The most valuable companies right now aren’t building software for end users. They’re building the ground upon which other software stands. Consider that Stripe, Twilio, and Plaid together process a material fraction of the world’s digital economy, and most people couldn’t tell you what any of them actually sell because they don’t sell to you, they sell to the company that sold to you. Most mistakenly call this B2E or B2B but that fails to distinguish SaaS providing solutions that a business employs from that which provides solutions to what a business deploys; welcome to Infrastructure as a Service.

With most, Infrastructure as a Service gets lumped in with “cloud computing” by people who stopped thinking about it around 2012. Ask most founders what IaaS means and they’ll say AWS: servers, storage, and compute you don’t want to own. True, but that’s one slice of what’s actually become a $14 trillion layer of the internet. By 2027, APIs are projected to contribute $14.2 trillion to the global economy, more than the GDP of the UK, Japan, France, and Australia combined. As I explain what this is, appreciate that AWS, Azure, and Google Cloud also sell SaaS products sitting on top of their own infrastructure. Azure sells Office 365 and Google Cloud sells Workspace. The distinction between infrastructure and software isn’t about which company you’re buying from; it’s about what layer of the stack you’re buying. AWS S3 is infrastructure: raw capability you build on top of. Google Sheets is SaaS: a finished product you use directly.

One sells to builders. The other sells to users.

That structural difference applies as much to Stripe, Twilio, and Plaid as it does to Amazon’s server farms. These companies don’t sell to end users; they sell to the companies building products for end users. That’s what makes them infrastructure rather than software, and it’s what’s become a $14 trillion layer of the internet that most founders are either standing on without realizing it or accidentally trying to rebuild from scratch.

SaaS has a feature ceiling that every mature product company eventually hits. A Platform is a misrepresentation because a platform better characterizes software upon which a business builds a service. Regardless, what matters is noting that you can keep shipping roadmap items, but at some point, the product needs capabilities a team has no business building. A payroll feature in your vertical HR product means you need to understand tax withholding logic across 50 states, ACH network requirements, and banking partnerships. A payment feature means PCI compliance, fraud modeling, cross-border FX logic, and card scheme relationships with Visa and Mastercard. An identity verification layer means KYC (Know Your Customer) compliance, document verification models, and access to fraud consortium data. None of those are features, they’re infrastructure. Treating them like features is how teams end up two years deep into building something they should have embedded.

We all can appreciate the word infrastructure in the context of the real world; say, a city. And I’m intrigued by a missed opportunity by investors, a misunderstanding by startup development organizations, and an oversight by founders, in appreciating the difference between being SaaS and being IaaS (Infrastructure). A city invests in roads, water systems, and power grids not because politicians are civil engineers, but because we know it needs that infrastructure to function. SaaS in this analogy is a car, city bus, or Waymo; all of which is sold to customers but none of which works without the infrastructure as a service. What cities do not do is hire in-house teams to build and maintain the specialized systems that run that infrastructure; they bring in companies that have devoted their entire existence to that specific problem.

The city sets the conditions; specialists deliver the capability.

I fell upon this in my work with startup ecosystems; in my study of why accelerators and incubators are failing more often than they should. Startup incubators (the programs cities, universities, and economic development organizations build to support early-stage companies) should work the same way, and almost none of them do. Their mandate is real: give founders access to mentors across the world, connect them to investors, help them identify partners, manage their pitch decks, deliver a real curriculum, and run deal rooms that give investors a clean look at the companies coming through. That is a serious, operationally complex job.

Most incubators handle it by stitching together a video delivery tool, a community app, a shared Google Drive folder passing as a deal room, and a spreadsheet of mentor contacts no one updates. The program director becomes a part-time IT administrator while investor introductions happen over emails no one can find six months later.

Ironically, an incubator’s job is to teach founders to stop building things they don’t need to build. And then those same incubators spend their operating budget on consumer SaaS tools that weren’t built for the job. A video delivery tool is not startup program infrastructure; it’s a commodity. A Slack group is not a mentor network; it’s a chat room with a logo. What a startup incubator actually needs is civic infrastructure, purpose-built and comprehensive enough that a community can deliver on what it promises to founders. That means matchable global mentor networks, investor relationship management, partner identification, pitch deck versioning with structured feedback, tracked curriculum delivery, and deal room management that gives investors something credible to look at. Incubators that actually develop companies understand that the product is their program. That program runs on infrastructure, not willpower.

The incubator that builds its own community app instead of embedding infrastructure is making the same mistake as the SaaS company that builds its own payments stack instead of using Stripe. It’s the same as a city selling cars, building city busses, and paving roads.

