The money question has long backgrounded a history of debate in economics. After observing how economic debates usually evolve, I have concluded that a large part of the persistent confusion that permeates economic discourse stems from a poor understanding of the nature of money. This article will therefore aim to address these fundamental misconceptions and explain why different understandings of what money is have wide-reaching policy implications and that getting this right is crucial in formulating good policy and achieving our goals in society.

Money is one of those fundamental creations of society that everyone uses but few stop to question. Put simply, money is that which we use to pay for things. However, the full explanation of money is rather more complex. Is money essentially a physical commodity that emerged from primitive barter? Or is it a social credit instrument, a token of debt shaped by law and state authority? These are the two broad camps I intend to cover here. Economists and thinkers have debated these questions and the ontology of money for centuries, and the answer profoundly influences how we design economic policy.

This essay will therefore explore two major competing theories of money: the commodity (or ‘metallist’) view and the credit/state (or ‘chartalist’) view, and why it matters which story we believe. I intend to explain why I see the credit state money perspective as being the most accurate view of modern money and show how each paradigm and the evolving perspectives on money, from Adam Smith to John Maynard Keynes to modern MMT (Modern Monetary Theory) economists, carries its own narrative and policy implications.

The commodity theory of money paints a familiar picture as it is the pervasive conventional wisdom for where money came from. In the beginning, there was barter. Human societies, it says, started with people directly exchanging goods such as goats for grain or shoes for fish, until the hassle of the ‘double coincidence of wants’ (needing to find someone who has what you want and wants what you have) led to the adoption of a common medium of exchange (Bell, 1998). According to this view, enterprising traders gradually converged on the most marketable commodity – perhaps gold, silver, or salt – as a universal exchange medium to lubricate trade. Over time, this commodity-money was formalised into coins of set weight and purity, often stamped by rulers to certify the content. Money’s value, in this story, derives from the intrinsic value of the commodity it’s made of or backed by (precious metal content, for example), not from any declaration by an authority.

This perspective was articulated by many classical and neoclassical economists. Adam Smith in The Wealth of Nations described how money likely arose as people realised the need for a universally accepted commodity in trade, noting that before money, ‘barter’ exchanges were stymied by the lack of a common medium. “If [a buyer] should chance to have nothing that [a seller] stands in need of, no exchange can be made between them” (Smith, 1776). Later, the Austrian economist Carl Menger famously argued in 1892 that money emerged organically from barter through the self-interest of traders, without state intervention. “Money has not been generated by law. In its origin it is a social, and not a state institution”, Menger wrote, insisting that the state only came later to “perfect” the coinage of an already-existing money commodity (Menger, 1892). In other words, money is a “creature of the market” under this theory, a product of voluntary exchange and the goods people found most convenient to trade, rather than an arbitrary creation of states.

From this metallist viewpoint, even when paper notes or tokens came into use, they were seen merely as promises to pay the ‘real’ money, the commodity (like gold), or as backed by it. The 19th century economist Ludwig von Mises, building on this logic, argued that even unbacked (fiat) money must have originated as a commodity at some earlier point. His “regression theorem” held that people only accept fiat money because they expect it can ultimately be converted to something of tangible value, tracing back to a time when it had a commodity value (Mises, 1912). Mises dismissed the idea that government fiat alone could create money value, calling such a notion “etatist” and self-contradictory. For metallists, the role of the state is at best to certify the weights of coins or restrain fraud; the state might stamp gold and silver coins, but it was the metal that really gave money its worth. This underlies sound money doctrines and a pre-disposition to favour endogenous market-oriented solutions to economic problems, given the belief that money’s provenance lay in market exchange in the ways described.

Under this paradigm, money is ‘neutral’, essentially a veil over the real ‘barter’ economy of goods and services. Changes in the money supply mostly just change prices and have no lasting impact on real production or employment, especially in the long run. The classical Quantity Theory of Money (popularised by monetarist thinkers like Irving Fisher and later Milton Friedman) fits in here. If you control the money supply, you control inflation and keep government hands off except to maintain the gold standard or a stable currency. If money is a scarce commodity or firmly backed by one, excessive government spending is seen as dangerous, akin to clipping coins or printing too many banknotes, which would only debase the currency and cause inflation.

In this mindset, fiscal policy should behave like a household budget (spend only what you collect in taxes or borrow in markets), and unemployment might be viewed as an unfortunate but unavoidable artefact of market activity, something intrinsically produced by human interactions and not a function of institutional design or government policy. Indeed, by the late 20th century, orthodox policy leaned on the notion of a ‘Non-Accelerating Inflation Rate of Unemployment’ (NAIRU) – essentially, a belief that a certain level of joblessness is the inevitable trade-off to keep prices in check (Mitchell, 2011). Using unemployed people as an inflation-fighting buffer stock was eventually implicitly accepted with a resurgence of classical thinking on economics and money in the 1970s. Central banks focused on controlling inflation by adjusting interest rates or money growth, while ‘full employment’ as a policy goal took a backseat to price stability.

