I saw a tweet recently along the lines of: “Watching software stocks get destroyed…Bill Gurley said companies were just starting to find discipline on cost and stock comp when the AI boom kicked off. Might be delayed reckoning time.” That’s pointing at something real. But it’s also mixing two separate forces that happen to be hitting software at the same time.

One is macro: the price of time changed. The other is structural: the price of labor changed, and the software stack is getting re-bundled.

Monster #1: Duration (Rates Ate My Multiple)

A big slice of the “software stocks are getting destroyed” story is just arithmetic. Software is long-duration: much of the value sits in cash flows far in the future. Raise the discount rate and the future gets cheaper.

Here’s a back-of-the-envelope way to see it without pretending this is a full DCF.

In steady state, a reasonable approximation is:

EV/Revenue ≈ m/(r - g)

Where:

m = sustainable free cash flow margin (as % of revenue)

r = discount rate

g = terminal growth rate

Toy numbers (illustrative, but not insane):

m = 25% (mature high-quality SaaS)

g = 3%

Case A: r = 8%

EV/Rev ≈ 0.25/(0.08 - 0.03) = 5.0x

Case B: r = 12%

EV/Rev ≈ 0.25/(0.12 - 0.03) ≈ 2.78x

That’s a ~44% drop in the revenue multiple with no change in product, competition, or execution. Just the price of time moved.

In plain English: when interest rates were low, investors were willing to pay $5 today for every dollar of revenue in the future because future cash flows looked attractive when discounted back to today. When rates rose, that same dollar of future cash flow became worth less in today’s terms, so the multiple compressed to 2.78x. The business didn’t get worse. Time got more expensive.

This is the environment where cost discipline stories appear: cost control, reduced stock-based compensation, less growth at any price. When the market stops subsidizing your future, you have to earn your present.

But this is the easy monster. It’s a macro knob. The second monster changes what the business is.

Monster #2: AI Attacks the SaaS’s Two Hidden Assumptions

Classic SaaS relies on two assumptions:

Seat pricing maps reasonably well to value created

Costs are mostly fixed, so gross margins expand as you scale

AI puts both under stress. And it does so via two mechanisms: labor deflation and variable cost inflation.

Labor deflation —> seat compression. A lot of software’s historic unit of billing—a seat—was a proxy for the unit of work. Pay per seat because the seat does the work.

AI changes the unit of work.

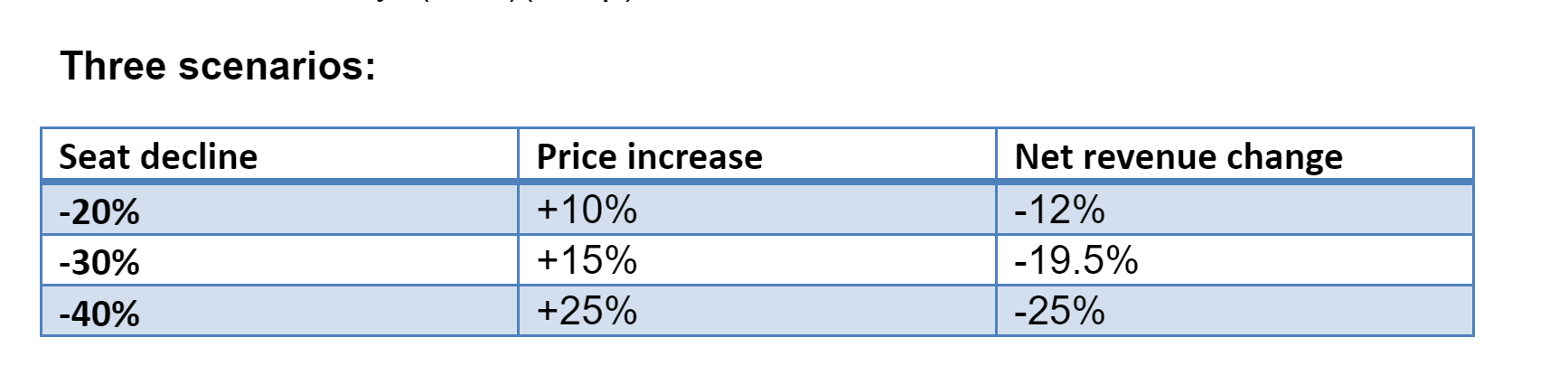

Consider what happens when AI tools make workers meaningfully more productive. A simple sensitivity analysis shows the problem. Let seats drop by s% and price per seat rise by p%. Revenue scales by (1 - s)*(1 + p)

In plain English: Even if you successfully raise prices by 25%, if your customers need 40% fewer seats because AI makes their workers more productive, you still lose a quarter of your revenue. You can win the pricing negotiation and still lose the revenue war.

