Insights · 2025

Payer 2025 Trends in Cost Containment & 2026 Outlook

An analysis of payer margin pressure, denial trends, and what the industry should expect heading into 2026.

Executive summary

•

Payers are entering 2026 under sustained margin, regulatory, and operational pressure. Scrutiny around denials, appeals, and prior authorization is increasing, while providers are rapidly deploying AI-driven tools that accelerate revenue optimization and appeals—intensifying pressure on payer operating models.

•

Policy, prior authorization and formulary remain central cost-containment levers, influencing ~25–30% of medical spend. However, wide variation in policy coverage across payers, often with only 30–40% overlap, has led to inconsistent denial outcomes, higher administrative burden, and increased provider and member abrasion without proportional clinical or financial benefit.

•

As these pressures continue and rise in intensity, NOF1 enables this shift by structuring and benchmarking policy and contract data, accelerating opportunity identification, quantifying financial impact, and supporting more effective, defensible contracting and policy decisions.

Evolving payer pressure

Payers are facing a questioning eye towards status quo

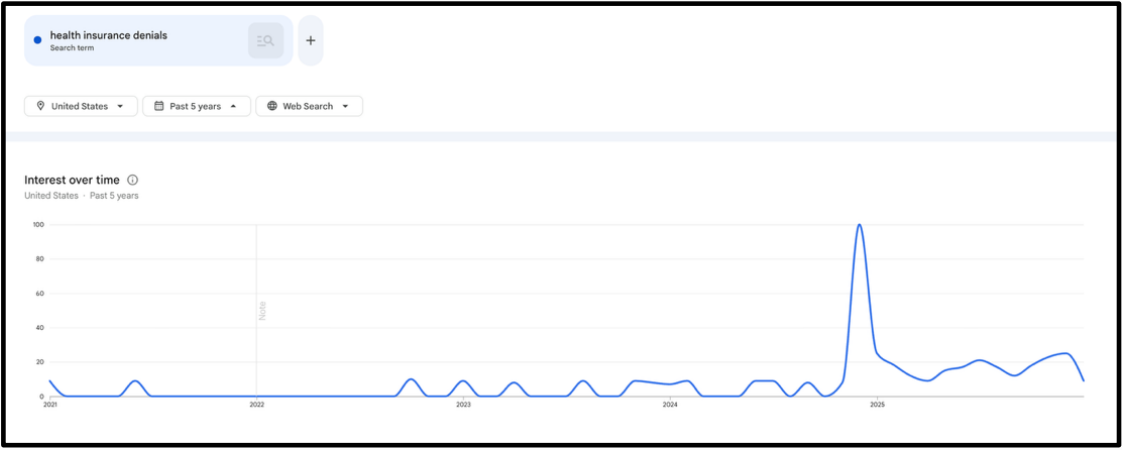

Denial search-based interest over the last 5 years

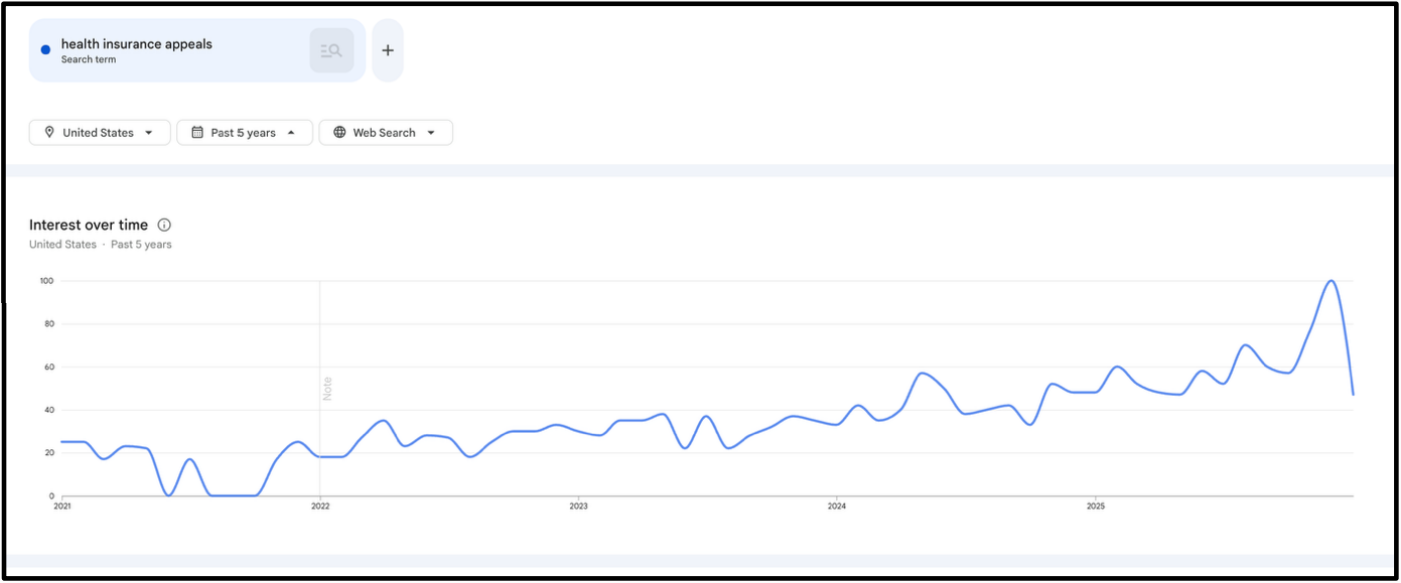

Appeals search-based interest over the last 5 years

... and a regulatory pressure to change prior auth and necessity reviews

AHIP

Health plans, led by America's Health Insurance Plans (AHIP), pledged to streamline, simplify, and reduce prior authorization burdens by standardizing electronic submissions, reducing services requiring review, honoring prior approvals during transitions, improving communication and transparency, and expanding real-time responses. Plans aim to accelerate decisions and reduce admin hurdles for providers and patients.

CMS

CMS's final rule mandates FHIR-based APIs and measurable standards to modernize data exchange and prior authorization processes. Impacted payers must implement APIs by 2027, speed decision timeframes (72 hours urgent, 7 days standard), and publicly report metrics, improving transparency, reducing administrative burden, and enhancing patient and provider access to data

... while providers leverage AI for revenue optimization faster than payers are industrializing control

Scribe

In-visit speech to text scribing of provider and patient conversation

Add-on services of automated coding extraction, HCC extraction

Payer impact: "RCM" services attached to core functionality can increase payment pressure and higher risk scores for VBC context

Denial prevention

EMR-embedded capabilities to inform providers at point of care of clinical necessity criteria that allow providers to navigate payer policies without running into

Payer impact: Positive impact, informs providers of payer preferred care pathway without creating administrative overhead of denials

Appeal support

Automated appeal drafting and submission post-denial

Payer impact: Leads to higher volumes of appeals per denied claim, increasing pressure on payers to either auto-approve appeals or decrease denials (despite being warranted)

.. driving quarterly margins to their lowest over the last 8 quarters

Publicly reported margins by quarter, (%)

Payers' approach to managing this pressure

Payers relied on a more targeted set of cost reduction / margin levers in 2025

Policy revamp / prior auth improvement

Identifying gaps in coverage criteria and payment integrity rules and assessing the optimal path to bridge gaps while optimizing admin expense and managing provider / member abrasion

Site of care management

Deeper assessment of clinical and pharmaceutical services that may be serviced across multiple sites of care and reviewed applicability (e.g., Obs vs. IP, ASC vs OP, Injection in Office vs. Home)

Network narrowing / cost renegotiation

Wide variety of levers here deployed, including:

- Contract renegotiations with stronger willingness to lose contracts if systems don't align to rates