In summary, the metallist commodity theory sees money as a market phenomenon that predates states. First came barter, then commodity money, and eventually modern money evolved from those origins with states shaping and often seen as interfering in market mechanisms. The state’s role is often seen as limited to protecting property rights and maybe coining metal, but it is not fundamentally what gives money its value or an entity of particular importance in our monetary production system. Money’s value comes from its material (or its convertibility into a valuable material) and exchange value, and fiscal or monetary mismanagement is feared primarily because it might undermine the natural order of a market allocating resources via price (e.g. through inflation or redistribution). This worldview naturally leads to policy preferences like tight control of the money supply, balanced budgets or gold standards to constrain governments, and using interest rates or unemployment to guard against inflation. It’s a logically appealing story but, as I’ll expound on next, history and anthropology have not been kind to the barter myth, and an entirely different theory of money has long challenged these orthodox assumptions.

Contrast the above with the credit or chartalist theory of money, which flips the origin story on its head. The credit theory holds that money did not emerge from bartering goods at all. Rather, money arose as a unit of account and a system of IOUs (debts and credits) within early communities, often orchestrated or at least denominated by some central authority (like a temple or a ruler). In this view, money is fundamentally a social relationship, a credit-debt promise, and a creature of law or institutional design.

Over a century ago, economists began unearthing evidence that undercuts the barter narrative. In 1913, British economist and anthropologist Alfred Mitchell-Innes wrote a seminal essay titled What is Money? which boldly concluded “Credit and credit alone is money… Credit is simply the correlative of debt” (Innes, 1913). Every monetary transaction, Innes argued, creates a creditor and a debtor; money, therefore, is not a concrete commodity but an accounting of obligations or a token of someone’s liability and someone else’s asset.

Innes’ exposition is so compelling in fact that it is worth extracting some key parts at length:

“A first class credit is the most valuable kind of property. Having no corporeal existence, it has no weight and takes no room. It can easily be transferred, often without any formality whatever. It is movable at will from place to place by a simple order…

Credit is the purchasing power so often mentioned in economic works as being one of the principal attributes of money, and, as I shall try to show, credit and credit alone is money. Credit and not gold or silver is the one property which all men seek, the acquisition of which is the aim and object of all commerce. The word “credit” is generally technically defined as being the right to demand and sue for payment of a debt, and this no doubt is the legal aspect of a credit today…

we have been led to the notion that payment in coin means payment in a certain weight of gold. Before we can understand the principles of commerce we must wholly divest our minds of this false idea. The root meaning of the verb “to pay” is: that of “to appease,” “to pacify,” “to satisfy,” and while a debtor must be in a position to satisfy his creditor, the really important characteristic of a credit is not the right which it gives to “payment” of a debt, but the right that it confers on the holder to liberate himself from debt by its means—a right recognized by all societies. By buying we become debtors and by selling we become creditors, and being all both buyers and sellers we are all debtors and creditors. As debtor we can compel our creditor to cancel our obligation to him by handing to him his own acknowledgment of a debt to an equivalent amount which he, in his turn, has incurred…

This is the primitive law of commerce. The constant creation of credits and debts, and their extinction by being cancelled against one another, forms the whole mechanism of commerce and it is so simple that there is no one who cannot understand it. Credit and debt have nothing and never have had anything to do with gold and silver.

It is by selling, I repeat, and by selling alone—whether it be by the sale of property or the sale of the use of our talents or of our land—that we acquire the credits by which we liberate ourselves from debt.” (Innes, 1913)

The above presents a searing attack on the fundamental but understandable misconceptions that lead one to arrive at commodity theories of money and grants a compelling counter narrative.

The central idea Innes explains here is this: “the really important characteristic of a credit is not the right which it gives to “payment” of a debt, but the right that it confers on the holder to liberate himself from debt by its means”. This is crucial to understand our modern monetary and non-convertible fiat currency system. No longer does the state that issues the credit unit of account promise to provide (‘convert’), upon redemption, a physical commodity (e.g. gold) in ‘payment of a debt’; it solely promises to uphold the more essential characteristic of credit: that of providing the holder the opportunity to extinguish their own liabilities to the state. It can be shown that these private liabilities are primarily the taxes levied by the state in pursuit of provisioning the public purpose. Modern state money, then, can be analysed first and foremost as a tax credit, with the state as a single (monopoly) supplier of that which is demanded in payment of taxes (Mosler, 2024). Taxes are therefore a sufficient anchor of general acceptability of a state currency.

Innes showed through historical examples that many so-called ‘commodity monies’ were just credit instruments. For instance, medieval tally sticks in England were wooden sticks notched to record the Crown’s debts and tax credits. Innes pointed out that no purely barter economy had ever been described by anthropologists. Instead, ancient societies kept ledgers of credits and debits long before coins. Temples in Mesopotamia recorded who owed grain to whom, and people traded by exchanging promises (clay tablets, tokens, or written tallies) to settle debts at harvest time. Money, in this sense, began as ‘creditary’ units (a way to measure and settle debts) not as gold or silver circulating by weight (Innes, 1913).

Crucially, the credit theory dovetails with the state theory of money, known as chartalism (from the Latin charta for token or ticket). Georg Friedrich Knapp, a German economist, advanced the state or chartalist perspective in his 1905 book The State Theory of Money. Knapp argued that money is fundamentally a creation of the public authority. “The money of a State is... what is accepted at public pay offices”, he wrote, meaning that whatever the state declares it will accept in payment of taxes or fees automatically becomes money in that society (Bell, 1998; Knapp, 1905). It doesn’t matter if it’s a gold coin, a piece of paper, or a tally stick; what matters is that the state proclaims it accepts that token for settling your obligations to the state. “Money is a creature of law”, Knapp insisted. Its validity “is not derived from the material of which the [token] is made”, but from the legal decree that this token will discharge debts.

