You’ve definitely heard it: it’s the dusk of SaaS. It’s as if we’ve got evidence coming from every direction. Here’s a random set of conversations I had last week.

A chat with a fellow leader from a software development company about how they get less and less work, which used to be mainly all sorts of SaaS startups.

A story shared by a former developer-turned-product-consultant about how he’s now dropping his productivity tools (Linear, Harvest, Zoom notetaking, etc.) as he’s generating his own tailored productivity tool with Claude Code.

Discussion about Duolingo, whose valuation, despite showing healthy financials, nosedived.

A conversation with a friend who has an idea to disrupt language learning products with (obviously) a largely vibe-coded tool. Curiously enough, that wasn’t my first friend who set out to pursue the idea over the last year.

I didn’t even reach out to have those exchanges. They came to me organically. In just one week. One might look at the list and suggest that the world is giving us hints.

It’s easy to build a consistent picture of a new reality. One where it’s easy to generate yourself a digital product. Either for own use—and drop all the subscriptions as a result—or to commercially challenge incumbents. One way or another, old-school SaaS would be doomed. Sure, it won’t go down with one quick hit, but a thousand cuts will eventually do the job.

Or will they?

Let’s look at a few notable examples of what’s been dubbed SaaSpocalypse—the culling of established SaaS businesses. One of the most vivid examples is Duolingo.

A remarkable 75% slide down in 12 months. Color me impressed. All while reporting most active users ever, best revenues ever, best profits ever, and becoming a poster kid for AI adoption (for better or worse). It’s as if they crossed all the t’s, dotted all the i’s, and they still got brutally punished by the markets. Interesting, isn’t it?

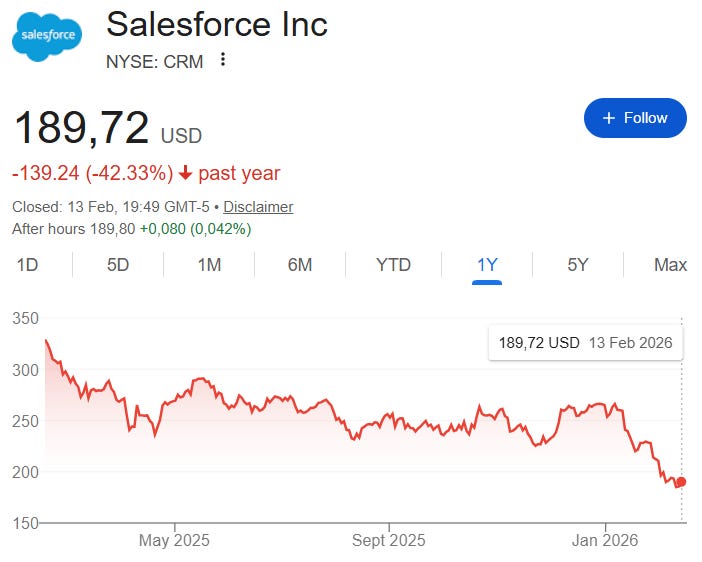

While Doulingo is, indeed, a vivid example, they’re hardly alone. Salesforce has just had a record year, too. Sure, the dynamic of growth is slowing down, but what do you expect of such a behemoth? The share price, though? Down by 40%.

Intuit is in the exact same spot. Everything’s up. Save for the stock price, that is. The valuation went down by 30%.

We could go on and on. The question worth asking: Why is it so bad if it’s so good?

Obviously, the future projections SaaS companies make may be somewhat more conservative these days. But would that justify such a sell-off? My friend might have ditched Notion, Harvest, and Zoom subscriptions, but how many people would need to follow suit for the product companies to notice? Klarna might have been a big Salesforce client to drop, but we don’t hear it becoming a trend.

For now, it’s still anecdotal evidence.

Ultimately, if such stories scaled, we’d see the impact in the numbers: active users, revenues, profits, etc. And we don’t. Duolingo isn’t worried about two of my friends trying to make a shot at its business. Investors are even less so.

