Neal Stephenson is among my all-time favorite authors. Many dozens of hours of my youth were spent lost in the pages of a Neal Stephenson book, and yet I do not consider these hours "lost" in any way. Though Stephenson is best known for visionary science fiction, he is equally skilled as an ethnographer of geeks. As if that weren't cool enough, he occasionally serves up highly insightful commentary on the state of innovation.

Yet like his one-time protagonist Isaac Newton, Stephenson has always had a few curious obsessions unrelated to the main body of his work. Prominent among these is his interest in the phenomenon of money, which plays some kind of role in nearly every Stephenson yarn. Despite his general perspicacity, I'm afraid that Stephenson is as much of a mystic when it comes to monetary economics as Newton was when it came to alchemy.

For example, take his 1995 story, "The Great Simoleon Caper", in which he presages the development of a Bitcoin-like alternative currency. In that story, a protagonist laments the damage that inflation is doing to his savings:

I graduated college with a thousand bucks in savings. With inflation at 10% and rising, that buys a lot fewer Leinenkugels than it did a year ago.

Now, this is believable - a kid just out of college might be silly enough to keep his nest egg in a checking account even in a time of 10% inflation. But if he had half a milligram of sense, the kid would buy something whose interest rate was adjusted for the 10% inflation.

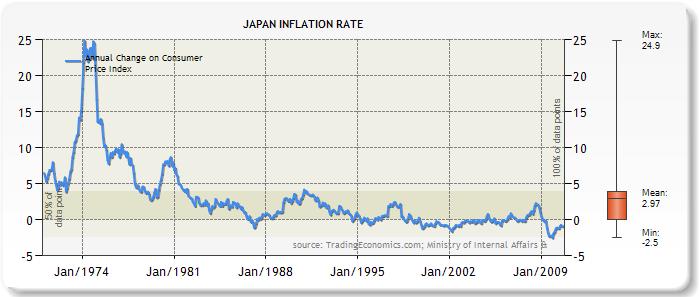

Remember, unexpected inflation hurts savers, but expected inflation doesn't. If inflation runs at 10% forever, people will just structure their nominal debt contracts to take this into account, by raising the nominal interest rate. In fact, this happened in response to the persistent inflation of the late 70s:

\

\

It's the unexpected swings in inflation that take away the ability of your savings to buy Leinenkugels (whatever those are).

On the next line, Stephenson offers an explanation for inflation:

"The government's never going to get its act together on the budget," Joe says. "It can't. Inflation will just get worse. People will put their money elsewhere."

This is a theory called the "fiscal theory of the price level", and in Stephenson's defense it has been advanced by a number of prominent economists, including recent Nobel winner Chris Sims. But recent events in places like Japan have not been kind to this theory; even as Japan's government debt has skyrocketed to unprecedented, astronomical levels, the country has remained mired in deflation. Nor is Japan unique in this regard. Of course, Stephenson could not have known in 1995 that this would happen, so let's cut him some slack in this case.

{kind=link}

{kind=link}

In later writings, Stephenson wrestles with the age-old question of what exactly it is that gives money value. In his 2011 novel Reamde, which postulates a Bitcoin-like system merged into a World of Warcraft-style online game, Stephenson echoes a common trope about gold, a metal that in the past was often used to make coins that were used for transactions:

Gold, he learned, was considered to be a reliable store of value because extracting it from the ground required a certain amount of effort that tended to remain stable over time. When new, easy-to-mine gold deposits were found, or new mining technologies developed, the value of gold tended to fall.

Although the phrase "was considered to be" entails a certain amount of ambiguity, Stephenson must be given a rap on the wrist here for failing to notice that gold is not, in fact, a reliable store of value, and has not been one ever since governments stopped fixing the price of the metal. Here is a picture of gold's dollar price from 1970 through 2005:

As you can see, from 1980 through 2000, gold's value fell in dollar terms. If you were a 50-year-old living in 1980, and you bought gold under the impression that it was a "reliable store of value", then by the time you were forced to retire, you would have lost around half of your investment. Yet no major gold deposits or advances in mining techniques occurred between 1981 and 1982, when gold's price crashed precipitously. Gold lost its value because of something unrelated to the difficulty of getting gold out of the ground.

Money is a really weird thing, it turns out. It has to fulfill several roles at once - it has to be a stable short-term store of value, but also a medium of exchange and unit of account. Figuring out how it is that one object can fulfill all those roles - and when one of the roles might come to dominate the others - is no easy task. In fact, it turns out that there is a whole tribe of geeks - several tribes, actually - who have dedicated quite a lot of time and brain power to plumbing the mysteries of money. For example, in this excellent blog post (and also this one), David Andolfatto - a very smart geek who has spent quite a bit of time thinking about the nature of money - explains why gold is no longer used in transactions. (Happily for Stephenson and other Bitcoin fans, it turns out that Andolfatto thinks Bitcoin might someday end up being a lot better than gold - or anything else; see also here and here.)

In fact, the last few years have turned a lot of monetary theories on their head. Quantitative easing, which had scared quite a lot of people about the prospect of high inflation, ended up causing nothing of the kind. Gold climbed to dizzying heights and promptly lost a third of its value. Simple folk theories of money continued to prove incongruent with observed reality.

{kind=link}

Geeks who are interested in money should know that if believers in a gold standard are like alchemists, there are a lot of very smart people out there trying to invent chemistry. The question of money demand is a hard one, and the human race doesn't really have good answers to this question yet. It's not a problem that was solved 400 years ago - it's a problem still waiting to be solved.