In a useful analogy, Knapp likened state-issued money to a ticket you receive when you check a coat for safe-keeping or to a postage stamp. The physical token itself has negligible intrinsic value, but it symbolises a social relationship, the right to reclaim your coat, the right to post your letters, or in the case of money, the right to have your tax obligation cleared. The state’s stamp on a coin or note is like the cloakroom attendant’s token. It promises that when you present that token, it will be accepted for something in return (in the state’s case, for a tax receipt recording that you have extinguished and lowered your own debt balance).

Even Adam Smith, who expounded on the commodity theory, hinted at this credit principle in a passage in The Wealth of Nations. He noted that a government could “give a certain value” to otherwise worthless paper simply by declaring it will accept that paper for taxes:

“A prince, who should enact that a certain proportion of his taxes should be paid in a paper money of a certain kind, might thereby give a certain value to this paper money” (Smith, 1776).

In one stroke, Smith recognised the chartalist insight that people will value the token that can pay taxes, because taxes are an enforced obligation. As MMT economists often quip, ‘taxes drive money’ because you need the government’s tokens to settle your tax obligations that are denominated uniquely in those tokens/IOUs. If you don’t obtain the government’s money to pay your taxes, you could lose your property or go to jail. That creates an ongoing demand for the currency which gives it acceptance value, quite apart from any commodity backing. This mechanism elegantly solves a puzzle that metallists struggled with once money was no longer gold, the question of why would people accept ‘worthless’ paper money or bank deposits? The Chartalist answer is because those units are needed to settle debts, especially debts to the state (Bell, 1998). Far from being a mere afterthought to money’s story, the state is front and centre.

It’s important to note that this conception of tax-driven state credit money is not asserting that, on an individual level, we seek paid employment just so we can pay taxes. Of course, it’s clear to anyone reading this that you go to work, sell assets, or acquire rent on your assets, not to pay off debts in the first instance, but to consume. We all want to provide satisfactory living conditions for ourselves and our families and because we know we can acquire the real production that facilitates these conditions by first obtaining monetary credit instruments for onward exchange, we sell our labour (or assets) to obtain them.

But here’s the crucial point. It’s precisely because discharging the state’s own liabilities back to itself via tax redemption is the only method in which to relieve oneself of this debt that the state’s money is readily accepted. There is a long series of exchanges that constitute monetary production and the provision of final goods and services for sale for us to consume. At each and every node, all parties intrinsically accept payment in the state’s IOUs because in aggregate, taxes must be paid. So, it’s never about individuals needing to pay taxes that motivates them to enter monetary exchanges using the state unit of account, it’s a mechanism that operates at the aggregate level of the economy to drive the monetary system in the first place. Taxes create a non-negotiable baseline demand for the unit of account, and state spending supplies it; network acceptance then scales it.

John Maynard Keynes, the great British economist, was won over by this line of thinking. In his 1930 Treatise on Money, Keynes embraced Knapp’s ideas, declaring that

“the Age of Chartalist or State Money was reached when the State claimed the right to declare what thing should answer as money to the current money-of-account… To-day all civilised money is, beyond the possibility of dispute, chartalist” (Keynes, 1930).

Keynes emphasised that a money unit of account (e.g. dollars, pound sterling) is specified by the state, and the actual money is that which the state accepts in payment of obligations. In other words, governments define the unit of currency and ensure its acceptance by imposing tax debts payable in that unit. This is not a modern invention as Keynes noted that authorities have been doing this “for some 4,000 years at least”, going back to ancient civilisations where temple or palace authorities used taxes or tribute to give value to early money tokens (Keynes, 1930).

The chartalist-credit theory also sheds light on the history of coinage. Why did ancient or medieval states bother stamping coins with a face value often higher than the metal content? Because the value came from the ‘fiat’ (decree) that the coin would be accepted for its face value in taxes. For example, if a King stamped a copper coin as ‘worth one gold unit’ for tax purposes, people would treat it as such, even if its metal was worth far less as long as they needed it for taxes.

This also explains why debasing coins (mixing in cheaper metal or shaving off edges) was historically a big deal. Economist Stephanie Kelton (née Bell) explains

“To understand why the State objected to the debasement of precious metal coins, we must understand the reason for taxation. The purpose of taxation is to get people to work and produce for the State. That is, the state wants bridges, armies, etc. and gets the private sector to produce them by imposing taxes. To pay the taxes, the private sector must acquire the state’s money. By debasing coins, gold could be brought to the mint, coined, and exchanged against the unit of account in order to reduce one’s tax liability. The community, then, would have been able to satisfy their nominal tax liabilities by producing less for the State” (Bell, 1998).

In other words, since the state has no need for its own credit money but has need for real resources to provision for the public purpose, it needs us to need its credit money by levying taxes. Government spending then provides the credit which is required in exchange for the real production that the state wants. And if the private sector can obtain state IOUs via coin debasement or counterfeiting without sacrificing real resources, it compromises this mechanism and undermines the state’s capacity to provision itself at current prices.

Thanks for reading Jamie's Substack! This post is public so feel free to share it.

