Wealth Levels, Wealth Inequality, and the Great Recession [pdf]

web.stanford.eduThis study is misleading, because it uses 'household' wealth, instead of individual wealth, and may be incorrectly interpreted as showing a decline in the middle class, when it is really showing the results of changes in family structure over the past 50 years. This graph shows how this choice affects the results: http://1.bp.blogspot.com/-g3WZGpDibPM/Up3ZAPRtScI/AAAAAAAAJq...

{kind=link}

The following blog-posts go in to more detail:

http://politicalcalculations.blogspot.ca/2013/12/the-major-t...

http://politicalcalculations.blogspot.ca/2013/12/the-widows-...

http://politicalcalculations.blogspot.ca/2013/12/the-men-who...

Supporting 1 person on x income is harder than supporting two people on 2x income. Put simply, a couple does not need two stoves, and any shared trip is less expencive etc. There are a few edge cases at the individual level for things like end of life care and taxes, but the overall economic bennifits are huge.

On the other hand, 1 person with x income pays less income tax than 2 people with 2x income.

The US has joint filing for married couples so that's not the case, whereas it would be in e.g. the UK.

It most certainly is the case in the US... http://en.wikipedia.org/wiki/Marriage_penalty

It's a generally around a 1/2 a % penalty which is swamped by other benefits.

AKA 2 incomes of $87,850 x2 = 175 700 vs extra 879$ in taxes.

At extreme incomes of say 20+M a year or below 18k it's actually far less than 1/2%.

However, there are huge benefits for SS for being a married couple even more so if there is a large income disparity, so on average if they plan ahead Marriage tends to lower taxes. On top of lower expenses which enable better tax avoidance mechanisms.

Irrelevant.

Calling it misleading is stretch. There are dozens of factors that you can cherry pick to cast aspersions on the increase in inequality but if you step back they don't come close to explaining it. There are another dozen that can be chosen that do the opposite.

Very interesting reads, thank you for sharing them.

However, just looking at the time scale over which the net worth changes described in the original article occurred, and their magnitudes, it doesn't seem likely that the effect they describe can be explained so easily by social factors. Hypothesizing that it's just a social change related to shrinking households leads to some interesting questions about what that really means in practical terms: Did the bottom 5% go from an average net worth of -$9K to -27K over the course of a decade because, on average, three individuals in the red would get together to form a combined household with pooled debts? Did the 25th percentile go from an average of $10k to an average of $3k because of parents getting divorced and kids moving out en masse? Meanwhile wealthy people's family structures remain static.

I think the data you link and the data in the article are reconcilable. Income and wealth are different things, after all. Perhaps wealthier folks' net worth dropped less precipitously during the Great Recession because they experienced nothing worse than a drop in the valuation of their primary residence. Meanwhile less wealthy folks suffered a greater loss because they were more likely to get foreclosed on, therefore suffering a loss of all the equity they had built up in their homes. This trend wouldn't show up as much in the income numbers because losing your house doesn't necessarily coincide with losing your job, certainly not the way things were playing out in 2008.

The wealthier folks were simply less leveraged:

1. If you own 10% equity in a home which declines in value 20%, you now have negative wealth. A 200% decline.

2. If you own 50% equity in a home which declines in value 20%, you have suffered a mere 40% decline.

Not sure why someone voted you down, that quite believably would play into it and certainly doesn't seem to contradict the numbers in the paper in any obvious way.

(The wealthiest folks did see an increase in wealth over the 10-year time considered by the paper while everyone else saw a loss, but that's possibly because the wealthiest 10% also had a comparatively smaller amount of their assets tied up in their homes to begin with.)