Scale and domain are different; the error is identical. Building a feature, buying a tool, and embedding infrastructure are three different decisions. Getting them mixed up burns years of engineering time, creates real regulatory risk, and leaves you with something that can’t compete with companies whose entire existence is the capability you half-built.

Helpful perspective? Share this

The textbook definition from Salesforce’s IaaS overview is accurate as far as it goes; Infrastructure as a Service provides essential computing resources, servers, storage, and networking, over the internet, allowing businesses to use these resources without buying or maintaining physical equipment. The concept has expanded well beyond that.

When Stripe describes itself, it doesn’t say “payment processor.” It calls itself financial infrastructure for the internet. Twilio frames what it builds as “an infrastructure layer for every step of the customer journey.” Plaid calls itself a financial data network, not a fintech app. These aren’t SaaS products in the traditional sense, software you subscribe to and use directly. They’re Infrastructure as a Service: capabilities that other companies build products on top of, in the same way that roads aren’t destinations but make every destination reachable. Gartner projects that by 2026 over $3 trillion in global GDP will be enabled by API-based transactions, and most of that runs through companies most people have never heard of because they live in the infrastructure layer, not the application layer above it.

We can run the same logic through workforce technology; somewhere increasingly important as we discuss jobs and the future. For example, Human Capital Management platforms and Applicant Tracking Systems record events: a hire logged, an offer extended, a performance review filed, a separation processed. What they cannot see (and were never designed to see), is behavioral signal between such events. The patterns that predict whether a new hire will stay 90 days or three years. The engagement decay of a startup team or the company-wide sentiment shift that produces a wave of departures before a single notice is handed in. These aren’t features the HR Tech that employers use should build; predictive analytics is a completely different data model, a different ML training pipeline, and a dataset that builds up over time across employers and industries in ways no single platform accumulates on its own. MustardHub is the infrastructure layer here, embedding inside existing workforce systems and generating the behavioral signal that transactional platforms were never built to produce, so that any HCM platform, scheduling tool, or vertical SaaS product serving franchise staffing or restaurant operations or construction crews can surface attrition risk; workforce intelligence under its own brand, without building a behavioral data science team from scratch.

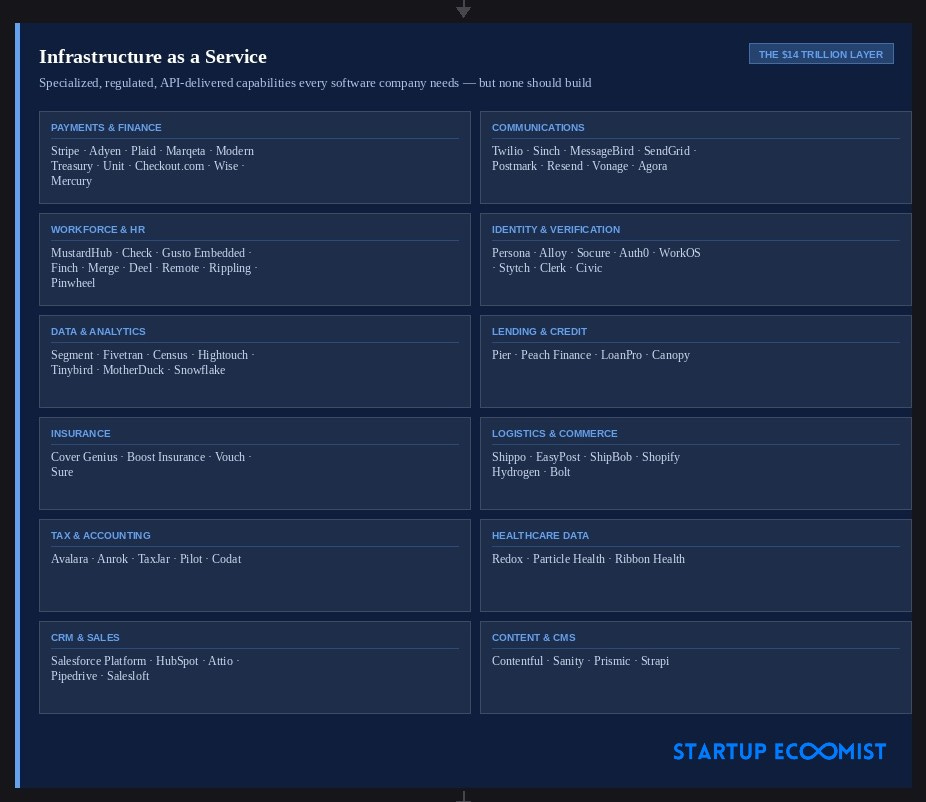

What occurred to me is that each sector of our economy represents a category where the regulatory complexity, the machine learning depth, or the partnership requirements are severe enough that specialized companies emerge. Understanding this tells a founder where they’re wasting engineering time, tells an investor where the real moats are, and tells an economic developer which companies are actually worth backing in a region trying to build something durable. Without this map, the build-vs-embed decision is a gut call. So, I threw together a guide to where that infrastructure lives and who built it.

