Media Coverage

Image: Unsplash/Negley Stockman

11-MINUTE READ

TL;DR

Music copyright was valued at $47.2bn in 2024, nearly doubling in a decade

Publishers are growing faster (~6%) than labels (~5%) — for now

Macroeconomics and music economics are diverging

Glocalisation is having distinct effects on small, medium and large markets

Image: Unsplash/Vitaly Gariev

Purpose and Progress

What is music copyright worth? Whether you’re a singer or songwriter, a label or a publisher, a streaming platform or a policy maker — the answer matters. You need to be able to see yourself within the big picture. A decade into this arduous annual calculation, this ‘need’ provides as strong a motivation as it has from the beginning.

We are grateful for the help of all three major trade bodies: IFPI, CISAC and International Confederation of Music Publishers (ICMP[1]). Thanks also to MIDIA, who surveyed over 250 publishers[2]. Finally, the generous cooperation of rights holders and streamers enabled significant methodological advances to help bring the true value closer than ever before.

1 ICMP recently completed their own analysis across their top sixteen markets. Whilst their calculations are not global, they intend to get there, which will surely become a crucial component of this exercise.

2 Repeat readers will note MIDIA is a new data source, having replaced Music & Copyright for the calculation’s publisher data.

Image: Unsplash/Neza Dolmo

The Big Numbers

The global value of music copyright reached $47.2bn in 2024.

That's up just $2.3bn (5.2%) on the prior year; growth is slowing largely because this is the first year where the pandemic effects have vanished.

Recall how Covid rocked our industry. Streaming revenues for labels surged but public performance income for CMOs sank. After years of recovery, we’re now settling back into a steadier state.

Stacking the puzzle pieces shows a mixed bag of growth stats. Labels grew year-on-year by 5% to $29bn, songwriter CMOs grew by 8% to $13.6bn and publisher direct revenues (i.e. with no CMO involved) fell slightly, down 1% to $4.6bn.

Image: Unsplash/Mick Haupt

Ten Years Gone

It’s not just this report that’s celebrating a ten-year anniversary. Music Business Worldwide launched a decade ago, and was first to announce the big number: $25 billion: The best number to happen to the global music business in a very long time.

Literally ten years to the day, we can quickly take stock of how far the music industry has come. Taking a simple waterfall snapshot,[3] music copyright value has nearly doubled in the past decade.

Notable is how the three ‘pieces of the puzzle’ have changed over the decade. CMOs have grown by 50%, labels have doubled, and publishers’ direct revenues have swelled by 112%. ICMP has long championed the ability of publishers to licence their rights directly, circumventing the constraints of the collective, and this performance supports their argument.

3 Ignoring caveats like exchange rates and methodologies.

Image: Adobe Stock/VladyslavShcherbakov

Fair Division?

What makes this work particularly useful, especially as the data have grown more precise, is how it illuminates the causes and consequences of fair division — that is, the split between record labels and artists on one side, and songwriters, publishers, and their CMOs on the other.

The world of copyright isn’t 50:50 and this simple rule explains why. If you're selling music to consumers (e.g. subscription services) then labels do better than publishers, whereas if you're licensing to businesses (e.g. TV, radio, retail, hospitality) then publishers tend to do better than labels.

Back in 2014, labels’ business-to-consumer (B2C) revenues were struggling as streaming had yet to take off and CDs and downloads were withering on the vine, while publishers and CMOs continued to report record collections thanks to inflation being embedded in their business-to-business (B2B) licensing formulas. As a result, the global value of copyright was split near 50:50.

With the rise of streaming, the scales have further tipped toward B2C and a 62:38 split in favour of labels and artists.

If the rule is as simple as ‘B2C favours labels, B2B favors publishers’, then one increasingly pertinent question is which lane would AI music fall into? There have been numerous reports of rights holders striking ‘landmark’ deals where each side will receive approximately half of royalties generated from the AI platform. Revisiting this exercise in future years will help tell us how this new value of music copyright gets divided up.

