CoreWeave, the AI infrastructure company that went public in early 2025, carries $14.2 billion in debt on its balance sheet. That’s not unusual for a cloud infrastructure company, except CoreWeave isn’t financing data centers or fiber optic cables. It’s financing GPUs. Billions of dollars secured primarily by NVIDIA H100 and H200 chips.

This represents something unprecedented: semiconductors being structured like infrastructure assets. As one legal analysis notes, “GPUs are evolving from mere compute tools into strategically significant financing components—forming a new asset class at the heart of global AI infrastructure.”

But here’s the tension: traditional financeable assets have durability. Boeing 737s generate cash flows for 20-30 years. Municipal bonds pay out over decades. The entire machinery of modern finance, including valuation models, securitization structures, and derivatives markets, assumes assets retain value long enough for these instruments to mature.

GPUs might be technologically obsolete in three years.

This essay explores what happens when Wall Street builds trading infrastructure for ephemeral assets. The transformation is accelerating, but the market lacks the primitives of mature asset classes: standardized valuation, liquid secondary markets, robust derivatives.

A financial asset has quantifiable value, generates cash flows, can be transferred with clear title, and has transparent price discovery. A financeable asset adds the ability to serve as collateral, predictable depreciation curves, stable cash flows, established legal frameworks, and liquid secondary markets.

Real estate is both. Cryptocurrency is arguably financial but inconsistently financeable. A Boeing 737 is highly financeable after decades of aircraft leasing created robust frameworks.

GPUs? They’re becoming both, but the infrastructure remains immature, and unlike 737s, they face obsolescence before loans mature.

According to analysis of GPU-backed credit markets, “In just 18 months, GPUs-as-collateral went from a quirky experiment to a $10 billion-plus segment of the structured credit market.”

The timeline: CoreWeave’s $2.3 billion facility in August 2023, Lambda Labs’ $500 million “first-of-its-kind” GPU ABS in April 2024, CoreWeave’s additional $7.5 billion in May 2024, and a $2.6 billion facility at improved terms in January 2025.

The mechanics mirror traditional ABS: special purpose vehicles hold GPU assets, UCC-1 filings perfect security interests, chips and compute revenue serve as collateral.

But pricing reveals frontier risk. CoreWeave’s early facilities carried SOFR+13%. By early 2025, AAA-rated GPU ABS priced at ~110 bps. Spreads compressed from 1300 bps to 110 bps in eighteen months.

Here’s a structural dynamic that deserves scrutiny: NVIDIA often invests in companies, like CoreWeave and Lambda, that then use NVIDIA’s products as collateral to buy more NVIDIA products.

From NVIDIA’s perspective, it’s vertical integration: invest in customers, ensure they can afford your products, capture hardware sales and equity upside. From a lender’s perspective, it’s reassuring: NVIDIA’s investment signals confidence. From a systemic perspective, it’s concentration risk. Compare this to Boeing Capital financing aircraft purchases. Boeing’s aircraft had 20-30 year useful lives. NVIDIA is doing the same for assets that might be obsolete before loans mature. The model assumes continuous technological advancement creates continuous demand for older-generation compute. If that assumption breaks, the circularity becomes a spiral.

Valuing a GPU depends on current earning power, obsolescence trajectory, residual value, operational costs, and redeployment optionality. Current pricing is fragmented: H100s sell for $25-40K new, but secondary market pricing varies wildly (<1yr: $18-25K; 1-2yr: $12-18K; 2+yr: $7-12K). Cloud rental rates collapsed 44% to $1.80-$4/hour as 300+ providers entered the market.

The depreciation controversy exposes uncertainty: Amazon shortened GPU depreciation from 6 to 5 years in February 2025. In the same month, Meta extended from 5 to 6 years. Same technology, opposite decisions, representing a potential $176B earnings adjustment through 2028.

Industry estimates suggest GPUs retain ~50% of value after 3 years and ~20% after 5 years. These curves would be catastrophic for most ABS. Without standardized methodologies, every deal becomes bespoke and transaction costs soar.

GPU secondary markets remain fragmented across OEM purchases, broker networks, and P2P platforms. But there’s a constraint: GPUs aren’t mobile. Value is tied to power, cooling, connectivity, and location. An H100 in Iceland (cheap power, cold climate) is worth more than one in Singapore.

This necessitates location-differentiated pricing, ownership transfer without physical movement, or tokenized ownership. What’s needed: standardized benchmarking (beyond MLPerf scores), transparent exchange-style marketplaces, and robust data. Silicon Data is positioning itself as “the designated data repository for compute market transactions,” creating transparent benchmarks.

A parallel experiment unfolds in crypto markets. Platforms like GAIB and USD.AI are “transforming traditionally illiquid assets like GPUs into tokenized, on-chain financial instruments.”

On-chain tokenization offers three things traditional finance can’t easily replicate: instant global liquidity (24/7 trading without intermediaries), transparent audit trails (immutable on-chain records), and composability with DeFi (use tokenized GPUs as collateral in lending protocols, bundle into yield-bearing assets, integrate into algorithmic trading).

The catch: regulatory uncertainty, custody risk, and challenges enforcing on-chain ownership claims over physical hardware. But for participants outside traditional banking or seeking exposure without long-term capital commitments, tokenization offers a genuinely novel approach.

In October 2025, Ornn raised $5.7 million for “the world’s first compute futures exchange.” In January 2026, Architect Financial announced exchange-traded futures on datacenter compute, using Ornn’s indices.

The structure is elegant: unlike oil futures settling on spot price, compute futures use “Asian-style” settlement—paying out based on arithmetic average of daily index values, mirroring how compute is actually consumed as a flow over time.

