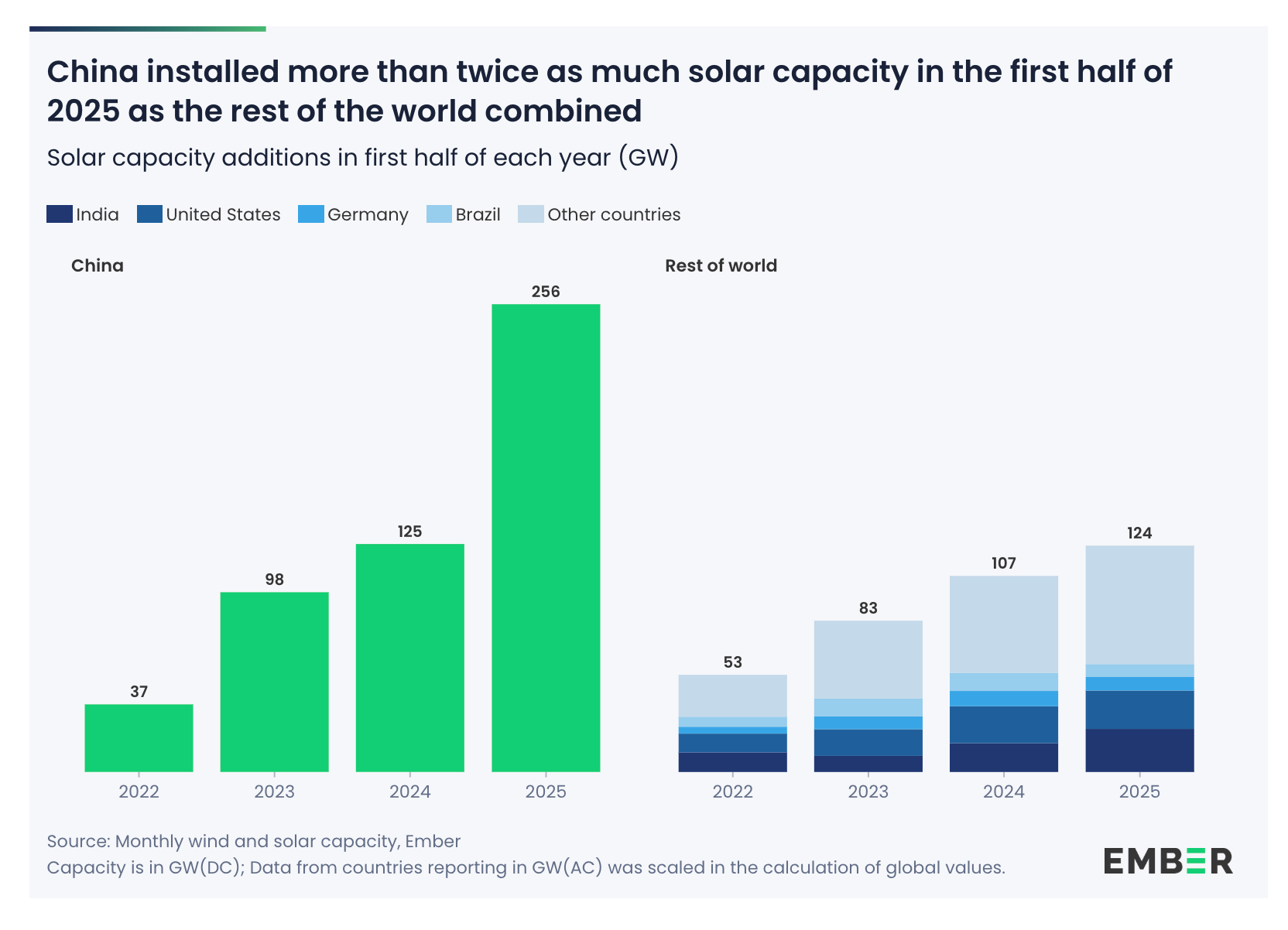

In the first six months of 2025 China installed more than 250GW of solar power capacity. That staggering figure from the think tank Ember is measured on a comprehensive basis including decentralized solar and is somewhat larger than the official number released by the Chinese Energy Administration, which was a barely less staggering 212 GW.

Source: Ember

In several different places I’ve been trying recently to find ways to grasp and convey the scale of economic history-making going on in China. The Chinese solar numbers are the latest challenge.

China’s new-build solar additions in the last six months are more than the US has installed in total: China Flow > US stock. Germany was once the global champion of solar. China’s new additions in six months are two times Germany’s installed capacity.

In the first half of 2025 China’s new additions were more than twice the new capacity installed by the entire rest of the world this year. The #2 on the list, India, installed 24GW. The US at #3 installed 21GW. There is an order of magnitude difference.

Is the comparison unfair to the US? After all, the US green energy push has been thrown off the rails by Trump’s administration. Ok. Take 2024, the heyday of Bidenomics and the IRA. In that year, the US installed a “record-breaking” 50 GW of solar (all in, distributed and grid). On an annualized basis that is one tenth the rate of install achieved by China in the first half of this year. Now the US electricity system is much smaller than that of China. But it is not one tenth, it is half as large as its Chinese counterpart. Scaled by underlying capacity, in the best year of Bidenomics the rate of solar install was one fifth China’s surge in H1 2025.

There are distorting factors in play on the Chinese side. The H1 2025 figures reflect the late stage of a Five-year plan and an imminent shift in subsidy regime. Chinese businesses (and consumers) are hyper-reactive to incentives.

There is little doubt that H2 2025 will see a slowdown. The upward path of Chinese renewable investment has not been steady. The memory of the savage shakeout in the late 2010s lingers in the industry. A new policy regime in the second half of 2025 is forecast to result in a serious slowdown. The annual new installation in 2025 is likely to be only 50 greater than that achieved in the first half of the year - 300-310 GW on the national energy agency basis. That would compare to 277 GW installed in 2024 and global build out in 2025 expected to be between 650 to 700 GW.

And the remarkable fact is that China could do far more. Earlier this year the capacity of China’s PV Industry at full stretch was guesstimated at 1200 GW of solar PV per annum. That huge capacity is the result of helter-skelter private sector innovation and ambition and successive waves of subsidy, at both national and local level. National subsidies began with the 2009 financial-crisis stimulus. National backing was dramatically amplified by local and regional efforts. Cumulatively the sums added up to tens of billions of dollars. One frequently cited figure attributed to the Wood MacKenzie consultancy is $50 bn in Chinese government subsidies to solar manufacturing over the period 2011 to 2023.

If those numbers are approximately accurate, it was a spectacularly effective use of public funds, a world-transforming industrial policy no less. We should be asking ourselves why no government in the West ever attempted anything so bold, or frankly had any prospect of getting so much bang (in terms of manufacturing capacity) for so few bucks ($50 bn is comparable to the US CHIPS act, or one year of German defense spending).

Clearly, 1200 GW of solar PV manufacturing capacity is far ahead of current demand and has led to painful commercial pressure in the Chinese industry and government-led efforts to consolidate the industry and rationalize supply. Underused factories cost real resources which weigh on Chinese living standards. They contribute to the lopsided pattern of Chinese growth that represses the Chinese standard of living. But a path to climate stabilization requires an annual new installation of between 700 and 1000 GW globally, for the foreseeable future. So, the capacity that China has built is not excessive. It is precisely on the scale that the planet needs. If we are to have any hope of actually achieving climate stabilization, China is our main pillar. As Wood MacKenzie puts it: “an energy transition without Chinese supply chains is unthinkable.”

The point is that once again China is teaching us to think at scale. The future scale of a more developed, post-Western world is gigantic. If we are to have any hope of climate stabilization the only realistic policy, therefore, is not some twee Western European vision of “sustainability”, it is radical and transformative. Cities will be bigger, energy needs will be bigger, production will be bigger than anything we have previously conceived. 1200 GW in PV manufacturing capacity not crazy. It is, give or take, right-sized.

Renewable power has to force its way through. Given the obduracy of politics and the entrenched political economy of fossil fuels, clean energy needs not just to be efficient, or optimal, it needs to be bludgeoningly, overwhelmingly, unanswerably DOMINANT. We need even the last die-hard fossil hold-out to understand that the map of power generation looks like this.

It should be great news in this context that Saudi Arabia has become a major importer of Chinese solar panels.

Rather than moaning about subsidies we should recognize that China is the only large country driving the energy transition at anything close to the necessary speed and scale. The question should be how to build markets for China’s solar panels both at home and around the world.

If this raises security concerns, let us address those whilst we figure out how to install the GW of panels we need. After all, the panels are the relatively simple and safe bit. If inverters and control of systems are an issue, let us figure out protocols for addressing those concerns. If long-term supply diversification is an issue, let us work towards redistributing capacity. But as far as the climate crisis is concerned, we do not have time. It is bad enough to fail to invest in the energy transition. It is a scandal of an even greater order to refuse to make use of green energy capacity that has actually been built and paid for by someone else.

In China the huge surge in renewable energy capacity may be turning the balance of emissions. Don’t stake your life on it, don’t shout it too loudly, but the latest data suggest that China may have peaked. When I mentioned this data to folks in the State Council apparatus in Beijing, they were a bit surprised and went away to check their own figures. They never came back to tell me what they found.

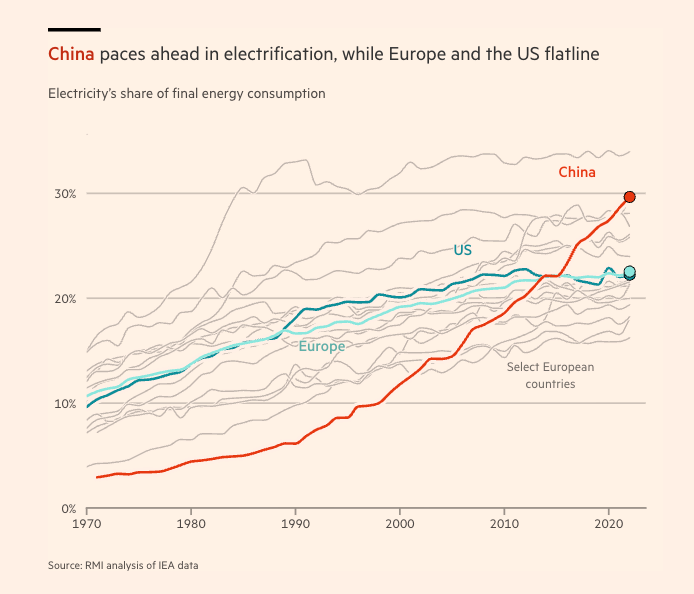

We need the solar momentum to keep building. China needs to keep pushing its own electrification (more on this in another Chartbook soon). It needs to go on shifting electricity demand. It needs to go on electrifying and building its “electrostate”. This was one of the other striking graphs of recent times, from the FT report.

Whereas in Europe and US the share of electricity in final energy consumption is stuck at 22 percent and has been for more than a decade, despite all the huffing and puffing about decarbonization, in China, electricity’s share has risen to 30 percent and the trajectory is steeply upwards. (The high-side outlier, btw, is Japan). Electrification, because we know how to produce it with low emissions, is the gateway to cleaning up the energy system.

Of the solar panels that Europe is installing at an accelerating rate, 95 percent come from China. The EU has a 40 percent local content goal by 2030. One can only hope they don’t take that too seriously. The US is the exception in avoiding direct imports of Chinese PV, instead sourcing its panels by way of connector countries. But you have to be a true MAGA believer to think that solar electrification is not going to happen in the US too (more on this to come).

The really exciting vista opened up by China’s extraordinary solar boom are the possibilities it offers for the low income and developing world.

As I’ve been at pains to insist in Chartbook, the low income and developing world is NOT “one story”. We need to distinguish two polar types. On the one hand there are the rapidly growing countries like India with low per-capita power consumption. Then, on the other hand, there are the poorest of the poor in fragile and conflict affected situations where the problem is not how to power growth, but how to avoid a spiraling descent into ever deeper misery. Those in the growing but underpowered category number in the billions. Those with no electric access at all number around 750 million. For both it is nothing short of obscene to describe dirt-cheap Chinese solar panels and batteries as “excessive”.

Perhaps the very best news of the last few months have been the reports showing the impact of the Chinese solar boom on the developing world.

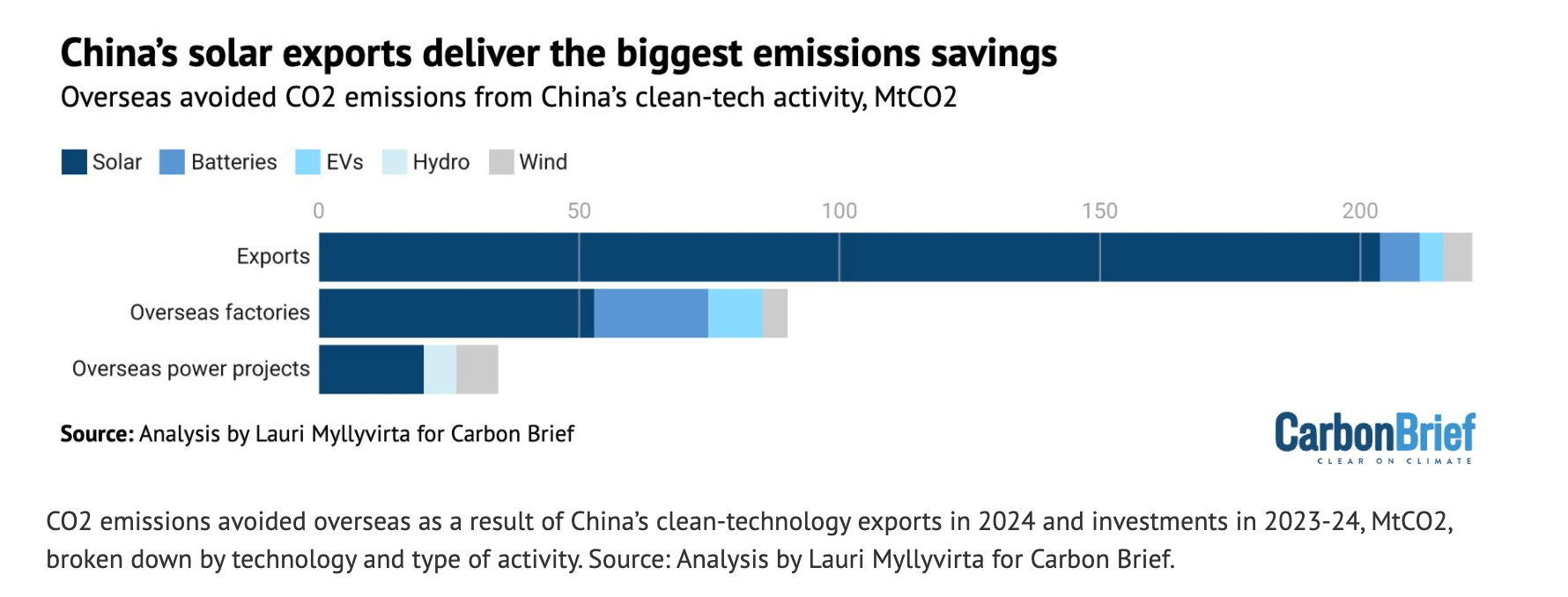

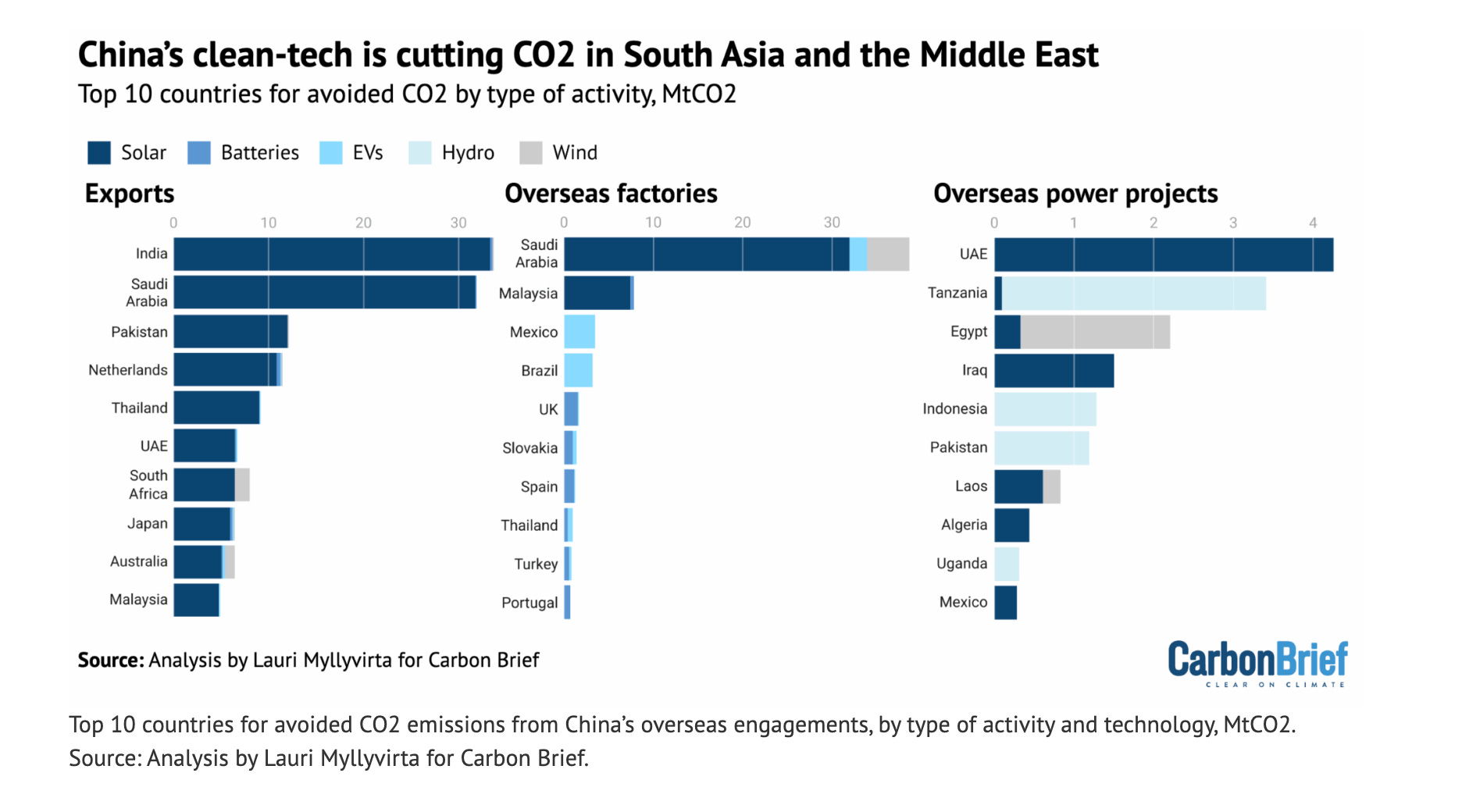

Across Asia China’s solar exports are slashing future carbon emissions. Look at the figures for exports to India, Saudi and Pakistan, weighted in terms of emissions abated, and look at the manufacturing and power projects in Saudi Arabia and the Emirates. If the US won’t power AI data centers with renewables at home, and prefers a steampunk model relying on 19th century furnace-and-turbine technology (Fickling), perhaps Trump’s geopoliticking will allow solar power AI to happen, at least in the desert.

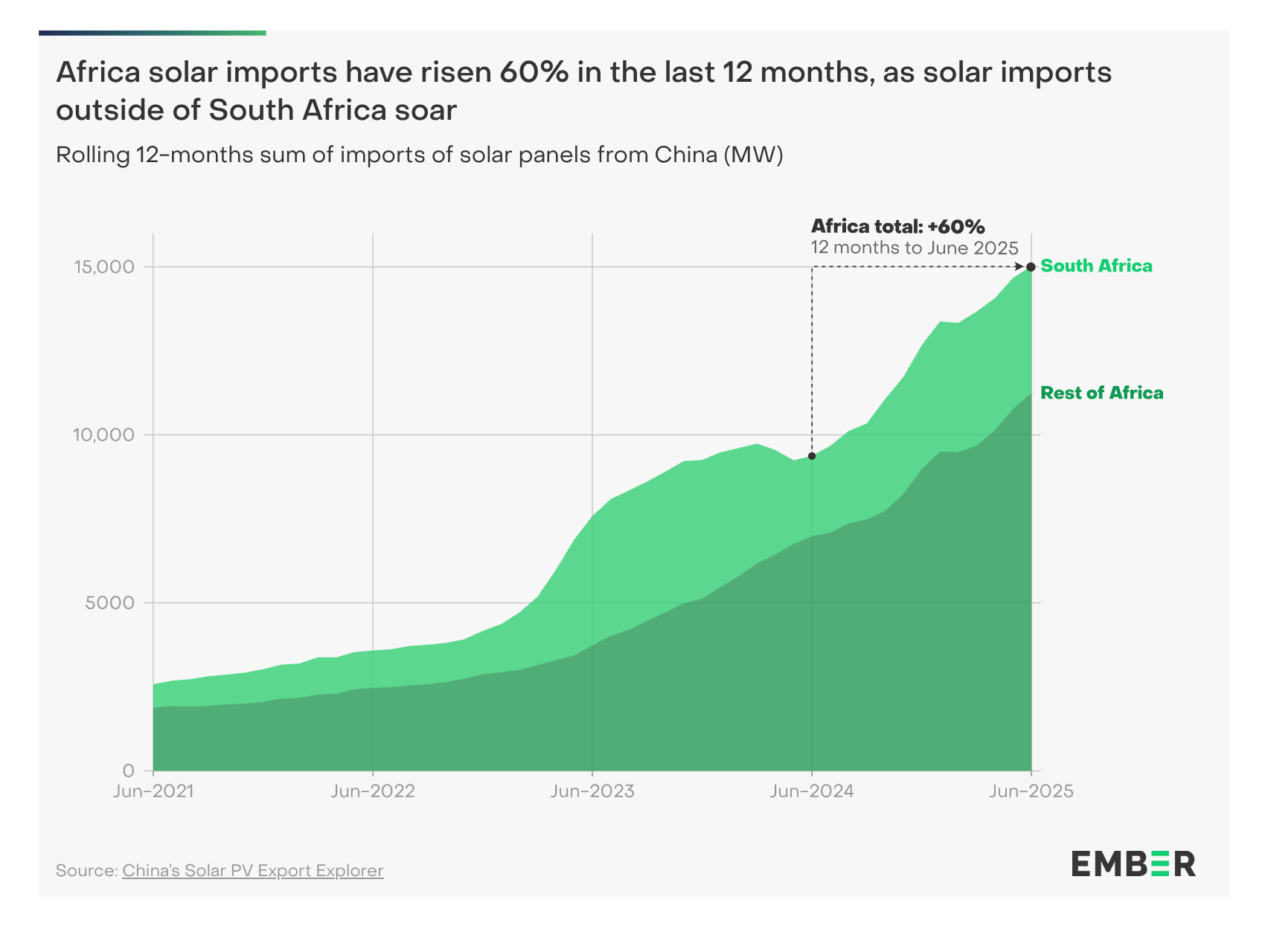

At the other end of the scale of electrification and poverty, there is extremely encouraging news of a surge in Chinese solar panel exports to Africa.

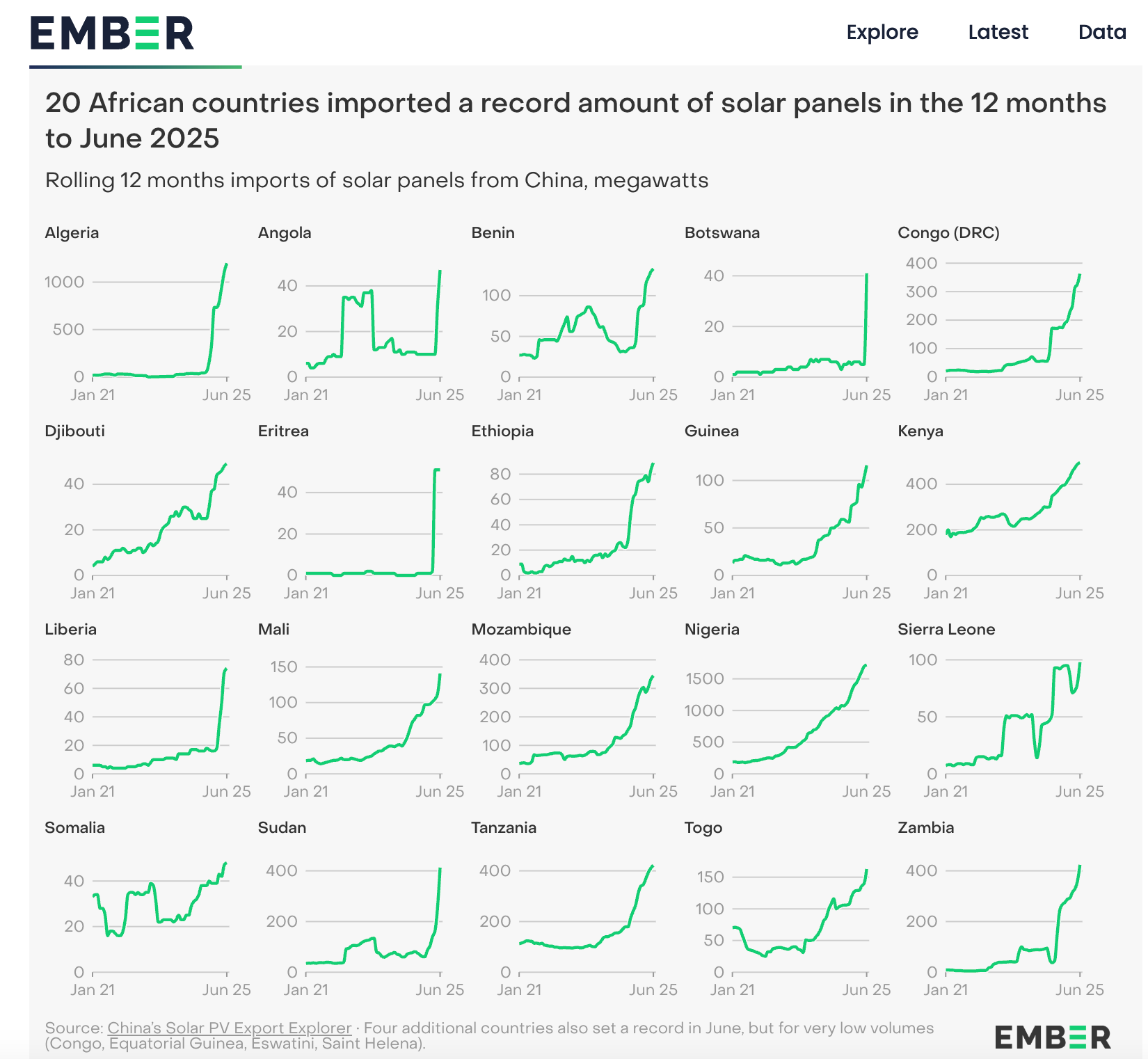

Look at the sudden leap upwards in imports on a country by country basis.

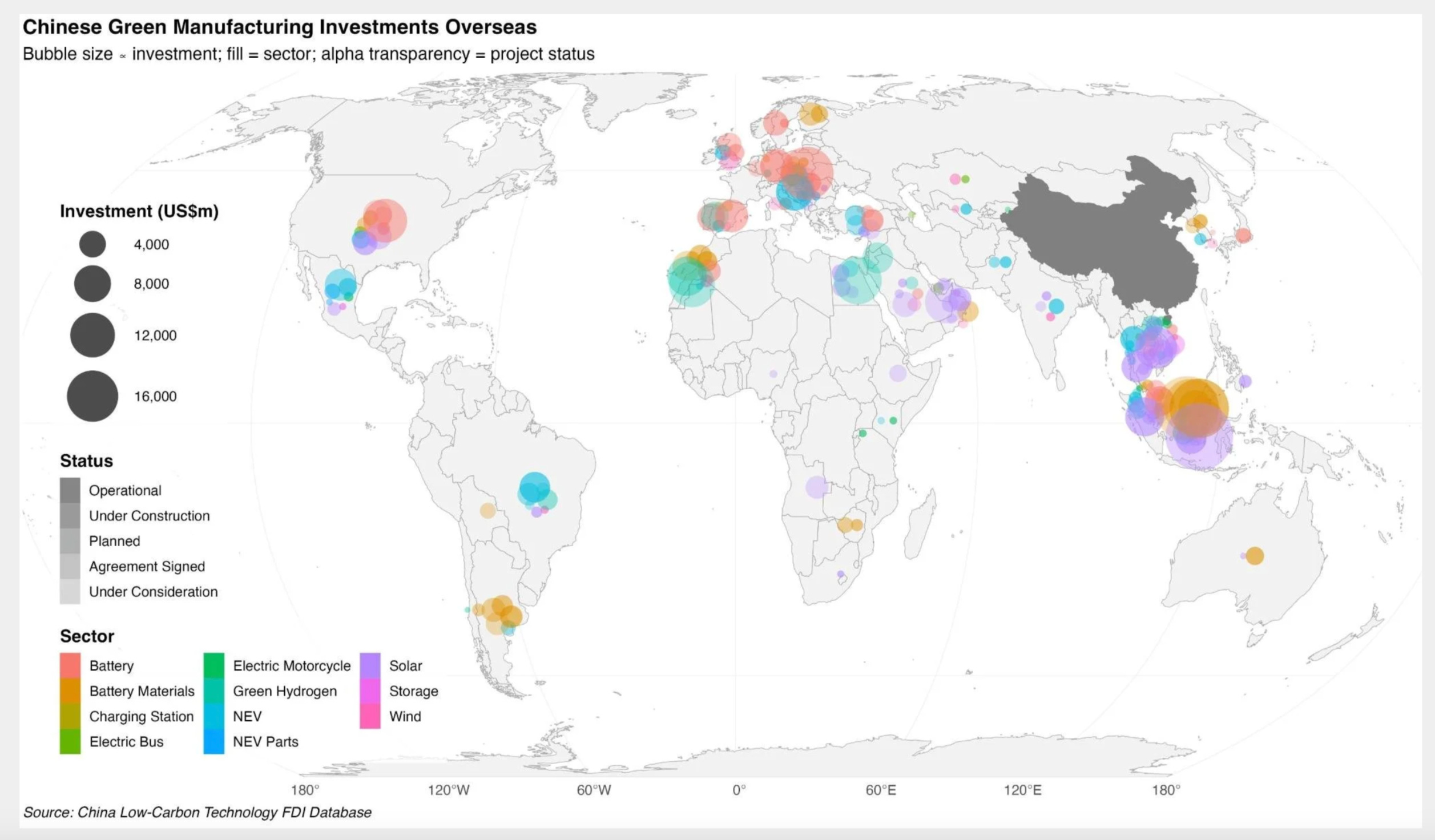

And China is not just exporting panels, since 2022 it is also engaged in huge FDI in manufacturing. My friends at the Net Zero Policy Lab at Hopkins together with Boston University’s Global Development Policy Center have prepared a remarkable data base on China’s overseas green manufacturing investment. I will come back to these numbers because they go beyond solar. But they are welcome sign of the proliferation of Green energy manufacturing capacity.

You might ask, why add to capacity when we already have too much? But as David Fickling at Bloomberg points out: more local capacity easily spills over into more local demand-ambition.

A solar panel factory established the same month east of Jakarta could churn out 1.6 gigawatts of modules each year, enough to provide nearly all the additional 17.1 GW of photovoltaic generation Indonesia had been forecasting up to 2035. With capacity growing so fast, ambitions are accelerating, too: Last month, the government announced it was working on increasing its solar target six fold, to 100 GW.

This cycle is precisely what we need. China is teaching the world to think big.

Of course, Trump will go on thumping around the world demanding that trade partners take whatever quantity of American LNG that he demands. And some will say yes. But as Fickling writes:

“Right now, Beijing is offering cheap, clean power, employment, trade and a route to prosperity. Washington is offering tariffs, policy chaos, White nationalist memes and South Korean workers in shackles after a raid on an EV battery factory. This is no way to win the grand strategic contest of the 21st century.”

That is an understatement. When thinking about global policy we unfortunately still tend to Euro-size ourselves and center the mid-(20th)century US as the gold standard, evoking episodes like the Marshall Plan. What has happened with China’s green energy revolution in the 2010s and 2020s is more expansive and consequential than that. In technological terms, this isn’t like 1940s postwar reconstruction or “catching up”. This is more innovative. It is more akin to the truly expansive phase of steam power in the 1820s, widening out from its restricted 18th-century base in isolated parts of industrial Britain. It is more like models of mass production proliferating beyond Ford and Detroit over the decades between the 1910s and the 1950s. That the Marshall Plan even comes to mind reflects the fact that the Cold War has never left us and that in China’s green energy revolution there is deliberate policy intent at work, not in the details, or in command and control, but in the general direction. But that makes this reality only more dramatic. Solar and batteries (combined in China itself with ultra-high voltage long range transmission) are something akin to a general purpose technology being driven to planetary scale over a period of no more than two decades by CCP-led China. And this technological set is not just general purpose and affordable, it is our only adequate response to date to the diagnosis of climate emergency. My sense is that many folks in the West are working quite hard to avoid the obvious, though daunting, conclusion that this combination of criteria marks the opening of a new epoch of world economic history.

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you will receive the full Top Links emails several times per week.