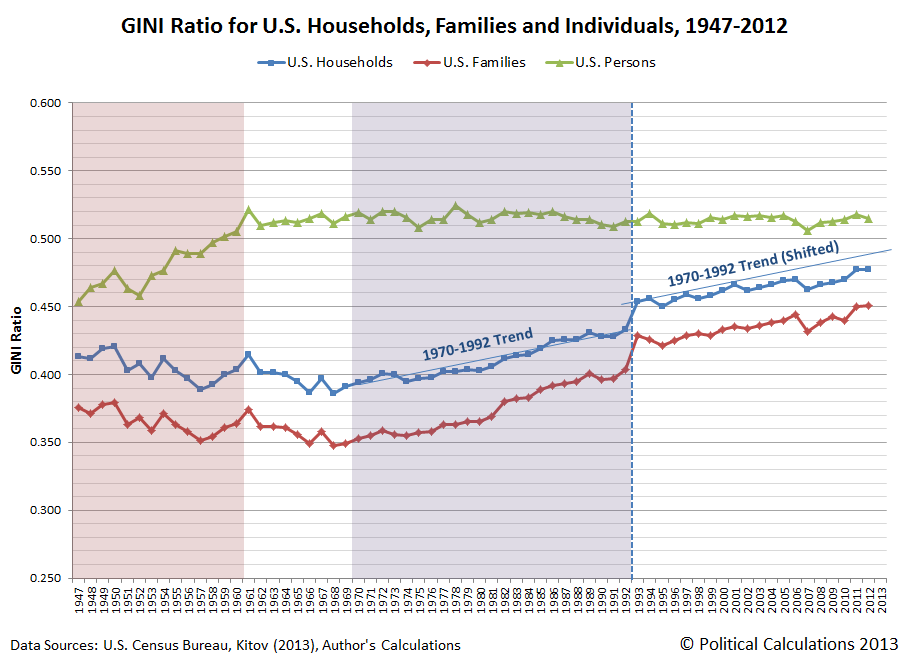

Wow, very interesting that GINI by individual is fairly constant.

However, household GINI is definitely the more relevant figure, as most big economic decisions (where to work, where to live) are made at the household level rather than at the individual level.

But the number of households is strongly influenced by people's personal social decisions such as divorce or living with relatives. Thus the household GINI is strongly influenced by people's personal decisions in addition to their economic circumstances.

More concretely, if I divorce my wife and we become two households does that mean that US economic inequality has increased? I would say not, but the household GINI would say that it has.

If social circumstances make for a increase in divorces or a change in the fundamental structure of the family, I don't see why it's not something to take into consideration beyond "personal decisions".

Could it be that conservatives might actually be right about that?

The point is that it doesn't tell you anything about "wealth inequality" insofar as the socialists whom push this discussion want it to.

Since when is "wealth" inequality a "socialist" thing? It's a matter of such importance that The Economist considers it the most pressing issue in economics of our times.

There is also nothing "socialist" about the publication. And the fact that the stats may be skewed by certain underlying variables (like every other study on Earth, who knew) does not invalidate the findings, although it does invite for further refinement of the data for more conclusive information.

I would say that yes, US economic inequality has increased, quite concretely! Unless you both have precisely the same income post-divorce, as a couple you were more equal than when single.

>>However, household GINI is definitely the more relevant figure...

Not relevant to the point OP made.

Whether or not it's "better," it still impacts the numbers.

Middle class individual income have been stagnant since 1970.

That's interesting, but it makes me wonder about the value of GINI as an indicator if it hides the obviously horrifying effects the 2008 crash had on the bottom quintile and the very bad effects of driving median wealth into negative territory, where it remains stagnant.

I suspect a lot of people reading this board and living in Silicon Valley and other tech boom towns don't feel what that graph is saying in terms of day to day impact.

Your chart shows income distribution, while the linked study is talking about net worth.

You are correct about the chart, but if you look at the second and third blog-posts, you will see how family structure has changed, and how it will have a similar impact on measured household wealth. I wish that I had a similar wealth distributions graph handy, but this was the best source I could remember, and I think it serves to adequately demonstrate the point.

