Summary

- Foreign technology companies cannot be entrusted with meeting Europe’s growing digital needs. This includes American big tech firms.

- Trump rarely hesitates to weaponise technological dependencies or attack the EU’s digital rules. A change of president in the future is unlikely to alter these dynamics.

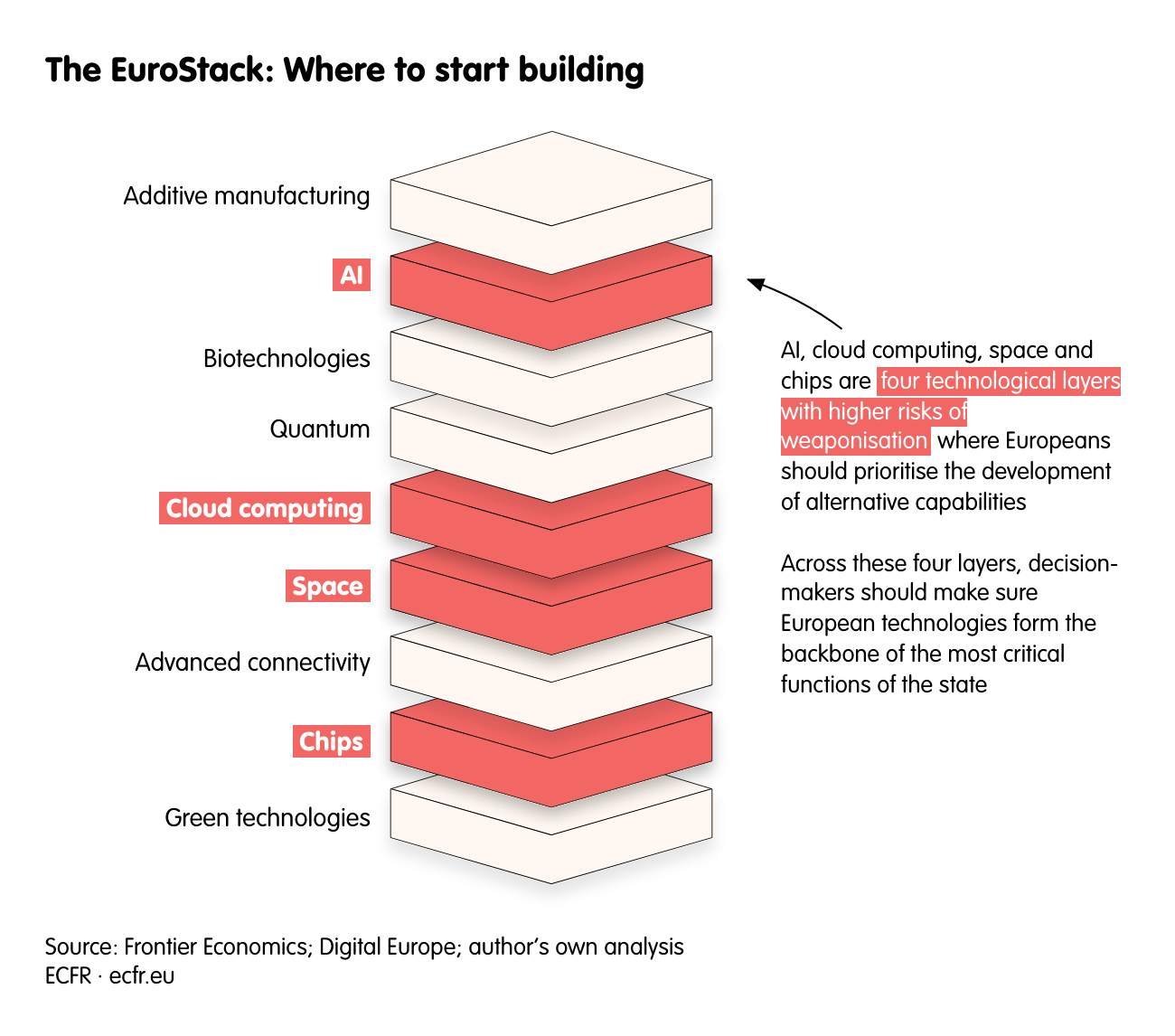

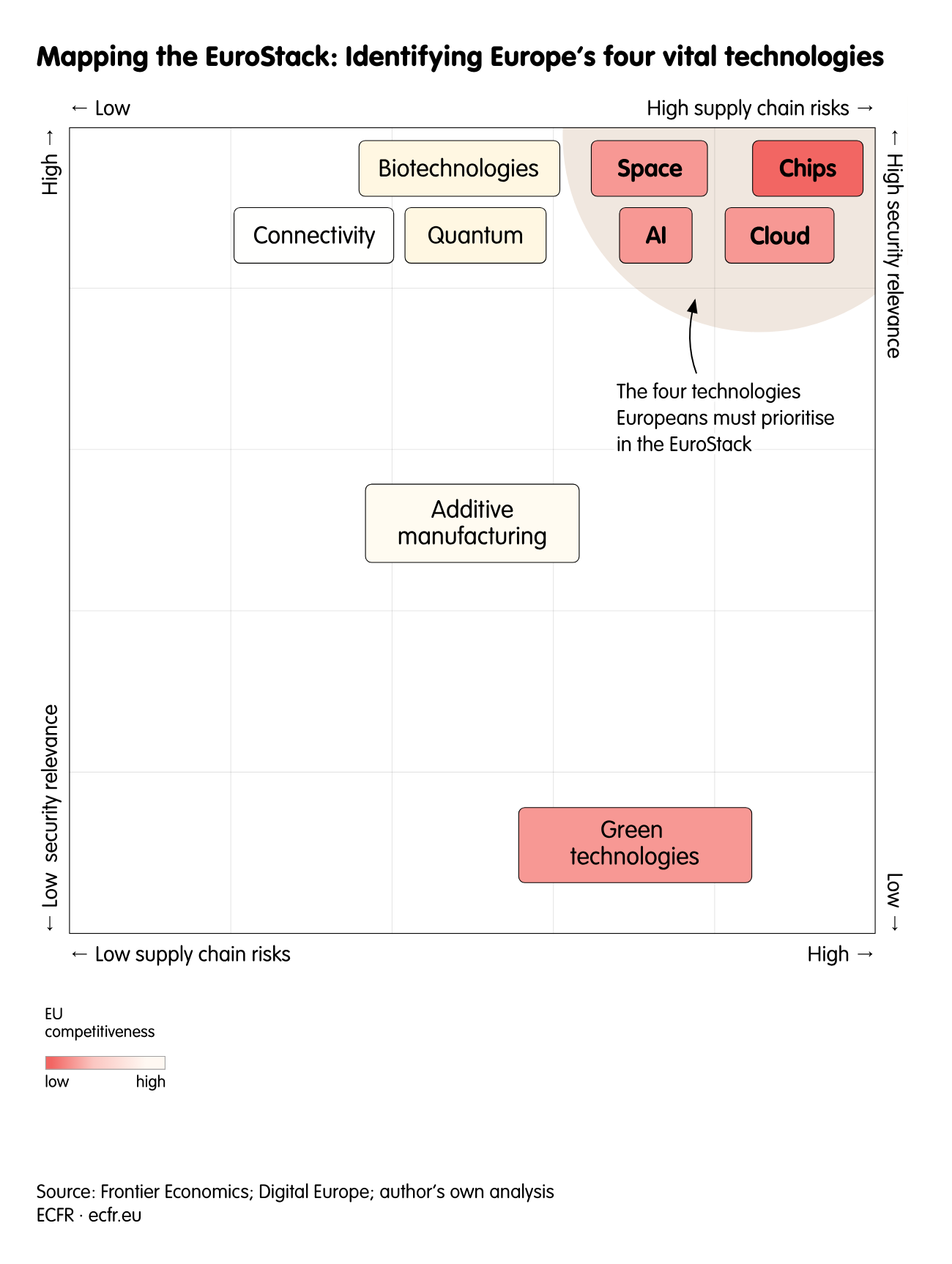

- The EU should build an independent “stack” of technologies to shield itself from other powers weaponising tech against it. Building this “EuroStack” must begin where such risks are greatest, namely in the domains of space, chips, cloud computing and AI.

- The EU does not need to construct an entirely independent new tech ecosystem to strengthen its defences. Instead, it needs to build “just enough” capabilities in these key areas to extricate itself from its dependencies.

- American backlash against this effort is likely. But Europeans can make strategic concessions where necessary while keeping their eyes fixed on the sovereignty prize.

Liberation Day 2.0

It is November 2026. President Donald Trump announces a new executive order on “Regulating Access to American Technology”. This decision grants the president powers to declare a digital security emergency and limit or shut down US digital services—like cloud services, AI applications and military software—to foreign users. The purported goal is to safeguard national security and technological supremacy. The executive order cites European digital policies and taxes as threats to American technology security. Asked how his move could affect US allies, Trump remarks that “some countries may not be our allies in the future”.

The reactions of US big tech companies are mixed. Some praise the president for his “courageous leadership”, while others vow to challenge the executive order through all legal avenues. The absence of clarity in the law regarding executive powers over digital services creates a fog of uncertainty.

In early 2027, the State Department announces sanctions against “the suppression of free speech abroad”. Romanian prosecutors who charged former presidential candidate Calin Georgescu with plotting a coup are placed on US sanctions lists. American digital companies suspend services to these individuals, denying them access to emails, social media accounts and cloud data.