This is the nightmare: you can raise prices and still lose revenue because the billed unit is collapsing. At that point you have a pricing instrument problem. Seat-based subscriptions are miscalibrated. Outcome/workflow pricing starts looking inevitable.

But outcome pricing has a hidden cost: it forces renegotiation. It’s not “add AI and enjoy expansion.” It’s “re-contract the relationship while competitiors and platforms are trying to commoditize you.”

Real-world evidence is already emerging:

Zendesk and other support platforms are seeing customers consolidate seats as AI handles tier-1 queries.

Salesforce is navigating this by shifting to consumption-based pricing for AI features, but that means abandoning the seat-based model that made them predictable.

But it gets worse for the SaaS companies. AI introduces variable COGS (cost of goods sold) into businesses built for fixed-cost economics. This is the underappreciated killer. SaaS historically has a beautiful cost structure: ship once, serve many times, mostly fixed costs, gross margin stability. Your operating leverage is the whole point.

AI features drag you into a different game: variable inference costs that scale with usage. Here’s a toy example:

c = cost per AI interaction (in dollars)

n = AI interactions per seat per month

AI COGS per seat per month: c × n

Now anchor it to a familiar SaaS price point:

Assume $100/seat/month.

If you want to preserve 80% gross margin, your total variable costs must stay under $20/seat/month.

Suppose your non-AI COGS is $15/seat/month (85% GM baseline).

That leaves only $5/seat/month of headroom before gross margin falls from 85% → 80%.

So you can ask a brutally concrete question:

How many AI interactions per seat can you afford before you’ve permanently reset your margin structure?

If c = $0.002 per interaction, then n = 2,500 interactions/month hits $5.

If c = $0.01, then n = 500 interactions/month hits $5.

In plain English: Once your product shifts from “dashboard you check occasionally” to “copilot you interact with constantly,” you can hit cost breakpoints surprisingly fast. A support rep using an AI assistant 50 times per day across 20 working days is already at 1,000 interactions per month. An engineer using AI code completion? Easily 100+ interactions per day.

The twist: competitive equilibrium might force you to eat that cost. If the AI features become table stakes, you can’t always pass the variable COGS through. You either compress gross margins or you lose deals.

This is how SaaS turns into something more like a consumption business, with different multiples.

And then there’s rebundling. 2010-2022 was an unbundling era. Cloud + APIs + distribution fragmentation created a thousand SaaS categories. Point solutions could thrive because software was modular and buyers were willing to stitch toolchains together.

LLMs push in the opposite direction:

They make “good enough” feature replication cheap

They allow platforms to ship broad capabilities across many workflows quickly

They collapse the value of “thin UI around a common job-to-be-done”

So even if total demand rises, capture can shift up (platforms/suites with distribution) or down (infra/models close to the user). The middle layer of software-only point solutions without an anchor gets squeezed.

Some examples of this in action:

Microsoft ading AI writing assistance directly into Office 365 threatens standalone tools like Grammarly and Jasper.

Salesforce’s Einstein Copilot bundling features that previously required separate point solutions.

Notion and Confluence adding AI that can replicate functionality from specialized knowledge management tools

Browser vendors (Arc, Chrome) embedding AI features that threaten standalone productivity tools

This isn’t an “AI will replace software” claim. It’s a claim about where value accrues in the stack. Point solutions that can’t defend their position get compressed from both sides: platforms above them bundle good enough versions, while users below them can increasingly access raw model APIs.

The result: even companies that solve the seat compression and COGS problems still face a distribution crisis. They’re playing defense on pricing and defending their right to exist as standalone products.

Two Repricings, Two Different Questions

There are two stories in the software wreckage:

Macro repricing: Higher rates punish long-duration cash flows. That forces discipline.

AI repricing: Seat-based pricing and fixed-cost economics get attacked, while the stack rebundles. That forces a business model rewrite.

The first monster changes the price of software stocks. The second changes the nature of many software businesses.

For operators:

Don’t just “add AI.” Decide what your unit of value is when humans aren’t the unit of labor anymore—and whether you’re willing to run a variable-cost business. If you’re still seat-priced in 2027, you either have a spectacular moat or you’re about to learn you don’t.

For investors:

Don’t just ask “who has AI features?” Ask: Who still has a durable right to charge, and who can do it without turning gross margin into a random walk? The companies that win won’t be the ones with the best AI—they’ll be the ones whose business model still works after AI becomes table-stakes.

The delayed reckoning isn’t just about SBC or cost discipline. It’s about whether “SaaS” is still the correct noun for describing what these businesses actually are.

If you enjoy this newsletter, consider sharing it with a colleague.

I’m always happy to receive comments, questions, and pushback. If you want to connect with me directly, you can: