.jpg - Wikimedia Commons")

The physics of a transformer fits on a single page of any sophomore engineering textbook. Two coils of wire wrapped around a magnetic core, primary and secondary, with the ratio of turns setting the voltage ratio. The challenge is doing it at 500 kilovolts with 99.5% efficiency, and then running the machine for forty years under continuous load, through lightning strikes, short circuits, and daily thermal cycles.

That is not hypothetical. The Department of Energy defines a large power transformer as a unit rated at 100 MVA and 115 kilovolts or above. These machines sit at the top of the grid hierarchy and step voltage up or down between generation, transmission, and distribution. At that scale, the design reduces to three simultaneous problems, each a different physical mechanism that must be controlled without compromising the others.

The first is magnetic. Every time the alternating current reverses, sixty times per second in the United States and fifty in most of the world, the magnetic domains inside the core flip with it, dissipating energy through hysteresis. The same changing flux also induces circulating eddy currents in the steel itself, which were known after Léon Foucault described them in 1855, and those currents dissipate more energy as heat. Core losses run continuously, whether the transformer is serving a load or sitting idle at its rated voltage.

The second is resistive. Windings carry current, and every amp through every ohm of copper generates heat by Joule's law, published in 1841 and still the reason why a transformer that serves a load gets hot while one sitting idle does not. At the low-voltage side of a 750 MVA autotransformer, currents reach the thousands-of-amperes range. Reducing resistive loss means more copper, bigger conductors, shorter paths, and therefore more weight, more cost, and a bigger machine to move.

The third is mechanical. If you have ever stood next to a substation and heard the low continuous hum, that is the core vibrating at twice the grid frequency as the steel changes dimension with every magnetic cycle, a phenomenon called magnetostriction. That is the benign version. The destructive version arrives during an external short circuit, when fault currents drive radial and axial forces on the windings that scale with the square of the current, and a winding designed to carry 2,000 amps has to survive 30,000 amps for a few cycles without the thousands of individual copper strands shifting a millimeter. Unlike the other two problems, this one is not a loss to minimize but a failure to prevent, and it has no margin for error.

Doing all three at once, reliably, at scale, for forty years, is what separates an engineering exercise from an industrial capability. The United States has spent the past four decades losing that capability, one node at a time. It starts with the steel.

Grain-oriented electrical steel, or GOES, is the material at the heart of every large transformer core. It is a silicon-iron alloy at roughly 3% silicon, rolled into sheets 0.18 to 0.35 millimeters thick, with the crystalline grains forced into a specific orientation called the Goss texture, named after Norman Goss, who patented the process in 1934. The trick is that every grain aligns its magnetic easy axis along the rolling direction. Hence, the steel conducts flux along one axis with extraordinary efficiency and resists it along every other. A premium GOES sheet reduces core losses by roughly 20% compared with conventional grades, which, in a 500 MVA transformer, translates into megawatts of electricity not wasted as heat over 40 years of service.

Producing it is one of the most demanding metallurgical processes in heavy industry. The slab has to be reheated above 1,350 degrees Celsius to dissolve precipitate inhibitors that later pin grain boundaries, then cold-rolled to the final gauge, and finally decarburized in wet hydrogen to bring the carbon content below 0.003 percent. The entire coil goes into a high-temperature box anneal at 1,200 degrees Celsius for five to seven days, and during that week inside the furnace, through a phenomenon called abnormal grain growth, Goss-oriented grains consume the rest of the matrix and grow to centimeters across a sheet that is barely thicker than a credit card. Premium grades are then laser-scribed in transverse lines to refine the magnetic domains and cut losses by a further ten to fifteen percent. Each step is unforgiving, and a single deviation in composition, atmosphere, or timing ruins the whole coil.

The global capacity map is concentrated and lopsided. China's Baosteel alone operates 1.16 million tonnes per year of GOES capacity on a single integrated line, and Chinese producers combined accounted for roughly 56 percent of global output in 2023. Nippon Steel and JFE cover most of the remainder from Japan, with POSCO running the Korean supply. ThyssenKrupp Electrical Steel, the only sizable European producer, announced in December 2025 that its Isbergues plant in France would drop to half capacity and close entirely from June through September 2026, citing Chinese imports that had tripled since 2022. The decision removes the last European producer of premium GOES at a moment when the continent has committed to major grid expansion. This sequencing undermines European industrial and energy autonomy.

The United States has one producer. Cleveland-Cliffs, which acquired AK Steel in March 2020 for 1.1 billion dollars, runs Butler Works in Pennsylvania. Butler produces up to 250,000 tonnes per year of electrical steel with around 1,300 employees, and it is the only US source of the thinnest M2 grade used in premium transformer cores. A 195 million dollar hot-mill expansion is targeted to begin production in 2028, and a separate 75 million dollar grant from the Department of Energy is funding the electrification of the slab reheaters. Until those expansions deliver, every domestic transformer manufacturer draws from the same single mill.

The second thing a transformer needs is a winding that survives forty years of electromagnetic abuse, and a person who can build it.

The working conductor in a high-voltage winding is Continuously Transposed Cable, or CTC. It is a bundle of five to eighty-five individually enameled rectangular copper strands, woven together so that each strand rotates through every radial position along the length of the cable. The rotation is called Roebel transposition, patented by Ludwig Roebel in 1912. Without it, each strand would experience a different loop voltage due to the leakage flux field, and connecting them in parallel at the winding ends would drive circulating currents large enough to dominate the load losses. With it, flux linkage equalizes across every strand, and those currents collapse below half a percent of load current. The manufacturing tolerances are unforgiving: enamel concentricity within 2 microns, strand height within 8 microns, and transposition pitch never exceeding 120 times the strand width.

A disc winding for a 500 kV transformer is built by hand. Each pancake-shaped disc is wound around a cylindrical mandrel, discs are connected at alternating inner and outer crossovers, and above 132 kV, the winding is interleaved, with non-adjacent turns woven between adjacent ones so that a lightning impulse arriving as a 1.2-microsecond voltage ramp at over a million volts distributes linearly along the winding instead of concentrating on the first few discs. The winder holds conductor tension steady while placing kraft pressboard spacers, radial duct sticks for oil cooling, and interleaving transpositions that change every few discs. Tolerances are judged by eye. A misaligned spacer or an over-tensioned conductor does not appear as a fault until the first external short circuit in year seven of service, when the winding buckles under radial forces and the transformer fails the next time lightning hits the line.

The work cannot be fully automated because every large power transformer is engineered to order. The utility specifies impedance, basic insulation level, tap range, cooling class, and short-circuit withstand requirement, and the winding geometry changes accordingly. Peter Ferrell of the National Electrical Manufacturers Association told Latitude Media that transformers are largely handmade and that it takes years to learn to wrap wire around a transformer's core. Wood Mackenzie's August 2025 report attributed the industry's failure to scale to labor shortages at the OEM level, and flagged copper windings as a second emerging bottleneck. Training a master winder runs between five and ten years. The value of an experienced winder is the hardest part of this story to explain to a non-engineer, and transformer plants closed in the 1980s and 1990s under financial logic that never accounted for the human capital walking out the door. Naveen Abraham, chief EPC officer at Plus Power, summarized the current delivery window for the same outlet: suppliers are telling customers that orders placed today will be delivered in 2028.

The third thing a transformer needs is everything else, and that is where the story stops being about one machine and starts being about who builds what.

A 500 kV power transformer is a 300-tonne assembly, and the active part, the core and the windings, is where the engineering lives. The bushings that carry the conductor through the tank wall have to hold off a million volts between the copper and ground, through a porcelain shell that has to survive lightning, sun, ice, and the occasional gunshot from a rural substation. The on-load tap changer inside the tank executes thousands of switching operations per year under live current, without the utility ever taking the transformer offline. The welded steel tank must maintain a vacuum during factory impregnation and then hold hot oil for 40 years without leaking. Radiators, pumps, Buchholz relays, conservator bladders, dissolved-gas-analysis monitors. Each one is the output of a different specialty industry that took fifty years to build and about ten years to consolidate.

The Western bushing market consists of three companies. HSP in Cologne, Hitachi Energy’s Micafil division in Switzerland, and Trench Group, which Siemens Energy sold to the private equity firm Triton Partners in April 2024. The Western tap changer market is effectively one: Maschinenfabrik Reinhausen in Regensburg holds between 35 and 40 percent of global share, and the top three OLTC makers combined control between 82 and 90 percent of world production. A US transformer manufacturer scaling up production has to negotiate separately with each of these firms, within each firm's delivery window, for each unit it hopes to build. Every time a firm is sold to a PE fund, every time a factory cuts shifts, the US manufacturer’s schedule shifts with it. In China, the same specifications ship from inside the same industrial group. TBEA operates over 420 million kVA of transformer capacity across Shenyang and Hengyang, and the same corporate group also makes its own GOES, CTC, bushings, and tap changers. Chinese transformer exports reached 64.6 billion yuan in 2025, up 36 percent year on year, according to Bloomberg, citing customs data published in January 2026. The fragmented supply chain is paying the integrated one to ship its inventory across the Pacific.