It’s a fair critique, but it really doesn’t come close to explaining the 2003–2013 data.

The ratio of 95th percentile household net worth to median household net worth doubled from ~9x to ~18x. That’s not just some artifact of changing family structures. That’s a massive increase in wealth inequality.

Basically, your point is interesting, but in context it’s mostly a distraction. (But I agree that a chart showing individual rather than household wealth would be nice to see.)

I think you are right that those blogs do not fully explain what happened after 2003. It seems like the measured wealth dip (amongst all groups) from 2007-current is quite consistent with losses due to the drop in housing prices from the great recession (though I have no solid data to back this up). Lower income households tend to have a greater proportion of their wealth tied up in housing (and with less home equity due to a variety of factors including low down payments in those years), so they were likely disproportionately (negatively) impacted.

I am not sure what could explain the changes between 2003-2007, though I would be very interested to hear any ideas.

This study is misleading, because it uses 'household' wealth, instead of individual wealth (...)

Perhaps, but there is no hard data at the individual level because, as it happens, basically every comprehensive dataset on income or wealth relies on tax or census data, which are aggregated at the household level by design. So any empirical claim about individual-level data should be taken ex ante with a big grain of salt and evaluated carefully; especially in a heavily politicized field like economics where data is scarce and motivated reasoning reigns.

Take, for instance, the graph you cite [1], which cites Kitov and Kitov (2013) [2] along with the US census bureau as a source. The problem is, what that paper provides is not an empirical dataset but a microfounded model for predicting individual income --with all the problematic epistemological/overfitting caveats that they come with. Presenting that graph as an empirical fact and not as a debatable modeling exercise is quite misleading.

Besides, as others have pointed out, all the links you provide discuss income, not wealth (and no, their arguments/reasoning about income do not readily/trivially translate to wealth, as you commented below). If you are interested, check out the work of Cheryl Doss [3], who has conducted actual empirical work about the differences between household and individual equality in Ecuador, Ghana and India.

(PD: Oh wow even their claims about changing family structure in that blog [4] is disturbingly model-dependent. Much is made about the percentage of single-person households following an S-shaped curve, inflecting at 1968. However, they fit a sigmoid to what is a patently linear trend in the total number of single-person households beginning in 1950, and extrapolate back to 1900 despite having only two data points for that period. This wouldn't pass even a cursory peer-review, sorry.)

[1] http://1.bp.blogspot.com/-g3WZGpDibPM/Up3ZAPRtScI/AAAAAAAAJq...

[2] http://www.ecineq.org/ecineq_bari13/FILESxBari13/CR2/p177.pd...

[3] http://www.genderassetgap.org/sites/default/files/Doss%20-%2...

[4] http://politicalcalculations.blogspot.ca/2013/12/the-widows-...

Long story short:

The wealth of non rich Americans is almost entirely contained in their highly leveraged houses. If housing prices collapse, their wealth collapses.

In 2008, housing prices collapsed.

Not exactly. The 25th percentile's wealth was dropping even before the recession, which suggests some additional downward pressure, although I am not sure what that could be off the top of my head.

My suspicion is that it may be due to the inflation adjusted real wage effects, which hit the bottom 25th percentile the hardest, as that is generally their only source of income, and their resulting margin for wealth storage is so much closer. [1] Honestly, real wage income has been flat since about 1965, and for many has been going down since the great recession. [2] And if you only got high school or less, well, you're just boned. [3] (Note, take sources with a grain of salt, as they're 5 minute Google searches)

[1] http://1.bp.blogspot.com/-aGE47oMJAQw/UhZtjjtKorI/AAAAAAAAJz...

[2] http://www.pgpf.org/Chart-Archive/~/~/media/A130E85DDC064B81...

[3] http://www.frbsf.org/wp-content/blogs.dir/1/files/1106bb.gif

That would explain only a slowing in the rate of wealth increase, not a decrease in wealth.