Derivatives enable: AI companies to lock in compute costs, GPU owners to stabilize revenue and presell capacity, lenders to hedge depreciation risk, and speculators to gain exposure. Ornn projects compute futures could reduce capital costs 20-40%, with a potential $5T derivatives market.

The buildout happens in phases: cash-settled compute futures (now), physical GPU futures (emerging), options/volatility products (2-3 years), and eventually exotic structures like obsolescence insurance. Critical to all: index development. Ornn’s OCPI is “built on real transaction data from live GPU markets.”

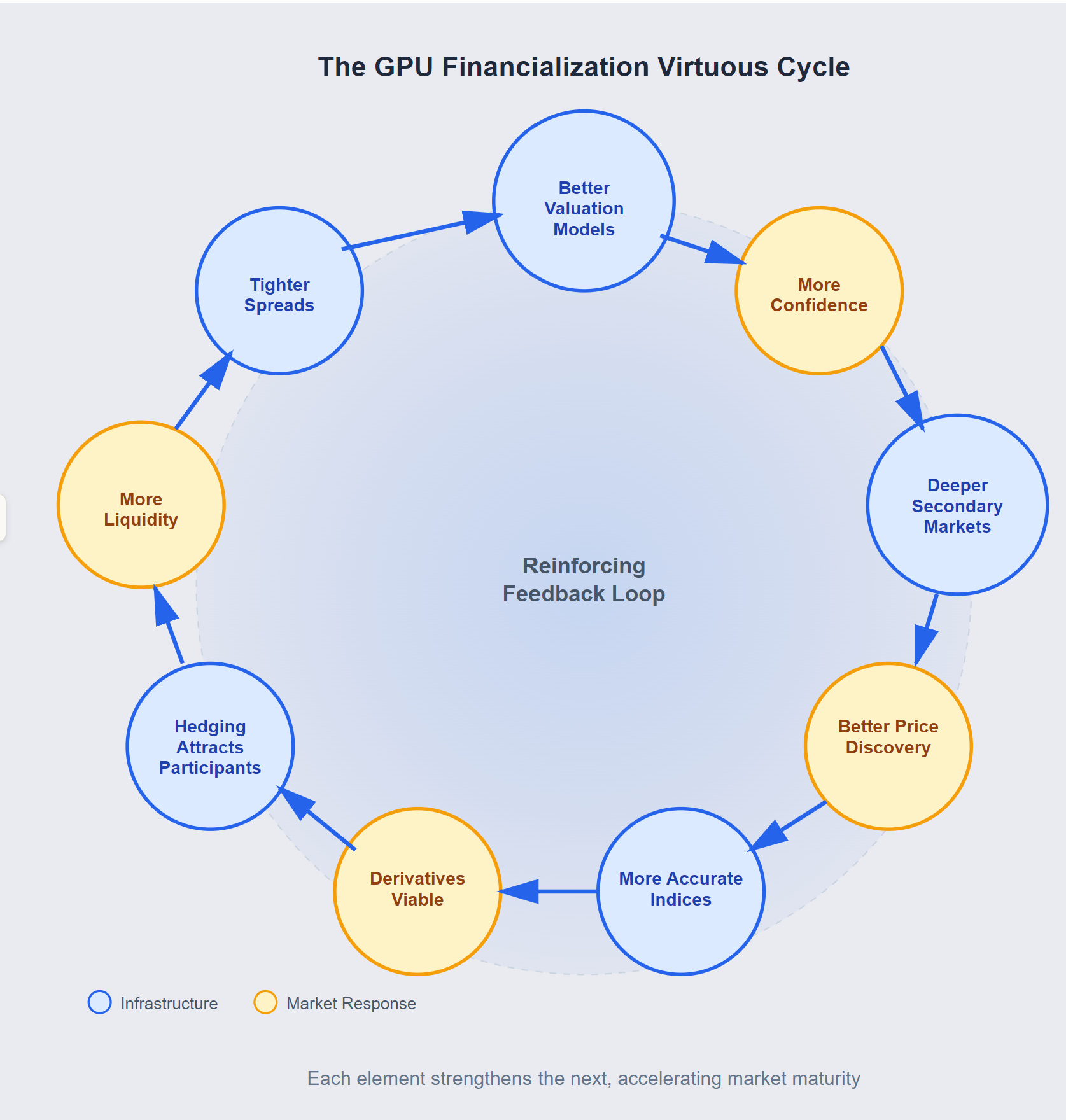

Valuation, secondary markets, and derivatives are locked in recursive feedback loops. You need reliable valuation to create liquid markets, but need liquid markets to generate reliable valuations. You need both for viable derivatives, but derivatives improve valuation models and create liquidity.

This returns us to the fundamental tension: can you build mature financial infrastructure around assets that become obsolete in three years?

Traditional financeable assets have durability. 737s generate cash flows for 20-30 years. Automobiles retain value for 5-10 years. GPUs have 3-5 year economic lives. One analyst warns: “If inference demand doesn’t scale 16x as projected, secondary markets will collapse, salvage value assumptions will prove optimistic, and hyperscalers will face forced write-downs.”

This creates extremely steep depreciation curves making long-term debt risky, high uncertainty in residual values, risk that financial infrastructure becomes obsolete faster than the assets, and the cascade assumption problem. If specialized inference chips outperform older training GPUs, the cascade breaks and there’s no secondary market.

If you enjoy this newsletter, consider sharing it with a colleague.

I’m always happy to receive comments, questions, and pushback. If you want to connect with me directly, you can: