A note before you read: This essay reflects my personal research and views, based entirely on publicly available sources. It is not connected to any client work or professional engagement, and it does not represent the views of any organization I am affiliated with. Nothing here should be read as a critique of any specific company or individual. The insurance system is complex, and the professionals who work within it operate within structures they did not design. This essay is about structural economics and emerging consumer alternatives, not about fault. It is intended as general information only and does not constitute medical, legal, tax, or financial advice. Verify current rules and consult appropriate professionals before making decisions that affect your family’s health coverage.

Healthcare in America is not one product. It has never been one product. There are many products: primary care, catastrophic protection, prescriptions, dental, vision and mental health. All sold under one name, by one set of intermediaries, at one difficult-to-understand price. The bundle exists for reasons that made historical sense and that continue to serve certain purposes well. But it was assembled around institutional economics as much as patient need, and that tension has real consequences for the families paying for it.

The families who have started to take the bundle apart are discovering something that has not been widely explained to them: that some of the pieces, on closer inspection, are not worth what they cost; that others can be had for far less; and that a few can be had for nothing at all.

This essay is about what happens when you take the bundle apart, and why, in 2026, the conditions to do so have never been better.

What follows is, on its surface, a practical guide. But underneath the numbers and the case studies, it is something else: an account of what ordinary people do when institutions stop serving them well. American healthcare did not fail suddenly or dramatically. It evolved in the way that many institutions fail, gradually and at the edges, in ways that were individually tolerable until, for many families, they were not. The families assembling alternatives are not revolutionaries. They are pragmatists, doing what people have always done when the system they relied on stops working: building something in its place. That quiet act of construction is worth understanding, both for what it saves and for what it reveals about the relationship between institutions and the people they were designed to serve.

Consider, for a moment, the strange thing that happens when an American visits a primary care physician. The visit is fifteen minutes. The physician, who manages a panel of 2,500 or more patients, has perhaps glanced at the chart on the way into the room. The conversation is constrained by what insurance will reimburse and what the next patient’s appointment requires. The physician does not call back. There is a portal that routes messages through staff. The next visit is six weeks away.

This is not the fault of the physician. It is the structural reality of a payment system in which insurance dictates what counts as a billable visit, how long it can last, and how much can be reimbursed. The result is that primary care, which is supposed to be the relational, longitudinal heart of medical practice, has become its most rushed and least personal layer. Most patients have come to accept this as the nature of the thing. It is not. Neither, it turns out, have all physicians.

There is a different kind of arrangement, and it has been growing for two decades. It is called Direct Primary Care, and the model is straightforward. A patient pays a flat monthly fee, typically between $75 and $150 per adult, directly to a physician. The fee buys unlimited visits, longer appointments (thirty to sixty minutes is standard), direct access to the physician by phone, text, or email, and laboratory work at wholesale prices. There is no insurance involvement because insurance has been deliberately moved to where it makes sense in the equation.

The economics work because the physician’s overhead collapses when insurance is removed. A typical primary care practice spends roughly forty cents of every dollar billed on the administrative apparatus of dealing with insurance: coders, billers, prior authorization specialists, and denial appeals. The DPC physician spends none of that. The result is that a panel of six to eight hundred patients paying directly generates more revenue per physician than a panel of twenty-five hundred patients billed through insurance and produces a fundamentally different experience of care for both patient and physician.

According to Hint Health’s 2026 Direct Primary Care Trends Report, the most comprehensive industry analysis to date, there are now more than 2,700 DPC clinicians practicing across 49 states, serving more than 1.4 million members. DPC Frontier’s practice mapper lists more than 1,300 distinct practices nationwide. DPC membership expanded by 837% from 2017 to 2025, significantly outpacing U.S. population growth over the same period.

What makes this development newly important is that, as of January 1, 2026, the federal tax code now treats Direct Primary Care as a qualified medical expense. A family can pay up to $300 a month in DPC fees from a Health Savings Account, tax-free, while simultaneously holding a high-deductible insurance plan that handles catastrophic events. Bronze and Catastrophic plans on the federal marketplace, the cheapest available, are now HSA-compatible. The combination, until recently a regulatory tangle, is now blessed by federal statute. This is the architecture of what we will call, throughout this essay, the hybrid stack.

The way to understand the hybrid stack is to recognize that healthcare, despite being sold as a single product, is, in fact, a series of layers, each with its own economics. The mistake of the American insurance system, broadly speaking, is to charge a single premium for all of them and to extract its margin from the spread between what it pays for each and what it charges in aggregate. The opportunity for the family is to see the layers separately and to source each one from the seller best suited to provide it.

There are seven such layers, and each behaves differently. Catastrophic protection, the first, is what insurance was originally designed for: the ER visit, the cancer diagnosis, the major surgery, the ICU admission, the prescription drug that costs ten thousand dollars a month. The economics of insurance work for these events because they are rare, expensive, and impossible to predict; the only sensible response is to pool risk across many people. This layer remains, and will remain, the province of real, contractually binding insurance.

The second layer is primary care, which we have already addressed. The third is specialty and surgical care, where the picture is more situation-dependent. For a family with frequent, expensive specialty needs, comprehensive insurance is genuinely protective. For a family with predictable, occasional needs, cash-pay arrangements at transparent-pricing facilities can dramatically beat insurance-negotiated rates after the deductible. The Surgery Center of Oklahoma, in Oklahoma City, has become a national resource for the second category: it publishes its prices, and 40 percent of its patients now travel from out of state to use its services. A laparoscopic gallbladder removal is posted at $6,836, all in (per surgerycenterok.com, May 2026). A breast biopsy costs $1,900, according to a December 2025 profile in Medical Economics. The same procedures at a typical hospital can run three to ten times as much.