Not necessarily. Everybody has a burn rate for money, as a natural feature of living in a market economy where we do work for pay. At its minima, its the cost to meet Maslow's needs. In the worst version, if our pay goes below the absolute minima, then we'll likely be eating our wealth, looking for other support, going homeless, or dying.

Unfortunately, we also tend to be habit creatures, and our burn rate often stabilizes to our pay and our social class (keeping up with the Jones'). If our real wage starts to go down, then we often have trouble adapting, and keep burning as if we were still at the prior equilibrium (credit card debt, eating into savings, taking out loans).

This is made even worse when the source of real wage reduction is the subtle erosion of our buying power through inflation. We complain about how much things cost, but we still see our paychecks slightly increasing so it seems good, and the burn gets worse.

> some additional downward pressure, although I am not sure what that could be

I'm not an economist, so these are speculative, but seem reasonable based on the fact that we're talking about loss of wealth from households below median:

Loss of life (specifically heads of household) due to the wars (I'm guessing most military households, being young and having maximum education of high school to "some college" will be below median)

Increased energy costs (gas being a marginal cost would hit people with less marginal income harder).

Loss of jobs to automation (I'm thinking secretaries, anything that can be replaced by an iphone, etc)

Declining birth rate (last I heard total high school graduations were supposed to peawould tend to lead to oversaturated teaching jobs, also relatively low-paying.

Chrysler was in distress long before the recession.

Those describe downward pressure on income, not wealth necessarily:

None of these would lead to a decrease in wealth so quickly, except for situations in which the wealth had to be consumed to make up for loss of job / disability / sickness / overconsumption.

Re: Military families: Most people getting killed/dismembered were too young to have any wealth to lose. Even still, their wealth would actually increase upon death as the military's life insurance policies are quite generous.

Wage freezes at nominal values which did not keep pace with inflation during the 2000s, I'd guess.

Converting home equity to consumption is my guess.

Remember HELOCs?

HELOCs are back and bigger than ever!

Home-equity lending surpassed 2009 levels in 2013, with $111 billion in new home equity lines of credit (HELOCs) opened. In the fourth quarter, new lending increased 43% from quarter four 2012, according to data from Experian-Oliver Wyman Market Intelligence Reports and Experian’s IntelliView tool.

http://www.marketwatch.com/story/helocs-made-a-comeback-in-2...

Haha awesome.

Though I imagine that surpassing "2009 levels" is not very exciting. Wake me up when they surpass 2005 levels!

The chart that showed the movements of the various percentiles showed an interesting thing, where in 2003, the 25th percentile's wealth started to drop, while at the exact same time the higher percentile's wealth suddenly went up, before dropping after the recession hit. I have a feeling there's a link

2003 was when the stock market recovered.[1] The wealth of the rich is highly correlated with the stock market.

[1]http://finance.yahoo.com/echarts?s=%5EGSPC+Interactive#symbo...

What's the home ownership rate in the bottom quartile of net worth? The closes I could find was rate for the bottom 90%, which was apparently 66% in 2004.

I don't know. Probably pretty low. Which is why it shouldn't be surprising that so many have zero or near zero wealth.

{kind=link}

{kind=link}

{kind=link}

Project it back a few years, and I'd bet we're poorer on average as a country than we were when I was born. Man, 43% decline for the median? Ouch.

I also like that the mean wealth in America is 6x the median wealth.

Actually, I find the numbers for the 75th+ percentiles a bit surprising, as my mental model had them with significant uptick after about 2011 or so. Kind of a wealth transfer from the lower percentiles. Whereas, this research seems to show that while erosions were smaller for the top (due to their non-real estate growth), no demographic they researched showed overall wealth growth from 2007 on. At best, they've gotten back to zero slope.

I saw a chart a few weeks back depicting this. Starting in the early 80's it started heading downward. I can't find it at the moment, but if I do, I'll post a link.

A lot of factors contribute but housing was one of the major factors. "Net worth" was/is tied directly to their home and the 2006/07 crash. With the government screwing with the markets and investors buying homes as rentals, we just might see another sharp decline shortly...

http://www.zerohedge.com/news/2014-06-24/americas-most-impor...

I didn't read anything about how the increasing numbers of older Americans who are not working might have a significant bearing on the matter.

edit: What I'm saying is, America has a baby-boomer generation that is retiring in droves, more power to them but don't do a study at a major university sounding alarm bells unless an important factor like a massively retiring baby boomer generation is considered.

Here's a problem I have with the definition of "wealth".

My wife in I, who recently finished professional schools, earn (combined) in the top 5%. But because of our student debt, when I do a "wealth" calculator, I'm apparently literally at the bottom of the wealth chart - 0%. Leads me to question:

1. Is College attendance increasing, or decreasing over time?

2. Is price of College attendance increasing, or decreasing over time?

I suspect both increasing. Would that explain some (or most, or all?) of this phenomenon? Average or lower income individuals will mostly go from positive to negative to put themselves through school, while rich or upper class will not. Would be interested how much of the phenomena that would explain.

The wikipedia article on Income inequality in the United States is surprisingly detailed and I highly recommend it if you have any interest on wealth. It's such a polarized topic that the comments almost immediately turn into inaccurate or out of context talking points.

http://en.wikipedia.org/wiki/Income_inequality_in_the_United...

Income and wealth are quite different topics...

The average American is not wealthy. The median net worth is $45K [1], which is below Japan, Canada, Australia and much of Western Europe.

[1] http://money.cnn.com/2014/06/11/news/economy/middle-class-we...

It's depressing how 1/4 households basically have no wealth at all.

If you take a minute to consider the demographics involved and the nature of wealth, it is neither depressing nor surprising nor even "bad".

Consider, for example, that many people have negative wealth.

Consider what factors, and in what way?

Also, whether or not something is depressing, surprising, or bad is entirely subjective. Something you do not consider surprising may in fact be surprising to another individual, so without knowing them it's sort of silly to say "it isn't surprising". If they say it is surprising, it means to them it was. If you do not think others should be surprised, it may be useful for you to explain what knowledge you have that prevented your being surprised.

To be wealthy means that one possesses sufficient wealth (stuff) to live comfortably even after they quite their job.

The bastardized term of "wealth" used here, however, refers simply to material possessions even when not in sufficient quantities to provide any passive lifestyle advantages; suddenly a paid off car worth $5,000 is "wealth." The estimated $30,000 in equity I possess on my $200,000 home is "wealth". It's all a bit frivolous.

By definition, the poor and middle classes don't possess true wealth. Their value is their human capital and time, which they exchange for money. Even the "working rich" - doctors and lawyers - don't routinely possess "wealth" in the traditional sense of the term.

Then we compare the $30,000 equity I possess to actual wealth... such as the land under a shopping mall. What is the use in such an exercise?

NEWS FLASH: People who own really valuable stuff possess really valuable stuff. The rest of us don't. Let's write books about this and study the shocking phenomenon?

You simply can't compare actual wealth - such as the land under a shopping mall, which generates sufficient revenue for many people to live comfortably - to "wealth".

Now, demographically... Why would anyone be surprised that a significant portion of the population has zero wealth? Honestly I'm surprised it's only 25% who have zero. How much "wealth" should a university student have? How about someone who's been working for a few years? How about someone who's been retired for twenty years and expects to die within the next ten?

Middle class people gradually build up a small stock of "wealth" (we used to call this "savings") throughout their working careers. Then after retirement they gradually draw it down until they die.

So yes, it is not surprising that many people have zero or negative wealth.

"Middle class people gradually build up a small stock of "wealth"" That's part of the point. As the chart in this study shows, the middle class is not building anything. In fact, it's declining.

I wonder if a large cohort of middle class individuals have recently retired.

The Socialist Revolution is coming?