Before we go any further, here is the thesis you actually need to understand:

If any major US defense contractor is working with technology of unknown origin, the bottleneck for disclosure will not be Congress, the Pentagon, or the Intelligence Community. It will be GAAP. It will be SEC risk disclosures and Sarbanes-Oxley compliance.

Because the moment this becomes verifiable, it stops being a national-security fairy tale and becomes a material nonpublic fact – the kind that boards, auditors, and shareholders cannot legally ignore. Everything that follows is just the accounting.

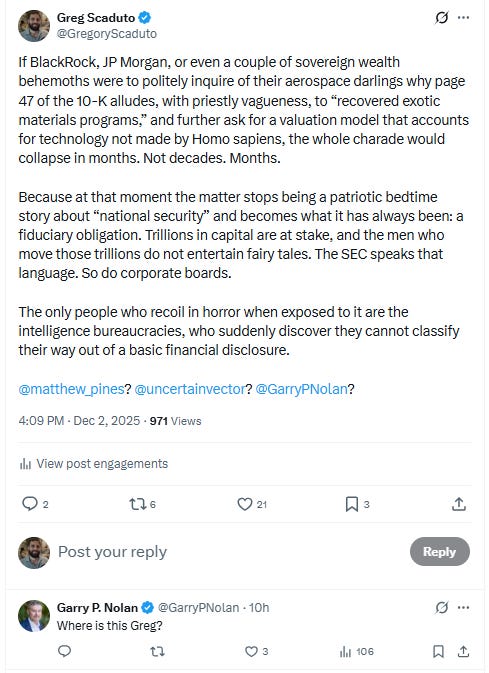

I wasn’t expecting Dr. Garry Nolan to actually respond to this, because he usually only replies to my jokes:

Let me first answer Dr. Nolan directly: my original post was pulled straight from a fever dream of Matthew Pines, and there has not been explicit mention of UAP in the 10-K filings of the behemoth defense companies like Lockheed Martin, at least not to my knowledge. My post was a hypothetical to make a point I’ll further explain below. BUT there was another recent, little-known SEC filing that is of interest.

In 2024, a small but noisy firm called Tuttle Capital – more known for spectacle than substance – submitted a filing to the SEC. Buried within the ritualistic jargon of risk disclosures, amid the clauses and footnotes no citizen ever reads, was a quiet line that pierced the veil: “Government confirmation or denial of advanced alien tech is uncertain.” There it was. Alien technology, not whispered by conspiracy theorists in basements, but acknowledged in the language of official finance.

The fund itself, absurdly named the UFO Disclosure ETF – ticker symbol UFOD – was never brought to market. But it didn’t have to be. Its filing, like a classified sentence left unredacted in a government PDF, revealed more than it was supposed to. For years, UAP had existed at the edge of sanctioned reality – recorded in cockpit tapes, shrugged off by committees, and buried in the public subconscious under the label of delusion.

But now Wall Street had broken the fourth wall. The fiction had been punctured. The market, cold and indifferent to ideology, had joined the conversation. And once capital begins to take an interest, the boundaries of permissible truth shift accordingly.

The household names like Lockheed Martin are not seeing their inventories audited by KPMG in places that were previously roped off. Not yet. But the silence won’t hold – not in a system where silence itself becomes a liability.

And here’s the part most people don’t understand: UAP language won’t start appearing in 10-Ks because CEOs suddenly start taking Joe Rogan seriously. It appears for one reason only: materiality. The minute any verifiable involvement with “technology of unknown origin” becomes known to auditors, boards, or regulators – even indirectly, even through a leak, even through a congressional confirmation – it crosses a legal threshold. Under Item 105 of Regulation S-K, any factor that could plausibly affect a company’s valuation, litigation exposure, R&D assumptions, or operational risk must be disclosed. And once something must be disclosed, its absence becomes its own liability. That’s how the dam breaks: not through belief, but through compliance. Not through revelation, but through accounting.

Materiality doesn’t trigger itself; it must be triggered by knowledge. And boards don’t gain knowledge through sci-fi revelations or midnight confessions, but through channels they are legally obligated to acknowledge. A congressional confirmation. A DoD Inspector General finding. A leaked contracting document. A whistleblower with contemporaneous records. A classified program described in a secure briefing that a board member attends by virtue of their clearance. The moment any of this crosses into the boardroom – even as a plausibly credible allegation – the clock starts. Audit committees must evaluate it. Outside counsel must be consulted. Internal controls must be reviewed. And once the possibility becomes known to the people responsible for disclosures, silence becomes indefensible. At that point, it isn’t about aliens. It’s about liability exposure and the risk of a future shareholder lawsuit claiming the company concealed a material fact it had reason to believe was real.