Even if we could generate a product with AI (we can’t, and it has nothing to do with how good the latest Claude Code is), the sheer scale of operations would give plenty of warning before these established business models collapse.

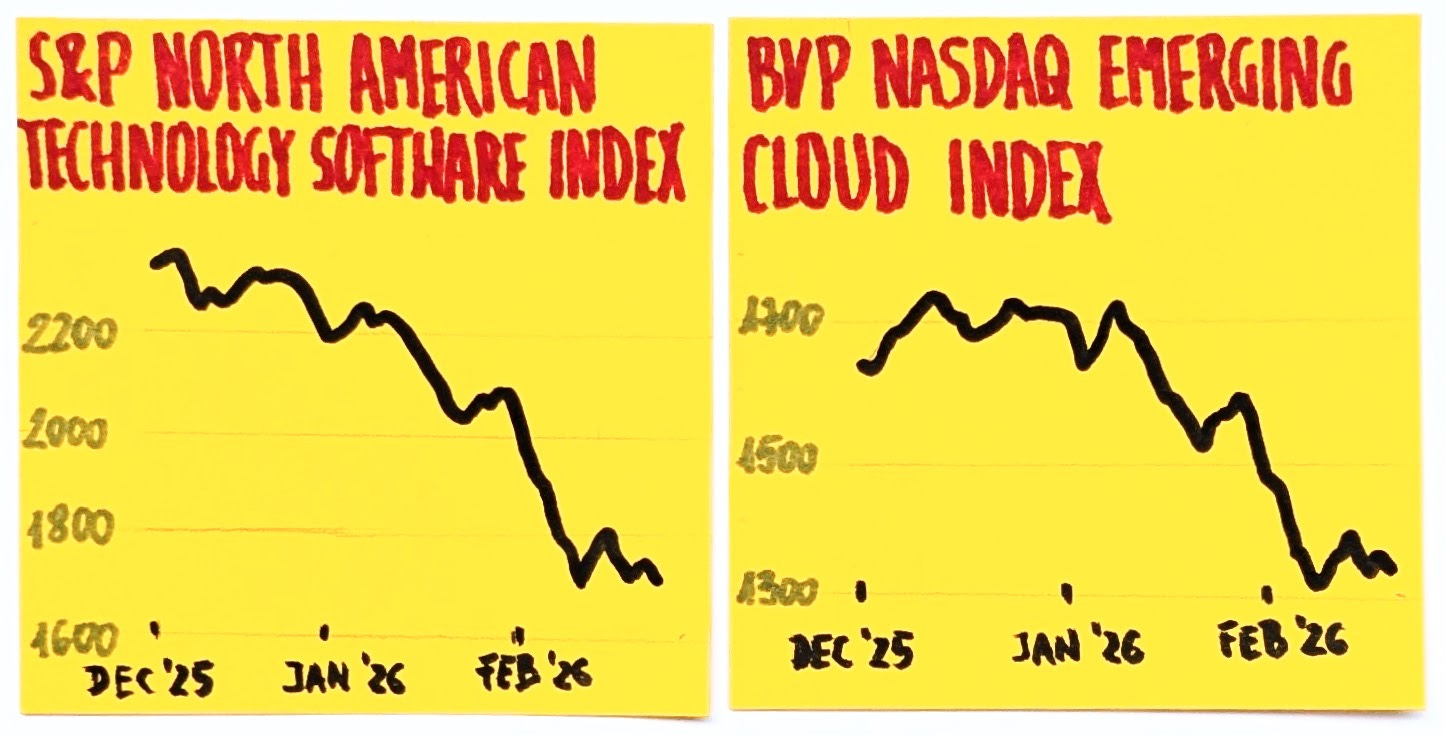

The landscape we see is not that different from what we saw a year ago, but suddenly all we see is gloom and doom.

So what the hell is going on?

The answer may be simpler (and more boring) than we expect. SaaS companies were simply overpriced in the first place. Let’s take all those Duolingos, Salesforces, Intuits, et al and run the Starbucks Test against them.

Check the revenues and profits of an established company for the past few years.