The fourth layer is prescriptions, where the picture has shifted dramatically in the last few years. Mark Cuban’s Cost Plus Drugs, founded in 2022 as a public benefit corporation, now lists more than 2,000 medications at acquisition cost plus a 15 percent markup and a $5 pharmacy fee. Amazon’s RxPass, for $5 a month with a Prime membership, covers eligible medications on the RxPass formulary, currently including more than 50 common generics. GoodRx compares cash prices across tens of thousands of pharmacies and often finds prices below the insurance copay. For most common chronic-disease medications, including those for hypertension, hypothyroidism, type 2 diabetes, and depression, the cheapest source is now outside insurance entirely, and the savings can be substantial even for the well-insured.

The fifth and sixth layers, dental and vision, are perhaps the clearest cases where insurance has outlived its purpose. Annual dental benefit caps of one to two thousand dollars mean that a single root canal can hit the limit. Practice membership plans, in which a family pays the dentist directly for cleanings, X-rays, and discounts on additional work, typically run $30 to $40 per adult per month and beat traditional dental insurance for most families. Vision is similar: Costco Optical, Warby Parker, and online retailers have made eyewear genuinely cheap, and a routine eye exam, paid for out of pocket, is usually less than $150. The arithmetic of dental and vision insurance no longer holds up for most people.

The seventh layer, mental health, is the weakest of all under the traditional insurance model. Networks are narrow. Wait times are long. Many of the best therapists do not take insurance at all. Direct-pay therapy, sliding-scale platforms like Open Path Collective, and the willingness of DPC physicians to handle the medication-management portion of routine mental health care have, for many families, produced better access and better outcomes than what insurance can deliver.

For most families, that combination begins with a high-deductible Bronze plan for the catastrophic layer, adds a Direct Primary Care membership for the primary layer, uses cash-pay arrangements for predictable specialty care, sources prescriptions entirely outside insurance, and replaces dental and vision insurance with direct relationships. The savings for a typical middle-income family can run from $5,000 to $20,000 a year, depending on state, age, and health status. The quality of day-to-day care, by most measures studied, improves.

A caveat is in order here, and it is not a small one. In the American healthcare landscape, there exists a category of arrangement that markets itself as an alternative to insurance, costs less than insurance, and is not insurance: the health-sharing ministry. The names are familiar to anyone who has listened to Christian radio or browsed alternative-medicine websites: MediShare, Christian Healthcare Ministries, Samaritan, Sedera, Liberty HealthShare. Their marketing is polished, their rhetoric carefully appealing, and their defining structural feature is this: they have no contractual obligation to pay any member’s medical bills.

The membership documents say so, in language reviewed by lawyers. Approximately 30 states have passed safe-harbor laws that exempt these arrangements from insurance regulation entirely. Federal law treats them as exempt from the Affordable Care Act’s requirements. They are voluntary cost-sharing arrangements, a phrase that should be read with the emphasis on voluntary.

The risk is not theoretical. Sharity Ministries, formerly Trinity HealthShare, administered by Aliera Healthcare, filed for bankruptcy in 2021. Court documents filed during the liquidation process showed over $300 million in unpaid member claims. State regulators warned members that recovery would likely be a fraction of the total, according to statements from the New Hampshire Insurance Department.

Liberty HealthShare, the subject of a 2023 ProPublica investigation, was found to have used $140 million of $300 million in member fees over a seven-year period to fund businesses affiliated with its leadership, including a boutique airline, a marijuana farm, real estate, and carpet stores, while members’ bills went unpaid. Medical Cost Sharing Inc., whose assets were seized by the Justice Department in the same year, had collected $8 million in revenue and used approximately 3 percent of it to pay medical claims, according to DOJ prosecutors.

The state of Colorado alone among American states requires health sharing ministries to publicly disclose their financial data. The most recent disclosure, for 2023, found that of the $96 million in member medical costs submitted, only $34 million was actually paid. The rest was either deemed ineligible under various exclusions or simply not paid. This was Colorado, the regulated state. The unregulated states have no comparable data, and what we know suggests that what we do not know is worse.

The savings are bounded. The downside is unbounded.

Health sharing ministries are excluded from the framework presented in this essay, and the exclusion is principled. The savings, compared to insurance, are real but bounded: five to ten thousand dollars a year for a family. The downside is unbounded. An $80,000 surgery was denied as a pre-existing condition. A $200,000 cancer treatment was denied because the diagnosis came within an exclusion window. A ministry that simply collapses, leaving the member with no recourse and no contract to enforce. Insurance is contractually required to pay covered claims; health sharing is not. Direct Primary Care memberships are contractually required to deliver the services paid for. Cash-pay arrangements are contracts per transaction. Health sharing arrangements, by their own legal documents, are not contracts at all.

The marketing is most aggressive toward the families who can least afford a catastrophic denial. For families in financially fragile positions, for families with chronic conditions, for families considering this arrangement during pregnancy, the asymmetric risk is exactly the wrong shape. That is not a coincidence. Everything that follows in this essay relies on contractually binding cost models. Families should insist on the same.

Two regulatory developments shape the landscape families now face, pulling in opposite directions. The first, which took effect on January 1, 2026, made traditional comprehensive insurance significantly more expensive for many families. The second made the hybrid stack significantly cheaper. Together, they have created a moment in which the rational answer to the cost of American healthcare is, for many families, no longer the answer most Americans currently give.

The first development is the return of the subsidy cliff. From 2021 through 2025, under the American Rescue Plan and the Inflation Reduction Act, the Affordable Care Act’s premium tax credits were temporarily expanded to cap household premium contributions at 8.5 percent of income for everyone. Those enhanced subsidies expired on December 31, 2025. The original ACA rules, which limit subsidies to families earning below 400 percent of the federal poverty level, were reinstated. The 400 percent threshold in 2026 is approximately $62,600 for a single person, $84,600 for a two-person household, and $128,600 for a family of four (figures differ in Alaska and Hawaii). Earning a single dollar above the threshold strips all subsidies, not just a portion. The cliff is binary and brutal.

The result, for families above the threshold, is sticker shock. A sixty-year-old couple who paid a few hundred dollars a month under the enhanced subsidies in 2025 now pays $2,000 a month for the same plan in 2026. The friend whose situation prompted this essay, a middle-aged man considering early retirement, was quoted $1,700 a month for marketplace insurance for himself and his wife. He had not retired in haste. He had calculated, carefully, what his savings could support. The healthcare line item changed the calculation.

The second development, which took effect the same day, is the One Big Beautiful Bill Act. The law, signed on July 4, 2025, made three structural changes that, taken together, amount to federal validation of the hybrid stack. Bronze and Catastrophic ACA plans, the cheapest available, are now Health Savings Account compatible regardless of their deductibles. Direct Primary Care memberships no longer disqualify HSA contributions, up to $150 per month for individuals and $300 per month for families. And HSA dollars can now pay DPC fees tax-free, within the same limits.

The combination is more important than either piece alone. A family can now hold a low-premium catastrophic insurance plan, fund a Health Savings Account up to $8,750 a year (plus a $1,000 catch-up if either spouse is fifty-five or older), pay their Direct Primary Care fees from that account, and use the remainder for their out-of-pocket medical expenses. The entire arrangement is constructed from contractually binding pieces and tax-advantaged at every step. The federal government has, almost without anyone noticing, blessed an architecture that existed at the margins of the healthcare system for two decades. The architecture is now ordinary tax law.

This convergence (the cliff and the validation) arrives at a moment when the underlying infrastructure has matured. The Direct Primary Care movement has crossed the threshold from niche to general availability. Cash-pay surgical centers exist in most regions of the country. Cost Plus Drugs and Amazon RxPass have made cash-pay prescriptions a viable strategy for the first time in decades. A family making this transition in 2020 would have had to assemble the pieces from scratch and might not have found them. A family making this transition in 2026 has a fully developed alternative ecosystem to draw on. The system has not been fixed. But the workaround has matured, the pieces are in place, and the cases that follow show what it looks like when a family builds it.

A common objection to the hybrid stack is that it cannot work for families with chronic conditions, and this objection deserves to be taken seriously and, with some care, refined. The objection is correct in a narrow sense and wrong in a broader one, and the distinction matters for a great many American families.

The chronic conditions for which the hybrid stack does not work well are a small and specific set: active cancer treatment, end-stage renal disease requiring dialysis, conditions requiring infused medications that cost $10,000 a month or more, transplant patients on lifelong immunosuppressants, advanced heart failure requiring frequent specialist intervention, and active inflammatory bowel disease requiring biologics. These are conditions in which the family is hitting the deductible and out-of-pocket maximum every year, and in which the predictable cost-sharing of comprehensive insurance is genuinely worth more than the higher premium.

But the great majority of what is called chronic disease in America is not in this category. Type 2 diabetes managed with metformin, the first-line drug, costs about $4 a month from Cost Plus. Hypertension on a generic ACE inhibitor or ARB costs pennies. Hypothyroidism on generic levothyroxine costs $5 to $15 a month. Most autoimmune conditions on stable maintenance therapy, most well-managed asthma, most cases of GERD, depression, anxiety, fibromyalgia, and migraine are routinely managed with generic medications that cost almost nothing, and benefit dramatically from the time-rich, relational care that DPC provides and that fee-for-service insurance, with its fifteen-minute appointments, structurally cannot.

Multiple sclerosis is a useful example because it sits in the middle. The medications for MS can be expensive, but for many patients with stable disease, the relevant care consists of an annual or semiannual visit with a neurologist who knows the patient’s history, periodic MRI scans to monitor disease activity, and management of any associated symptoms. The neurologist relationship, for a family with the means, can be a concierge arrangement at a cost of $125 to $200 a month, which delivers continuity and access that no insurance network can match. MRI imaging can be obtained either through insurance (after the deductible has been met) or at an independent imaging center for cash (at a cost of $400 to $700, rather than the $2,000 to $5,000 a hospital system charges). The family chooses, each time, whichever path makes more sense for that scan.

The dividing line is not chronic versus not-chronic. It is the acuity and frequency of expensive specialty intervention.

The principle, then, is not that families with any chronic condition should remain in comprehensive insurance, but that families whose conditions involve frequent and expensive specialty interventions should. The rest can use the hybrid stack, often more effectively than traditional insurance, because the time-rich primary care DPC provides is exactly what chronic disease management requires. Published studies of DPC outcomes have found associations between DPC membership and improved chronic disease management, including better blood pressure and diabetes control, lower hospitalization rates, and lower emergency room utilization compared with matched cohorts. The structural reason is not difficult to identify: DPC physicians have time to think about their patients, and patients have access to that thinking.

What does this look like in the life of an actual family? The arithmetic of the hybrid stack is most easily understood through specific cases. What follows is a short tour of the most common situations in which an American family currently finds itself, with the numbers for each. The cases are constructed, but the numbers reflect 2026 marketplace pricing, current Direct Primary Care fees, and the federal regulatory environment now in effect. They are illustrative estimates; actual costs vary by state, age, health status, and plan selection. Consult a licensed insurance broker, tax advisor, or financial planner before making coverage decisions.

A Family of Four, Below the Cliff

Consider a family of four in Denver with a household income of $95,000. Two parents in their early forties, two children aged eight and eleven, all generally healthy. The Denver family qualifies for premium tax credits because their income is below the 400 percent threshold for a family of four ($128,600 in 2026).

Under the hybrid stack, they purchase a Bronze ACA plan that costs about $4,400 a year after subsidies and pay $3,000 a year ($250 a month) for a family DPC membership. They contribute the maximum to a Health Savings Account, which yields about $2,000 in federal tax savings in their bracket. They purchase a family dental membership for about $1,000, get their glasses at Costco, and order their occasional prescriptions through Cost Plus Drugs.

The savings are modest, less than $3,000 a year, but the more significant difference is in the experience of care. The children have a pediatrician they can see the same day for an ear infection. The parents have a physician who answers texts. No one is rushed through a fifteen-minute appointment. For a family below the cliff, the financial case for the hybrid stack is real but moderate. The case on quality grounds is strong.

A Family of Four, Above the Cliff

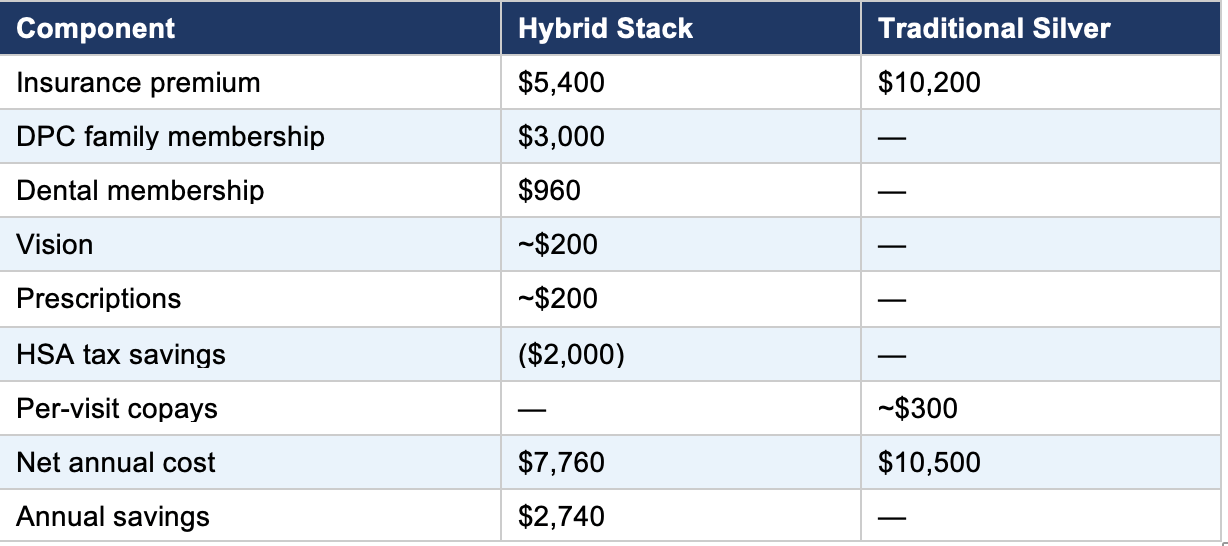

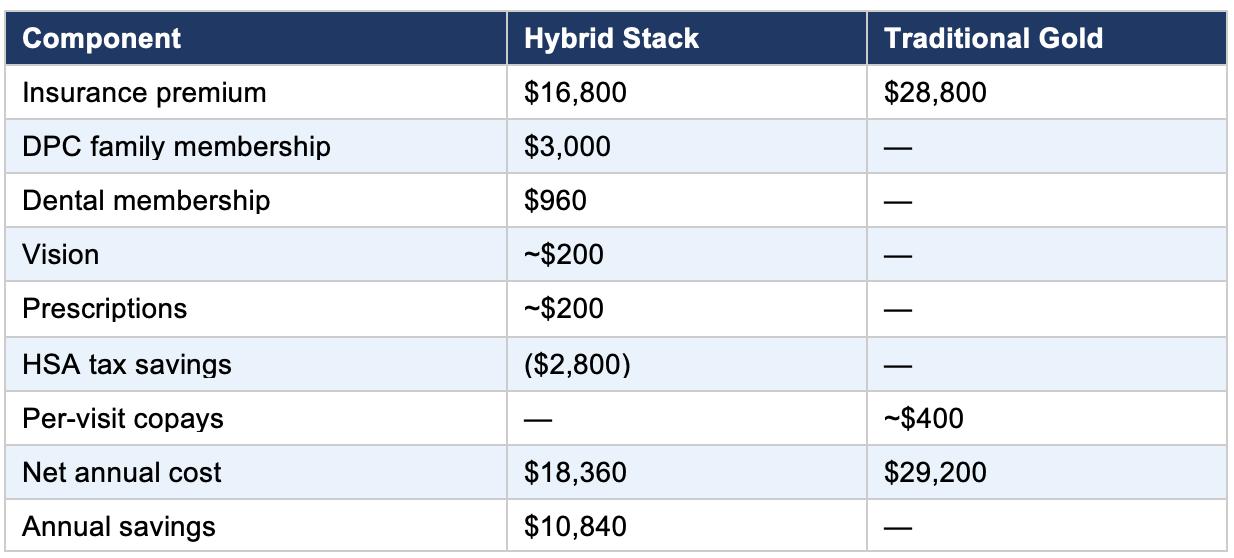

Consider the same family, transplanted to Austin, with a household income of $165,000. They are above the cliff and ineligible for any subsidy. The marketplace quote for a Silver plan is $2,400 a month, or $28,800 a year. The Bronze plan is $1,400 per month ($16,800 per year) and is now HSA-compatible.

Under the hybrid stack, the Austin family pays the Bronze premium, the same DPC fee as the Denver family, and the same dental, vision, and prescription costs. The HSA tax savings in the higher bracket are about $2,800 per year.