Image: Unsplash/Natalie Runnerstrom

Rich North, Poor South Revisited

Last year, we analysed the discrepancy between the explosive growth in streaming volume and more modest growth in label income. This year we revisit that calculation with the richer markets of Japan, South Korea, Singapore and Hong Kong separated from Asia, offering more precise takeaways.

Recall how we learned that, back in 2023, the poorer south was driving the double-digit volume growth whereas the rich north ‘paid our bills’.

That story continued into 2024, as the rich four of Europe, North America, Australia and the cluster of Japan, Korea, Hong Kong and Singapore are responsible for almost 60% of the reported streaming volumes but, with their higher per-stream payments, nearly 90% of the value. If the ‘rich four’ slow down, they’ll bring the global figure down with it.

The key point? Robust streaming volume growth does not necessarily mean the same for revenue. And that may not change anytime soon.

Image: Unsplash/Feliphe Schiarolli

Convergence or Divergence?

A central tenet of capitalism is that poor countries can catch up with rich ones, thanks to a combination of cost-competitiveness and comparative advantage. (At least that’s what they teach you at school.)

In this regard, this year’s data show two examples of music economics diverging from macroeconomics — with important ramifications for rights holders, users, and especially investors.

First, let’s look at India and Japan. On the macro side, India has officially overtaken Japan in GDP terms.

On the music side, however, rather than convergence, a different story is playing out. Calculating each country's music revenues as a percentage of the global total shows Japan’s and India’s shares have both dipped, to 8.5% and 1.2%, respectively. But unlike the macro story, there are few signs of convergence. To wit, Japan is being touted as a ‘high headroom market,’ as it was a late-adopter of streaming and has lots of room to grow. India, for its part, has been sputtering with its dependency on ad-funded video. Point being, even if on the macro level India has caught up to Japan, it’s hard to envisage a similar story in music.

Vinit Thakkar of Sony Music India

Every good research paper considers alternative views, and so to counter this pessimistic outlook, Vinit Thakkar of Sony Music India has spotlighted the country’s recent history of “irreversible non-linear change.” Back in 2016, the argument goes, the leap from 2g to 4g was truly transformative and in the decade since, India has achieved mass adoption of digital wallets. Like a volcano, the next tipping point for music subscription has been bubbling under the surface, according to Thakkar, and could explode before the decade is out.

Now let’s turn to the second development that underscores how music doesn’t always follow macro: the USA.

Spotify launched in the US in 2011, and as streaming soon took off around the world, a rational economist would have predicted that absolute revenue in the US would increase while relative share would go down. Not so.

Back in 2011, the US made up a quarter of a $15bn business. Today it's 38% of a $30bn business — that’s a 40% bigger share of an 80% bigger pie. Back then, no rational economist would have predicted this outcome and there’s a reason why. Music economics is diverging from macroeconomics — and that realisation may force analysts-and-investors alike to reset their ‘up and to the right’ global forecasts and projections.

Back in 2011, the US made up a quarter of a $15bn business. Today it's 38% of a $30bn business — that’s a 40% bigger share of an 80% bigger pie.

Image: Adobe Stock/Andrey Oleshko

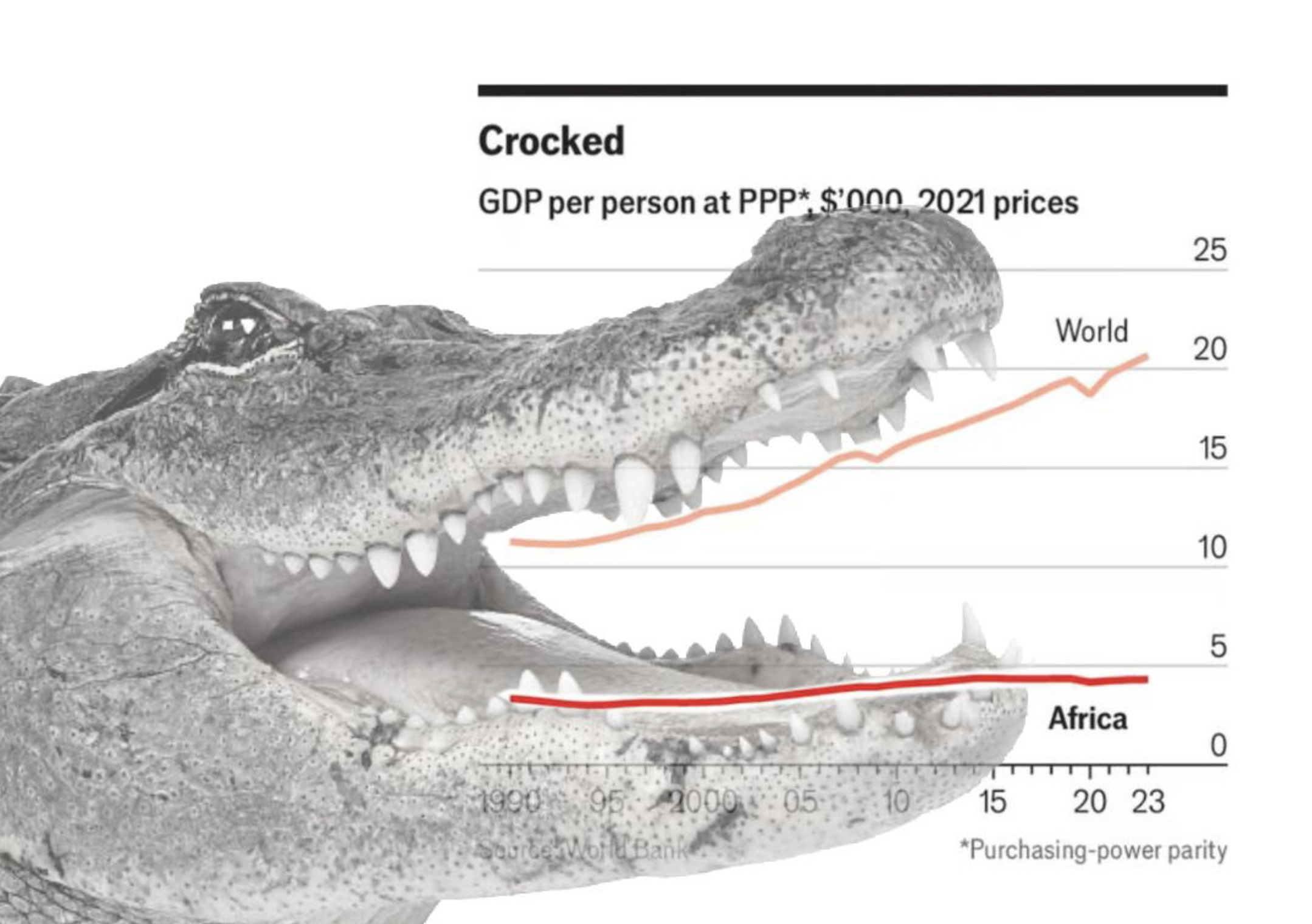

When the crocodile smiles

One way macroeconomics and music economics do seem to be operating in parallel is the emergence of the "Crocodile smile." The term was coined by The Economist to illustrate the growing economic gap between Africa and the rest of the world that resembles the jaws of a yawning crocodile. While the rest of the world grows, Africa remains flat.

In music, streaming services have been in emerging markets for the best part of a decade now. This provides ample data to understand their absolute and relative performance over time.

Three markets merit close attention due to their relatively early adoption of streaming alongside a strong macroeconomic performance. Mexico and Poland saw Spotify launch in 2014; Indonesia in 2016. All three have seen significant growth in their GDP per capita over the past decade: Poland up 80%, Mexico 47%, and Indonesia 30%.