Assume it’s Starbucks (or any other brick-and-mortar business, really).

Figure out the valuation of the company.

We look at the same numbers but draw different conclusions altogether. Established, healthy brick-and-mortar businesses might have their valuations in the range of 25x-30x their net profit. If we looked at, say, Walmart, it would be the same. That is, before investors started treating Walmart as an ad company and pumped its share price.

It makes sense. If you were to buy a private business, waiting 25 years for a return on investment is already too long. Thus, we arrive at such valuations on the premise that there’s a good chance the business will grow and return on investment will arrive early. In other words, these already assume future growth.

So, how would our SaaS companies fare against the Starbucks Test?

Save for the last year, Salesforce hovered between break-even and $4B in net profit over the past half-decade. Then it jumped to ~$6B net profit last year. The Starbucks Test would then suggest a valuation around $120B if we considered a broader time window. More if we believe in above-average growth potential (treating Starbucks’ growth as a benchmark).

If we took only the last year as the most meaningful reference point, then $180B might make more sense. Surprise, surprise! That’s where Salesforce’s valuation is now.

Intuit then. Net profits of $4B would put us at a $120B valuation tops. Wanna guess where the discounted stock price lands Intuit now? Yup, just slightly below that mark.

Duolingo? Admittedly, it’s a less established business than Salesforce or Intuit, and it still seems to be on a more aggressive growth trajectory. Still, with their actual net income of ~$160M, the Starbucks Test would suggest a valuation of around $5B. Yes, that’s precisely where it went after the year-long ride not-exactly-in-the-most-desirable-direction.

Can you see a pattern?

One way of framing these stories is that the market stopped treating SaaS as a privileged player. It’s not an apocalypse. It’s just the end of privilege.

Admittedly, losing a privilege may feel like an apocalypse to the formerly privileged. But that’s another discussion.

The end of SaaS is not nigh. If anything, the markets found a new darling (AI labs), and the old one is not nearly as fashionable anymore. As a result, the part of valuations based on the promise of future hype disappeared.

It’s not a default assumption that a SaaS product will be growing nearly indefinitely. Such a perception must be earned. For an old-school SaaS product, that is. If you’re building the next-generation-AI-whatever, you can still count on the implied future growth bonus. Hell, if you do that and co-found with some prominent experts, you can cash in on 10x such a bonus.

For everyone else, we started treating digital product businesses as we would any other endeavor. We care more about the numbers we can see, which describe the actual current realities, rather than future projections, which are—let’s admit it—mostly smoke and mirrors.

Startup growth projections were notoriously rosy and as notoriously unreliable (and it’s largely VC’s own doing, let me add). The investors chose to “believe” in super-optimistic projections only because occasionally a startup would go supernova and erase the losses from everyone else who vastly underdelivered.

It was a shaky structure from the very beginning. At the risk of pissing some people off, I welcome the change. SaaS valuations were absurd. And yes, that makes AI labs’ valuation an order of magnitude more absurd in comparison. I, for one, prefer a reality with more modest and healthier assessments.

The subscription-based payment model is as viable as ever. In fact, many companies hit hard by the SaaSpocalypse have just reported strong financials.

As consumers, we grow more and more accustomed to paying for services. Just check how many subscriptions you had two decades ago, a decade ago, and now. I bet the trend is as clear as day.

We’ll never grow short of “our needs we want addressed,” so there will always be ideas for new products and services. Yes, the options we have to address these needs evolve (I’m looking at you, Anthropic). Thus, the products and services we create will evolve too. We can count on human ingenuity and entrepreneurship to see those needs turned into solutions. And we’ll still be paying for them “as a service.”

And if you need a final argument, the rockstars of the startup world—the AI labs—are selling their stuff under the very same subscription-based model. Sure, they do it in a hybrid way (subscription plus usage), but it’s only because they can’t afford a pure SaaS model.

The solutions change. Business model? Not that much.

There is another side to this discussion, focused on the vision of everyone being able to generate their own custom products. This post is already long enough, however. Let me cover the “everyone will be a product developer, so no one will need SaaS” issue in the next article.