So now picture, if you will, a portfolio manager at a sovereign wealth fund in Singapore. Or a risk officer in a New York glass tower, deep inside the machinery of BlackRock. Perhaps an equity analyst assigned to Lockheed Martin, armed with a spreadsheet, a deadline, and a muted sense of wonder. These are not men and women prone to fantasy. They do not believe in aliens. They do not need to. What they believe in is liability. Material exposure. The quiet arithmetic of risk.

Now picture them scanning page 47 of a defense contractor’s 10-K. Buried in the boilerplate: a passing mention of “special access programs” linked to “legacy technologies.” No elaboration. No appendix. A footnote that vanishes into fog. That might have passed unquestioned in the Clinton years, when the data moved slower and the press didn’t read footnotes. But this is not 1995.

And if you happen to possess a PhD, particularly in astrophysics, I must beg you to read the next sentence with the care you usually reserve for deriding the unwashed laity: everything I’m about to say concerning these inconvenient UAP claims is not speculation, nor mysticism, nor some carnival of wish-thinking, but a plain recital of events that have actually occurred and remain, to the eternal irritation of your guild, matters of public record.

I draw no conclusions; I merely report. And yes, you will not find any of this in the journals you cherish like ecclesiastical relics. But then, truths had the discourtesy of being true long before the journals existed, and all truths yet to be discovered, by definition, have not been vetted by your editorial boards or blessed by the high priests of peer review.

Professors, this is the world the rest of us inhabit. The cosmos has never promised to obey your syllabi or arrange itself into palatable frameworks. And yet we, not you, must still make ethical decisions in the here and now, using whatever fragments of reality come to hand, however unaesthetic they may be to academic sensibilities.

We have watched Congressional hearings. We have read whistleblower statutes with teeth. We’ve seen decorated veterans swear under oath that recovered craft exist, and that some of them are not made by human hands. There is testimony – names, ranks, dates. A strange consensus, soft but gathering mass, that the official story may no longer be the whole story.

If that turns out to be true – if any part of the US defense apparatus is engaged in the study or reverse-engineering of non-human technology – then what follows is not science fiction, but mere accounting principles.

Because once such involvement becomes verifiable, a new set of rules apply: SEC disclosure, shareholder materiality, audit exposure. The quiet language of compliance suddenly becomes a battlefield of its own.

This is all just GAAP. That’s all this comes down to for the risk-averse oligarchs in Patagonia fleece who’ve never read past the executive summary. These are not intellectuals; they are the Excel-slinging disciples of Milton Friedman who will all run off a cliff together, or show up to work in ridiculous fleece vests if enough of their frat brothers are doing it. How do I know this? I’m one of them, chief. I have several of these vests.

If a public contractor is engaged in programs involving “technologies of unknown origin,” and those programs are material to their R&D pipeline, their valuation assumptions, or their geopolitical risk exposure, then that is a material nonpublic fact. One that must be disclosed under Item 105 (Risk Factors) or 103 (Legal Proceedings) of Regulation S-K.

The only reason it hasn’t been? Because the government has, until now, maintained plausible deniability. But that dam is cracking. The Schumer-Rounds amendment, though gutted in final markup, contained language about recovered materials and biologics. Congressional staffers have met with multiple individuals claiming first-hand knowledge of crash retrievals. The Overton window is not just shifting…it’s being pried open.

The moment a contractor’s involvement is confirmed, whether through an oversight leak, a FOIA dump, or a reluctant nod from the DoD Inspector General, the risk calculus changes overnight.

At that point, the silence isn’t weird, but a Sarbanes-Oxley problem.

And the responsibility shifts.

It shifts to the asset managers. Because if you’re Vanguard, and 3% of your portfolio is in aerospace and defense, and it turns out one of those companies is sitting on technology that rewrites the physics of propulsion, your exposure isn’t theoretical. It’s immediate. Repricing happens fast when the market realizes it’s been underwriting the next Manhattan Project with no visibility.

So what happens next?

You get questions. From institutional investors. From sell-side analysts. From ESG committees trying to figure out how to score a company rumored to have non-human biologics in cold storage.

And you get pressure. Pressure on boards to verify whether such programs exist. Pressure on audit committees to demand better internal controls. Pressure on the SEC to issue guidance. Because capital doesn’t like ambiguity. It likes disclosure.

Which brings us back to the fairy tale. The idea that all of this could stay in the shadows because it makes people uncomfortable. That a program of such magnitude and consequence could remain insulated from the rules that govern every other publicly traded enterprise.

That story is ending.

The minute Wall Street decides UAPs are no longer a sideshow but a sovereign risk, a tech arbitrage, and a balance-sheet wild card – the dam breaks.

And months later, not decades, the charade collapses. Because in the end, aliens may be speculative. But material risk isn’t.

I’ve been saying this for some time now: the point of leverage for the UAP disclosure movement is not another Jesse Michels podcast (God bless him though). It’s, boringly, Wall Street.

This is just what I think. But I have a BA from Fordham. What do you think?