The savings now exceed $10,000 a year, in addition to the qualitative benefits. For families above the cliff, the hybrid stack is no longer a luxury or a curiosity. It is the rational response to a pricing structure that has become punitive at the top end.

A Married Couple, Below the Cliff

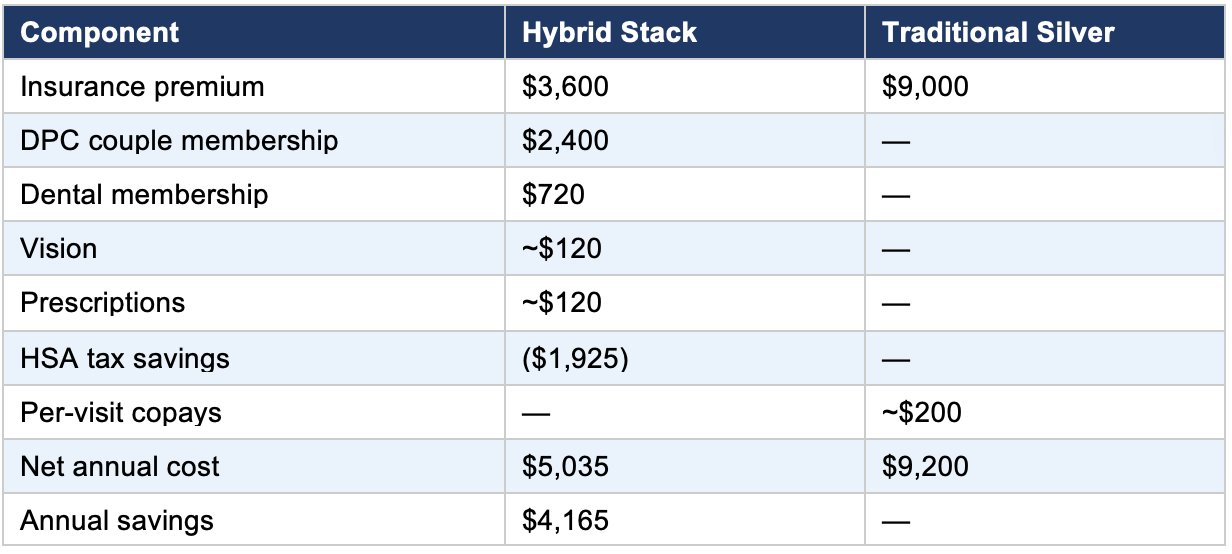

Consider a married couple in Raleigh, both 47, with a household income of $72,000. One spouse manages mild hypothyroidism, well-controlled, on generic levothyroxine. They are below the $84,600 cliff for a household of two. After subsidies, their Bronze plan runs $300 a month, $3,600 a year. A couple’s DPC membership runs $2,400 a year. Their HSA tax savings are about $1,900. Levothyroxine is $15 per month from Cost Plus.

Four thousand dollars a year, plus a physician who answers their texts. Hypothyroidism is exactly the sort of chronic condition that the hybrid stack handles well: cheap medication, simple monitoring, and care that rewards the kind of unhurried relationship a DPC physician can actually provide.

A Married Couple, Above the Cliff

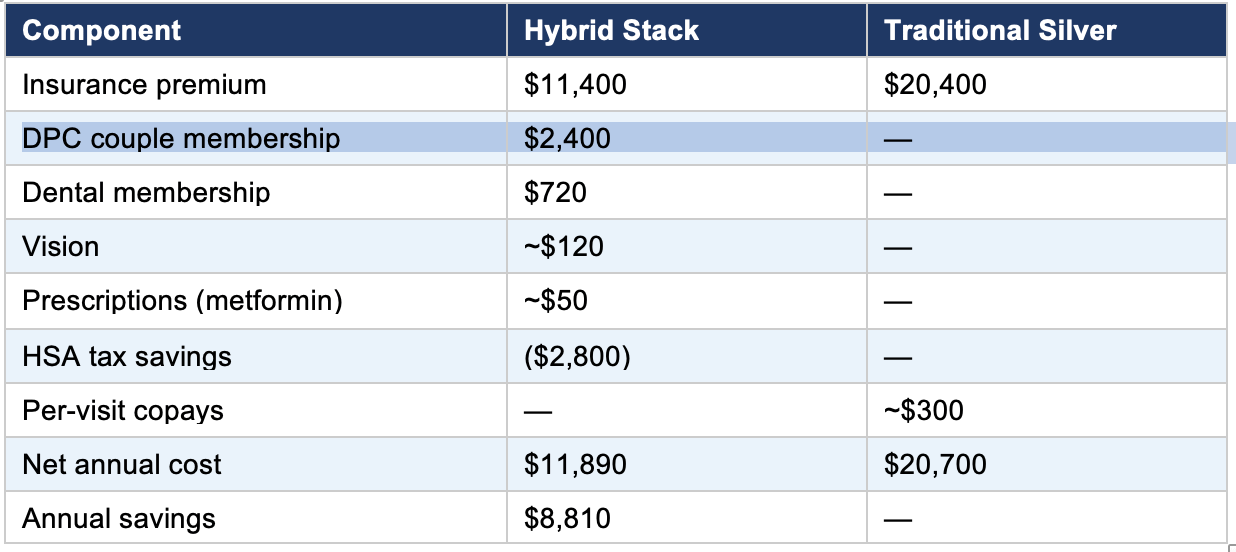

Consider the same couple, transplanted to Nashville, with a household income of $135,000. One spouse has well-controlled type 2 diabetes, managed with metformin and lifestyle. They are above the cliff. The unsubsidized Bronze plan runs $11,400 a year; the Silver plan, $20,400.

Type 2 diabetes is the model case for what the hybrid stack does well. The DPC physician has time to discuss diet, exercise, and medication during unhurried quarterly visits. Lab work is wholesale. Metformin is essentially free. And the spouse managing the condition has, for the first time in years, a physician who knows them well enough to notice when something has changed.

The case that motivated this essay, the friend who calculated his retirement and then was shocked by the marketplace quote, deserves its own treatment. He is fifty-five years old. His wife is on his insurance. They have no children at home. They have enough money to support themselves for two to three years without working, which was the plan. The healthcare line item, at $1,700 per month, is the one threatening it.

He is, in this, an entirely typical case. There are millions of Americans in his situation: the cohort between the end of employer coverage and the beginning of Medicare. The cohort has a name in the actuarial literature: the pre-Medicare bridge. What used to be a manageable few years has become, with the return of the subsidy cliff, the most expensive segment of the American healthcare market. ACA premiums are age-rated, which means a sixty-year-old pays roughly twice as much as a thirty-year-old for the same plan, and a sixty-four-year-old pays three times as much. Without subsidies, an unsubsidized Silver plan for a couple in their early sixties now costs $25,000 to $30,000 per year. At a four percent safe withdrawal rate, that single line item requires six to seven hundred fifty thousand dollars in additional portfolio value before any other expense.

This has derailed more early retirements than any other expense. Only 17 percent of large employers still offer retiree health benefits, down from a generation ago when this was standard. For the 83 percent of pre-Medicare retirees without employer-sponsored continuation coverage, the bridge is on you.

But the bridge, looked at the right way, is also where the hybrid stack delivers its most dramatic results. The reason is that pre-Medicare retirees, particularly those with significant assets, often have unusual flexibility in how they generate taxable income. ACA subsidies are based on Modified Adjusted Gross Income, not on assets. A couple with one and a half million dollars in retirement savings can structure their drawdowns to show a Modified Adjusted Gross Income of $75,000 by drawing primarily from Roth IRAs (where return of contributions does not count as income) and taxable accounts (where return of capital is not income and capital gains can be timed). The same couple, if they take the same dollar amount from a traditional IRA, would show $110,000 in MAGI and lose all subsidies. The difference, in subsidy alone, is $15,000 to $20,000 a year. Over a five-year bridge to Medicare, the difference is $75,000 to $100,000.

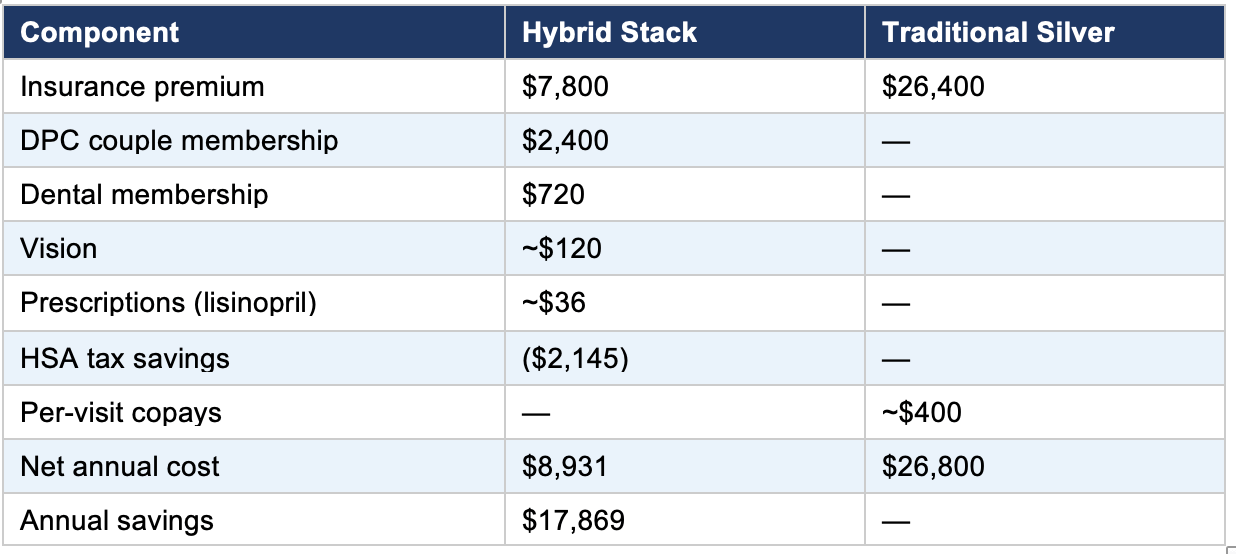

Consider a couple in San Antonio, both sixty, retired with a million and a half dollars in savings split among a traditional IRA, a Roth IRA, and taxable accounts. They manage their MAGI to $75,000 by drawing primarily from the Roth and the taxable account. One spouse has mild hypertension on generic lisinopril. They are otherwise healthy.

Their stack: a Bronze ACA plan, after subsidies, at $7,800 per year. A DPC couple membership at $2,400. Maximum HSA contributions, including catch-up, with about $2,145 in tax savings. Lisinopril at $3 a month.

Eighteen thousand dollars a year, against a Silver plan, for the same couple. Over the five years until they reach Medicare, that is $90,000. The bridge, instead of consuming the retirement, becomes manageable. The plan that had been derailed gets back on track.

The same couple, if their income is fixed by a defined-benefit pension and cannot be managed below the cliff, still does considerably better with the hybrid stack than with traditional Silver, though the gap is narrower: about $12,000 a year rather than $18,000. For pre-Medicare retirees, the income management opportunity is the central financial decision of the bridge years, and it is one that traditional financial planning has only recently begun to address. The hybrid stack, combined with thoughtful drawdown sequencing, transforms what was an existential threat to early retirement into a solvable problem.

