This doc aims to explain how traders trade derivatives in the contract world and how impact the underlying instruments in the real world.

Before I head into the how and why, will cover the what first.

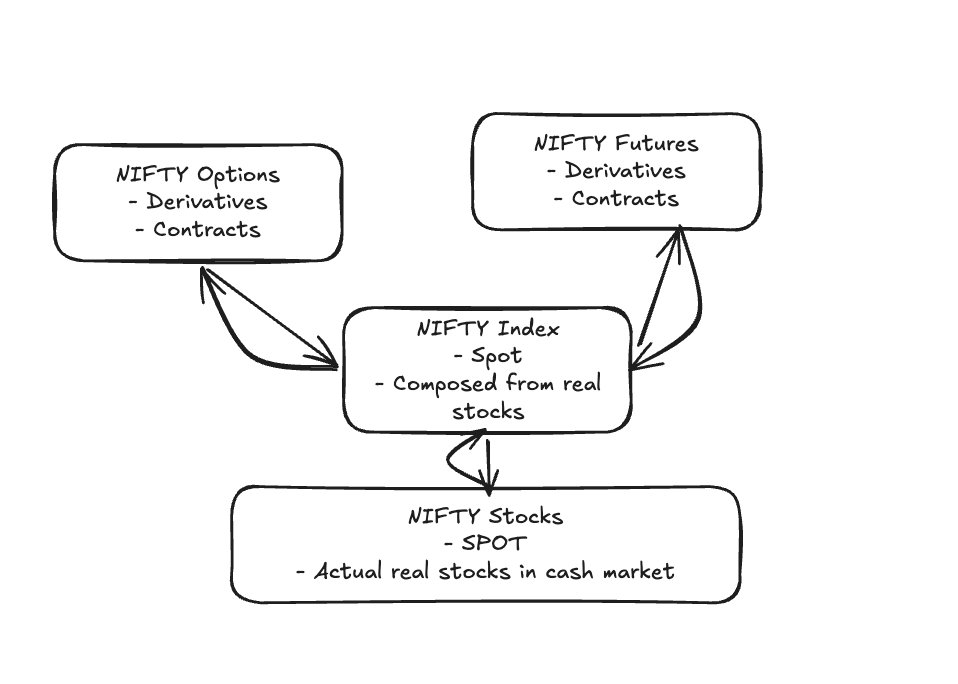

NIFTY is a benchmark index designed to track performance of 50 stocks that represent India listed on NSE.

NIFTY futures or NIFTY FUT are derivative contracts whose underlying is the NIFTY 50 index. The underlying instrument is also called as “spot”. The word contract means that its just an agreement between a buyer and seller speculating on where the NIFTY will be in the future. You are not trading the actual stocks but the expected value of the index. To put it simply you are placing a bet.

NIFTY options are another type of derivative contracts whose underlying is NIFTY 50 index. In these contracts, the agreement gives the buyer the right but not obligation to buy NIFTY at a pre determined price (strike price) on or before a certain date. Now you are no longer trading actual stocks or the expected value of it, you are trading the probability and expectation of where the index may move. Your bet is on direction, range & volatility.

Suppose you and a sweets vendor agree today that on 1st March you will buy the sweets from him at 50$ each. This agreement means that whatever happens, you’d pay 50$. On 1st March, if the price of sweet is 80$ then you would make a profit of 30$ / sweet. If the price of sweet is 30$, you’d make a loss of 20$. Futures contracts have obligation to settle (cash-settled for index futures). At the time of date of settlement, the difference is paid to the winner.

Options are of two types. Call & Put.

Suppose instead of agreeing on the price of the sweet, you decide to pay the vendor 10$ to be able to buy the sweets for 50$. This is called a premium. If the price of the sweets rise to 70$, you can exercise your right and make a profit of 10$ (70 new price-50 decided price -10 premium). If the price of sweet drop to 30$, you had agreed to buy it for 50$ by paying a premium for 10$. Your best choice is to not exercise your right to buy and just take the premium you paid for it as loss.

Call options are right to buy, Put options are right to sell.

In this hypothetical scenario where the prices of sweets are moving too much, a gambling person with no appetite for eating sweet would still want to make money based on his predictions. Say the person believes that the sweets are overvalued at 80$ and the people wouldn’t continue to buy it at that price, so he guesses the prices would go down. In this case, the person would pay the the vendor 10$ to get the right to sell the sweets at any point in the month for 80$. If the price of the sweet goes to 40$, the person would make bank of 30$ / sweet (80 old price he can sell at - 40 new price - 10 premium). If the price of sweet goes up to 100$ the gambler would best not to exercise it and just book the 10$ premium as loss.