Does that macroeconomic success translate into music success?

To find out, alongside an index of their GDP per capita, let’s plot an index of each country’s monthly average revenue per user (ARPU), which labels receive from premium streaming services. For the technocrats reading this, we exclude free tier, trials, and third parties to avoid volatility from ad markets and ensure the trends reflect the price consumers pay.

Now we see the yawning crocodile as Poland’s ARPU rose only 5%, while Mexico has remained flat and Indonesia trended down 13%.

Capitalism purports a rising tide lifts all boats. The crocodile smile challenges this theory and illustrates that some boats rise faster than others — which is what we’re seeing in music as well. Although GDP per capita is growing, meaning people are getting wealthier, that wealth-effect isn’t translating into recorded music revenues. Sure Poland, Indonesia, and Mexico have all reported consistent recorded music revenue growth since 2017, but when compared to their stellar macroeconomic performance, one could argue they’re not growing fast enough.

That argument gathers momentum when you consider this analysis does not adjust for inflation. In real terms (stripping inflation out), GDP per capita remains robust for Poland and Indonesia, less so for Mexico. Perhaps the lack of price increases (or overdependence on family plans) despite their increasing wealth is a causal factor of the crocodile smile.

Image: Unsplash/Abstral Official

And finally, Glocalisation

If the crocodile smile offers a timely reminder that theory doesn’t necessarily translate into practice, the same holds with Glocalisation, which upends conventional wisdom that the world is flat.

Glocalisation has unwittingly become my middle name. An unplanned flippant remark on the BBC One Show in the spring of 2023 (aimed at helping launch my book Pivot) now flows through all media verticals from the boardroom to the conference halls. The gist is the surprising success of local artists singing in their local language. This phenomenon continues to percolate, and as it evolves we’re still defining it in real time. What seems clear enough is that glocalisation produces winners (e.g. non-English-speaking markets with a strong national identity), losers (e.g. English-speaking markets that are not American), and confusers (e.g. Spanish charts are dominated by Spanish language but not necessarily Spanish artists).

Glocalisation also alters the balance of music imports and exports. The latest net-export figures show that Sweden, with its well documented success in writing for the English language and K-Pop machine, is now close to overtaking the US, but more noticeable is Korea — which achieved a positive trade balance only last year and is now very close to overtaking the UK. Of course, ratios like export-import are a relative figure with (at least) two sides to their story, but for Koreans it's clear, and welcome, that imports are flat and exports are exploding.

Music trade may not directly impact the global value of copyright — you pay $12 per month regardless what you stream — but it does indirectly impact how that value is allocated. Of all the streaming income generated by consumers inside a country, how much stays (and is reinvested) in that country, and how much is repatriated overseas? There is also a potential induced effect that glocalisation lowers trade between countries and within international record labels as the domestic dominance of charts reduces the incentives to break artists from beyond the label’s borders.

One overlooked factor in assessing the effects of glocalisation is country size. To illustrate this, we’ll conclude by uncovering fascinating trends from relatively small Denmark, medium-sized Korea, and large (or extra large) Brazil.

Denmark: Linguistic Protectionism

The Danish language is spoken by six million people. Neither Swedes nor Norwegians understand it. Yet 16 of the top 20 albums (and 15 of the top 20 songs) in Denmark last year were by Danish artists performing (where lyrics were present) in Danish.

Linguistic protectionism may explain what is going on. Danish artists know that if they all perform in Danish, they'll keep the attention of their listeners satisfied with local fare and fend off the blockbuster English-language artists from afar. We see this on the charts as much as in the festival season, which are predominantly Danish-language.