Geography matters in this story, and matters in ways that are not always obvious. The hybrid stack works everywhere in principle, but it works best in particular places, and the variation among states is wide enough that it can be the difference between a straightforward strategy and one that requires real effort to assemble.

Three dimensions matter. The first is the cost and competitiveness of the state’s ACA marketplace, which varies by a factor of three or more across states for the same person. The second is the density of Direct Primary Care practices, which is now substantial in some states and still thin in others. The third is the state regulatory environment, which determines whether DPC can operate without bureaucratic friction and whether transparent-pricing facilities are available nearby.

Combining these factors produces a rough geography of the hybrid stack. Texas, Florida, Colorado, and Tennessee form a tier of states with strong infrastructure across all three dimensions: DPC-friendly state laws, growing DPC density, transparent-pricing surgery centers, and multiple ACA carriers competing in the marketplace. Three of the four have no state income tax, which compounds the HSA advantage. A second tier, including Minnesota, North Carolina, Arizona, Utah, Georgia, Indiana, Michigan, Kentucky, Louisiana, Mississippi, Missouri, Oklahoma, South Dakota, and Wyoming, has DPC laws on the books and growing density, with workable ACA markets. Oklahoma, in particular, is home to the Surgery Center of Oklahoma, which functions as a national resource.

A third tier, the populous coastal and industrial states, presents a more mixed picture. California has the most DPC clinicians in absolute numbers, but also the most restrictive regulatory environment and the highest costs. New York, Illinois, Massachusetts, and similar states have a growing DPC presence but high overall costs and more restrictive rules on alternative arrangements. A fourth tier, comprising West Virginia, Vermont, Hawaii, and Alaska, presents real challenges: high ACA premiums, limited DPC density, and regulatory environments that offer little room for alternative arrangements.

As of 2025, 34 states have enacted laws that generally define Direct Primary Care as a medical service rather than insurance, according to the Direct Primary Care Coalition. The list includes most of the South, much of the Mountain West, and a scattering of states elsewhere. The states without specific DPC laws still allow the model to operate under general medical practice rules; the legislation matters for legal clarity rather than as a strict precondition.

For families in Tier IV states with the flexibility to relocate, the financial case for moving can be substantial: $10,000 to $20,000 a year in healthcare cost differences alone for some couples. This does not justify uprooting a family for healthcare reasons in isolation, but for families already considering a move, whether for early retirement, remote work, or any of the other reasons American life is increasingly portable, the healthcare ecosystem deserves to be a serious factor in state selection. It rarely is. It should be.

An honest essay about a strategy must include the cases in which the strategy does not apply, and the hybrid stack has its honest limitations. There are families for whom traditional comprehensive insurance is genuinely the better answer, and the framework is not improved by pretending otherwise.

The clearest case is the family with a high-acuity condition: active cancer treatment, dialysis, expensive infused medications, transplant immunosuppression, and advanced heart failure. For these families, the out-of-pocket maximum protection of comprehensive insurance is genuinely valuable, and the higher premium is offset by predictable cost-sharing during periods of heavy utilization.

A second case is the family whose employer offers heavily subsidized coverage, typically covering 70 to 80 percent of premiums. The math of an individually built hybrid stack rarely beats well-subsidized employer coverage on cost alone, though families in this situation can often add a DPC membership as a complement.

A third case is the risk-averse family that simply prefers the predictability of comprehensive coverage to the variance of high-deductible plans. There is nothing wrong with this preference, as long as it is conscious. Comprehensive insurance trades a higher monthly cost for lower variance. Some families value the trade. Either choice is defensible if it is made deliberately.

A fourth case is geographic: families in regions where Direct Primary Care simply is not yet available within a reasonable distance. A practice locator is listed in the resources at the end of this essay.

A fifth case is a near-term family-planning pregnancy. ACA-compliant plans must cover maternity care without waiting periods, but the deductible exposure on a Bronze plan can be substantial during a year of pregnancy and delivery. For families planning a pregnancy, a Silver plan with a lower deductible during the relevant year often makes sense, returning to Bronze once the family is past the high-utilization period.

A final case is the family without the financial cushion to absorb the higher deductible if a major event occurs. Under HSA-qualified HDHP rules for 2026, out-of-pocket maximums can reach $8,500 for an individual or $17,000 for a family (per IRS Revenue Procedure 2025-19). If emergency savings cannot support that exposure, a lower-deductible plan provides important protection even at a higher monthly cost.

What unifies these exceptions is that each represents a situation in which one of the assumptions of the hybrid stack does not hold: the assumption of moderate medical needs, the assumption of unsubsidized individual market exposure, the assumption of a tolerance for variance, the assumption of geographic access, the assumption of timing flexibility, and the assumption of financial cushion. When those assumptions hold, the hybrid stack delivers on its promises. When they do not, a family is better served by a different arrangement.

The framework’s value is not in being right for everyone. It is in helping families choose deliberately rather than by default. Most American families currently choose by default. Their employers offer one option, or two; they pick one. Their marketplace offers a row of plans differentiated mainly by metal tier; they pick one. The hybrid stack offers a different sort of choice, in which the family decides what each layer of healthcare is worth and where to source it. The choice takes more thought. For most families, it produces better results.

The argument of this essay has been mostly economic, because the economic case is the most easily measured. But the real case for the hybrid stack, in the experience of families who have made the transition, is not financial. It is harder to put a number on, which is why most discussions of healthcare policy and personal finance never do.

In practice, the hybrid stack delivers a different relationship with medical care. The primary care physician is a person who knows the family, who answers texts when something concerning comes up at ten on a Saturday night, who has thirty unhurried minutes to talk through whatever needs talking through, who has not been forced by the constraints of insurance billing to compress the encounter into fifteen minutes of checkbox-driven documentation. The pharmacy bill arrives, and is twelve dollars, and is paid, and is not the subject of a phone call to anyone. The MRI is needed, shopped, and obtained at an independent imaging center for $500 rather than $4,000, and the result is reviewed by the physician who knows the patient. The whole arrangement is, in a way that healthcare in America has not been for most patients in living memory, calm.

The structural reasons for this are not mysterious. Insurance was designed to address a specific problem: catastrophic events that could bankrupt a family. It does this reasonably well. It was never designed to address relational primary care, routine procedures, chronic disease management, or any of the other things that constitute the bulk of medical encounters. It has expanded into those areas because of historical accident and tax policy, and the result has been, for many families, a kind of generalized friction that they have come to accept as the nature of medical care. It is not the nature of medical care. It is the nature of medical care under a particular payment system.

The families assembling hybrid stacks have not solved American healthcare. They have done something smaller and more practical: they have recognized that the system, as it exists, has more flexibility than it appears. The flexibility exists but has not been widely communicated. Insurers, hospital systems, and pharmacy benefit managers each operate within business models built around their existing product structures. That is not a conspiracy; it is simply how large industries function. The practical result, however, is that most families encounter these alternatives only by accident, if at all. The federal government has moved toward price transparency in fits and starts, leaving the overall picture opaque for most households. The result is that the flexibility exists, is legal, is tax-advantaged, and remains largely invisible to the people it could most help.

And yet the pieces are now in place, the regulations have aligned, and the infrastructure has matured. A family with an hour to study its options can, in 2026, construct an arrangement that twenty years ago would have required moving to another country. The architecture is not what most Americans currently have. It is, increasingly, what they could have.

The argument of this essay has been that more of them should. The decision belongs to each family, and it should be deliberate and account for the family’s specific situation, risk tolerance, geography, and existing medical needs. The default, which is to take what comes from the employer or the marketplace and assume it is the only option, can leave significant value on the table for families who have the flexibility to do otherwise. There are other options. They are legal, tax-advantaged, and available, and for many families, they represent a meaningfully better arrangement than their current one.

In the end, the system will not be fixed by any of us. It may be fixed eventually by Washington, or it may not. In the meantime, what families can do is what families have always done: look at the situation as it actually is and, within it, make the most thoughtful arrangement they can. The hybrid stack is one such arrangement. It is not perfect. It is not for everyone. But for many families, in this peculiar moment of regulatory convergence and infrastructure maturity, it represents something closer to a real answer than the system itself has produced. That is worth knowing about. It is worth, at least, the hour of attention required to consider whether it might apply to you.

The data on Direct Primary Care growth and demographics in this essay draws principally from the 2026 Direct Primary Care Trends Report published by Hint Health (press release, PRNewswire, April 23, 2026), which analyzed data from over 2,700 DPC clinicians and 1.4 million members. Practice density figures draw on the DPC Frontier mapper (dpcfrontier.com) and policy tracking by the Direct Primary Care Coalition (dpcare.org).

The 2026 marketplace pricing and the return of the subsidy cliff are documented in CNBC’s January 6, 2026, analysis citing KFF data; healthinsurance.org’s ongoing ACA coverage; and the Peterson-KFF Health System Tracker. The 400 percent FPL thresholds ($62,600 single, $84,600 couple, $128,600 family of four for the contiguous U.S.) are drawn from these sources.

The provisions of the One Big Beautiful Bill Act are drawn from the text of H.R. 1 (119th Congress, signed July 4, 2025), IRS Notice 2026-05, and IRS Revenue Procedure 2025-19, which established the 2026 HSA contribution limits ($4,400 self-only, $8,750 family, $1,000 age-55 catch-up) and HDHP out-of-pocket maximums ($8,500 individual, $17,000 family).

The discussion of health sharing ministries draws from: the ProPublica investigation of Liberty HealthShare (February 2023); Christianity Today’s coverage of the Sharity Ministries bankruptcy (April 2022), which cited October 2021 court documents showing over $300 million in unpaid member claims; the New Hampshire Insurance Department’s statement on member recovery (NHPR, December 16, 2021); and the Colorado Division of Insurance’s annual disclosure reports.

Surgery Center of Oklahoma figures are drawn from the practice’s posted prices (surgerycenterok.com, May 2026) and Medical Economics’ December 2025 profile of founder Keith Smith, which cited a breast biopsy price of $1,900. Cost Plus Drugs, Amazon RxPass, and GoodRx figures draw from those companies’ publicly available pricing as of early 2026.

The pre-Medicare bridge analysis draws on the Mercer Health and Benefits 2024 National Survey of Employer-Sponsored Health Plans (17 percent retiree benefit figure) and Vanguard’s June 2025 analysis on early retirement bridge strategies.

The geographic analysis combines Hint Health DPC density data, the Direct Primary Care Coalition’s state policy tracker, and the Peterson-KFF state-level marketplace data.

Resources for families considering the hybrid stack:

DPC Frontier practice mapper: mapper.dpcfrontier.com

Healthcare.gov subsidy calculator: healthcare.gov

Cost Plus Drugs: costplusdrugs.com

GoodRx cash price comparisons: goodrx.com

Free Market Medical Association (transparent-pricing facilities): fmma.org

Surgery Center of Oklahoma posted prices: surgerycenterok.com

About the author: I am a cybersecurity professional, retired Air Force officer, and adjunct professor, not a healthcare economist. I wrote this because a friend’s early retirement plan was derailed by a marketplace insurance quote. My wife and I have also been using this model for the last 10 years. There was, at least for him and for families in similar situations. The hybrid stack is not a manifesto. It is a practical framework, and it has limits I have tried to be honest about. If it helps one family ask better questions, that is enough.