In fact, as Knapp and later Hyman Minsky (a twentieth-century economist in the chartalist tradition) pointed out, the reason sovereign states tax in their own currency is not to finance their spending (they can issue the currency at will), but to create a demand for their currency and thereby mobilise resources. “The need to pay taxes means that people work and produce in order to get that in which taxes can be paid” Minsky wrote, adding “the fact that taxes need to be paid gives value to the money of the economy” (Minksy, 1986). In other words, taxes are not directly fungible with real resources, but function to facilitate via an inductive process, the transfer of real production from private use to public use. Taxation only works to create real fiscal space in this way to the extent that by surrendering nominal credit, private actors correspondingly lower their own real consumption or investment, or firms correspondingly lower their employment levels, releasing real resources so that they can be employed by the state in a non-inflationary way.

Once money is understood as state credit, it becomes clear that the state not only does not spend out of revenue but cannot do so. It is not logically coherent for nominal revenue, whether raised through taxation or the issuance of government securities, to ‘finance’ government spending in the ordinary sense of that term. Government spending is the act that brings new units of the currency into existence. Taxes and bond sales, by contrast, are operations that occur logically after spending and act to restructure the balance sheets of the non-government sector.

To see why, consider the nature of a currency-issuing state’s liability. The state’s money is its own IOU. It is not a pre-existing asset the state can collect, store, and later redeploy. When the state levies a tax, it does not acquire something it can then spend. It extinguishes its own nominal liability (and that of the taxpayer). When it issues a bond, it does not obtain currency to fund expenditure in the same way a firm does when it issues a corporate bond to the market. It offers a longer duration fixed rate version of its own IOU in exchange for an existing demand deposit or reserve balance that already originated from prior state spending.

Thinking of this process as ‘borrowing in order to spend’ is therefore a category error. It is analogous to imagining that an individual could finance their future spending by collecting and hoarding their own handwritten IOUs after others have returned them. Once the IOU is returned to its issuer, it ceases to exist as a spendable object. The piece of paper might still exist, but the actual abstract ‘thing’ that constituted it as ‘money’ no longer does. In exactly the same way, tax payments and bond purchases do not provide the state with a stock of new money to draw upon. They simply alter the quantity and composition of financial assets held by the non-government sector. To the extent that taxes release real resources do taxes enable increased government spending at current prices? Yes, absolutely – that’s what they’re for. But this is conceptually and, importantly, materially different to financing spending from that revenue in a nominal way.

To drive this point home, because it sits at the root of so many persistent misconceptions, it is the act of government spending itself that constitutes ‘borrowing’ in the strict accounting sense. When the state spends, it issues a new monetary liability into the economy. That liability must be accepted and held by someone in the non-government sector in exchange for some real value provided. At that moment, a creditor–debtor relationship is formed, with the state as debtor and the recipient of spending as creditor, ‘lending’ to the state. The public debt stock increases at this point, not at the point of subsequent security issuance. In this sense, sovereign spending entails a form of borrower-imposed borrowing with the state, as monopoly issuer of the currency, unilaterally setting the terms under which its liabilities are issued and held, including the interest to be paid.

The conventional framing, inherited from the commodity view of money, instead treats government borrowing as lender-imposed and as occurring primarily through the sale of bonds to financial markets, which are assumed to discipline the state by dictating terms and interest rates. Once the credit theory of money is taken seriously, this interpretation collapses. Bond issuance does not finance expenditure and does not create new net state liabilities. It merely alters the maturity and interest-rate structure of liabilities that already exist, exchanging overnight, floating-rate monetary IOUs for longer-duration, fixed-rate IOUs. Recognising this distinction is crucial, because the belief that markets ‘fund’ government spending underpins the mistaken view that financial markets possess an ex-ante power over sovereign fiscal capacity, rather than the far more limited role of choosing whether and how to hold liabilities that have already been issued.

Government spending is thus conceptually prior. The currency must be issued before it can be taxed or exchanged for securities. Recognising this sequencing is not a semantic trick1, it follows directly from the ontology of money as state credit, and failure to properly grasp it is responsible for a great deal of confusion in both macroeconomic theory and public debate.

In summary, through the chartalist credit theory, money is a creature of and nominal liability of the state, and its value and use as a medium of exchange comes from the tax obligations that back it, not from the material housing of which a credit IOU often consists. All money represents a credit-debt relationship as Innes and later researchers such as anthropologist David Graeber have shown historically (Graeber, 2011).

Importantly, rather than a neutral veil, money in this view is an active tool of the state that issues it, created when one party (creditor) accepts to hold another’s (debtor) IOU, and its quantity adapts endogenously to the needs of the economy. Indeed, post-Keynesian economists in the 20th century emphasised that in modern economies, money is endogenous, in that the private banking system’s creation of money via loans (and to a large extent the state’s autonomous fiscal policy components) is primarily an emergent factor of private activity. By contrast, the orthodox tradition long viewed the money supply as exogenously determined by central banks and their influence on the ‘fractional reserve’ money multiplier effect on bank loans (Kaluza, 2013).