Meanwhile, the Department of Commerce announces another reform to its export control regime. The export of advanced AI chips for data centres now requires an individual licensing agreement—from which other parties can only gain an exemption if they enter into a technology security agreement with the US. Trump officials signal they are keen to work out a such an agreement with the EU, but only if the bloc drops its “unfair” regulatory barriers against US digital trade. Semiconductor orders from EU gigafactories are put on hold.

After a tech dinner at Mar-a-Lago, the Trump administration declares that Meta and Apple will not be paying the fines totalling €700m recently levied on them by the European Commission. The White House announces a law similar to the European blocking statute that prohibits digital and tech companies from complying with the EU’s digital regulations and allows those companies to recover damages.

Europe’s technological dependencies

Can we trust foreign technology companies to form the backbone of Europe’s digital transition? The digital realm’s spread into virtually all aspects of modern economies and societies means policymakers across the EU ought to be providing an answer. Worries about numerous European dependencies on China are now well aired in the public debate. Yet, so far, European decision-makers have only just started to grapple with what it means to be so deeply dependent on American digital technologies.

Three US giants provide 70% of Europe’s cloud computing infrastructure. American companies dominate Europe’s phone operating systems, and OpenAI’s ChatGPT has become synonymous with the concept of AI. Starlink represents a near-monopoly on Europe’s satellite internet services, as does Nvidia in AI chips. The market for social media—the digital squares of the European demos—are also dominated by US companies Meta and X.

Until recently, Europe’s technological dependencies were a problem confined to the world of antitrust and innovation policy. But Trump’s second stint in the White House has already transformed Europe’s digital overreliance into a geopolitical test. He has not hesitated to weaponise the economic and technological dependencies of others in pursuit of his own objectives.

In Ukraine, American officials threatened to shut off Starlink satellite services unless Kyiv agreed a minerals deal with Washington. The chief prosecutor of the International Criminal Court lost access to US digital services after being targeted by American sanctions. Against Europe, Trump has weaponised both the threat of tariffs and the promise of tariff relief in an attempt to force the EU to water down its digital regulations, which seek to protect European citizens from the unfair practices of technology companies.