And then, if the assembly and the supply chain line up, the machine still has to pass its tests and leave the factory on its own. Every large power transformer is tested individually because each is engineered to order. The test protocol ends with an impulse-voltage test at 1,425 kilovolts for a 500-kV-class unit, simulating a direct lightning strike, and a partial-discharge test that holds the winding at 150 to 180 percent of rated voltage for 30 minutes while the lab listens for the microscopic electrical discharges that predict future insulation failure. The tests happen in Faraday-shielded high-voltage halls thirty to fifty meters tall, each one a multi-hundred-million-dollar facility that can test exactly one transformer at a time. If the unit fails, it goes back to the floor for rework, and the test hall slot is gone. Then the transformer has to be physically loaded onto a Schnabel car, a multi-axle railcar in which the 300-tonne transformer becomes a structural member between two hydraulic end units. North America operates around thirty such cars in total, of which only three to ten can carry the heaviest current LPTs. Route clearance planning takes up to 9 months because every bridge along the path must be load-rated for a gross weight that a 1970s road design never anticipated. The American Society of Civil Engineers’ 2025 Infrastructure Report Card graded US bridges at a C, with an average age of 47 years against a 50-year design life. A transformer ordered today, built over two years across nine countries, and tested in a hall that another utility is also waiting to use, still has to cross a country whose infrastructure is older than the transformer it is replacing.

The United States built its own large power transformers until 1989. By 2010 it was down to a handful of factories, most of them owned by foreign multinationals. The industry did not collapse, it contracted under its own gravity, across forty years in which nothing failed fast enough to force investment in replacement capacity. The grid that needs replacing today was built between roughly 1950 and 1980, and the units installed back then were engineered to last forty years. Westinghouse exited large power transformers in 1989, selling the business to ABB. General Electric wound down its Pittsfield, Massachusetts plant through the 1990s, while McGraw-Edison was absorbed by Cooper Industries and then by Eaton, and ASEA merged into ABB, which later sold the transformer arm to Hitachi. The Department of Energy's 2020 baseline study found that of 754 large power transformers in the US fleet at that time, 617 had been imported, a structural import dependency of roughly 82 percent that has persisted largely unchanged since.