Gorm Arildsen, CEO at KODA

Gorm Arildsen, CEO at KODA, arguably the world's best run collective management organisation, doesn’t see anything cynical here:

“What looks like linguistic protectionism is really a natural progression. We’re in the age of hyper-personalisation, and as the world becomes harder to read, we gravitate toward shared cultural moments to help ground us. In Denmark that collective impulse has lifted local music to heights even global superstars can’t displace. It’s a breeding ground for creative confidence.”

Image: Unsplash/Joel Muniz

Taking the K out of K-Pop

K-Pop is massive in Korea, but with limited domestic scale and a shrinking population, export isn’t just a strategy—it’s existential. Japan’s trajectory serves as a powerful reminder of what happens when domestic success becomes the ceiling rather than the springboard. K-Pop seems intent on avoiding this fate.

Unsurprisingly, the genre of K-Pop has overtaken pop in Korea, whereas it's half the size of pop in Japan — yet its streams are now growing twice as fast. Japan is Korea’s biggest export market, with 14 of the top 100 artists in Japan this year tagged as K-Pop. Soon, with BTS’s imminent return, we could see a tipping point where K-Pop overtakes pop in Japan.

Should this happen, it raises more questions than answers — especially when it comes to syntax of the genre “K-Pop”. For example, do we need a separate genre-tag for J-Pop to differentiate Japanese pop, and what if J-Pop is actually K-Pop? Muddying these genre matters further, Japanese executives even refer to this phenomenon as J-K Pop. And let’s not forget the consumer who may see it simply as pop music, because it is so popular.

JH Kah 가종현, CEO of HYBE Latin America

“Tower records still thrive in Japan, that should tell you a lot! Indeed, an entire floor of their flagship Tokyo store is dedicated to K-Pop. However, Japanese label culture suffered from decades of inertia whereas Koreans are inherently more hungry — our mantra is survive and thrive. That’s why you are now seeing Japanese labels hiring more Korean executives, and Korean labels going directly into Japan. The lines are getting blurred both on stage and backstage.”

Image: Unsplash/Abstral Official

Betting Big on Brazil Pays Global Returns

From the small Danes who have gone Danish, to the mid-sized Koreans who are exporting to Japan, we conclude by going large, or extra large, to Brazil — a top ten music market with a population of 213 million people and a land mass slightly smaller than Europe.

The YouTube top 100 artist chart for Brazil provides the litmus test for glocalisation: simply scroll from top to bottom and you will not see any international artists — no Spanish, nor English language, not even K-Pop Demon Hunters. It’s all Portuguese.

For a market that’s turned its back on the English and Spanish language, one could be mistaken for seeing Brazil as isolated and self-serving, forgoing global ambitions. But due to its sheer size, that’s no longer the case.

Cue up Little Love by MC Cabelinho, Quem Tiver Sofrendo Se Vira! by Evoney Fernandes, or the Ao Vivo no Buzu album by Natanzinho Lima. These Brazilian artists are reaching the top of global charts thanks to (only) local demand.

Roni Maltz Bin, CEO of Grupo Sua Música

Roni Maltz Bin, CEO of Grupo Sua Música, sheds light on the staggering local numbers that got these Brazilian artists onto global charts:

“Little Love by MC Cabelinho peaked on the Brazilian charts and reached #2 on the Top Global Debut Album Charts — even though 99.5% of the album’s streams came from inside Brazil. Ditto Evoney Fernandes, who peaked at #7 despite 97.4% of his streams coming from Brazil. Natanzinho Lima debuted in the same week as Bad Bunny and still reached #4 on the Spotify Global chart with 98.3% of all streams coming from Brazil. This shows the strength of the Brazilian market — it can break artists on the global charts even when their artists are only being streamed locally.”

The glocalisation of the value of copyright reminds us that the big figure that is calculated each year is being allocated across markets differently. These three winners of glocalisation remind us that more of that value is staying within their domestic markets, as opposed to being repatriated back to international headquarters. The free market of streaming has achieved what the regulated market of broadcast failed: domestic prominence.