However, today it is widely acknowledged, even by central banks, that most actual money used in circulation is bank credit, conjured when banks extend loans. For example, the Bank of England plainly explains that “the majority of money in the modern economy is created by commercial banks making loans” (McLeay et al, 2014). This aligns perfectly with the credit theory where your bank deposit is simply the bank’s IOU to you, created alongside your IOU (the loan) to the bank. The entire monetary system can be seen as a hierarchy of IOUs, with the state’s currency (central bank reserves and cash) at the top because it’s the token universally accepted for taxes, effectively the IOU of the state that everyone in the jurisdiction must obtain and is therefore the most readily accepted in exchanges.

It’s important to note that chartalism doesn’t deny that gold or other commodities have historically been used as exchange media in their own right. But these are isolated and limited exceptions and don’t reflect the ontological reality that our modern monetary production economies are predicated on a system of debt-based credit. For sure, commodity backed currencies have been widespread (e.g. the gold and silver standards of the 19th and 20th centuries), but these have always reflected policy choices by state authorities to promise to convert its currency liabilities into them upon redemption. As Stephanie Kelton has written, the metallist vs. chartalist debate was never about whether gold was used, but about why it was used and what underlies its value. The assertion is that taxes are a sufficient but not necessary way to drive demand for and adoption of a state money and that our current monetary production system is indeed predicated on this mechanism. In modern states, taxes are the strongest, most generalised source of demand but other obligations and institutional practices can also reinforce acceptance.

By the mid-20th century, this chartalist understanding was echoed by Abba P. Lerner in his doctrine of ‘functional finance’ which held that “money is a creature of the State” and that the correct role of fiscal policy is not to balance budgets but to ensure full employment and price stability, using taxes and spending as tools to regulate aggregate demand (Lerner, 1943). Lerner famously said government should not think like a household constrained by a scarcity of finance; if there are unemployed resources for sale in the state’s currency, the government can always ‘afford’ to issue new IOUs (spend) to put them to use, and if inflation threatens, it is indicative of the state failing to purchase production at current prices, meaning an excess of spending compared with the capacity of the economy to supply that which is required. This is all premised on the idea that the currency is under sovereign control, not a scarce commodity and is diametrically opposed to any sound money or nominal fiscal rule doctrine.

Having explored these two competing ontologies of money, it is hopefully clear that they are incompatible, and I now want to show that they lead to very different policy conclusions. The reason I have gone into some detail above is because I want to turn now to those implications, and why getting the nature of money ‘right’ is not just an academic exercise but something that has far-reaching effects on the realpolitik of modern-day policymaking and it is something that affects unemployment, inflation, and our responses to economic crises.

The foundational story one believes about money’s nature shapes one’s stance on government budgets, central bank operations, inflation-fighting strategies, and more. It’s like two different lenses on the economy, each internally coherent in its own way, but each prompting a very different set of policies and priorities. These two lenses cannot both be right as they are ontologically divergent and so the rest of this essay argues the credit-state view better fits the institutional facts.

Under the commodity-money view, a government is constrained by finances much like a household or a gold miner. It needs to find money (via taxing or borrowing or digging gold) before it can spend. Large deficits are seen as dangerous signs of fiscal profligacy, risking high inflation or default. Proponents of this view often favour rules to discipline government spending (balanced budget requirements, gold standards, or independent central banks focusing on tight money).

In contrast, the state credit money view shows how a sovereign government that issues its own fiat currency never needs to find its own currency before it can spend – it creates money by spending it. Government budgets, then, are not like household budgets and it is never a useful analogy to employ, even when communicating to the lay public. The constraint on a currency-issuing government is not insolvency in its own money, but inflation and real resource limits. Too much spending relative to the economy’s capacity can cause inflation, of course, but the solution is to manage total spending in the economy (via taxes or other tools) to match the real output available, not to arbitrarily balance budgets or limit deficits as a result of a sound money doctrine derived from a flawed understanding of the nature of money and the role of the state in constituting the monetary system.

In practice, this means a government can run deficits whenever there is slack in the economy (unemployment, under-utilised capital) without worrying about ‘finding the money’. If the government spends more than it taxes, by accounting identity the non-government sector accumulates that much extra currency (a financial surplus). The metallist camp tends to miss this sectoral perspective because it treats money as a finite commodity that moves around, whereas the chartalist camp sees that government deficits are also nominal net private saving by design.

The key policy distinction is that budgeting should focus like a laser on real functional outcomes and available production availability and not focus its analysis on the monetary layer.