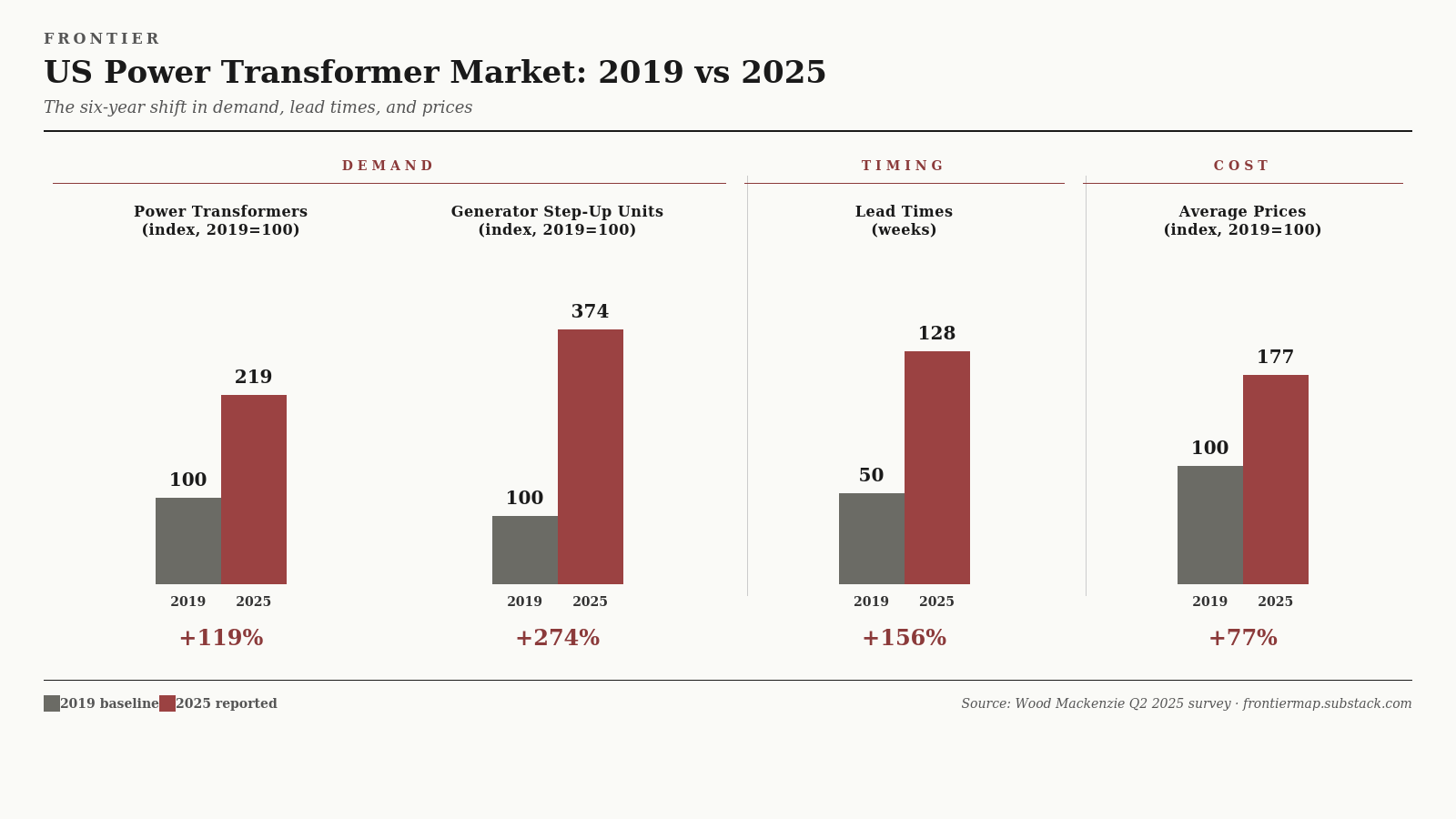

The demand side stayed quiet through 2019. Then it exploded. Power transformer demand in the US has grown between 116 and 119 percent since 2019, and demand for generator step-up units, the transformers that sit at the output of every new power plant, has grown 274 percent, driven by data center construction, electric vehicle charging infrastructure, battery storage, renewable integration, and the replacement cycle of a fleet with an average transformer age of 38 years. The Wood Mackenzie Q2 2025 survey reported lead times of 128 weeks for power transformers and 144 weeks for generator step-up units, against pre-pandemic norms of roughly 50 weeks. Prices are up 77 percent since 2019. Those numbers are the balance sheet of an industry that was allowed to run itself into the ground for three decades while its customer base looked elsewhere.

The bill for that inattention is now arriving. A Sandstone Group analysis published in April 2026 estimated that up to half of the data center capacity planned for 2026 in the United States will not come online on schedule because of electrical equipment shortages that the industry did not anticipate when the projects were approved. Half. Not as a transformer count, but as the power that is not being delivered to the machines, the US economy is betting on.

The response is underway, and it is foreign for now. In September 2025, Hitachi Energy announced a $457 million investment in a new large power transformer factory in South Boston, Virginia, the single largest such facility planned in the United States. Hyundai is investing $200 million to expand its Montgomery, Alabama, plant. Siemens Energy is putting $150 million into its Charlotte, North Carolina, facility. Hyosung HICO, a Korean firm operating in Memphis, remains the only US-based producer qualified for 765 kV class transformers. The only two sizeable independent US manufacturers, Virginia Transformer Corp and Pennsylvania Transformer Technology, have also announced capacity expansions, but they account for only a small share of the total. Wood Mackenzie estimates that roughly $1.8 billion of new LPT capacity has been announced across the US between 2023 and 2025, most of it by Japanese, Korean, German, and Swiss companies.

These projects will take time to produce transformers. A new LPT factory requires three to five years from announcement to first delivery, due to test hall construction, winding room commissioning, and workforce training. Hitachi's South Boston plant is scheduled to begin operations in 2028 and to reach full capacity around 2030. The Alabama and North Carolina expansions follow similar timelines. Wood Mackenzie projects that US domestic LPT production will close the current supply gap, reducing it from roughly 30 percent today to around 5 percent by 2030, assuming all announced capacity comes online on schedule. Between 2026 and 2029, the country will continue importing most of the large transformers it installs.

Next to Hitachi Energy's South Boston plant, Virginia is building 96 new homes for the workers who will operate the factory. The country is rebuilding the industrial capability it lost, one factory and 96 houses at a time.