Indian markets are biggest in the world in the quantity of derivatives we trade. What that means is its also the most liquid. Our regulatory bodies are the most strict when it comes to making it difficult for an average person to enter the markets for just speculation. Clearly - our derivative markets have a strong opinon on how our markets would be doing. However, as established earlier, derivatives are ultimately contracts where participants bet against each other, not transactions involving the actual underlying stocks or index. My area of interest is understanding how much these derivative markets influence movements in the spot market.

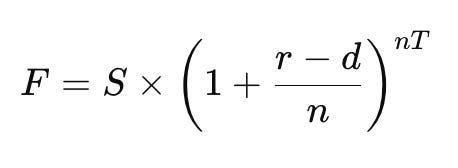

This is the discrete compounding futures pricing formula. Where F is futures price, S is spot price, r is annual risk free interest rate, d is the annual dividend yield, n is number of compounding periods per year, and T is time to expiry.

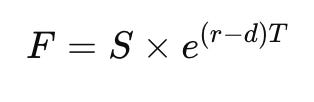

Since the markets continously compound every instant, calculus simplifies the formula to be above.

Just like every other instrument on the market, if the demand is higher than the supply one could expect the prices of that instrument to go up and sometimes skyrocket.

Does this formula predict NIFTY futures accurately?

Approximately - yes. And you can thank arbitrage for that. This answers most doubts around why the pricing formula works. You have to trust the system to continuously correct itself to honor certain financial principles.

If the formula were not followed, it would imply the existence of risk-free profit, and markets do not allow that to persist.

If the futures price is too high relative to fair value, a trader would:

Sell NIFTY futures

Buy the NIFTY spot basket (or equivalent exposure)

This creates

selling pressure in futures, and takes the futures price down

buying pressure in spot, and spot increases

This continues till the formula holds true.

Same is true if the futures price is too low, the arbitrageur would just buy futures, and short / sell spot instrument. Following consequences like above till equilibrium is maintained.

To be exact - the formula does not predict futures, it simply anchors where they are allowed to trade relative to spot, if not risk free profit oportunities will arise and arbitrage ensures it goes back to fair value.

Yes, temporarily.

If demand for futures increases, driving the futures price higher, an opportunistic trader (or more likely, a trading algorithm) would short futures and buy spot, pushing prices back toward fair value.

Heavy futures buying lifts futures prices. When traders and systems short futures and buy spot, they end up creating real demand in the cash market. Demand in spot means upward pressure on prices. While this convergence happens, arbitrageurs are effectively buying the underlying constituents of the NIFTY.

The entire system hinges on arbitrage.

It ensures that whenever pricing gaps appear between related instruments, traders exploit them, and by doing so, eliminate the possibility of persistent risk-free profit.

Don’t options seem harmless! They are just bets between traders on how the market / spot would behave at X date. But the nature of how traders trade them moves spot.

When I mentioned above Indian markets are the highest in the amount of the contracts in the derivative markets, you have to also thank system constructs like Market Makers for their role in this.

While trading options, or making a bet between one trader and another, in a liquid market like NIFTY, we actually may not be trading with a human on the other end. If you want to buy a call option (you are being bullish), you would get one. And most often, Market Makers sell it to you.

Market makers primarily make money from bid–ask spreads and rebates, not directional views. But since they just sold you a call option, you have made them just do a directional trade. Now selling calls has made them exposed to Negative Delta (they lose money if the spot rises). To neutralize this risk they need to either buy spot or futures. This is called as hedging.

When you are short, it means you sold something first and have to buy it later.

Imagine markets rising, and many traders already being short, at some point they decide they have had enough losses and its time to close their positions - what do they need to do to book ? BUY.

Enough buying pressure induced drives the market up and makes the rest of the short traders even more nervous and start closing their positions and thus enforcing that rally.

Short covering rally is just one of those market moments, there are others like Gamma Squeeze, Volatility Crush, Put Unwinding, Call Unwinding.

It is easy to walk away with the idea that derivatives always dictate what happens to spot. That is not true.

The futures - options - spot linkage only works when hedging and arbitrage flows are large enough relative to the depth of the cash market. If they are not, derivatives remain what they fundamentally are: contracts between traders.

If calls and puts across strikes offset each other, market makers do not need to hedge much. Little hedging means fewer trades in futures and negligible impact on spot.

The NIFTY cash market is extremely deep. FIIs have been net sellers for long stretches, yet prices still rise because domestic mutual funds, SIP flows, and institutions absorb supply. The sheer amount of liquidity in the cash market can sometimes dwarf derivatives-driven flows and give cash the final say.

That does not mean futures and options do not drive spot. They do. But fundamentals and cash flows usually dominate direction, while derivatives tend to amplify, dampen, or shape short-term moves.