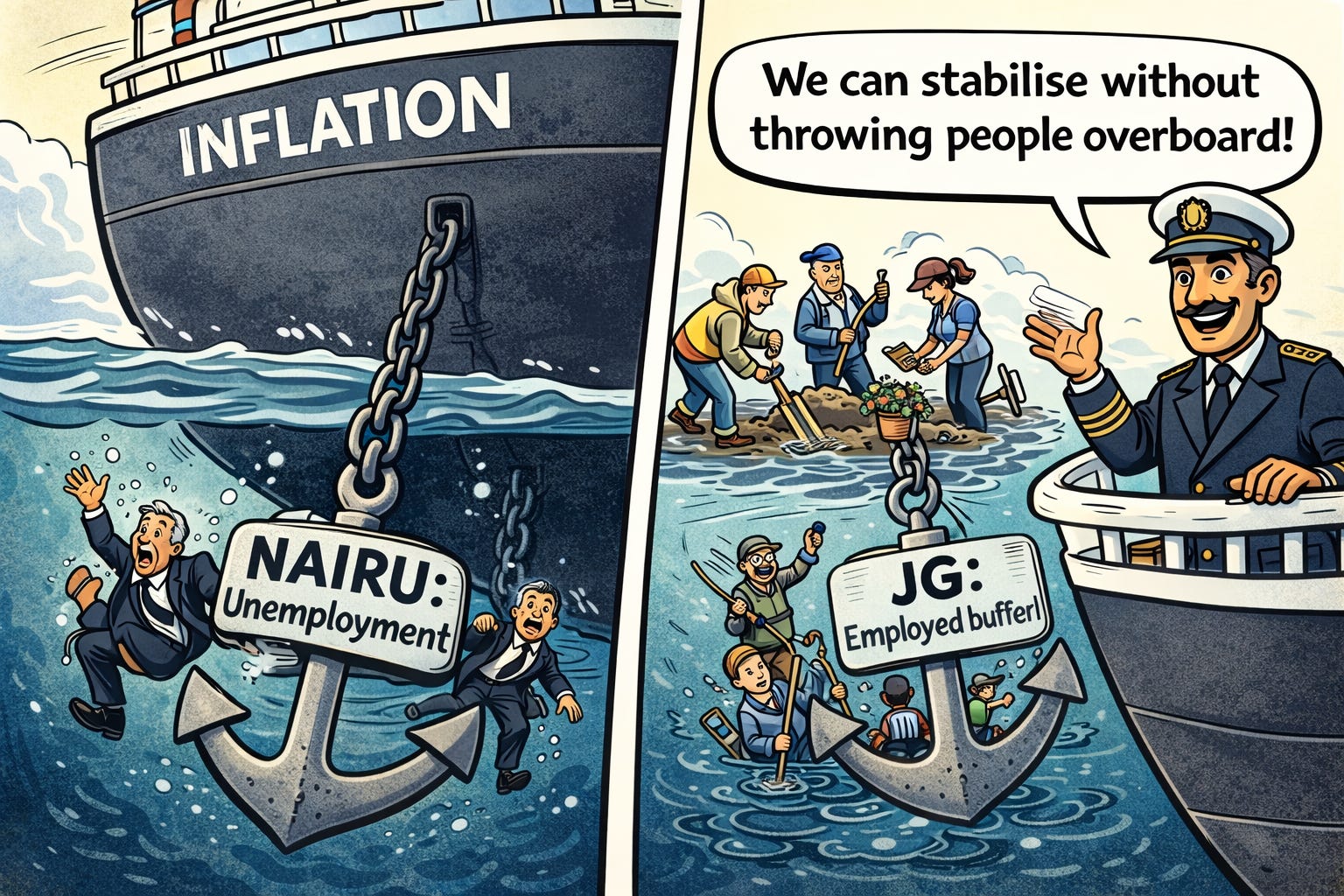

Under mainstream neoclassical frameworks (descending in part from metallism and orthodox monetarism), controlling inflation is often about controlling the money supply or interest rates (monetary policy dominance) and about maintaining a buffer of unemployment to restrain wage demands (the NAIRU concept). If unemployment gets ‘too low’, this view assumes workers will bid wages up and cause inflation; therefore, some slack (people out of work) has been seen as unfortunately necessary to keep prices stable.

This approach can be thought of as using an ‘unemployment buffer stock’ to anchor inflation. As economist Bill Mitchell wryly observes, this became the conventional choice with society using unemployment as the buffer to stabilise prices, accepting joblessness as the trade-off for stable inflation (Mitchell, 2011). Classical economics frames unemployment as a natural consequence of the dynamics between the supply and demand for labour for the process of production and people’s desire for leisure (i.e. there is no involuntary unemployment as a consequence of state policies or lack of demand). In stark contrast, the chartalist/MMT approach, adopting the implications of a state credit theory of money fully, is that not only does equilibrium involuntary unemployment often exist, but that we can achieve price stability without creating the conditions for this to occur at all.

The state, with its coercive broad-based powers of taxation, is the party responsible for monetary unemployment (defined as people looking for but failing to find work paid in the state unit of account). This phenomenon occurs when it fails to provide the credit via its spending to satisfy aggregate demands to settle tax liabilities as well as an endogenously fluctuating desire to net save (Mosler, 2018). Given the state’s imposition of tax obligations and its monopoly over net financial assets, sustained unemployment is ultimately a policy choice, even if proximate causes include private credit/investment cycles and confidence. The state can always absorb labour slack and ensure full monetary employment.

It is therefore ontologically consistent with a state credit view of money to assert that it is the responsibility of the state to ensure all those wishing to work have the opportunity to do so. Involuntary unemployment is a unique feature of our monetary production economies and is not an unavoidable law of nature.

Traditional Keynesian full employment policies recognised the role the state must play in filling a private aggregate demand gap, but one clear interpretation is that they ultimately failed to produce sustainable full employment as they lacked a nominal anchor when oil shocks and incompatible claims on national income in the 1970s produced stagflation (Mitchell, 2013). They sought to boost employment via demand stimulus, often in high-end sectors, public works programmes or the military, directly competing in the labour market and setting the stage for the wage-wage and wage-price spirals that became the undoing of Keynesian macroeconomics in that decade.