- Reference based pricing and setting out of network costs

VBC

- Expanding Primary Care focus to specialty, including across: Oncology, Cardiovascular

- Increasing utilization of home based VBC (e.g., HarmonyCares, Landmark)

Plan repricing

Reprice plans as a last resort in turbulent lines of business, specifically in Medicare and ACA

Meanwhile, payers are using policy to manage appropriate spend

Commercial

~30% spend

managed

through policy / PA

Medicare

~25% spend

managed

through policy / PA

But policy remains to be a widely different capability across payers

~10-40% spend managed through policy and prior auth in Commercial LOB

~15-30% spend managed through policy and prior auth in Medicare LOB

Across payer policy, there's only 30-40% overlap across any two payers

| Source Payer | Aetna | UHC | Cigna | Anthem-NY | BCBSMA | BCBST | Cambia | Capital Blue | Emblem | HCSC | Health Partners | IBC | Kaiser | Moda | Oscar | Pacific Source | Premera | Providence | Select Health |

| Aetna | 14 | 18 | 39 | 15 | 11 | 23 | 10 | 4 | 23 | 15 | 28 | 15 | 25 | 7 | 5 | 15 | 12 | 15 | |

| UHC | 58 | 34 | 47 | 19 | 13 | 37 | 16 | 6 | 35 | 41 | 48 | 23 | 43 | 15 | 6 | 23 | 19 | 19 | |

| Cigna | 39 | 23 | 44 | 16 | 8 | 22 | 9 | 5 | 19 | 18 | 20 | 15 | 25 | 7 | 7 | 23 | 12 | 11 | |

| Anthem-NY | 57 | 18 | 30 | 21 | 14 | 35 | 16 | 4 | 31 | 23 | 38 | 14 | 36 | 9 | 4 | 21 | 16 | 16 | |

| BCBSMA | 39 | 12 | 22 | 37 | 29 | 44 | 29 | 5 | 62 | 12 | 25 | 23 | 11 | 3 | 8 | 49 | 18 | 25 | |

| BCBST | 45 | 14 | 18 | 35 | 50 | 49 | 40 | 8 | 53 | 14 | 32 | 26 | 12 | 4 | 8 | 38 | 27 | 34 | |

| Cambia | 40 | 17 | 19 | 39 | 30 | 21 | 21 | 5 | 30 | 17 | 27 | 18 | 21 | 5 | 7 | 28 | 20 | 22 | |

| Capital Blue | 37 | 16 | 15 | 37 | 44 | 36 | 49 | 6 | 43 | 13 | 28 | 24 | 13 | 3 | 8 | 33 | 27 | 32 | |

| Emblem | 50 | 22 | 31 | 32 | 28 | 25 | 40 | 23 | 35 | 29 | 37 | 29 | 14 | 11 | 23 | 23 | 37 | 38 | |

| HCSC | 57 | 20 | 24 | 53 | 59 | 32 | 46 | 27 | 6 | 21 | 38 | 26 | 26 | 10 | 7 | 44 | 23 | 26 | |

| Health Partners | 53 | 36 | 28 | 55 | 15 | 10 | 36 | 12 | 6 | 30 | 45 | 19 | 47 | 14 | 9 | 21 | 18 | 21 | |

| IBC | 58 | 25 | 20 | 51 | 23 | 16 | 34 | 18 | 6 | 35 | 31 | 20 | 42 | 11 | 6 | 21 | 19 | 20 | |

| Kaiser | 55 | 22 | 28 | 39 | 33 | 21 | 44 | 17 | 6 | 32 | 15 | 26 | 25 | 6 | 15 | 39 | 38 | 45 | |

| Moda | 66 | 30 | 32 | 63 | 11 | 7 | 32 | 9 | 3 | 29 | 32 | 54 | 14 | 14 | 6 | 14 | 12 | 11 | |