This issue is also not limited to Trump’s whims; a potential change in US leadership in 2028 will not necessarily provide relief for Europe. In his last weeks in power, President Joe Biden adopted the AI diffusion rule, which curtailed the number of American AI chips that a number of countries, including EU member states, could import. There was no way out of this for the 18 states affected: the administration was uninterested in striking a deal with them nor did it wish to punish them. Its goal was to limit leakage of chips to China, America’s primary strategic competitor.

The US could also coerce Europe by imposing qualitative restrictions on exports to Europe. In the realm of defence, for example, Trump has announced that any F-47 fighter jets sold to allied nations will be downgraded, citing potential future shifts in alliances. Trump has also mused that Nvidia Blackwell chips sold to China could be “enhanced in a negative way”. A similar “qualitative restriction” approach could include selling inferior technology in satellite networks, chips, digital services or AI models.

The experience under Biden should have been a sharp reminder that it is not just Trump-style direct coercion that Europeans have to worry about. For any number of reasons, Europe might find itself confronted with service shutdowns, facing restrictions on the absolute amounts of US digital technologies it can import, or denied components essential to developing digital technologies.

No ride to the rescue

The “Liberation Day 2.0” scenario also highlights the way in which political weaponisation of technology directly impinges on the business interests of the American giants. Aware of these risks, major technology companies have already made clear their intention to take on the US administration where its policies threaten to interfere with their operations in Europe. For instance, Microsoft has committed to legally challenge the US government if it mandates a shutdown of the company’s cloud services in Europe. Amazon Web Services unveiled a “European Sovereign Cloud” that will be “locally controlled in the EU, led by EU citizens and subject to local laws”.

However, Europeans cannot rely on technology companies to stand up to this administration and its successors. Even if one assumes the best of intentions, American companies have to abide by American legislation and its extraterritorial effects. Using non-US subsidiaries or contractors abroad may also offer no solution: the government could extend restrictions to include these and sue the parent company at home for potential breaches. For example, US export control laws have a broad jurisdictional reach and may also apply to non-US companies that manufacture goods containing American technology or components. Similarly, the 2018 CLOUD Act gives American authorities the power to request cloud-stored data even if these are located abroad. Additionally, the Supreme Court recently limited the ability of lower courts to block presidential orders, resulting in fewer checks and balances on potential weaponisation. And this is before technology company owners consider the personal risk of opposing presidential policy: Elon Musk’s criticism of Trump’s budget bill led to threats of subsidy cuts.

In nearly any scenario, America’s technology firms will always be in the weaker position in the face of a determined administration.

Could Europeans ride to their own rescue and retaliate against American weaponisation of technology? Europe’s military dependency on the US makes this improbable, to put it lightly. This was one factor that mitigated against retaliatory action by the EU following Trump’s imposition of tariffs in early 2025—despite its own potential power as an international trading bloc.

Building Europe’s technology stack

Europeans cannot rely on either the self-interest of American technology companies or (as things currently stand) even themselves to keep Europe’s computers on and its data centres running. They therefore need to decide how to de-risk from foreign digital technologies and build alternative capacities of their own.

The EuroStack

The “EuroStack” offers a ready model for European policymakers. This model organises digital technologies into a system of interconnected layers, displaying the relationships between different types of technology. For example, one can easily see how AI capabilities depend on cloud capabilities and, in turn, cloud capabilities depend on chips capabilities. The stack demystifies the digital transition, allowing policymakers (or indeed the lay person) a clearer understanding of where dependencies might exist.

The idea of the EuroStack has been around for the last two years, mostly confined to debates within civil society and among antitrust specialists. But this year political scientists Henry Farrell and Abraham Newman brought it firmly into the realm of international relations. They argued the EuroStack could be part of the solution to withstanding geopolitical pressure from both China and America.

Building a European digital stack is the logical political response for Europeans to the predicament they find themselves in.

EuroStack for realists

Critics of the EuroStack point out that owning every layer of the technology stack would be counterproductive and prohibitively expensive. That is self-evident. But to de-risk from America’s digital technologies, the EU does not need to own every layer across all sectors. To make the EuroStack a manageable and achievable endeavour, Europeans should follow three principles.

First, it is neither necessary nor desirable to replace foreign oligopolies with European ones—this would only generate its own new set of economic and political problems. Instead, the objective must be to build viable European alternatives, which would compete in the market alongside American providers.

Second, European technologies do not need to be adopted across all sectors at once. For example, decision-makers should make sure European technologies form the backbone of the most critical functions of the state, like public administration and defence. But for sectors such as agriculture, education and tourism, continued dependencies on American technology would incur lower risk. Even in these sectors, mitigation measures like promoting the uptake of open-source solutions can further reduce risk.

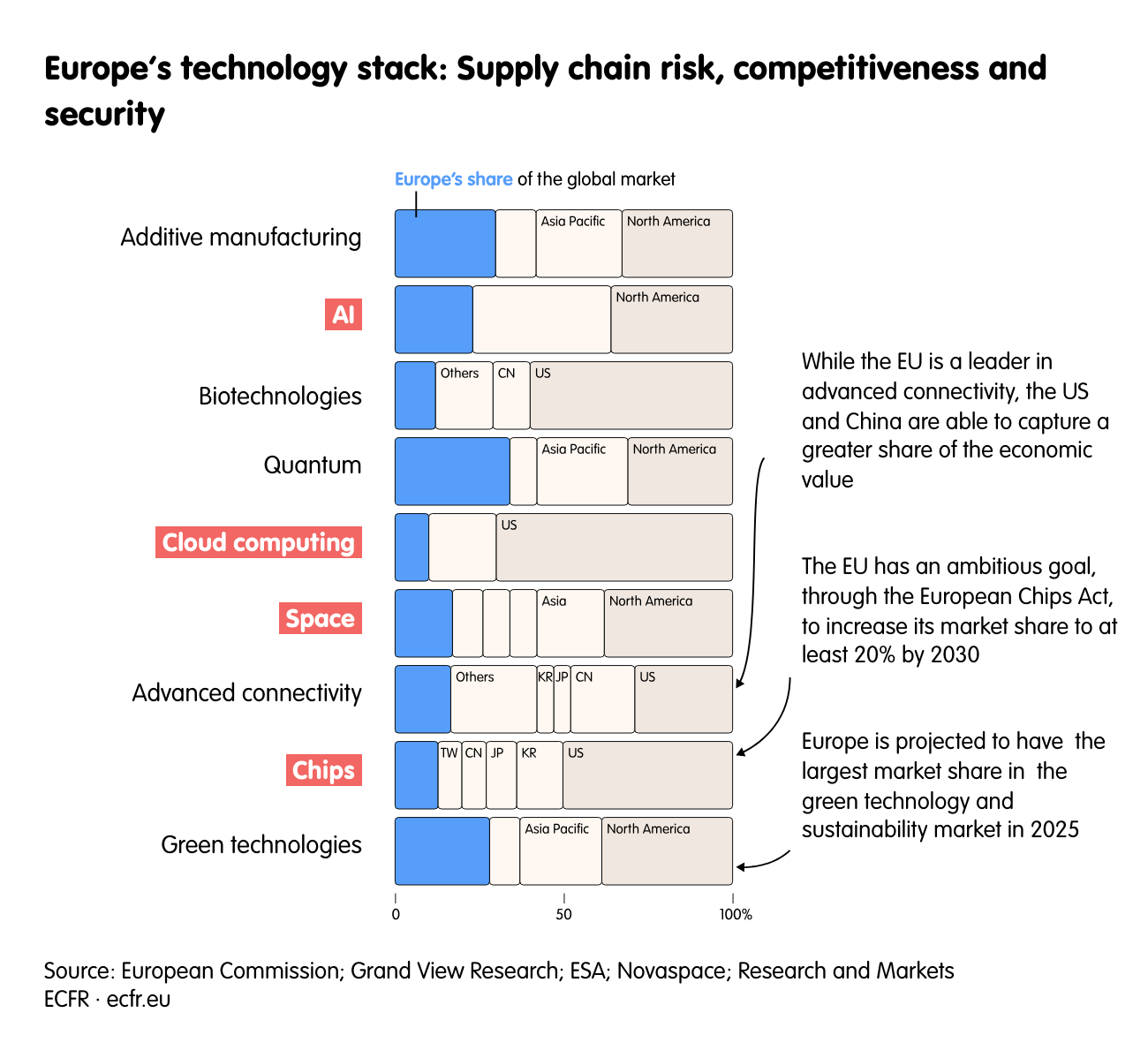

Third, the EU must focus efforts on the layers where the weaponisation risk is greatest. For example, when it comes to advanced connectivity (the networks and devices that enable fast and reliable communications), the EU’s exposure is low thanks to its substantial presence along the connectivity value chain, with the exception of raw materials and components. The EU is also home to Nokia and Ericsson, two world leaders in equipment manufacturing. As a result, building the EuroStack should start with dedicating resources to other parts of the stack.

The four vital digital technologies for Europe

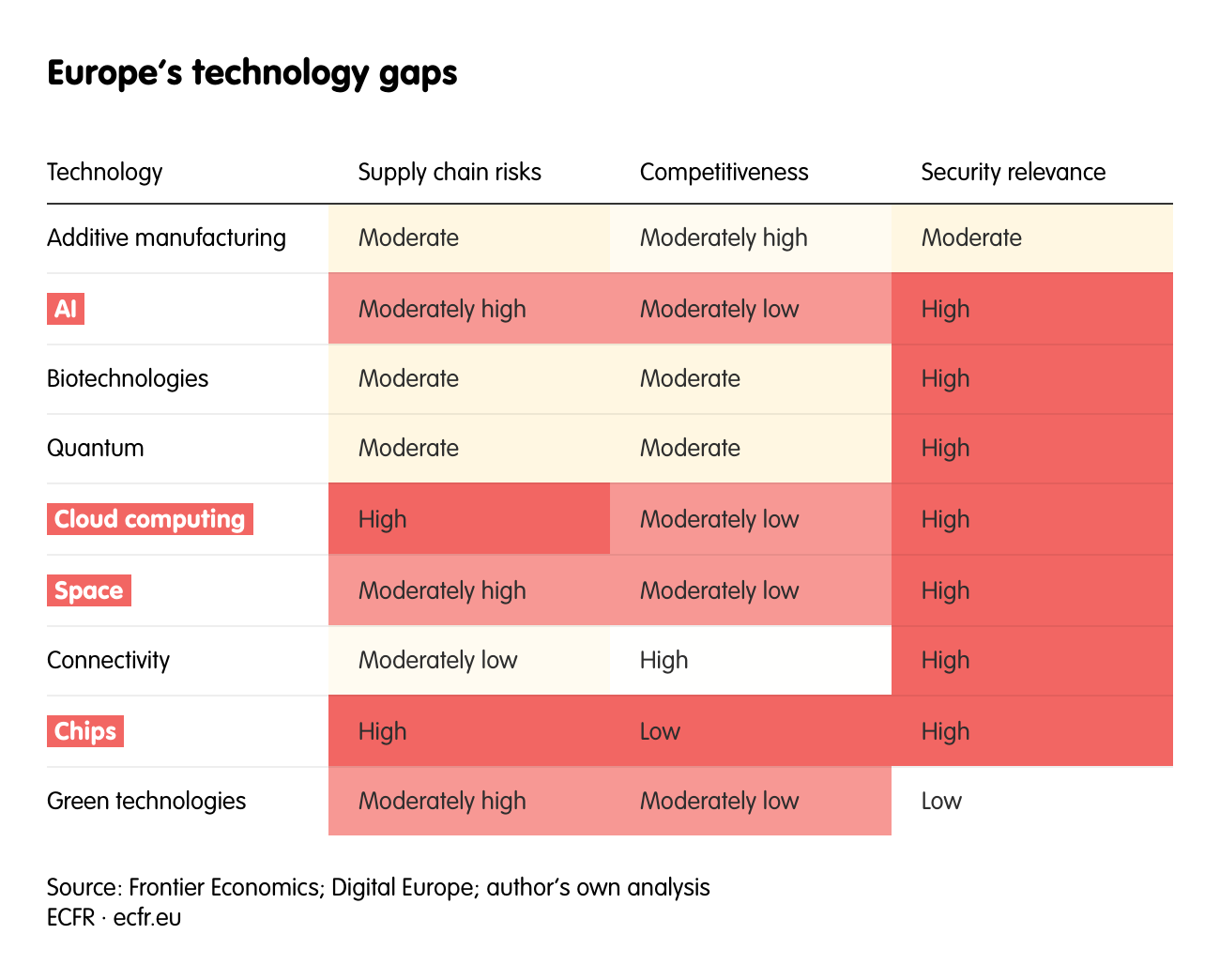

The EU and its member states should prioritise the development of, and access to, alternative capabilities in four vital technological layers. These are: space, chips, cloud computing and AI. In these four technologies, the risks are highest due to their vulnerability to weaponisation, weak European competitiveness and importance in security terms because of the military capabilities they can provide.

Different types of dependency exist within each technology. These are explored below, along with recommendations decision-makers should follow if they are to reclaim sovereignty in digital technologies and avert weaponisation by the US and others.

Space: The EuroStack’s lifeline

The opportunity

Space is a vital technology for Europe’s competitiveness and security: the Council of the EU this year described space as “a building block for strategic autonomy”. It can provide internet access in areas where traditional infrastructure is lacking and for places experiencing emergencies. But the contribution of space technologies goes beyond connectivity and includes navigation management (like GPS), environmental monitoring and scientific applications. The value of the space economy is estimated to hit €1.6trn by 2033.

The EU is already home to some prominent space and satellite manufacturers, such as Airbus and Thales. However, it falls short in the manufacturing of certain parts of the supply chain, such as user terminals and navigation receivers, where it is dependent on the US and Asia. The European Space Policy Institute has found that the EU is not a space power and lags behind the US, China and Russia because it lacks autonomous capabilities.

The problem

One of the most prominent applications of space technologies is in the area of defence and security. In Ukraine, the use of space technologies to support military operations is unprecedented, mainly due to Starlink satellites provided by Musk’s company SpaceX. Ukraine’s deputy prime minister, Mykhailo Fedorov has said: “Starlink is indeed the blood of our entire communication infrastructure”.

However, Starlink is emblematic of the supply chain risks inherent in space technologies and their potential weaponisation. When the US negotiated with Ukraine over access to the country’s critical minerals, American officials threatened to cut the country’s access to Starlink. Musk himself said this could cause Ukraine’s “entire frontline [to] collapse”. When Polish foreign minister Radoslaw Sikorski shot back to say they could look for a new provider, the American replied: “Be quiet, small man. [… T]here is no substitute for Starlink.”

The Starlink saga laid bare Europe’s dependencies in the realm of space technology. With its 8,000 cheap satellites, SpaceX dominates the market. The EU’s response is the IRIS2 project, which aims to put 290 satellites into service. However, IRIS2 will not be operational before 2031, while its scale and mission are much smaller. SpaceX is also likely indispensable for Europe’s launch needs. The European Ariane 6 rocket was passed over for the launch of a European weather satellite, as the operator EUMETSAT preferred to make use of SpaceX’s launch services and its reusable Falcon 9 rocket.

What to do about it

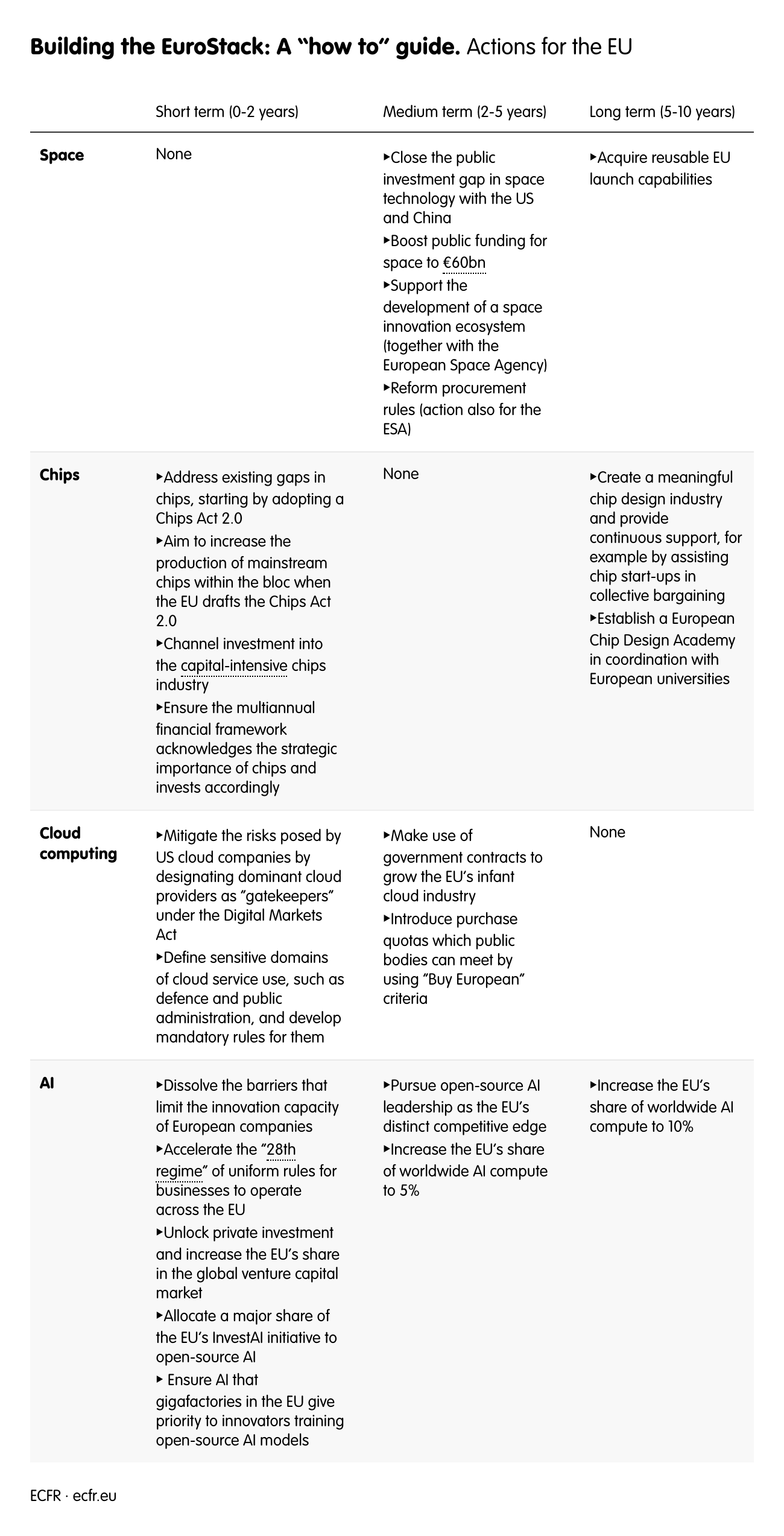

To become a space power, the EU must close the public investment gap with the US and China.The EU and its member states invested less than €12bn in space in 2023, while the US invested $66bn. In the medium term (2-5 years) the EU should aim to increase its public funding available for space to €60bn.Such expenditure could be classified under NATO’s commitment for allies to spend 5% of their GDP on core defence requirements and defence-related spending. Member states could also tap into the ReArm Europe plan, which seeks to leverage €800bn through fiscal flexibility and the €150bn SAFE loan instrument.

In the same time horizon (2-5 years), the EU and the European Space Agency (ESA) should support the development of a space innovation ecosystem. The emergence of private space companies offering cost-effective solutions represents a paradigm shift. However, the Council of the EU noted in 2024 that private sector engagement and investment in the European space economy is still limited. To reverse this trend, Mario Draghi, author of a major report on European competitiveness, proposed a space fund that would enable the European Commission to act as an “anchor customer” and attract further private investment. Alongside this, both the EU and the ESA should reform their procurement rules. For the EU, faster and more flexible procurement rules are essential to cater to the rhythm and needs of start-up innovation. For the ESA, the rule of “geographical return”, which assures states that their national contribution will correspond to contracts, should be abolished.

In the long term (5-10 years), the EU must acquire its own reusable launch capabilities. Such a project is already under way: in November 2025, the ESA named a shortlist of potential companies that could be contracted to build the continent’s first reusable rocket launcher. This is an essential step that will ensure Europeans have access to “just enough” capabilities that will allow unconditional access to space. However, it is important that these capabilities are delivered on time and that delays are avoided. (The IRIS2 satellite project noted earlier was initially planned to provide services by 2027.) Taken together, these measures could help build the first layer of the technology stack and thus provide protection for Europe against weaponisation in space.

Chips: The EuroStack’s core

The opportunity

Chips are an indispensable element of Europe’s technological infrastructure. They are essential for many other layers, such as AI, and multiple other industries, including defence, automotives and energy. In contrast to most of the other layers of the technology stack, the EU has acknowledged its chips dependencies and attempted to alleviate them. In 2022, it adopted the European Chips Act, which aims for 20% of the world’s chip manufacturing to take place within the EU by 2030. However, the act’s effectiveness is severely limited. The European Court of Auditors reported the target will almost certainly be missed. On current trends, the court forecasts the EU is more likely to achieve a global market share of 11.3%. In response, the EU’s 27 member states published a declaration as the Semicon Coalition in September 2025 calling for a more ambitious and forward-looking chips act. This shows that Europe’s slow progress has been recognised at the political level, potentially opening the way for decision-makers to agree effective solutions to this problem.

The problem

Chips are also the stack technology that has most often experienced disruption in recent years. In 2020, the covid-19 lockdowns led to shortages of Chinese chips, which slowed down European car production. The US administration’s short-lived AI diffusion rule described earlier (and which was later dropped under the Trump administration) imposed strict quantitative limits on the number of AI chips that some European countries could import. Most recently, China extended its restrictions on the export ofrare earth materials used to create chips.

The strategic nature of chips and the frequent disruptions within their supply chains make European chip capabilities essential. However, currently the EU possesses only upstream capabilities, in the field of equipment for chip fabrication thanks to the presence of the world-leading company ASML. (No other such companies are based within the bloc.)

In the rest of the chip supply chain, Europeans have virtually no presence at all. EU states lack manufacturing capacity (foundries) for the most advanced chips and there are no large designers to compete with the likes of Nvidia or Qualcomm. As a result, only 1% of global chip design is done by European companies, while the EU also accounts for less than 10% of global chip manufacturing.

What to do about it

In the short term (0-2 years) the EU should address its existing gaps, starting by adopting a Chips Act 2.0.The European Court of Auditors notes that the original Chips Act focused on cutting-edge chips, and thus overlooked industry demand for mainstream chips. But mainstream chips (in the range of 65-90 nanometers) represent the bulk of demand coming from European companies, mainly in the automotive and industrial sectors. When it drafts the Chips Act 2.0, the EU should concentrate on increasing the production of mainstream chips within the bloc. This will minimise further dependencies on China and build “just enough” capabilities to help it avoid the weaponisation of other dependencies.

In the same time horizon (0-2 years), the EU should channel investment into the capital-intensive chip industry. Funding for the European Chips Act came primarily from member states’ state aid. The EU must reinforce these efforts and ensure that its forthcoming multiannual financial framework acknowledges the strategic importance of chips and invests accordingly. That being said, in the current fiscal climate public funding by itself is unlikely to strengthen the EU’s capabilities in this part of the EuroStack. In AI, the private sector pledged €150bn in funding until 2030, to top up the EU’s €50bn InvestAI initiative. Similar pledges in chips will thus be required to send the right signals to the rest of the market.

In the medium term (5-10 years), the EU should aim to create a meaningful chip design industry. To achieve this, it will need to ensure an increased number of chip designers are trained up within the European workforce. Currently, only 6% of European STEM graduates are expected to enter the chip industry by 2030, and chip designers represent a fraction of this number. The EU should therefore establish a European Chip Design Academy in coordination with European universities. The academy would offer funding for relevant academic programmes and meet demand in this area.

Besides nurturing talent to grow the nascent chip design industry, the EU must provide continuous support, for example by assisting start-ups, which will need collective bargaining power to access design components that are provided by TSMC (Taiwan), Samsung (South Korea) and Intel (America). The EU should take these needs into consideration within its Digital Partnership Agreements and act as a collective voice.

Cloud computing: The EuroStack’s bedrock

The opportunity

Europe’s computations and data storage increasingly take place “in the cloud”, making cloud computing the bedrock of the future European technology stack. In 2024, 52% of European businesses made use of cloud services; the European Commission aims to increase that figure to 75% by 2030. Cloud infrastructure is essential for the development of other technologies, such as the “internet of things” and AI. Cloud computing has also become a core component for essential state functions, from e-government to the conduct of military operations.

The problem

Despite the central role of the cloud, the EU market is “largely lost to US-based players”, according to Draghi. Amazon Web Services, Microsoft Azure and Google Cloud—known as the “hyperscalers”—control 70% of the European cloud market. In stark contrast, the largest European cloud providers, SAP and Deutsche Telekom, each account for 2% of the EU market. In total, European companies control 15% of EU market share in 2025, a substantial drop from 29% in 2017.

The dominance of US cloud providers stems from their ability to operate like IKEA, according to expert Bert Hubert. Like the store, they provide a service that is all-encompassing, where customers can find what they need to fulfil any need, in this case to build IT solutions. These comprehensive services range from data storage and email solutions to AI tools and even satellite ground stations. Conversely, European cloud providers are only able to offer a subset of cloud services. As Hubert puts it, “no one is interested in a less complete IKEA”. The integration of services within hyperscalers’ cloud ecosystems generates network effects that make switching providers more unlikely—and thus pose even tougher competition for Europeans wishing to catch up.

What to do about it

Urgent action is required to build the EuroStack’s cloud layer. In the short term (0-2 years), the EU should seek to mitigate the risks posed by US cloud companies by levelling the playing field for other providers. To do this, the EU should designate dominant cloud providers as “gatekeepers” under the Digital Markets Act. This would prevent anti-competitive practices such as tying access to cloud services with their other services and giving more favourable treatment to their own cloud services. The EU should also make use of its own upcoming Cloud and AI Development Act to ban other practices such as egress fees, which customers pay when moving data out of a cloud provider’s network, and dismantle other artificial barriers to switching services.

In the same time span (0-2 years), the EU should define sensitive domains of cloud service use, such as defence and public administration, and develop mandatory rules for them. In order to ensure the security, privacy and encryption of sensitive information, cloud services in these domains should be operated by European cloud providers. While European providers are unlikely to match the resources of the hyperscalers, this measure would ensure that the EU and its member states choose sovereign solutions in domains that matter the most. Policymakers in some member states have raised concerns about the potential breach of international trade rules that such provisions would entail.[1] However, the EU can fully comply with the World Trade Organization’s Agreement on Government Procurement by making use of the exceptions granted by the agreement to procurement that is “indispensable for national security”.

In the medium term (2-5 years), the EU must make use of government contracts to grow its infant cloud industry. Public procurement represents around 15% of the EU’s annual GDP, a figure approximating to €2.5 trn. A commitment by governments to “buy European” would redirect significant resources to homegrown cloud providers, which in turn is likely to lead to more competitive products and services. This is also in line with Draghi’s recommendation to introduce explicit minimum quotas for local production in public procurement. This would help member states become “launch customers” in new technologies. The EU should therefore introduce purchase quotas which public bodies can meet by using “Buy European” criteria. It can do this either by revising the Public Procurement Directive, changes to which are already planned for late 2026, or through the Cloud and AI Development Act,

AI: The EuroStack’s frontier

The opportunity

AI is likely to be the most transformative layer of the EuroStack. Its general-purpose nature means AI could reshape today’s industries and deliver significant economic benefits. In science, for example, the achievements of the AlphaFold model may enable the discovery of new medicines. In total, AI’s adoption across economies could drive a 7% increase in global GDP over the next 10 years. AI is also set to transform the military sphere and enhance conventional and cyber defence capabilities by matching or exceeding human performance across military operations.

The problem

Despite the transformative potential of AI, the EU is reliant on the US for the chips and compute that AI requires as well as for the AI models themselves. Chips make up only one part of the compute layer, which also requires a software component and the data centres that enable the development of AI models. The EU’s dependency on American AI chips and cloud services has been already documented in the sections above. But, even when committed to purchase AI chips from the US, the EU has been unable to build its own AI compute power. This year, the European Commission announced a flagship AI gigafactories initiative. But, taken together with France’s AI data centre ambitions, this will make up only 2% of the world’s compute by 2027. Such capabilities will fall far short in supporting an ecosystem of European frontier AI developers that can provide highly capable models. The EU will therefore be forced to import compute. At best, this would mean renting computational power on demand; at worst, it would mean losing European champions to US giants through acquisitions.