In payments and money movement, Stripe is the most recognizable example. Connect routes money between parties on a platform; Issuing handles card programs; Treasury is banking-as-a-service infrastructure. Businesses on Stripe generated $1.9 trillion in 2025, and Stripe Connect now supports more than 15,000 SaaS platforms, helping businesses embed payments and financial services into their products. Adyen runs a similar full stack from card acquiring to issuing, with strong footing in enterprise and cross-border commerce. Checkout.com favors high-growth marketplaces tend to favor while Marqeta built modern card issuing infrastructure and is the backbone behind cards at DoorDash, Square Cash App, and Instacart.

You’ll notice if you look at these, the interchange the words software, platform, and infrastructure, so I want to refine that with other examples.

Plaid connects bank accounts to software applications, enabling financial applications access user-permissioned banking data. Modern Treasury handles payment operations infrastructure (ledgering, reconciliation, and payment workflow layer). Unit and Treasury Prime offer banking-as-a-service for non-bank platforms, handling bank partnerships, regulatory compliance, and core banking APIs so that SaaS can offer checking accounts and debit cards without becoming a bank. Wise handles cross-border money movement through a single integration. Mercury’s embedded offering extends banking capabilities to startup-focused platforms. Peach Finance, LoanPro, and Canopy are the loan management and servicing layers. Avalara has been the tax compliance provider for over two decades. TaxJar integrates compliance directly into payment flows. Anrok handles SaaS sales tax specifically, which operates under different economic nexus rules than physical goods. Codat provides accounting data connectivity across QuickBooks, Xero, and Sage. The global embedded finance market is estimated to grow to $588 billion by 2030 from around $100 billion; that growth isn’t demand for new banking apps; it’s software companies finally embedding the financial infrastructure their products already need.

Consider communications, Twilio built the category of programmable communications, turning voice, SMS, WhatsApp, and email delivery into API calls. What once required telecom carrier relationships, dedicated hardware, and a network engineering team is now a few lines of code. Sinch and MessageBird/Bird compete in the same category with strength in omnichannel messaging. Vonage brings telecom to programmable voice and video. SendGrid nailed email at scale; Postmark and Resend focused on serving developers. Agora tackles for real-time video what Twilio did for voice. Your startup’s comms feature, built from scratch, will be worse and slower and more fragile; the only question is how long it takes to admit that.

In payroll and HR, Gusto Embedded and Check let vertical SaaS companies offer payroll without becoming payroll processors. Finch aggregates employment data across HRIS (Human Resources Information Systems) and payroll providers. Deel and Remote both expose their employer-of-record infrastructure via API, so a software company can offer global hiring without becoming a global employment compliance operation. Rippling extends workforce data and automation. Pinwheel handles payroll connectivity for income and employment verification. MustardHub covers the behavioral workforce intelligence layer above all of these, identifying employees likely to leave and when intervention is needed and detecting team-wide sentiment shifts that may trigger broader disengagement, embedded it into HR Tech helps businesses retain employees. According to Katie Navarra with Society for Human Resource Management (SHRM), replacing an employee costs half to twice their annual salary; difficult hires cost an employe more, $12,800 on average versus $4,000 for a standard hire.

Identity and verification reinforce the costs of getting this stuff wrong. Socure has become the gold standard for predictive identity verification; now essential infrastructure for the majority of the top 20 U.S. banks. Persona focuses on a configurable experience. Alloy is the identity decisioning layer banks and fintechs use to run KYC, KYB (Know Your Business), AML (Anti-Money Laundering), and fraud rules through one engine without building compliance logic themselves. Auth0, Stytch, and Clerk handle authentication infrastructure. WorkOS handles enterprise SSO and SCIM provisioning. This is the stuff that would take a company months of engineering. Civic covers decentralized identity verification.

Klarna Bank was fined approximately $45 million in December 2024 for inadequate AML controls; City National Bank was fined $65 million in January 2024 for failing to maintain effective risk management. The Infrastructure as a Service alternative to those fines is a per-verification fee.