| Oscar | 56 | 28 | 23 | 46 | 9 | 5 | 24 | 5 | 4 | 26 | 22 | 29 | 12 | 41 | 8 | 18 | 13 | 13 | |

| Pacific Source | 55 | 21 | 41 | 34 | 41 | 16 | 41 | 21 | 22 | 35 | 32 | 35 | 49 | 29 | 15 | 32 | 43 | 37 | |

| Premera | 46 | 18 | 30 | 44 | 58 | 28 | 52 | 27 | 5 | 53 | 19 | 29 | 23 | 15 | 8 | 8 | 25 | 29 | |

| Providence | 54 | 25 | 31 | 43 | 33 | 26 | 49 | 30 | 12 | 39 | 25 | 41 | 44 | 25 | 9 | 20 | 36 | 46 | |

| Select Health | 51 | 16 | 22 | 34 | 33 | 26 | 41 | 27 | 9 | 36 | 18 | 28 | 34 | 15 | 6 | 12 | 31 | 34 |

Policy variation creates noise, not signal — driving provider abrasion without proportional clinical or financial benefit.

... which also drives a high variation in effectuation of denials; increasing administrative overhead and adversely impacting member and provider experience

National average denial rate

Site of care has been one major lever for managing spend without disrupting care

Where do payers go from here? It depends on where they are today

Payers can be classified into one of 3 archetypes

Early payer⭐ | Mature payer⭐⭐ | Best-in-class payer⭐⭐⭐ | |

|---|---|---|---|

| Program philosophy | Focus on reaching market parity on policy and prior auth program scope / efficiency | Focus on creating incremental value and actively reacting to new clinical technologies | Objective is well balanced across patient outcomes, provider guidance, managing opex expense and containing cost |

| Policy & adjudication approach |

| Guided through manual research of peers & competitors' recent policies |

|

| Tech enablement | Limited tech involvement in PA process beyond administration software |

|

|

| Employer / Provider / Member perception |

|

|

|

As we look towards 2026, we expect payers to move towards the following actions

1.

Inform policy and prior auth programs with real data – not manual research flows – that highlight areas of focus that are most aligned to trends and new medical and pharmaceutical technologies

2.

Digitize policy and PA programs into machine-readable formats that enable safe automation and withstand compliance requirements

3.

Invest in interoperability to support FHIR-ready PA, denial, and appeals workflows

4.

Pilot automation use cases with UM vendors, in-line with CMS direction and CMS's own WISER pilot program

5.

Balance policy strictness with a desire to lower administrative burden and improve patient and provider experience

6.

Stand-up defensive programs relative to provider AI use cases, including: Coding level reviews for chart reviews, provider behavior analytics and contract reviews due to reduced OpEx

7.

Establish measurable, interoperable, and defensible operating models that prove administrative burden reduction without compromising clinical integrity or regulatory compliance

Payers that fail to move in this direction risk regulatory exposure, loss of pricing leverage, and structurally higher overpayment rates.

How we help payers

•

Illuminate policy blind spots – We bring structure and transparency to a fragmented policy landscape, enabling rapid comparison, benchmarking, and evidence-backed research across programs.

•

Accelerate opportunity identification – We compress 12 months of manual policy analysis into 4–8 weeks, enabling payers to identify, prioritize, and implement high-impact policy opportunities up to 10× faster.

•

Reduce public and regulatory scrutiny risk – We proactively surface unnecessarily restrictive criteria and support payers in aligning policies with evidence, provider behavior, and patient outcomes—reducing abrasion, appeals, and reputational risk.

•

Quantify financial impact – We tie policy variation directly to PMPM spend, utilization patterns, and denial outcomes, allowing payers to prioritize opportunities by financial materiality, not just clinical interest.

About us

NOF1 is a transparency platform for payer-provider policy and contracts. Our goal is to transform the way payers, providers, and other stakeholders collaborate to streamline how healthcare is provided while reducing unnecessary expense.