Image: Adobe Stock/nicholasjermy

Headwinds and Tailwinds

Where does the global value of music copyright go from here?

We instinctively know it will soon pass $50bn but should we be pumping our hopes up that it will double again in the next decade (or sooner) to a twelve figure number? Or should we buckle up for turbulence as subscription saturation hits the rich and, as we’ve seen, increasingly influential, north?

One headwind that needs no introduction is the rise of AI music. The question on everyone's lips: will this be complementary or cannibalistic to the existing $47.2bn business? This is where we can revisit our concept of ‘fair division’ and ask if the commercial prospects of recent deals with Suno and Udio might add value to B2C revenues, but wipe out value from the B2B business due to the displacement of production music libraries. If so, the impact of AI may be asymmetric.

Another headwind facing the music industry involves what economists call time-lags. The prior global value of copyright reports showed how streaming income for labels was exploding with more moderate growth for publishers. This year, we’re seeing CMOs and publishers (combined) grow faster than record labels. Perhaps this is the boom labels saw yesterday transferring to publishers today — meaning the slowdown labels show today will emerge in publisher collections tomorrow.

The most obvious tailwind, meanwhile, risks of repetition, but remains salient as ever: global needs to mean global. Of the 196 flags flying outside the United Nations building in New York, our industry yearbooks featured here capture barely a quarter of them. Ceteris paribus, the more we measure, the more value we capture.

Consider China. With $1.6bn in recorded music revenues, it’s now ranked fifth in size by the IFPI and will soon overtake both Germany and the UK. But that’s not a complete picture of copyright. Industry experts estimate a further 15% should be paid to Chinese publishers — and this isn’t being captured in any of the yearbooks. That's almost a quarter of a billion dollars currently not being calculated.

How many more known-unknown examples like this are there? And if we did know, and measured these markets accordingly, how much bigger might be the global value of music copyright? This is why global needs to mean global when we measure music copyright.

Acknowledgements

A huge debt of thanks to Chris Carey (FFWD) for tag-teaming on this calculation for ten consecutive years and Ralph Simon (Mobilium) for originally motivating this calculation. In addition, thanks to Gadi Oron and Sylvain Piat (CISAC); John Blewett and Lauri Rechardt (IFPI); Mitch Glazier and Matt Bass (RIAA); David Israelite and Justin Uehlein (NMPA); Bill Gorjance (peermusic); Mark Mulligan (MIDIA); Jackie Alway and John Phelan (ICMP); Jaime Marconette, Scott Ryan, Adrian Sarosi, and Mary Nwangwu (Luminate); Frederik Juul Jensen, Gorm Arildsen, Martin Folmann, and Jakob Hüttel (KODA); Simon Gozzi (STIM); Thomas Breslin (ReRight Music); Liz Martens (HSBC Economics); Vinit Thakkar (Sony Music India); Roni Maltz Bin (Grupo Sua Música); JH Kah (HYBE Latin America); Bernie Cho (President, DFSB Kollective); Jeongbeom Kim (Kreatorsnetwork); Tom Frederikse (Clintons); and many music industry executives from streaming services, labels, publishers, and CMOs who made this calculation possible. Special thanks to the incredible copy-editing wordsmith Sam Blake for making this calculation comprehensible and Alice Clarke for design and infographics.

--

Will Page is the author of the critically acclaimed book Tarzan Economics, which has been translated into five languages and published in paperback under the title Pivot. As the former Chief Economist of Spotify and PRS for Music, Will pioneered Rockonomics and shined a spotlight on Glocalisation, showing how and why local artists singing in their mother tongues are topping the charts on global streaming platforms. At Spotify, Will launched his ongoing and widely anticipated annual report on the global value of music copyright, and at PRS he saved BBC 6Music. A passionate communicator, he is a regular contributor to BBC, Financial Times, and The Economist. Will also serves as a fellow at the London School of Economics, Edinburgh Futures Institute, and the Royal Society of the Arts.