Data and analytics infrastructure is where the “build vs. embed” question gets interesting, because the data layer feels like something a technical team can handle but we’ve been doing this with Google Analytics for decades. Fivetran moves data from source systems to data warehouses; Hightouch run the reverse direction for marketing. Tinybird turns raw event data into real-time analytics APIs. Snowflake leans toward AI.

Cover Genius built global embedded insurance distribution infrastructure through partnerships with Booking Holdings, Uber, and Amazon. Boost Insurance lets companies build insurance products without an insurance license. Vouch and Sure cover startup-specific and point-of-need distribution.

Logistics and commerce infrastructure is where the physical economy meets the API economy. Shippo and EasyPost handle shipping labels, carrier rate comparison, and tracking across every major carrier without requiring individual agreements with UPS, FedEx, USPS, DHL, and dozens of regional operators. ShipBob’s API extends into fulfillment. Shopify’s Hydrogen provides composable commerce infrastructure for headless storefronts. Bolt handles checkout specifically, with a network-based one-click conversion rate that independent builds can’t match.

CRM and sales infrastructure was alluded to during my start. Salesforce built the category as SaaS, then became the platform that thousands of applications are built on top of rather than alongside. HubSpot operates the same way at a different market segment. The CRM becomes infrastructure the moment other software depends on it as a data source and workflow engine rather than using it directly.

Content infrastructure is the layer most frequently confused with tooling. A CMS (Content Management System) in its traditional form is SaaS: a finished product editors log into and use. Contentful, Sanity, and Prismic operate differently: they expose content as structured data via API, so that any frontend, any application, and any channel can consume it without being coupled to a specific rendering layer. That shift turns content management from a tool into infrastructure. We can also look at the difference between the software of WordPress and the software provided by WP Engine; both providing the CMS while one offers an infrastructure layer.

The most regulatory complexity, greatest need for innovation, and the worst consequences for getting it wrong are in healthcare. Healthcare data lives across hundreds of incompatible Electronic Health Record systems (Epic, Cerner, Athenahealth, Allscripts) each with its own data format and integration requirements. A digital health company that wants to read or write patient data isn’t solving an API problem; it’s facing years of individual hospital IT negotiations and a tangle of standards that don’t speak to each other. Redox solves this with a single API endpoint, CEO Trip Hofer helps distinguish IaaS, “Yesterday, Redox was your interoperability highway, moving data from point A to B. Today, it’s about giving you the ability to control, enhance, and shape how that data flows across your ecosystem, all in one place.” Particle Health handles patient record retrieval. H1 provides continuously updated provider data that makes finding an in-network provider actually work.

The pattern across all of these, payments, communications, workforce, identity, data, lending, insurance, logistics, tax, and healthcare, is the same in a domain with deep regulatory complexity, specialized machine learning or data network requirements, and relationship-intensive infrastructure that no single product team can capably own. Infrastructure as a Service exists because the cost of getting it wrong is catastrophic, in fines, fraud losses, engineering time, and in healthcare, patient safety, and the cost of using the infrastructure layer is a fraction of that.

Someone is going to read this and argue that AI disrupts this just as it is SaaS; this is where this got interesting for me to explore.

AI runs on top of Infrastructure as a Service. It doesn’t replace it. AI agents need to transact, move money, verify identities, and send communications, and they need to do all of that in a compliant, auditable, reliable way. The infrastructure requirement doesn’t go away with AI; it grows. Teams cannot reliably generate compliance logic, fraud models, or verification flows with a language model. Stripe’s fraud model is trained on transaction data from millions of businesses across trillions of dollars of volume. Behavioral workforce intelligence is best left to MustardHub. Redox’s healthcare data exchange network took over a decade to build across 12,000 organizations. Plaid’s bank connectivity came from years of individual institution agreements. No language model generates that expertise nor those relationships.

AI without infrastructure is a demo. AI on top of Infrastructure as a Service is a product.

Here’s the thesis, it’s simple: SaaS companies are not infrastructure while infrastructure is not what is sold to end users. Mixing up which one you’re building wastes years and resources building things that should have embedded. Usage-based revenue that looks variable is usually attached to regulatory moats and data network effects that are anything but – that difference is where there is a line here. API-first companies command a 25% valuation premium, and companies with mature API strategies see 12.5% higher revenue growth. Stop building the layer someone else already built better.

The teams who understand Infrastructure as a Service, who know which specialized companies exist for every domain where they shouldn’t be building, move faster, spend less, and build things that are harder to copy. That’s what office hours are for if working out which layer you’re actually building versus which layer you should be embedding.