It is the same picture when it comes to AI models. Mistral AI—Europe’s last hope in the sector—represents 2% of the world’s large language models (LLMs) market. Mistral AI also ranks bottom when it comes to capability benchmarks vis-à-vis its American counterparts, and its funding is dwarfed by companies such as OpenAI. It is indicative of the lack of European AI capabilities that many EU member state governments have chosen to sign strategic partnerships with American AI model providers instead of with European providers. For instance, Estonia and Greece commissioned OpenAI to integrate LLMs in their education systems while the European Parliament uses Anthropic’s Claude model for its archives.

What to do about it

To build the AI layer of the EuroStack, European policymakers must tackle dependencies in both AI compute and AI models.

Compute is an essential means to the EU’s AI ends. While Europe is unlikely to match America’s or China’s resources in this field, building a stock of European public and private AI compute is essential for security purposes. Recalling the need to build a “realistic”, deliverable EuroStack, the EU’s entire AI compute infrastructure does not need to be owned by Europeans to protect the bloc from weaponisation.

In the medium term (2-5 years), the EU should seek to increase its share of worldwide AI compute to 5%, and thence to 10% in the long term (5-10 years). This would allow EU entities to run some AI models locally and securely. It would also likely enable the development of specialised models that the EU would need to retain control over—such as in public administration, defence and in critical industries.

When it comes to AI models, a top-down approach will not work. (A top-down approach will be more effective in other parts of the technology stack, such as for chips and cloud computing.) Instead, the EU should aim to dissolve the barriers that have limited the innovation capacityof European companies in AI(as well as in other sectors). In the short term (0-2 years), EU decision-makers should accelerate the adoption and implementation of the “28th regime” of uniform rules for businesses to operate across the EU.

In the same time frame, the EU must unlock private investments and increase its share in the global venture capital marketin order to attract funding for the capabilities that will make up the EuroStack. This will require that institutional investors, such as pension and insurance funds, are incentivised to redirect assets towards riskier venture capital.

Lastly, the EU should pursue open-source AI leadership as its distinct edge in the medium term (2-5 years). A study carried out by MIT and start-up Hugging Face showed that the total downloads of Chinese open-source AI models have surpassed downloads from American companies.

The EU should aim for European open-source AI models to become the models of choice in this important market. Open-source AI would enable market entry for Europe’s low-resource actors and enable greater AI adoption through customisation. To send the right signals to the market, the EU should allocate a major share of its InvestAI initiative to open-source AI in the short term(0-2 years).In the same time period, the EU’s AI gigafactories should also give priority to innovators training open-source AI models.

The cards are stacked

As the saying goes: if the cards are stacked against you, reshuffle the deck. But if technologies are stacked against you, it is time to make a deck of your own.

The EU has suddenly found itself struggling to survive in a global order dominated by international power play. The rules of the game have changed, with direct implications for the EU’s dependencies in trade and technology. Since Trump’s return to power, much of the world has been transfixed by his tariff exploits: the weaponisation of trade dependencies has become ever-clearer to governments around the world. But technology dependencies remain less examined. The prospect of a “Liberation Day 2.0” shows how plausible technology weaponisation could be. The use and misuse of technological dependencies is already with us, from export controls on chips to Starlink’s role in Ukraine. The only way for Europe to protect itself from these attacks is to build its own independent stack of technologies. Sovereignty, in this regard, is not about restricting but about enabling. European alternatives can bring choice for consumers, citizens and states; they can compete alongside American providers.

The development of a EuroStack is likely to provoke reactions from the other side of the Atlantic. To minimise frictions, Europeans could adopt these measures without making strong reference to US dependencies—and indeed without even making reference to a EuroStack. Even so, measures such as preference for European companies in public procurement are unlikely to go unnoticed. In such cases, Europeans could get what they need with a bit of give and take, such as by providing strategic concessions where necessary. For instance, the EU could soothe Trumpian ire by helping America keep its advantages in particular areas, such as cutting-edge chips and AI compute infrastructure. Europeans have been here before: when the EU’s Galileo project sought to develop alternative solutions to satellite navigation, the bloc made strategic concessions to the US to alleviate tensions. But ultimately it was still able to develop its own alternative capabilities.

The high-level Summit on European Digital Sovereignty which took place in November 2025 recognised the importance of finding solutions to strengthen sovereignty in this area. But now Europeans must turn their political intentions into real-world capabilities. In this pursuit, they will need to be selective, and above all realistic. New and stronger capabilities cannot be built overnight across all layers. Decision-makers must begin where the risks of weaponisation are greatest, the EU’s competitiveness scores poorly, and defence security matters are a concern. Space, chips, cloud computing and AI are the places to start. Success requires the EU and its member states to view the development of alternative capacities in these technologies as essential investment that will increase both their economic and military security. Ultimately, the question is not whether Europeans can afford to build their own technology stack, but whether they can afford not to.

About the author

Giorgos Verdi is a policy fellow with the European Power programme at the European Council on Foreign Relations. His research focuses on the implications of critical and emerging technologies for the EU’s competitiveness, economic security and foreign policy.

Acknowledgments

This policy brief was supported by funding from Luminate Projects Limited. The author would like to thank Adam Harrison for his sharp feedback and edits that helped to make this brief better. The author would also like to thank Chris Eichberger and Nastassia Zenovich for their invaluable support in shaping the visual identity of the brief as well as Nele Anders and Mireia Faro Sarrats for their support on the advocacy front.

[1] Author’s conversations with member state officials, July 2025.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.