A superior approach that coherently connects the state’s capacity for credit issuance with private labour market dynamics is to use a buffer stock of employed labour instead, via a Job Guarantee (JG) Employer of Last Resort (ELR) program. This resolves the issues with Keynesian ‘pump priming’ strategies and produces a powerfully self-stabilising full employment economy. I will not expound on this here but I have written at length on how this works here (Smith, 2025).

Under a commodity money or orthodox view, the central bank is often seen as controlling the money supply and using interest rates to manage economic cycles primarily because fiscal policy is believed to be impotent in the long run due to the money-neutrality principle. Money is treated like a scarce resource obtained from the private sector that the central bank only creates in emergencies. But in reality (acknowledged by heterodox and now most orthodox economists too), central banks set the base policy interest rate but don’t directly control broader money supply. Banks create broad money deposits when they lend if creditworthy borrowers appear, and reserves are supplied on demand by central banks as needed to maintain monetary policy targets and the smooth functioning of the payments and financial systems (Sieroń, 2019).

The MMT framework which fully embraces the chartalist insights of the state credit theory, post-Keynesian endogenous money, and the employment buffer stock stabilisation approach to promote full employment AND price stability takes this further to suggest that the interest rate is a blunt tool and that a sovereign government should, in fact, keep the base interest rate at or near zero, or at the very least at a low fixed nominal value. Some MMT economists (e.g. Warren Mosler) argue that governments should “leave rates at zero” and focus on fiscal policy for stabilisation given the “natural rate is zero” (Mosler & Forstater, 2005). I expand on the reasons why using interest rate adjustments as our primary inflation control method is a poor policy approach here (Smith, 2025).

To illustrate the starkness of the difference, the orthodox paradigm’s reaction to a crisis (say 2008) involves policymakers often reaching first for monetary stimulus (e.g. quantitative easing) and/or a cut in interest rates – because there is an implicit fear of fiscal deficits which underpins austerity economics that flowed out of the GFC. In the MMT paradigm that recognises chartal state credit money, the response would lean more on direct fiscal action. Indeed, in the COVID-19 pandemic, we saw something interesting with governments around the world running enormous deficits to support their economies, and central banks implicitly ‘financing’ a large expansion in spending. Those actions are very different to what the economic discourse after the Global Financial Crisis (GFC) would have allowed, showing a big Overton window shift with regard to macroeconomics since then. Many economists, such as Kelton, have noted that the swift recovery in the US after 2020 (far faster than after the 2008 recession) is due in part to a large fiscal injection unconstrained by inherent deficit worries (Kelton, 2024). In other words, when reality forces their hand, even orthodox policymakers implicitly behave as if the state theory of money holds true.

Finally, there’s a broader philosophical implication. If one accepts the credit state theory, one realises that money is not a neutral, naturally scarce object that stands outside society. It is an institution, a public tool we have designed (consciously or not) to organise production and distribution within our society. We are not bound by some gold-minded deus ex machina forcing us to keep unemployment at 5% or else; we can choose a system where the public purpose (like full employment, public investment, healthcare, green transition) is financed directly by our sovereign currency-issuing capacity as long as they are activities we can collectively physically do. This is empowering but also requires responsibility. Abuse the power (by overspending beyond capacity) and you do get inflation. But crucially, as Lerner said, “government fiscal policy, its spending and taxing, its borrowing and repayment of loans, its issue of new money and its withdrawal of money, shall all be undertaken with an eye only to the results of these actions on the economy and not to any established traditional doctrine about what is sound or unsound” (Lerner, 1943). It shifts the debate from “Can we afford it?” to “Do we have the real resources and what are our collective priorities concerning the distribution of production for private or public purposes?”

On the other hand, if one firmly believes money must be commodity-based or inherently scarce, one might instinctively recoil from policies like large fiscal stimulus, direct job creation by government, or central bank financing of deficits (even if millions are unemployed) because those violate the perceived “natural” constraints on money. That bias in mainstream institutions and orthodox economics has often led to austerity policies which, from the perspective of a state credit money view, are exactly upside down – doing the wrong thing at the wrong time, based on a flawed ontology of the money used in society.

In closing, the contest between these incompatible theories of the origin and ontology of money within today’s monetary economies goes to the heart of debates on economics, on how to tackle unemployment and inflation, and on what role the state should play in shaping the direction of our production systems.

Should we constrain ourselves as if we were still on a gold standard, or leverage the monetary sovereignty we actually have in modern fiat non-convertible money regimes? The answer I propose is that we should do the latter; we should embrace our monetary sovereignty to achieve public purpose. We should act to achieve sustainable price-stable full employment, marshal the vast resources of society for a green transition, and properly guarantee a basic minimum living standard to all our citizens – given that it is materially possible to do so.

The mainstream neoclassical answer, stemming from the metallist view of scarce money tends to be more cautious: stick to the received rules and trust markets and scarcity to discipline policy. History, from the Great Depression to the GFC to the pandemic, has repeatedly shown the costs of the latter approach, when dogmatic fear of deficits or ‘printing money’ delayed needed action and made human suffering worse. As Keynes famously said, “Practical men, who believe themselves to be quite exempt from any intellectual influence, are usually the slaves of some defunct economist” (Keynes, 1936).

In the realm of money, many policymakers have been the unwitting slaves of the defunct barter-metallist view. It’s time, perhaps, for the credit-chartalist perspective, far from new, with roots in centuries of thought from Smith to Innes to Keynes and beyond, to inform a new reality-based understanding of money in the public discourse. If money is understood as it really is as an artifact of institutions and a credit-debt social relationship monopolised by state authorities, then we, through our democratic governments, can shape it to serve us, rather than constraining ourselves to serve it.

