This is a technical note for economists, which I am putting up basically so I can refer to it later on. Normal human beings may want to skip it.

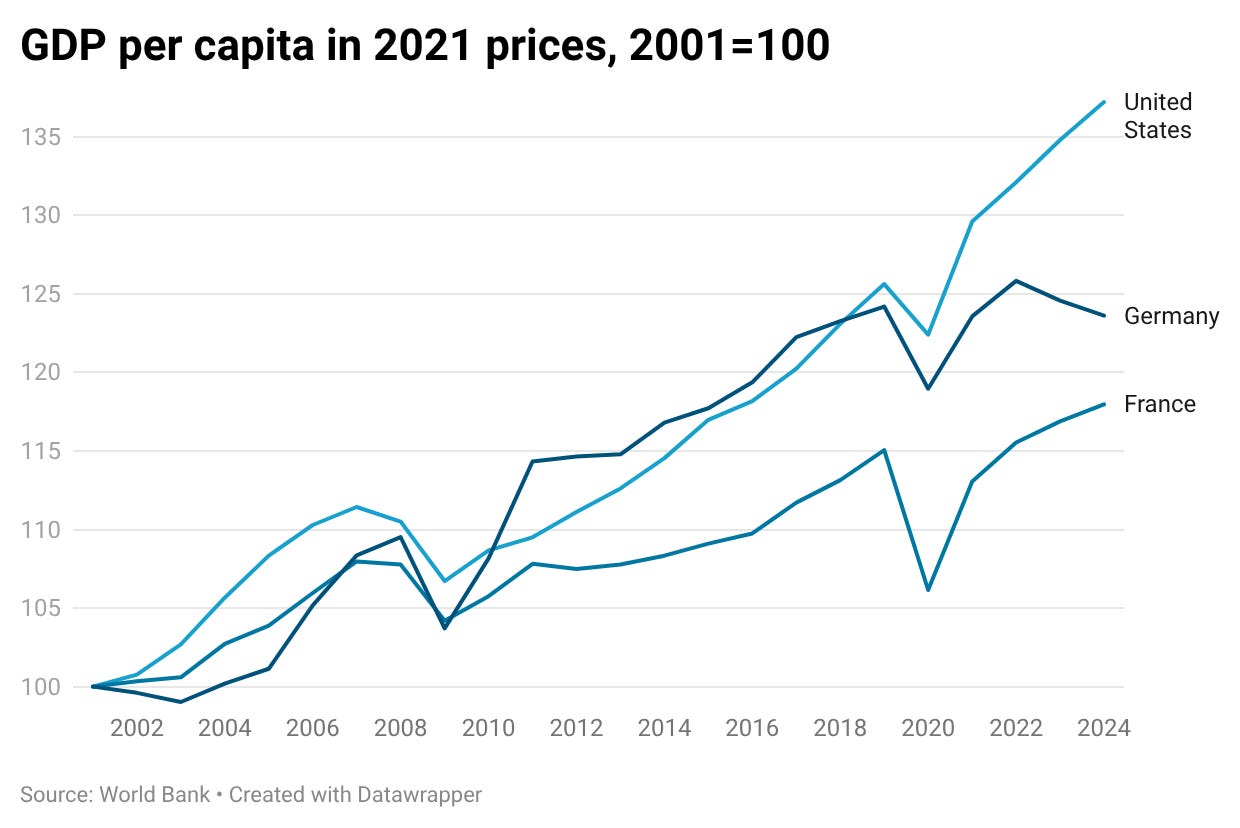

I recently wrote about the European economy, and how the widespread narrative that says that Europe is in decline isn’t supported by the evidence. As I noted, conventional measures of growth in GDP per capita have favored the United States since 2000:

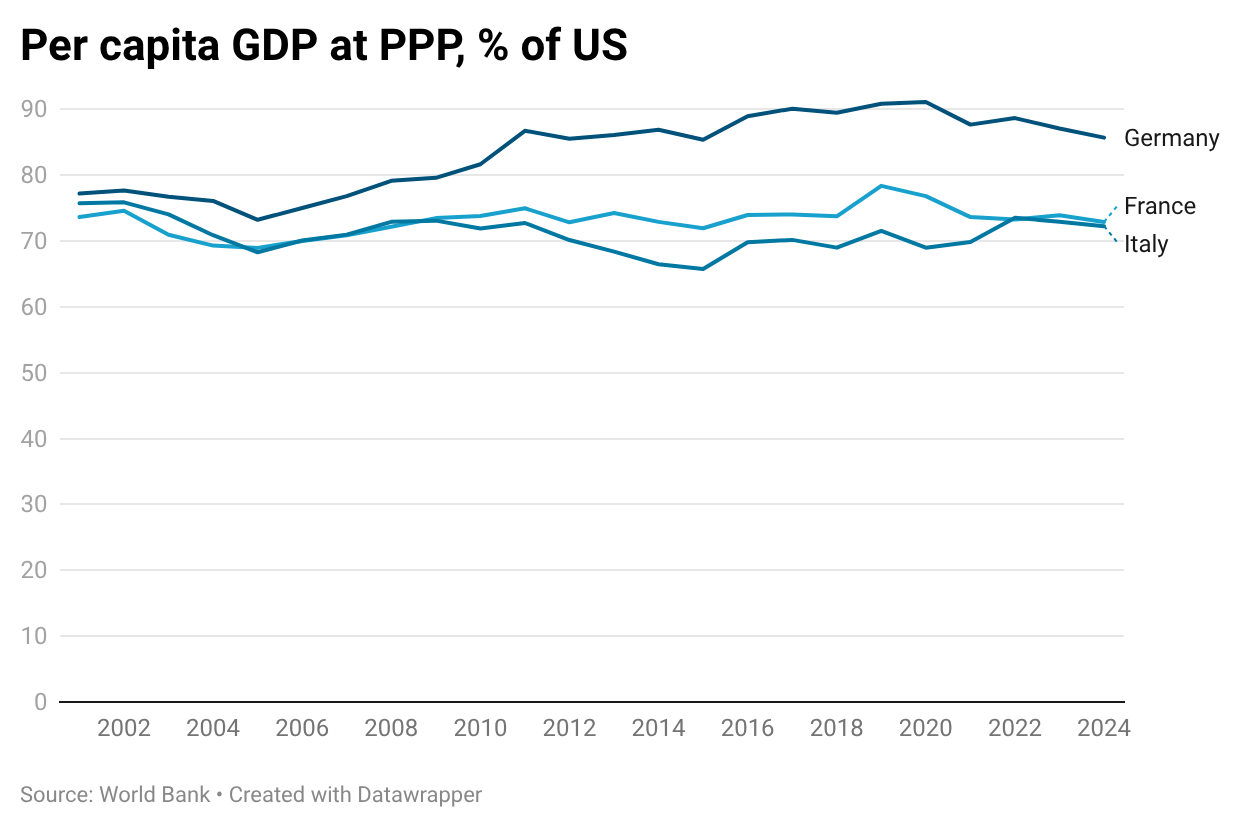

But European relative GDP per capita measured at PPP has not declined:

Call this the US-Europe paradox.

Of course, it isn’t really a paradox. It makes perfect sense given US dominance of sectors that are experiencing rapid productivity growth, which leads to a rise in relative US GDP at constant prices but doesn’t translate into a rise in relative GDP at current prices. But I worry somewhat that my attempt to explain what’s going on in terms that non-economists might be able to follow may, um, paradoxically have made it less clear to economists. So this note lays the story out economics-professor style, with a bit of math.

Economese from here on.

A stylized model of the US-Europe paradox

Imagine a world consisting of two countries, US and EU. Assume for the sake of simplicity that labor is the only factor of production, and that the two countries have equal labor forces.

There are two goods, tech (T) and nontech (N). Both are costlessly tradable. Preferences are Cobb-Douglas, with consumers in both countries spending a constant share 𝜏<1/2 of their income on T.

Labor productivity in the production of N is assumed to be the same in both countries, and again for simplicity I assume zero productivity growth in that sector. Because productivity is the same and N is tradable, this ensures that wages are the same in the two countries, and hence that GDP in current prices is the same.

However, there is technological progress in tech, T.

I assume that US has a comparative advantage in T, and hence that all T is produced there. It doesn’t matter for this model what the source of that comparative advantage is, although in the real world it has a lot to do with the positive externalities generated by industrial clusters.

Crucially for this analysis, T experiences more rapid technological progress than N. I assume that productivity in that sector rises at a rate ⍴, versus zero in N.

Given these assumptions, what does the model imply for measured growth and relative performance?

As I’ve set it up, the model implies that all T will be concentrated in US. Because T attracts a share 𝜏 of world spending, it will also account for a share 𝜏 of world GDP, and hence 2𝜏 of US GDP.

Given this, technological progress in T implies rising US real GDP, measured the way we actually calculate it — as growth in “chained” constant prices — at a rate of 2𝜏𝜌. Growth in EU real GDP is zero. (We could obviously add in some growth in N productivity to make this number positive.) Yet relative GDP at current prices remains 1.

Oh, and real wages rise at the rate 𝜏𝜌 in both nations.

And that’s the US-Europe paradox. US dominance in tech leads to higher measured growth in the United States than in Europe, but not to a divergence in relative GDP or living standards.

Now back to writing in something resembling English.