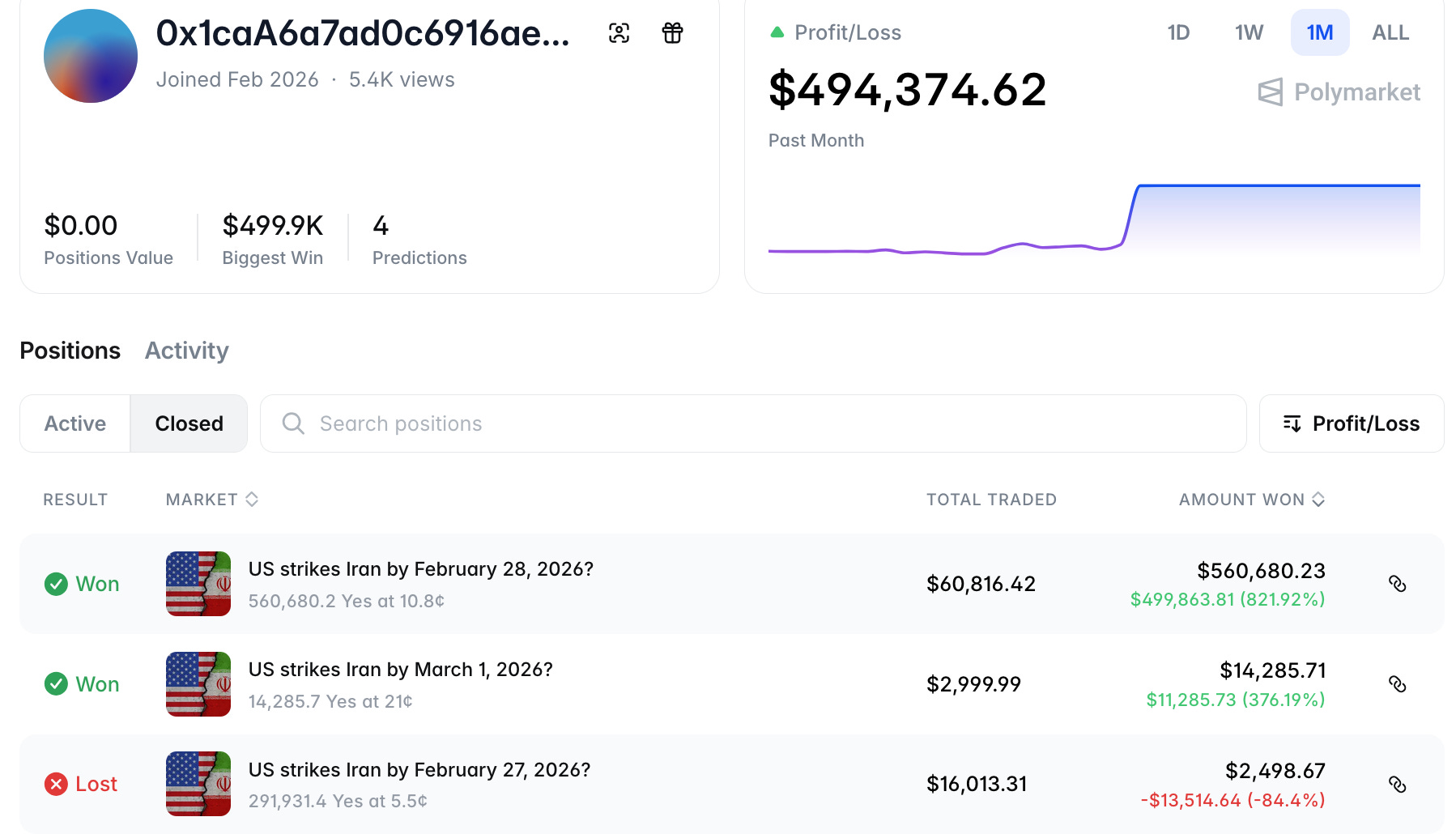

The latest incident involves betting on the precise date of the US strike on Iran. Six wallets were opened shortly before the strikes, bought large numbers of contracts referencing the event, and banked $1.2 million in profits in a matter of hours.

This is just the most recent in a long line of such cases. An anonymous trader made windfall profits back in January with a series of well-timed bets on the removal from office of Nicolás Maduro. Two Israelis were charged last month for trading on classified information ahead of the June 2024 strikes on Iran. And there is compelling evidence of insider trading ahead of earnings announcements by a set of companies that share the same auditor.1

Kalshi has conducted more than 200 investigations into insider trading, with a dozen cases currently active. As a regulated exchange operating in the United States, it is required to verify the identities of all traders. This know-you-customer (KYC) requirement is primarily designed to address money laundering and terrorism financing, but also facilitates the detection of insider trading and other violations of securities laws.

The preferred exchange for insider trading is therefore Polymarket, where accounts are funded and contracts settled using the USDC stablecoin. This results an unusual mix of secrecy and transparency—all transactions are visible on the blockchain but real world identities are concealed even from the exchange. Insider trading under these conditions becomes easier to notice but harder to prevent.2

Aside from the protection of anonymity, Polymarket offers traders the possibility of betting directly on geopolitical violence in ways that Kalshi does not. Both exchanges listed contacts on “Khamenei out as Supreme Leader” but these turned out to reference very different events. The Polymarket contract resolved to “Yes” while the corresponding Kalshi contract resolved to the price at last trade prior to his death.3

Facing intense backlash from traders, the Kalshi CEO argued that “as a federally regulated prediction market, we are required and feel it is important not to enable direct profiting from war, assassination, terrorism, or other violent outcomes.” However, as Sean Guillory and Dan Zimmermann have pointed out:

Markets that resolve on whether someone stays in power, speaks publicly, shows up somewhere, or holds a certain job carry implicit incentives connected to their continued existence. Nearly every such market dealing with control, decision, or public appearance is technically an assassination market… Prediction markets and smart contracts create the possibility that those who carry out political violence could also directly profit from it, anonymously and without intermediaries. That marks a profound shift in incentive structures.

This problem can’t be solved by simply adopting the principle of resolution at last trade. Someone with inside information (or with the capacity to directly influence the outcome) can trade in ways that sharply raise the price prior to event realization. Profits may not be as high as they would be under binary resolution, but they could still be substantial.

These are the kinds of issues regulators ought to be grappling with. They show few signs of doing so under the current administration. But this highly permissive stance will not last indefinitely, and prediction market platforms planning for a long term presence may want to consider the range of contracts and approaches to resolution that would survive more assertive oversight and more restrictive legislation.