Bell, S. (1998). THE HIERARCHY OF MONEY. The Jerome Levy Economics Institute . Retrieved from https://www.levyinstitute.org/wp-content/uploads/2024/02/wp231.pdf#:~:text=Exchange%2C%20it%20is%20argued%2C%20was,which%20was%20offered%20by%20another

Berkeley, A., Ryan-Collins, J., Tye, R., Voldsgaard, A., & Wilson, N. (2025). The Self-Financing State: An Institutional Analysis of Government Expenditure, Revenue Collection and Debt Issuance Operations in the United Kingdom. Journal of Economic Issues, 59, 3. Received from https://www.tandfonline.com/doi/full/10.1080/00213624.2025.2533726

Graeber, D. (2011). Debt: The First 5000 Years.

Innes, A. M. (1913). What is Money? Banking Law Journal, 17-18. Retrieved from https://cooperative-individualism.org/innes-a-mitchell_what-is-money-1913-may.pdf

Kaluza, L. (2013). Essays in Monetary Theory and Policy: On the Nature of Money. New Economics Perspective. Retrieved 2026, from https://neweconomicperspectives.org/2013/12/essays-monetary-theory-policy-nature-money-9.html#:~:text=orthodox%20approach%2C%20the%20money%20supply,endogenously%20determined%20within%20the%20system

Kelton, S. (2024, March). MMT sees America through rapid economic recovery. Independent Australia. Retrieved January 2026, from https://independentaustralia.net/politics/politics-display/mmt-sees-america-through-rapid-economic-recovery,18395#:~:text=The%20fiscal%20packages%20have%20been,or%20MMT

Keynes, J. M. (1930). A Treatise on Money. Cambridge. Retrieved from https://archive.org/details/in.ernet.dli.2015.45480

Keynes, J. M. (1936). The General Theory of Employment, Interest, and Money. Cambridge: Macmillan. Retrieved from https://www.files.ethz.ch/isn/125515/1366_keynestheoryofemployment.pdf

Knapp, G. F. (1905). The State Theory of Money. Retrieved from https://historyofeconomicthought.mcmaster.ca/knapp/StateTheoryMoney.pdf

Lerner, A. P. (1943). Functional Finance and the Federal Debt. Social Research. Retrieved from https://www.jstor.org/stable/40981939

McLeay, M., Radia, A., & Thomas, R. (2014). Money creation in the modern economy. Bank of England, Monetary Analysis Directorate. London: Bank of England. Retrieved from https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creation-in-the-modern-economy#:~:text=England%20www,by%20commercial%20banks%20making%20loans

Menger, C. (1892). On the Origins of Money. Economic Journal, 2, 239-255. Retrieved from https://cdn.mises.org/On%20the%20Origins%20of%20Money_5.pdf#:~:text=Power%20Money%20has%20not%20been,evolving%20commerce%2C%20just%20as%20customary

Minksy, H. (1986). Stabilizing an Unstable Economy. Retrieved from http://digamo.free.fr/minsky86.pdf

Mises, L. v. (1912). The Theory of Money and Credit. Retrieved from https://cdn.mises.org/Theory%20of%20Money%20and%20Credit.pdf

Mitchell, B. (2013). Buffer Stocks and Price Stability. William Mitchel - Modern Monetary Theory. Retrieved from https://billmitchell.org/blog/?p=24063

Mitchell, B. (2013). Whatever – its either employment or unemployment buffer stocks. William Mitchell - Modern Monetary Theory. Retrieved from https://billmitchell.org/blog/?p=17564#:~:text=But%20in%20the%20development%20of,a%20buffer%20stock%20was%20present

Mosler, W. (2018). Full Employment AND Price Stability. Retrieved from https://moslereconomics.com/wp-content/uploads/2019/02/Full-Employment-AND-Price-Stability.pdf

Mosler, W. (2024). The General Theory of Value. Retrieved from https://moslereconomics.com/wp-content/uploads/2024/12/The-General-Theory-of-Value-12-25-2024.pdf

Mosler, W., & Forstater, M. (2005). The Natural Rate of Interest Is Zero. Journal of Economic Issues, XXXIX(2). Retrieved from https://moslereconomics.com/wp-content/uploads/2018/04/The-Natural-Rate-of-Interest-is-Zero.pdf

Sieroń, A. (2019). Endogenous versus exogenous money: Does the debate really matter? Research in Economics, 73(4), 329-338. Retrieved from https://www.sciencedirect.com/science/article/pii/S1090944319303606

Smith, A. (1776). Chapter IV: OF THE ORIGIN AND USE OF MONEY. In The Wealth of Nations (pp. 25-27, 268). Retrieved from https://www.rrojasdatabank.info/Wealth-Nations.pdf

Smith, J. (2025). Why interest rates are a terrible tool for controlling inflation. Substack. Retrieved from https://jgs952.substack.com/p/why-interest-rates-are-a-terrible?r=m17ra

Smith, J. (2025). Zero-Interest Rates, Job Guarantee, and MMT in the UK. Substack. Retrieved from https://jgs952.substack.com/p/zero-interest-rates-job-guarantee?r=m17ra